Introduction

According to recent data, India’s total exports reached $413.30 billion between April and September 2025, up 4.45% from $395.71 billion in the same period last year. This indicates more Indian businesses are now getting paid by global clients.

If you're working with American customers, you've likely come across the term "ABA number" on payment forms. So, what exactly is the full form of ABA, and how does the ABA routing number work?

In this guide, we cover everything you need to know about ABA, including how it works, how to find it, how it compares to other common banking codes, and more. Let’s get started.

Key Takeaways

- ABA stands for American Bankers Association: It is the organization that created the routing number system to identify US financial institutions.

- ABA routing numbers are nine-digit codes: They identify specific banks for domestic transactions like wire transfers, direct deposits, and electronic payments.

- You need ABA numbers for US payments: When receiving money from US clients, platforms, or businesses, you'll need the correct ABA routing number along with your account details.

- ABA numbers appear on checks: You can find them on the bottom left corner of US checks, along with account numbers.

- PayGlocal simplifies global payment collection: Instead of managing ABA numbers and wire instructions, you can collect payments directly with local US accounts in USD and settle in INR.

What is the Full Form of ABA?

ABA stands for American Bankers Association. This organization developed the ABA routing number system to make check processing more organized across US banks.

An ABA routing number is a nine-digit code printed on checks and used in electronic transactions. It tells the payment system which specific bank or credit union should receive or send the money. Each financial institution in the United States has at least one unique ABA number.

For example, if you're receiving a wire transfer from a US client, they'll need your bank's ABA routing number along with your account number to complete the transaction. Without the correct ABA number, the payment won't reach your account.

The American Bankers Association still manages this system today, even though most transactions now happen electronically rather than through paper checks.

How Does an ABA Routing Number Work?

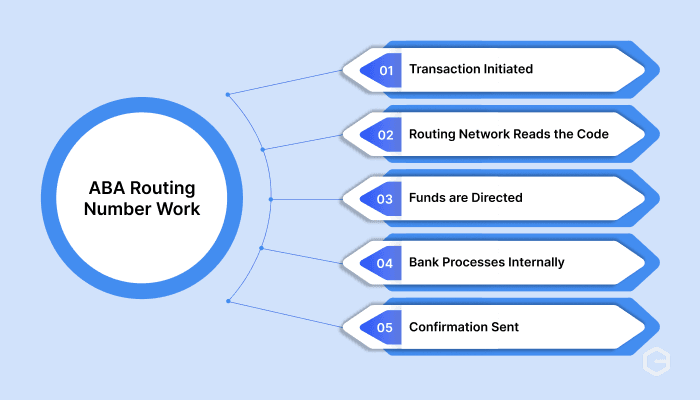

When someone initiates a payment in the US banking system, the ABA routing number acts like an address for the receiving bank. The payment network reads this nine-digit code to identify where the money should go.

Here's what happens during a typical transaction:

Step 1 - Transaction initiated: A client enters your ABA routing number and account number to send you money through their bank.

Step 2 - Routing network reads the code: The payment system identifies which bank the ABA number belongs to using a central database.

Step 3 - Funds are directed: The system routes the payment to the correct financial institution based on the ABA number.

Step 4 - Bank processes internally: Your bank receives the payment and credits it to your specific account using the account number.

Step 5 - Confirmation sent: Both sender and receiver get confirmation that the transaction completed successfully.

The entire process usually takes one to three business days for standard transfers, though wire transfers can be completed on the same day.

How to Find an ABA Routing Number?

You can locate ABA routing numbers in several places depending on your situation.

- On a check: Look at the bottom left corner of any US check. The first nine digits you see are the ABA routing number. The longer number next to it is the account number.

- Bank website: Most US banks list their routing numbers on their websites, usually in the FAQ or support section. You can search for "[bank name] routing number" to find it quickly.

- Bank statement: Your monthly or quarterly bank statement typically shows the routing number at the top or in the account details section.

- Online banking portal: Log into your online banking account and look for account details or direct deposit information. The routing number appears there.

- Bank's mobile app: Many banking apps show your routing number when you tap on account details or information sections.

* Contact the bank: Call your bank's customer service or visit a branch to ask directly. Have your account number ready for verification.

What is the Difference Between ABA and SWIFT Code?

ABA numbers handle domestic US transactions, while SWIFT codes manage international transfers between countries.

A SWIFT code (also called a BIC code) is an 8–11 character code that identifies banks worldwide. When you receive payments from the US to India, your client might need both their bank's ABA number (for the US side) and your bank's SWIFT code (for the international portion).

The main difference between the two is that the ABA number only works within the United States banking system, whereas SWIFT code works globally across different countries and currencies.

Example: When a US client sends you an international wire transfer to India, their bank uses the ABA number to process the payment locally first. Then the payment moves internationally using SWIFT codes to reach your Indian bank account.

When Do You Need an ABA Routing Number?

You need ABA routing numbers in specific situations when dealing with US payments.

- Receiving wire transfers from US clients: When a US business or individual sends you money via wire transfer, they need your bank's ABA routing number. This applies to both domestic US accounts and sometimes international transfers originating in the US.

- Setting up direct deposits: If you work with US platforms or employers who pay via direct deposit, you'll provide an ABA routing number along with your account number.

- Accepting ACH payments: For recurring payments from US clients, ACH transfers require the correct routing number to process automatically.

- US marketplace payouts: Platforms like Upwork, Fiverr, or Amazon that operate in the US might request ABA routing information for certain payout methods.

- Opening US bank accounts: If you establish a US business bank account to receive payments locally, you'll get an ABA routing number assigned to that account.

Common Mistakes to Avoid with ABA Routing Numbers

Getting your ABA routing number wrong can cause serious payment delays. Here are mistakes to watch out for:

- Using the wrong routing number type: Your bank might have different ABA numbers for wire transfers versus ACH payments. Always confirm which type your client needs to use.

- Confusing routing number with account number: The routing number identifies the bank, while the account number identifies your specific account. Mixing these up sends payments to the wrong place.

- Using old routing numbers after bank mergers: When banks merge or change names, routing numbers sometimes change. Verify you're using the current number.

- Assuming all branches share one routing number: Larger banks might use different routing numbers for different states or regions. Check which routing number applies to your specific account.

- Not verifying information with clients: When a US client asks for your banking details, provide clear instructions about which routing number they should use for their payment method.

- Forgetting to update payment platforms: If you change banks or accounts, remember to update your routing number on all platforms where you receive payments.

Get Paid Globally in Multiple Currencies Easily with PayGlocal

Dealing with ABA routing numbers, wire transfer fees, and international payment delays adds unnecessary friction to your business operations. You need a simpler way to collect from US clients without the traditional payment complexities.

PayGlocal removes these challenges by giving you local payment collection options in the US and other countries. Your international clients pay you the same way they pay local businesses, while you receive your money in INR directly.

Here's what you get:

- Multi-currency collection: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD.

- Dynamic checkout options: Accept payments through various methods, including cards and local payment options that your clients prefer.

- Zero fixed costs: Pay only when you do the transactions. No monthly fees, no setup charges, no documentation fees.

- Recurring payments made simple: Set up automatic billing for subscriptions and retainers without chasing clients each month for payments.

- One platform for everything: Manage all your international payments, view reports, and handle settlements from a single dashboard instead of juggling multiple tools.

Instead of explaining complex payment processes to every new client and waiting for international transfers to clear, PayGlocal offers all the payment collection options just like a local business in the US.

Final Thoughts

ABA stands for American Bankers Association, and ABA routing numbers are the nine-digit codes that identify US banks for domestic transactions. You need these numbers when receiving wire transfers, direct deposits, or ACH payments from US clients.

While ABA routing numbers serve an important purpose in the US banking system, managing them along with international wire transfers can create unnecessary complexity for your business. The good news is you don't have to deal with this friction anymore.

Modern payment solutions like PayGlocal simplify international payment collection by giving you local banking options in major currencies. Your US clients pay you like you're a local business, and you receive settlements in INR without any complex process.

Ready to make your international payments faster, smoother, and more secure? Get started with PayGlocal today.