When sending a payment to your overseas supplier, you likely feel confident that the funds will reach them without issue. However, concerns may arise: What if the payment is mistakenly sent to the wrong account? What if your business’s hard-earned funds are lost within the intricacies of international banking systems? These are legitimate concerns that can disrupt your operations, and understanding how to mitigate such risks is crucial for ensuring smooth, secure transactions.

BIC and SWIFT codes serve as key identifiers that ensure your international payments are routed accurately and efficiently, guiding your funds across global banking networks. Understanding BIC and SWIFT codes is essential for anyone importing or exporting goods or services.

In this blog, we’ll explore BIC and SWIFT codes, how they work, and why they are crucial for seamless global banking.

But first, let’s get a clear picture of what exactly BIC and SWIFT codes are about and when they come into the scene:

BIC is a unique identifier assigned to banks and financial institutions worldwide. Society for Worldwide Interbank Financial Telecommunication, SWIFT is a messaging network that banks and financial institutions use to exchange financial transaction information securely. Though BIC and SWIFT are often used interchangeably, they refer to the same identification system. BIC is commonly known as the SWIFT code, as SWIFT manages it.

When sending money across borders, you might wonder how banks ensure your funds arrive at the right destination. This is where BIC and SWIFT codes become crucial players in the financial world. These codes function as unique identifiers for banks and financial institutions, creating a secure transaction pathway and reducing the risk of errors that could lead to lost funds or delayed payments.

Now that you know what BIC and SWIFT codes are and their significance in international transactions, let’s delve into their structure and how they are composed:

To begin with, let’s understand what BIC or SWIFT code looks like. These codes are typically structured precisely, comprising 8 to 11 characters that convey crucial information about the bank and its geographic location.

Each component serves a specific purpose:

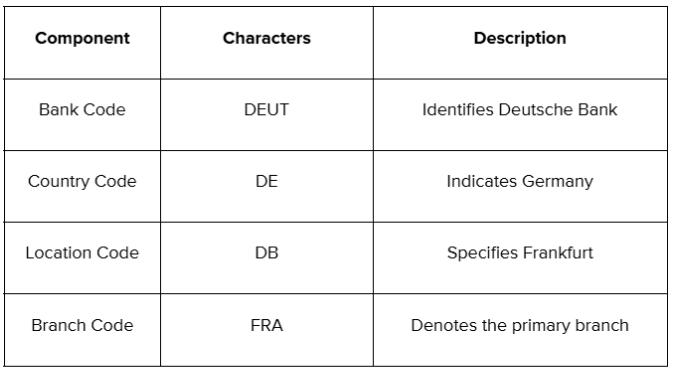

To explain the structure of a BIC and SWIFT code, let’s take a closer look at the example ‘DEUTDEDBFRA’. Here’s how this code breaks down:

The table depicts various components of a BIC code’s structure.

In this example, "DEUT" designates Deutsche Bank, confirming that the bank is located in Germany with "DE." The "DB" points to Frankfurt, where the bank’s primary operations are based, and the "FRA" indicates that this code refers to the bank's primary branch. This precise organization helps streamline international transactions, reducing the chance of mistakes and ensuring that your funds are sent exactly where they need to go.

Understanding this structure is essential for successfully managing international banking transactions.

Also Read: What is a Multi-Currency Account? - A Beginner’s Guide to Business Accounts.

Now that you understand the components that constitute BIC and SWIFT codes, let’s explore the specific requirements for their usage in global banking.

BIC and SWIFT codes are critical in international money transfers, functioning as the backbone of secure and efficient cross-border transactions.

These codes ensure that:

Now that you recognize the importance of these codes, let’s discuss how to find and effectively use SWIFT and BIC codes for your transactions:

Locating the correct BIC or SWIFT code is essential for ensuring that your international money transfers are processed smoothly and accurately. You can typically find these codes on your bank statements, often listed alongside other vital banking details.

Additionally, most banks provide this information on their websites, usually in sections dedicated to international transfers or customer service. It’s wise to double-check the code before initiating any transaction, as even a tiny error can result in delays or misdirected funds.

In regions participating in the SEPA (Single Euro Payments Area) framework, BIC codes are essential, as they are commonly required alongside IBANs to facilitate seamless transactions across borders.

While BIC and SWIFT codes are indispensable in the Eurozone, their significance extends far beyond Europe, especially in the United States. U.S. banks rely on these codes for international transactions to ensure funds are routed correctly to foreign institutions. This is particularly crucial given the intricacy of global banking systems, where multiple banks may be involved in a single transfer.

Also Read: Understanding the Use and Elements of MT103 in SWIFT Payment Transfers.

Now that you’re equipped with knowledge on locating these codes, it’s essential to address some common issues that can arise during their use:

An incorrect BIC or SWIFT code could lead to severe delays in processing your transaction or, worse, result in your funds being directed to the wrong bank. This complicates the process of retrieving your money and can create a cascade of issues for both you and the recipient. Therefore, it’s crucial to take the time to double-check the code you’ve entered, as common errors may include confusing similar-looking characters or inadvertently omitting critical digits.

If you ever suspect you’ve made an error in the code, you must contact your bank immediately to address the issue. Time is of the essence in these situations, as prompt action can help minimize potential complications and ensure that your funds are redirected correctly if needed. Banks typically have protocols to assist customers in resolving such mistakes, and they can guide you through the necessary steps to rectify any errors.

By being vigilant and proactive, you can safeguard your transactions, avoiding the stress and hassle that often accompany errors in the intricate sphere of international banking.

Also Read: Difference Between SWIFT Code and IFSC Code for Transactions

Now that we’ve tackled the potential pitfall, let’s clarify how BIC and SWIFT codes differ from IBANs and other banking codes:

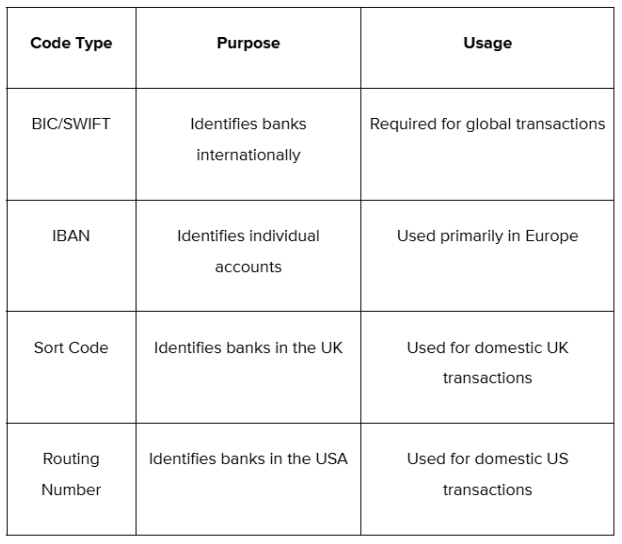

It’s easy to confuse BIC and SWIFT codes with IBANs and other domestic codes like Sort Codes and Routing Numbers. Here’s a quick comparison to clarify:

The table depicts various banking codes along with their purpose and usage.

Each code serves a unique purpose, making it essential to use the correct one for your transaction needs.

Also Read: SWIFT: The network powering international money transfer.

With these key distinctions in mind, it’s essential to summarize the key takeaways regarding the importance of using BIC and SWIFT codes.

Understanding BIC and SWIFT codes is essential for anyone involved in international banking. Correctly using these codes can significantly minimize the risk of errors that could cause delays or financial complications. As global transactions become more frequent, the clarity and reliability offered by these codes are vital for maintaining trust and efficiency in financial operations.

Paying attention to detail when entering these codes is crucial for safeguarding your transactions and improving your overall banking experience. As the global economy continues to grow, the importance of these identifiers will only increase, reinforcing their role in facilitating international transactions. So, the next time you initiate a cross-border payment, be sure to double-check those BIC and SWIFT codes to ensure your transaction stays on track!

Now that you’re equipped with knowledge about BIC and SWIFT codes, why not elevate your online transactions with PayGlocal? Experience the ease of multi-currency accounts, dynamic checkouts, and seamless global payment methods—all from one platform. Make your money work for you, ensuring secure and efficient transactions every time. Join PayGlocal today and transform the way you manage your finances across borders!

BIC and SWIFT codes serve as key identifiers that ensure your international payments are routed accurately and efficiently, guiding your funds across global banking networks. Understanding BIC and SWIFT codes is essential for anyone importing or exporting goods or services.

In this blog, we’ll explore BIC and SWIFT codes, how they work, and why they are crucial for seamless global banking.

But first, let’s get a clear picture of what exactly BIC and SWIFT codes are about and when they come into the scene:

Overview of BIC or SWIFT Codes

BIC is a unique identifier assigned to banks and financial institutions worldwide. Society for Worldwide Interbank Financial Telecommunication, SWIFT is a messaging network that banks and financial institutions use to exchange financial transaction information securely. Though BIC and SWIFT are often used interchangeably, they refer to the same identification system. BIC is commonly known as the SWIFT code, as SWIFT manages it.

When sending money across borders, you might wonder how banks ensure your funds arrive at the right destination. This is where BIC and SWIFT codes become crucial players in the financial world. These codes function as unique identifiers for banks and financial institutions, creating a secure transaction pathway and reducing the risk of errors that could lead to lost funds or delayed payments.

Now that you know what BIC and SWIFT codes are and their significance in international transactions, let’s delve into their structure and how they are composed:

Structure of BIC or SWIFT Codes

To begin with, let’s understand what BIC or SWIFT code looks like. These codes are typically structured precisely, comprising 8 to 11 characters that convey crucial information about the bank and its geographic location.

Each component serves a specific purpose:

- The first four characters are the Bank Code, identifying the financial institution.

- The following two characters form the Country Code, which indicates the nation where the bank is located.

- The subsequent two characters make up the Location Code, helping to pinpoint the specific city or area.

- Lastly, an optional Branch Code can include up to three additional characters to specify a particular branch.

To explain the structure of a BIC and SWIFT code, let’s take a closer look at the example ‘DEUTDEDBFRA’. Here’s how this code breaks down:

The table depicts various components of a BIC code’s structure.

In this example, "DEUT" designates Deutsche Bank, confirming that the bank is located in Germany with "DE." The "DB" points to Frankfurt, where the bank’s primary operations are based, and the "FRA" indicates that this code refers to the bank's primary branch. This precise organization helps streamline international transactions, reducing the chance of mistakes and ensuring that your funds are sent exactly where they need to go.

Understanding this structure is essential for successfully managing international banking transactions.

Also Read: What is a Multi-Currency Account? - A Beginner’s Guide to Business Accounts.

Now that you understand the components that constitute BIC and SWIFT codes, let’s explore the specific requirements for their usage in global banking.

Importance of BIC or SWIFT Codes

BIC and SWIFT codes are critical in international money transfers, functioning as the backbone of secure and efficient cross-border transactions.

These codes ensure that:

- Funds are sent accurately and safely to their intended destination.

- Communication is maintained between banks via the SWIFT messaging system, * which helps to eliminate potential errors that could lead to significant financial losses.

- A reliable framework in international banking is maintained, lowering the risk of misdirecting funds due to clerical errors.

Now that you recognize the importance of these codes, let’s discuss how to find and effectively use SWIFT and BIC codes for your transactions:

Finding and Using BIC or SWIFT Codes

Locating the correct BIC or SWIFT code is essential for ensuring that your international money transfers are processed smoothly and accurately. You can typically find these codes on your bank statements, often listed alongside other vital banking details.

Additionally, most banks provide this information on their websites, usually in sections dedicated to international transfers or customer service. It’s wise to double-check the code before initiating any transaction, as even a tiny error can result in delays or misdirected funds.

In regions participating in the SEPA (Single Euro Payments Area) framework, BIC codes are essential, as they are commonly required alongside IBANs to facilitate seamless transactions across borders.

While BIC and SWIFT codes are indispensable in the Eurozone, their significance extends far beyond Europe, especially in the United States. U.S. banks rely on these codes for international transactions to ensure funds are routed correctly to foreign institutions. This is particularly crucial given the intricacy of global banking systems, where multiple banks may be involved in a single transfer.

Also Read: Understanding the Use and Elements of MT103 in SWIFT Payment Transfers.

Now that you’re equipped with knowledge on locating these codes, it’s essential to address some common issues that can arise during their use:

Minimizing Human Error in SWIFT/BIC Code Entry

An incorrect BIC or SWIFT code could lead to severe delays in processing your transaction or, worse, result in your funds being directed to the wrong bank. This complicates the process of retrieving your money and can create a cascade of issues for both you and the recipient. Therefore, it’s crucial to take the time to double-check the code you’ve entered, as common errors may include confusing similar-looking characters or inadvertently omitting critical digits.

If you ever suspect you’ve made an error in the code, you must contact your bank immediately to address the issue. Time is of the essence in these situations, as prompt action can help minimize potential complications and ensure that your funds are redirected correctly if needed. Banks typically have protocols to assist customers in resolving such mistakes, and they can guide you through the necessary steps to rectify any errors.

By being vigilant and proactive, you can safeguard your transactions, avoiding the stress and hassle that often accompany errors in the intricate sphere of international banking.

Also Read: Difference Between SWIFT Code and IFSC Code for Transactions

Now that we’ve tackled the potential pitfall, let’s clarify how BIC and SWIFT codes differ from IBANs and other banking codes:

Distinctions Between SWIFT/ BIC, IBAN, and Other Codes

It’s easy to confuse BIC and SWIFT codes with IBANs and other domestic codes like Sort Codes and Routing Numbers. Here’s a quick comparison to clarify:

The table depicts various banking codes along with their purpose and usage.

Each code serves a unique purpose, making it essential to use the correct one for your transaction needs.

Also Read: SWIFT: The network powering international money transfer.

With these key distinctions in mind, it’s essential to summarize the key takeaways regarding the importance of using BIC and SWIFT codes.

Conclusion

Understanding BIC and SWIFT codes is essential for anyone involved in international banking. Correctly using these codes can significantly minimize the risk of errors that could cause delays or financial complications. As global transactions become more frequent, the clarity and reliability offered by these codes are vital for maintaining trust and efficiency in financial operations.

Paying attention to detail when entering these codes is crucial for safeguarding your transactions and improving your overall banking experience. As the global economy continues to grow, the importance of these identifiers will only increase, reinforcing their role in facilitating international transactions. So, the next time you initiate a cross-border payment, be sure to double-check those BIC and SWIFT codes to ensure your transaction stays on track!

Now that you’re equipped with knowledge about BIC and SWIFT codes, why not elevate your online transactions with PayGlocal? Experience the ease of multi-currency accounts, dynamic checkouts, and seamless global payment methods—all from one platform. Make your money work for you, ensuring secure and efficient transactions every time. Join PayGlocal today and transform the way you manage your finances across borders!