The global payments industry continues expanding rapidly, with the market size rising from $716.31 billion in 2024 to $1.12 trillion by 2029. This growth brings more payment options but also increases complexity around currency conversion costs.

International business transactions come with many hidden costs that can eat into your profit margins. Among these costs, forex charges stand out as one of the most significant yet overlooked expenses that businesses face when dealing with global payments.

In this guide, we break down everything you need to know about forex charges, why they exist, and effective strategies to reduce or avoid them entirely.

* Currency Conversion Fees: Forex charges are fees implemented when converting one currency to another during international transactions.

* Cost Coverage: Payment platforms charge forex fees to cover currency conversion costs, market volatility risks, and operational expenses.

* Cost-Effective Solutions: PayGlocal offers transparent pricing and competitive rates to help businesses reduce forex-related costs.

* Strategic Payment Methods: Multi-currency accounts and local payment methods are effective strategies to minimize currency conversion fees.

Forex charges, also known as foreign exchange fees or currency conversion charges, are costs imposed when money is converted from one currency to another during international transactions. These fees apply whenever you send, receive, or process payments in a currency different from your base currency.

When you make an international payment, your bank or payment provider needs to convert your local currency into the recipient's currency. This conversion process involves accessing foreign exchange markets, managing currency fluctuations, and handling the administrative work required for cross-border transactions.

For instance, if you're an Indian exporter receiving payment in US dollars, your payment processor will convert those dollars to Indian rupees. The difference between the market exchange rate and the rate you actually receive, plus any additional fees, constitutes your forex charges. These costs can vary significantly depending on your payment method, provider, and transaction amount.

Payment platforms and financial institutions charge forex fees to cover the costs and risks associated with currency conversion and international money transfers.

Here's why these charges exist across the payment industry:

* Market Access Costs: Payment providers need to access foreign exchange markets and maintain relationships with multiple banks globally to facilitate currency conversions.

* Exchange Rate Fluctuations: Currency values change constantly throughout the day, creating risk for payment processors who need to hedge against potential losses from rate movements.

* Compliance Requirements: International transactions require adherence to various regulatory frameworks, anti-money laundering checks, and reporting requirements in different countries.

* Infrastructure Maintenance: Managing global payment networks, security systems, and 24/7 customer support across multiple time zones requires significant operational investment.

* Liquidity Management: Payment platforms must maintain sufficient funds in various currencies to process transactions quickly and efficiently.

* Risk Management: Cross-border payments carry higher risks of fraud, chargebacks, and regulatory issues compared to domestic transactions.

Forex charges work through a combination of exchange rate markups and fixed fees applied during currency conversion processes.

When you initiate an international transaction, your payment provider accesses the interbank exchange rate, which is the wholesale rate banks use to trade currencies with each other. However, you don't receive this preferential rate. Instead, providers apply a markup that typically ranges from 0.5% to 4% above the interbank rate.

The conversion process involves several steps that generate costs. Your provider checks current exchange rates from multiple sources, applies a percentage markup to cover operational costs and profit margins, and then adds any additional fixed fees based on your payment method.

For example, if the interbank rate for USD to INR is 83.00, your payment provider might offer you a rate of 82.00, keeping the 1.00 difference as their markup. On a $10,000 transaction, this 1.2% markup would cost you ₹10,000 in forex charges alone.

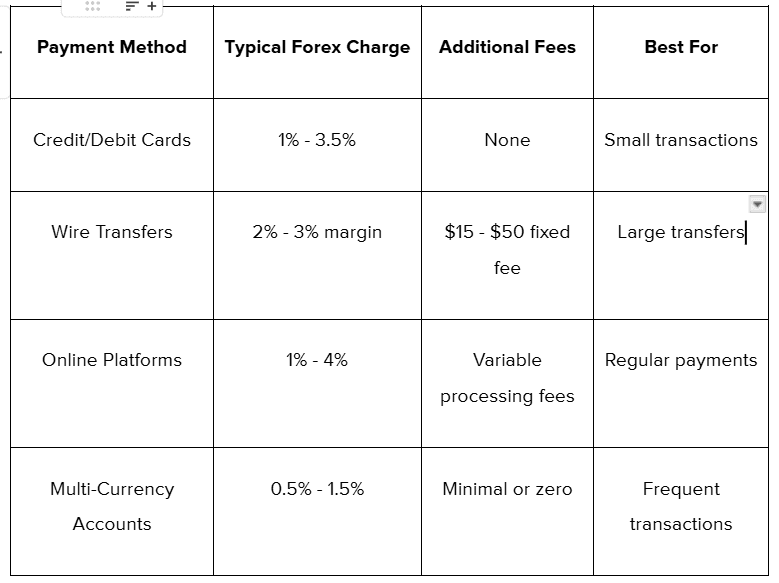

Payment methods carry different fee structures for international transactions. Here's a quick comparison of forex charges across different payment methods:

Each payment type has specific characteristics that affect your total transaction costs:

Card processing for international transactions typically involves the highest forex charges among payment methods. Credit card companies and banks impose foreign transaction fees that range from 1% to 3.5% of the transaction amount.

These charges occur automatically when you use your card for purchases in foreign currencies or on international websites. Even if the merchant displays prices in your local currency, the transaction might still trigger forex fees if the business is based overseas.

Many premium credit cards waive foreign transaction fees as a benefit, but standard cards typically charge between 2.5% to 3% per transaction. Debit cards often have similar fee structures, though some banks offer lower rates for certain account types.

Traditional wire transfers through banks involve exchange rate margins plus fixed transfer fees. Banks typically offer exchange rates that are 2% to 4% worse than interbank rates, which serve as their primary profit source for international transfers.

Additionally, banks charge fixed fees ranging from $15 to $50 per wire transfer, regardless of the amount. For smaller transactions, these fixed fees can represent a significant percentage of your total transfer value.

SWIFT charges may also apply for international wire transfers, adding another layer of costs to traditional banking methods.

Digital payment platforms and money transfer services offer varying fee structures for currency conversion. Some platforms charge fixed fees plus exchange rate markups, while others use transparent pricing models.

PayPal, for instance, charges a currency conversion fee of up to 4% above the base exchange rate for international transactions. Other platforms may offer more competitive rates but include higher fixed fees or monthly subscription costs.

Multi-currency accounts allow you to hold funds in multiple currencies, reducing the need for frequent conversions. However, when conversions are necessary, these accounts typically charge lower fees than traditional methods.

Some providers offer free conversions up to certain limits, while others charge minimal fees ranging from 0.5% to 1.5%. The key advantage is timing control. You can convert currencies when rates are favorable rather than being forced to convert at the moment of transaction.

Smart currency management strategies can significantly reduce your international transaction costs. Here are some effective methods to minimize or avoid forex charges entirely:

* Use Multi-Currency Business Accounts: Maintain balances in currencies you frequently transact in to avoid conversion fees on every transaction.

* Choose No-Fee Credit Cards: Select business credit cards that waive foreign transaction fees for international purchases and payments.

* Use Local Payment Methods: Accept payments through local banking networks in your customers' countries to eliminate cross-border conversion costs.

* Time Your Currency Conversions: Monitor exchange rates and convert larger amounts when rates are favorable rather than converting small amounts frequently.

* Compare Provider Exchange Rates: Research different payment providers' exchange rates and fee structures before committing to international transactions.

International payment fees can drain your business profits through hidden charges and poor exchange rates. Many payment providers lack transparency in their pricing, making it difficult for businesses to predict and control their cross-border transaction costs.

PayGlocal solves these challenges with a comprehensive payment solution designed specifically for businesses handling international transactions.

Here's how PayGlocal helps you save money on global payments:

* Low-Cost Multi-Currency Accounts: Hold funds in multiple currencies including USD, GBP, EUR, and CAD, at just 0.75% transaction fees, significantly lower than traditional banking options.

* Competitive Card Processing Rates: Process international card payments at 3-3.5% with no hidden markups or surprise charges on your transactions.

* 40+ Local Payment Methods: Accept payments through global payment methods, including local banking networks, to eliminate cross-border conversion fees entirely.

* Cost-Effective Recurring Billing: Set up recurring payments for subscriptions and repeat transactions without additional forex markup costs.

* Multiple Payment Options: Offer customers various payment choices through dynamic checkout, including cards and local methods, allowing them to select the most cost-effective option and avoid high forex fees.

PayGlocal is particularly valuable for exporters, freelancers, and e-commerce businesses that regularly handle international transactions and need predictable, cost-effective payment processing.

Forex charges are worth considering in international business transactions, but they don't have to drain your profits. Knowing about how these fees work and implementing smart strategies can help you reduce costs substantially.

The key is choosing the right combination of payment methods, timing your currency conversions strategically, and working with providers who offer transparent pricing. Multi-currency accounts and local payment methods can all contribute to lower overall transaction costs.

PayGlocal provides businesses with the tools and competitive rates needed to minimize forex charges while maintaining efficient international payment processing. Get started with transparent pricing and start saving on your global transactions today.

Most payment providers charge between 1% to 4% for currency conversion. The exact rate depends on your payment method and transaction volume.

Multi-currency accounts typically offer the lowest rates at 0.5% to 1.5%. Local payment networks often have zero conversion fees.

Banks add 2% to 3% markup to market exchange rates plus fixed fees. Wire transfers typically cost $15-$50 in additional charges per transaction.

No, specialized international payment providers often offer competitive or zero forex charges. Compare providers to find the best rates for your needs.

International business transactions come with many hidden costs that can eat into your profit margins. Among these costs, forex charges stand out as one of the most significant yet overlooked expenses that businesses face when dealing with global payments.

In this guide, we break down everything you need to know about forex charges, why they exist, and effective strategies to reduce or avoid them entirely.

Key Takeaways:

* Currency Conversion Fees: Forex charges are fees implemented when converting one currency to another during international transactions.

* Cost Coverage: Payment platforms charge forex fees to cover currency conversion costs, market volatility risks, and operational expenses.

* Cost-Effective Solutions: PayGlocal offers transparent pricing and competitive rates to help businesses reduce forex-related costs.

* Strategic Payment Methods: Multi-currency accounts and local payment methods are effective strategies to minimize currency conversion fees.

What are Forex Charges?

Forex charges, also known as foreign exchange fees or currency conversion charges, are costs imposed when money is converted from one currency to another during international transactions. These fees apply whenever you send, receive, or process payments in a currency different from your base currency.

When you make an international payment, your bank or payment provider needs to convert your local currency into the recipient's currency. This conversion process involves accessing foreign exchange markets, managing currency fluctuations, and handling the administrative work required for cross-border transactions.

For instance, if you're an Indian exporter receiving payment in US dollars, your payment processor will convert those dollars to Indian rupees. The difference between the market exchange rate and the rate you actually receive, plus any additional fees, constitutes your forex charges. These costs can vary significantly depending on your payment method, provider, and transaction amount.

Why Do Payment Platforms Charge Forex Fees?

Payment platforms and financial institutions charge forex fees to cover the costs and risks associated with currency conversion and international money transfers.

Here's why these charges exist across the payment industry:

* Market Access Costs: Payment providers need to access foreign exchange markets and maintain relationships with multiple banks globally to facilitate currency conversions.

* Exchange Rate Fluctuations: Currency values change constantly throughout the day, creating risk for payment processors who need to hedge against potential losses from rate movements.

* Compliance Requirements: International transactions require adherence to various regulatory frameworks, anti-money laundering checks, and reporting requirements in different countries.

* Infrastructure Maintenance: Managing global payment networks, security systems, and 24/7 customer support across multiple time zones requires significant operational investment.

* Liquidity Management: Payment platforms must maintain sufficient funds in various currencies to process transactions quickly and efficiently.

* Risk Management: Cross-border payments carry higher risks of fraud, chargebacks, and regulatory issues compared to domestic transactions.

How Does Forex Charge Work?

Forex charges work through a combination of exchange rate markups and fixed fees applied during currency conversion processes.

When you initiate an international transaction, your payment provider accesses the interbank exchange rate, which is the wholesale rate banks use to trade currencies with each other. However, you don't receive this preferential rate. Instead, providers apply a markup that typically ranges from 0.5% to 4% above the interbank rate.

The conversion process involves several steps that generate costs. Your provider checks current exchange rates from multiple sources, applies a percentage markup to cover operational costs and profit margins, and then adds any additional fixed fees based on your payment method.

For example, if the interbank rate for USD to INR is 83.00, your payment provider might offer you a rate of 82.00, keeping the 1.00 difference as their markup. On a $10,000 transaction, this 1.2% markup would cost you ₹10,000 in forex charges alone.

What Are the Different Types of Forex Charges?

Payment methods carry different fee structures for international transactions. Here's a quick comparison of forex charges across different payment methods:

Each payment type has specific characteristics that affect your total transaction costs:

1. Credit and Debit Card Forex Fees

Card processing for international transactions typically involves the highest forex charges among payment methods. Credit card companies and banks impose foreign transaction fees that range from 1% to 3.5% of the transaction amount.

These charges occur automatically when you use your card for purchases in foreign currencies or on international websites. Even if the merchant displays prices in your local currency, the transaction might still trigger forex fees if the business is based overseas.

Many premium credit cards waive foreign transaction fees as a benefit, but standard cards typically charge between 2.5% to 3% per transaction. Debit cards often have similar fee structures, though some banks offer lower rates for certain account types.

2. Wire Transfer Exchange Margins

Traditional wire transfers through banks involve exchange rate margins plus fixed transfer fees. Banks typically offer exchange rates that are 2% to 4% worse than interbank rates, which serve as their primary profit source for international transfers.

Additionally, banks charge fixed fees ranging from $15 to $50 per wire transfer, regardless of the amount. For smaller transactions, these fixed fees can represent a significant percentage of your total transfer value.

SWIFT charges may also apply for international wire transfers, adding another layer of costs to traditional banking methods.

3. Online Payment Platform Markups

Digital payment platforms and money transfer services offer varying fee structures for currency conversion. Some platforms charge fixed fees plus exchange rate markups, while others use transparent pricing models.

PayPal, for instance, charges a currency conversion fee of up to 4% above the base exchange rate for international transactions. Other platforms may offer more competitive rates but include higher fixed fees or monthly subscription costs.

4. Multi-Currency Account Conversion Fees

Multi-currency accounts allow you to hold funds in multiple currencies, reducing the need for frequent conversions. However, when conversions are necessary, these accounts typically charge lower fees than traditional methods.

Some providers offer free conversions up to certain limits, while others charge minimal fees ranging from 0.5% to 1.5%. The key advantage is timing control. You can convert currencies when rates are favorable rather than being forced to convert at the moment of transaction.

What Are the Best Practices and Tips to Avoid Forex Charges?

Smart currency management strategies can significantly reduce your international transaction costs. Here are some effective methods to minimize or avoid forex charges entirely:

* Use Multi-Currency Business Accounts: Maintain balances in currencies you frequently transact in to avoid conversion fees on every transaction.

* Choose No-Fee Credit Cards: Select business credit cards that waive foreign transaction fees for international purchases and payments.

* Use Local Payment Methods: Accept payments through local banking networks in your customers' countries to eliminate cross-border conversion costs.

* Time Your Currency Conversions: Monitor exchange rates and convert larger amounts when rates are favorable rather than converting small amounts frequently.

* Compare Provider Exchange Rates: Research different payment providers' exchange rates and fee structures before committing to international transactions.

Save on Every International Transaction with PayGlocal

International payment fees can drain your business profits through hidden charges and poor exchange rates. Many payment providers lack transparency in their pricing, making it difficult for businesses to predict and control their cross-border transaction costs.

PayGlocal solves these challenges with a comprehensive payment solution designed specifically for businesses handling international transactions.

Here's how PayGlocal helps you save money on global payments:

* Low-Cost Multi-Currency Accounts: Hold funds in multiple currencies including USD, GBP, EUR, and CAD, at just 0.75% transaction fees, significantly lower than traditional banking options.

* Competitive Card Processing Rates: Process international card payments at 3-3.5% with no hidden markups or surprise charges on your transactions.

* 40+ Local Payment Methods: Accept payments through global payment methods, including local banking networks, to eliminate cross-border conversion fees entirely.

* Cost-Effective Recurring Billing: Set up recurring payments for subscriptions and repeat transactions without additional forex markup costs.

* Multiple Payment Options: Offer customers various payment choices through dynamic checkout, including cards and local methods, allowing them to select the most cost-effective option and avoid high forex fees.

PayGlocal is particularly valuable for exporters, freelancers, and e-commerce businesses that regularly handle international transactions and need predictable, cost-effective payment processing.

Final Thoughts

Forex charges are worth considering in international business transactions, but they don't have to drain your profits. Knowing about how these fees work and implementing smart strategies can help you reduce costs substantially.

The key is choosing the right combination of payment methods, timing your currency conversions strategically, and working with providers who offer transparent pricing. Multi-currency accounts and local payment methods can all contribute to lower overall transaction costs.

PayGlocal provides businesses with the tools and competitive rates needed to minimize forex charges while maintaining efficient international payment processing. Get started with transparent pricing and start saving on your global transactions today.

FAQs

1. What is the average forex charge percentage for international transactions?

Most payment providers charge between 1% to 4% for currency conversion. The exact rate depends on your payment method and transaction volume.

2. Which payment method has the lowest forex charges?

Multi-currency accounts typically offer the lowest rates at 0.5% to 1.5%. Local payment networks often have zero conversion fees.

3. How do banks calculate forex charges on wire transfers?

Banks add 2% to 3% markup to market exchange rates plus fixed fees. Wire transfers typically cost $15-$50 in additional charges per transaction.

4. Do all payment providers charge forex fees?

No, specialized international payment providers often offer competitive or zero forex charges. Compare providers to find the best rates for your needs.