As your business grows and you take on more clients, the cost of collecting payments grows with it. Bank transfer fees, currency conversion charges, and the hours your team spends on manual processing all eat into your profit margins.

B2B payment gateways reduce these costs by handling transactions digitally with transparent pricing. Data shows that 35% of businesses flag high processing costs as a top challenge with traditional payment methods. The longer you stay on outdated systems, the more you pay for every invoice collected.

This guide breaks down in detail what B2B payment gateways are, their benefits, and how to choose and set one up for your business.

A B2B payment gateway is a digital platform that helps one business collect payments from another business. It sits between the buyer and your bank, handling the transaction securely so funds reach your account.

For instance, if your SaaS company bills a client in the UK every month, the gateway processes their card payment, converts the currency if needed, and deposits the amount into your account. You do not need to send manual invoices or chase wire transfers.

Unlike consumer payment setups, B2B gateways handle larger transaction amounts, recurring billing cycles, and often support payment methods like bank transfers and standing instructions alongside cards.

Switching from manual collection to a gateway changes how your finance team works day to day. The impact goes beyond just receiving money faster. Here are some of the main benefits you get.

The right gateway turns payment collection from a bottleneck into a smooth payment process. Your team spends less time chasing payments and more time on the work that grows the business.

B2B payment gateways are not limited to one type of business. Companies across industries use them to solve different payment collection problems depending on their clients, billing cycles, and markets.

Here’s how some of the most common industries put them to work.

Tip: Before choosing a B2B gateway, map out your top 5-10 clients by location and payment method. This tells you exactly which features you need most.

The process looks different depending on the provider, but the core steps are the same across most platforms. Here’s what happens when a business client makes a payment through your gateway.

1. Buyer starts the payment: Your client clicks a payment link, lands on your checkout page, or gets an automated invoice with a pay button.

2. Gateway collects payment details: The gateway securely captures the buyer's card number, bank details, or chosen payment method.

3. Payment is verified and authorized: The gateway checks the transaction with the buyer's bank or card network. Fraud checks and payment tokenization also happen at this step.

4. Funds are settled to your account: Once approved, the money moves to your business account. Settlement timelines vary by provider and method.

5. Records are updated automatically: The gateway logs the transaction, updates your dashboard, and sends confirmations to both sides.

Tip: Look for gateways that show real-time payment status updates. Knowing where your money is at every step saves your finance team hours of follow-up work.

When choosing the right B2B payment gateway, it is essential to match the platform to how your business actually operates. Some of the top things to evaluate before you decide on the right gateway:

Check which payment methods the gateway supports. If your clients pay by card, bank transfer, and UPI, you need a platform that handles all three.

For instance, a gateway that only supports cards will not help if half your clients prefer wire transfers. Start with your current client list and map out how they pay today.

If you sell to businesses in other countries, your gateway needs to accept payments in their local currency. A buyer in the US should be able to pay in USD, not be forced to convert to INR first.

Look for gateways that support collection in currencies like USD, GBP, EUR, and CAD. Multi-currency accounts that let you receive funds locally in those markets reduce transaction fees and payment failures.

Your gateway should connect to your existing website, billing tool, or ERP without heavy development work. Most modern gateways offer APIs, plugins for platforms like Shopify and WooCommerce, and even no-code options.

Ask how long the setup takes. Some platforms get you live in days. Others need weeks of technical work.

B2B transactions are often large in value, which makes them targets for fraud. Your gateway should include encryption, two-factor authentication, and a fraud screening engine that catches suspicious activity without blocking real clients.

For example, a good fraud engine checks device data, location, and card history in real time. This protects your revenue without adding friction for genuine buyers.

Gateway pricing usually includes a percentage fee per transaction and sometimes a fixed fee on top. Some providers charge setup fees, monthly platform fees, or hidden currency conversion markups.

Look for transparent pricing with no fixed costs. Pay-per-transaction models work best for growing businesses because you only pay when money actually comes in.

Tip: Ask providers for a pricing breakdown specific to your transaction volume and currencies. Standard rates on a website may not reflect what you actually pay.

Once you have picked a gateway, getting live does not need to be complicated. Most platforms follow a similar setup process, and with the right preparation, you can start collecting payments within days.

Here are the steps to go from sign-up to your first transaction:

Start by matching the gateway to your actual needs. List the countries your clients are in, the currencies they pay in, and the payment methods they prefer. Then check which providers support all three.

For instance, if you export services to the US and UK, you need a gateway that accepts USD and GBP through cards, bank transfers, and ideally local payment methods. Do not pick a provider just because it is popular. Pick one that fits your payment flow.

Most gateways require a merchant account, which is the account where your funds get settled. Some providers bundle this into their onboarding, so you do not need a separate application.

During this step, you will submit business documents like your registration certificate and bank details. Keep these ready to avoid delays.

Integration depends on your setup. If you run a Shopify or WooCommerce store, most gateways offer ready-made plugins you can install in minutes. For custom websites or apps, you will use the gateway's API.

For example, if your billing system sends invoices by email, you can integrate payment links so clients can pay directly from the invoice. No separate checkout page needed.

Once connected, set up the payment methods and currencies you want to accept. Turn on the ones your clients use most and disable the rest to keep your checkout clean.

If you serve clients in multiple countries, enable multi-currency collection so each buyer sees prices and pays in their own currency. This reduces confusion and lowers payment drop-offs.

Run test transactions using the gateway's sandbox or test mode before going live. Check that the payments process correctly, confirmations are sent, and funds appear in your dashboard.

After launch, monitor your first few weeks closely. Track success rates, failed payments, and settlement timelines. If something looks off, flag it with your provider early.

Tip: Most payment issues show up in the first 30 days. Set a reminder to review your gateway performance after the first month and adjust settings if needed.

Even after setting up a gateway, some problems show up once you start processing real transactions. Knowing these early helps you pick a provider that handles them well. Here are the most common issues businesses run into:

International card payments fail more often than domestic ones. Issues like incorrect card messaging, missing authentication protocols, or poor routing cause declines even when the buyer has funds.

For example, a valid Visa card from the UK might get declined if your gateway does not send the right data to the issuing bank. High failure rates mean lost revenue, frustrated clients, and a higher risk of chargeback disputes.

Some gateways only support a few card networks or one type of bank transfer. If your client in Germany prefers SEPA or your buyer in the UAE uses a local wallet, a limited gateway will not work.

The fix is choosing a platform with a wide range of global payment methods so your clients can pay the way they prefer.

If your gateway does not auto-match incoming payments with invoices, your team ends up doing reconciliation by hand. This is slow, error-prone, and gets worse as transaction volume grows.

Look for platforms that offer real-time dashboards, downloadable reports, and automatic settlement tracking.

Tip: Payment challenges grow as your business scales. A gateway that works for 10 transactions a month may struggle at 500. Choose one built for the volume you are growing towards.

B2B and B2C payments both move money digitally, but the way they work is quite different. If your gateway was built for consumer checkout, it may not handle B2B needs well. Here is how they compare:

If your business sells to other businesses, pick a gateway designed for B2B workflows. Consumer-focused platforms often lack support for invoicing, recurring mandates, and the multi-currency setups that B2B sellers need.

Collecting payments from business clients in other countries comes with extra friction. Card declines, currency conversion losses, missing compliance documents, and limited payment options slow down your cash flow and frustrate your clients.

PayGlocal is built to solve these exact problems for businesses selling globally. Here’s what you get.

No setup fees. No monthly retainers. No hidden documentation costs. We only win when you get paid. Get your cross-border B2B payments moving with a partner that knows the trenches.

A B2B payment gateway is no longer optional. If your business collects payments from other companies, especially across borders, the right gateway saves you time, reduces failed payments, and gives your finance team clear visibility over every transaction.

Start by listing how your clients pay today, where they are located, and what volume you expect over the next year. Then match those needs to a gateway that supports your payment methods, currencies, and growth plans.

Businesses that set this up early collect faster, lose fewer deals to payment friction, and scale with confidence. PayGlocal is helping Indian businesses do exactly that, with support for multi-currency acceptance, global payment methods, and zero fixed costs. Get started with PayGlocal today.

B2B payment gateways reduce these costs by handling transactions digitally with transparent pricing. Data shows that 35% of businesses flag high processing costs as a top challenge with traditional payment methods. The longer you stay on outdated systems, the more you pay for every invoice collected.

This guide breaks down in detail what B2B payment gateways are, their benefits, and how to choose and set one up for your business.

Key takeaways

- B2B payment gateways: They are digital platforms that help businesses collect and process payments from other businesses securely and automatically.

- How they work: A gateway connects your checkout or invoice to the buyer's bank or card network, processes the payment, and settles funds to your account.

- Key benefits: Faster collections, fewer errors, better cash flow visibility, and the ability to accept payments from clients worldwide.

- Cross-border matters: If you sell globally, your gateway needs multi-currency support and local payment methods, supported by platforms like PayGlocal.

- Choosing the right one: Look at payment method coverage, cross-border support, integration options, fraud protection, and pricing.

What is a B2B payment gateway?

A B2B payment gateway is a digital platform that helps one business collect payments from another business. It sits between the buyer and your bank, handling the transaction securely so funds reach your account.

For instance, if your SaaS company bills a client in the UK every month, the gateway processes their card payment, converts the currency if needed, and deposits the amount into your account. You do not need to send manual invoices or chase wire transfers.

Unlike consumer payment setups, B2B gateways handle larger transaction amounts, recurring billing cycles, and often support payment methods like bank transfers and standing instructions alongside cards.

What are the benefits of using a B2B payment gateway?

Switching from manual collection to a gateway changes how your finance team works day to day. The impact goes beyond just receiving money faster. Here are some of the main benefits you get.

- Faster payment collection: Clients pay through a link or checkout in minutes, not days. No more waiting for bank confirmations or check clearances.

- Fewer payment failures: Gateways use smart routing and retry logic to push through transactions that would otherwise fail at the first attempt.

- Better cash flow visibility: Your dashboard shows pending, completed, and failed payments in real time. You always know where your money stands.

- Less manual work: Automatic invoicing, payment matching, and settlement tracking replace spreadsheets and email follow-ups.

- Global reach: Accept payments from clients in other countries using their preferred local payment methods and currencies.

- Built-in security: Encryption, fraud detection, and authentication protocols protect every transaction without extra setup on your end.

The right gateway turns payment collection from a bottleneck into a smooth payment process. Your team spends less time chasing payments and more time on the work that grows the business.

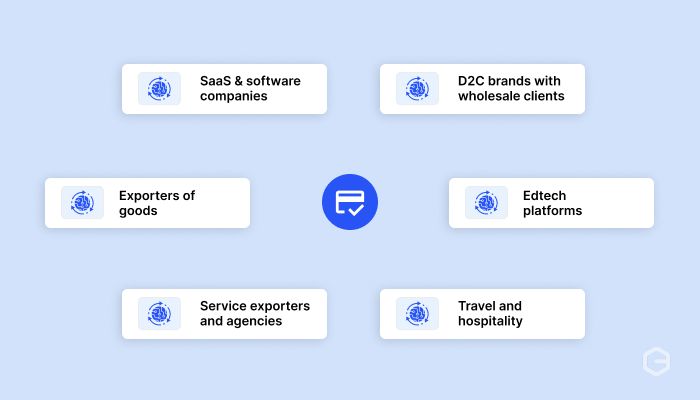

How do different industries use B2B payment gateways?

B2B payment gateways are not limited to one type of business. Companies across industries use them to solve different payment collection problems depending on their clients, billing cycles, and markets.

Here’s how some of the most common industries put them to work.

- SaaS and software companies: Collect monthly or annual subscription fees from global clients using recurring card payments and standing instructions.

- Exporters of goods: Receive payments from international buyers in their local currency through multi-currency accounts, avoiding costly wire transfer delays.

- Service exporters and agencies: Send payment links after project milestones and collect from clients in the US, UK, or Europe without chasing bank transfers.

- Travel and hospitality: Process high-volume international bookings with real-time fraud screening and higher approval rates on cross-border cards.

- Edtech platforms: Bill parents and students in different countries for courses and classes, with automated recurring charges that reduce drop-offs.

- D2C brands with wholesale clients: Manage bulk orders and invoiced payments from retail partners across markets through a single payment dashboard.

Tip: Before choosing a B2B gateway, map out your top 5-10 clients by location and payment method. This tells you exactly which features you need most.

How does a B2B payment gateway work?

The process looks different depending on the provider, but the core steps are the same across most platforms. Here’s what happens when a business client makes a payment through your gateway.

1. Buyer starts the payment: Your client clicks a payment link, lands on your checkout page, or gets an automated invoice with a pay button.

2. Gateway collects payment details: The gateway securely captures the buyer's card number, bank details, or chosen payment method.

3. Payment is verified and authorized: The gateway checks the transaction with the buyer's bank or card network. Fraud checks and payment tokenization also happen at this step.

4. Funds are settled to your account: Once approved, the money moves to your business account. Settlement timelines vary by provider and method.

5. Records are updated automatically: The gateway logs the transaction, updates your dashboard, and sends confirmations to both sides.

Tip: Look for gateways that show real-time payment status updates. Knowing where your money is at every step saves your finance team hours of follow-up work.

How to choose the right B2B payment gateway?

When choosing the right B2B payment gateway, it is essential to match the platform to how your business actually operates. Some of the top things to evaluate before you decide on the right gateway:

1. Payment method support

Check which payment methods the gateway supports. If your clients pay by card, bank transfer, and UPI, you need a platform that handles all three.

For instance, a gateway that only supports cards will not help if half your clients prefer wire transfers. Start with your current client list and map out how they pay today.

2. Cross-border and multi-currency capability

If you sell to businesses in other countries, your gateway needs to accept payments in their local currency. A buyer in the US should be able to pay in USD, not be forced to convert to INR first.

Look for gateways that support collection in currencies like USD, GBP, EUR, and CAD. Multi-currency accounts that let you receive funds locally in those markets reduce transaction fees and payment failures.

3. Integration and setup

Your gateway should connect to your existing website, billing tool, or ERP without heavy development work. Most modern gateways offer APIs, plugins for platforms like Shopify and WooCommerce, and even no-code options.

Ask how long the setup takes. Some platforms get you live in days. Others need weeks of technical work.

4. Security and fraud protection

B2B transactions are often large in value, which makes them targets for fraud. Your gateway should include encryption, two-factor authentication, and a fraud screening engine that catches suspicious activity without blocking real clients.

For example, a good fraud engine checks device data, location, and card history in real time. This protects your revenue without adding friction for genuine buyers.

5. Pricing and fees

Gateway pricing usually includes a percentage fee per transaction and sometimes a fixed fee on top. Some providers charge setup fees, monthly platform fees, or hidden currency conversion markups.

Look for transparent pricing with no fixed costs. Pay-per-transaction models work best for growing businesses because you only pay when money actually comes in.

Tip: Ask providers for a pricing breakdown specific to your transaction volume and currencies. Standard rates on a website may not reflect what you actually pay.

How to start accepting B2B payments online

Once you have picked a gateway, getting live does not need to be complicated. Most platforms follow a similar setup process, and with the right preparation, you can start collecting payments within days.

Here are the steps to go from sign-up to your first transaction:

1. Pick a gateway that fits your business

Start by matching the gateway to your actual needs. List the countries your clients are in, the currencies they pay in, and the payment methods they prefer. Then check which providers support all three.

For instance, if you export services to the US and UK, you need a gateway that accepts USD and GBP through cards, bank transfers, and ideally local payment methods. Do not pick a provider just because it is popular. Pick one that fits your payment flow.

2. Set up your merchant account

Most gateways require a merchant account, which is the account where your funds get settled. Some providers bundle this into their onboarding, so you do not need a separate application.

During this step, you will submit business documents like your registration certificate and bank details. Keep these ready to avoid delays.

3. Connect the gateway to your platform

Integration depends on your setup. If you run a Shopify or WooCommerce store, most gateways offer ready-made plugins you can install in minutes. For custom websites or apps, you will use the gateway's API.

For example, if your billing system sends invoices by email, you can integrate payment links so clients can pay directly from the invoice. No separate checkout page needed.

4. Configure payment methods and currencies

Once connected, set up the payment methods and currencies you want to accept. Turn on the ones your clients use most and disable the rest to keep your checkout clean.

If you serve clients in multiple countries, enable multi-currency collection so each buyer sees prices and pays in their own currency. This reduces confusion and lowers payment drop-offs.

5. Test, go live, and monitor

Run test transactions using the gateway's sandbox or test mode before going live. Check that the payments process correctly, confirmations are sent, and funds appear in your dashboard.

After launch, monitor your first few weeks closely. Track success rates, failed payments, and settlement timelines. If something looks off, flag it with your provider early.

Tip: Most payment issues show up in the first 30 days. Set a reminder to review your gateway performance after the first month and adjust settings if needed.

What are the common challenges with B2B payment gateways?

Even after setting up a gateway, some problems show up once you start processing real transactions. Knowing these early helps you pick a provider that handles them well. Here are the most common issues businesses run into:

1. High transaction failure rates

International card payments fail more often than domestic ones. Issues like incorrect card messaging, missing authentication protocols, or poor routing cause declines even when the buyer has funds.

For example, a valid Visa card from the UK might get declined if your gateway does not send the right data to the issuing bank. High failure rates mean lost revenue, frustrated clients, and a higher risk of chargeback disputes.

2. Limited payment method coverage

Some gateways only support a few card networks or one type of bank transfer. If your client in Germany prefers SEPA or your buyer in the UAE uses a local wallet, a limited gateway will not work.

The fix is choosing a platform with a wide range of global payment methods so your clients can pay the way they prefer.

3. Manual reconciliation

If your gateway does not auto-match incoming payments with invoices, your team ends up doing reconciliation by hand. This is slow, error-prone, and gets worse as transaction volume grows.

Look for platforms that offer real-time dashboards, downloadable reports, and automatic settlement tracking.

Tip: Payment challenges grow as your business scales. A gateway that works for 10 transactions a month may struggle at 500. Choose one built for the volume you are growing towards.

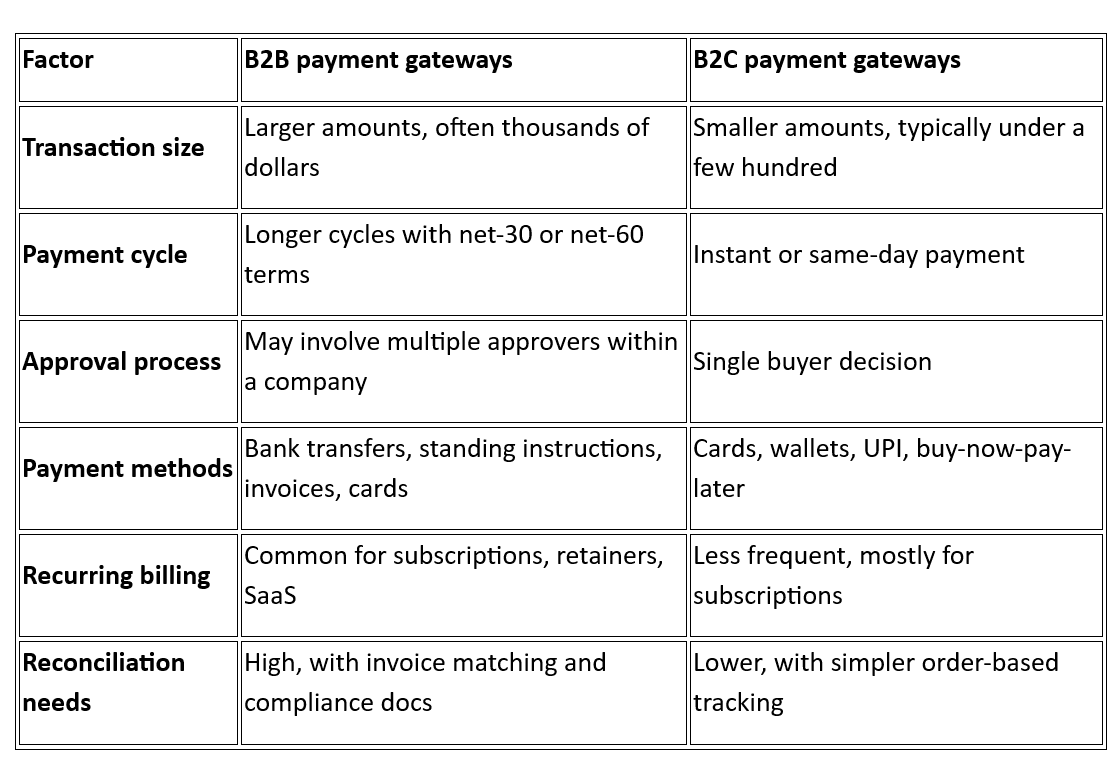

B2B vs. B2C payment gateways: What are their key differences?

B2B and B2C payments both move money digitally, but the way they work is quite different. If your gateway was built for consumer checkout, it may not handle B2B needs well. Here is how they compare:

If your business sells to other businesses, pick a gateway designed for B2B workflows. Consumer-focused platforms often lack support for invoicing, recurring mandates, and the multi-currency setups that B2B sellers need.

Accept B2B payments globally and scale faster with PayGlocal

Collecting payments from business clients in other countries comes with extra friction. Card declines, currency conversion losses, missing compliance documents, and limited payment options slow down your cash flow and frustrate your clients.

PayGlocal is built to solve these exact problems for businesses selling globally. Here’s what you get.

- Dynamic checkout: A customizable, fast checkout that supports global cards and local payment methods, so your clients pay their preferred way.

- Card payments: High approval rates on international credit and debit cards with smart routing and enhanced messaging to global issuing banks.

- Recurring payments: Set up subscriptions, standing instructions, and auto-debits on international cards for steady, predictable revenue.

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, CAD, and 33+ currencies from 180+ countries.

- One platform: Manage all your payments, reports, settlements, and compliance documents from a single dashboard.

No setup fees. No monthly retainers. No hidden documentation costs. We only win when you get paid. Get your cross-border B2B payments moving with a partner that knows the trenches.

Final thoughts

A B2B payment gateway is no longer optional. If your business collects payments from other companies, especially across borders, the right gateway saves you time, reduces failed payments, and gives your finance team clear visibility over every transaction.

Start by listing how your clients pay today, where they are located, and what volume you expect over the next year. Then match those needs to a gateway that supports your payment methods, currencies, and growth plans.

Businesses that set this up early collect faster, lose fewer deals to payment friction, and scale with confidence. PayGlocal is helping Indian businesses do exactly that, with support for multi-currency acceptance, global payment methods, and zero fixed costs. Get started with PayGlocal today.