An international customer discovers your brand, loves your product, and adds it to their cart. But at the final step, they drop off. The reason? Your checkout only speaks local, and their international card or digital wallet just won't work.

This isn't just a minor glitch; it’s a massive missed opportunity. The global e-commerce market is valued at $36.21 trillion in 2026, and it is estimated to hit $77.58 trillion by 2031. If your checkout isn't optimized for cross-border buyers, you are effectively closing your doors to 95% of the world’s consumers.

This guide breaks down cross-border e-commerce for Indian sellers. You'll learn how it works, its different models, common challenges, and how to start accepting cross-border e-commerce payments easily, without delays.

Cross-border e-commerce is the process of selling products or services online to buyers located in a different country. The seller and the buyer are in two separate countries, and the transaction happens through a website, app, or online marketplace.

For an Indian business, this could look like a D2C clothing brand shipping orders to customers in the US. Or a SaaS company in Bengaluru billing clients in the UK through recurring payments. Or a freelance designer in Mumbai receiving project fees from a client in Canada through a multi-currency account.

The key difference from regular e-commerce is that the transaction crosses a national border. That one detail changes how payments work, which currencies are involved, and how the buyer experiences your checkout.

Tip: If you already sell online in India and your product or service doesn't require a physical presence, you likely have what it takes to start selling internationally.

Every business that only sells domestically has a ceiling on how much it can grow. When demand in your home market slows down or competition increases, your revenue feels the pressure first. Cross-border e-commerce removes that ceiling.

Here's why it matters for Indian sellers specifically:

Indian businesses in sectors like textiles, IT services, education, travel, and handmade goods are already seeing strong demand from international buyers. The question isn't whether the opportunity exists. It's whether your setup is ready to capture it.

Note: Cross-border selling doesn't require a physical office or warehouse abroad. Many Indian businesses operate entirely from India and sell to 10+ countries.

A customer on the other side of the world visits your website, picks a product, and checks out. That sounds simple, but several things happen between that click and the money reaching your bank account.

1. Product discovery: The buyer finds your product through your website, a marketplace like Amazon, or a social media ad. Your product listing needs to show prices in the buyer's local currency to build trust.

2. Checkout and payment: The buyer selects a payment method they're familiar with, like a credit card, bank transfer, or a local digital wallet. Your payment gateway processes the transaction and handles currency conversion.

3. Fraud and security checks: The payment goes through fraud screening to verify that the card is real and the buyer is who they say they are. This step prevents chargebacks and protects your revenue.

4. Order fulfillment: You ship the product directly or through a logistics partner. For digital products and services, delivery happens immediately after payment confirmation.

5. Settlement: The payment provider converts the foreign currency into INR (or your preferred currency) and settles the funds into your bank account. Settlement timelines vary by provider.

Each of these steps introduces a point where things can go wrong. A buyer might abandon checkout because their preferred payment method isn't available. A legitimate transaction might get flagged as fraud. Or the settlement might take longer than expected, affecting your cash flow.

The businesses that do cross-border e-commerce well are the ones that get each of these steps right, especially payments and checkout.

Not every international sale follows the same structure. The relationship between the seller and the buyer determines how the transaction works, how payments flow, and what kind of setup you need. Here's a quick comparison of the main models.

Each model has different payment needs, and your choice of model affects how you collect money from international buyers.

B2B cross-border e-commerce involves one company selling to another company in a different country. Think of an Indian IT services firm providing monthly support to a client in the US, or a textile manufacturer supplying fabric to a retailer in Germany.

Payments in B2B are usually larger and less frequent. They often happen through SWIFT transfers or bank wires, and they can take several days to settle. Recurring billing is common for service-based contracts.

B2C is the most common model in cross-border e-commerce, in which the company sells directly to an individual buyer in another country through a marketplace. For instance, a skincare brand in Delhi could list its products on Amazon US and ship directly to customers in New York.

Payments here are smaller but more frequent. Buyers expect to pay using the methods they already trust, like Visa, Mastercard, or local options like iDEAL in the Netherlands.

D2C is a subset of B2C where the brand sells through its own website without any marketplace in between. This gives you full control over pricing, branding, and the checkout experience. A home decor brand in Jaipur, for instance, could sell directly to buyers in Australia through its own Shopify store.

The trade-off is that you're responsible for driving traffic and building trust on your own. Your checkout needs to support global payment methods and display prices in the buyer's currency to reduce drop-offs.

Note: Many Indian businesses start with B2C through marketplaces, then move to D2C once they build enough brand recognition to drive direct traffic.

Selling internationally sounds straightforward until your first international card payment gets declined. Or until you realize your international buyer has no way to pay on your website. Here are the problems Indian sellers run into most often.

Most of these challenges are connected to payments. The product, the shipping, and the marketing all matter. But if the payment doesn't go through, nothing else matters.

Tip: Before expanding to a new country, research which payment methods are most popular there. Offering even one local payment option can noticeably improve your approval rate.

Your checkout is the last step before a sale is complete. If a buyer can't find their preferred way to pay, they'll leave. It doesn't matter how good your product is. Here's what buyers in key markets prefer.

Offering the right mix of payment methods for each target market is one of the highest-impact changes you can make to your cross-border setup. It directly affects how many buyers complete their purchase.

The good news is that you don't need to set up a separate payment provider for each country. A single provider with wide payment method coverage can handle most of this for you.

You don't need a global office or a massive budget to start selling internationally. Many Indian businesses begin with what they already have and add the right tools as they grow. Here’s a complete step-by-step guide to get started:

Look at where demand for your product or service already exists. Check your website analytics for international traffic. Look at competitor brands selling similar products globally. Start with 1-2 countries where you see clear interest.

If you're selling through your own website, make sure it supports multi-currency pricing. Your product pages should display prices in the buyer's local currency. If you're using a marketplace like Amazon, check which countries your product category is available in and set up your Amazon global selling account accordingly.

This is the most important decision you'll make. Your payment provider determines which currencies you can accept, which payment methods are available at checkout, how quickly you get settled, and what your approval rates look like. Look for a provider that supports your target markets, offers local payment methods, and has strong fraud screening built in.

You'll need an import-export code (IEC) to start exporting from India. Depending on your product, you may also need specific certifications or an IEC code registration. Sort this out before you start accepting international orders.

Before you go live at full scale, run a few test transactions from your target countries. Check that the payment goes through, the currency converts correctly, and the buyer gets a confirmation. Fix any issues before you start driving traffic.

Once you're live, track your payment success rate, average order value, and customer feedback from international buyers. Use this data to decide when to add new countries or payment methods.

Tip: Your payment provider's dashboard should give you a clear view of approvals, declines, and settlements by country. If it doesn't, that's a sign you may need a better provider.

Every declined transaction is a customer who wanted to buy from you but couldn't. For Indian businesses selling globally, payment failures are one of the biggest reasons for lost revenue. The problem usually isn't your product or your pricing. It's the payment infrastructure behind your checkout.

PayGlocal is a cross-border payment platform built for Indian businesses that sell to global customers. Here's what it offers:

Card payments: Fewer international card transactions get declined because each payment is routed through the best path to the buyer's bank, which means more completed purchases at checkout.

D2C brands, SaaS companies, freelancers, travel businesses, and exporters across India already use PayGlocal to collect payments from global customers. The setup is simple, and the platform grows with your business.

Cross-border e-commerce is how Indian businesses reach customers they'd never find in the domestic market alone. The opportunity is large, the tools exist, and buyers around the world are already looking for what Indian sellers offer.

Your first step is to pick one or two target countries, set up your store for international buyers, and choose a payment provider that can actually support cross-border transactions at scale. Don't wait until you've figured out every detail. Start with a small batch of orders and improve as you go.

PayGlocal is built for exactly this, helping Indian businesses accept payments from 180+ countries in 33+ currencies with 40+ payment methods. The longer you wait to set up global payments, the more sales go to competitors who already have. Get started with PayGlocal today and start collecting payments easily from your global customers.

This isn't just a minor glitch; it’s a massive missed opportunity. The global e-commerce market is valued at $36.21 trillion in 2026, and it is estimated to hit $77.58 trillion by 2031. If your checkout isn't optimized for cross-border buyers, you are effectively closing your doors to 95% of the world’s consumers.

This guide breaks down cross-border e-commerce for Indian sellers. You'll learn how it works, its different models, common challenges, and how to start accepting cross-border e-commerce payments easily, without delays.

Key takeaways

- Cross-border e-commerce defined: It's the process of selling products or services online to buyers in other countries, covering everything from product listing to payment collection.

- Three main models: Business-to-business (B2B), business-to-consumer (B2C), and direct-to-consumer (D2C), each serve a different type of international buyer.

- Payments are the hardest part: Most cross-border sellers from India lose revenue to declined transactions, currency conversion fees, and slow settlements.

- Local payment methods matter: Buyers in each country prefer specific ways to pay. Offering those methods directly affects whether a sale goes through.

- PayGlocal supports 33+ currencies: Indian businesses can accept payments from buyers in 180+ countries using 40+ payment methods through a single platform.

What is cross-border e-commerce?

Cross-border e-commerce is the process of selling products or services online to buyers located in a different country. The seller and the buyer are in two separate countries, and the transaction happens through a website, app, or online marketplace.

For an Indian business, this could look like a D2C clothing brand shipping orders to customers in the US. Or a SaaS company in Bengaluru billing clients in the UK through recurring payments. Or a freelance designer in Mumbai receiving project fees from a client in Canada through a multi-currency account.

The key difference from regular e-commerce is that the transaction crosses a national border. That one detail changes how payments work, which currencies are involved, and how the buyer experiences your checkout.

Tip: If you already sell online in India and your product or service doesn't require a physical presence, you likely have what it takes to start selling internationally.

Why does cross-border e-commerce matter for Indian businesses?

Every business that only sells domestically has a ceiling on how much it can grow. When demand in your home market slows down or competition increases, your revenue feels the pressure first. Cross-border e-commerce removes that ceiling.

Here's why it matters for Indian sellers specifically:

- Larger customer base: Selling globally puts your products in front of buyers across continents who may never find you through domestic channels alone.

- Higher order values: Buyers in markets like the US, UK, and Europe often have more purchasing power. The same product can bring in more revenue per order when sold internationally.

- Currency advantage: When you earn in USD, GBP, or EUR and your costs are in INR, the exchange rate works in your favor. This can increase your profit margins on every sale.

- Less dependence on one market: Seasonal slowdowns, policy changes, or economic dips in India won't affect your international revenue the same way. Selling in several countries spreads your risk.

- Year-round demand: Festivals and buying seasons differ by country. While India's market may slow down in certain months, buyers in other regions may be in peak spending mode.

Indian businesses in sectors like textiles, IT services, education, travel, and handmade goods are already seeing strong demand from international buyers. The question isn't whether the opportunity exists. It's whether your setup is ready to capture it.

Note: Cross-border selling doesn't require a physical office or warehouse abroad. Many Indian businesses operate entirely from India and sell to 10+ countries.

How does cross-border e-commerce work?

A customer on the other side of the world visits your website, picks a product, and checks out. That sounds simple, but several things happen between that click and the money reaching your bank account.

1. Product discovery: The buyer finds your product through your website, a marketplace like Amazon, or a social media ad. Your product listing needs to show prices in the buyer's local currency to build trust.

2. Checkout and payment: The buyer selects a payment method they're familiar with, like a credit card, bank transfer, or a local digital wallet. Your payment gateway processes the transaction and handles currency conversion.

3. Fraud and security checks: The payment goes through fraud screening to verify that the card is real and the buyer is who they say they are. This step prevents chargebacks and protects your revenue.

4. Order fulfillment: You ship the product directly or through a logistics partner. For digital products and services, delivery happens immediately after payment confirmation.

5. Settlement: The payment provider converts the foreign currency into INR (or your preferred currency) and settles the funds into your bank account. Settlement timelines vary by provider.

Each of these steps introduces a point where things can go wrong. A buyer might abandon checkout because their preferred payment method isn't available. A legitimate transaction might get flagged as fraud. Or the settlement might take longer than expected, affecting your cash flow.

The businesses that do cross-border e-commerce well are the ones that get each of these steps right, especially payments and checkout.

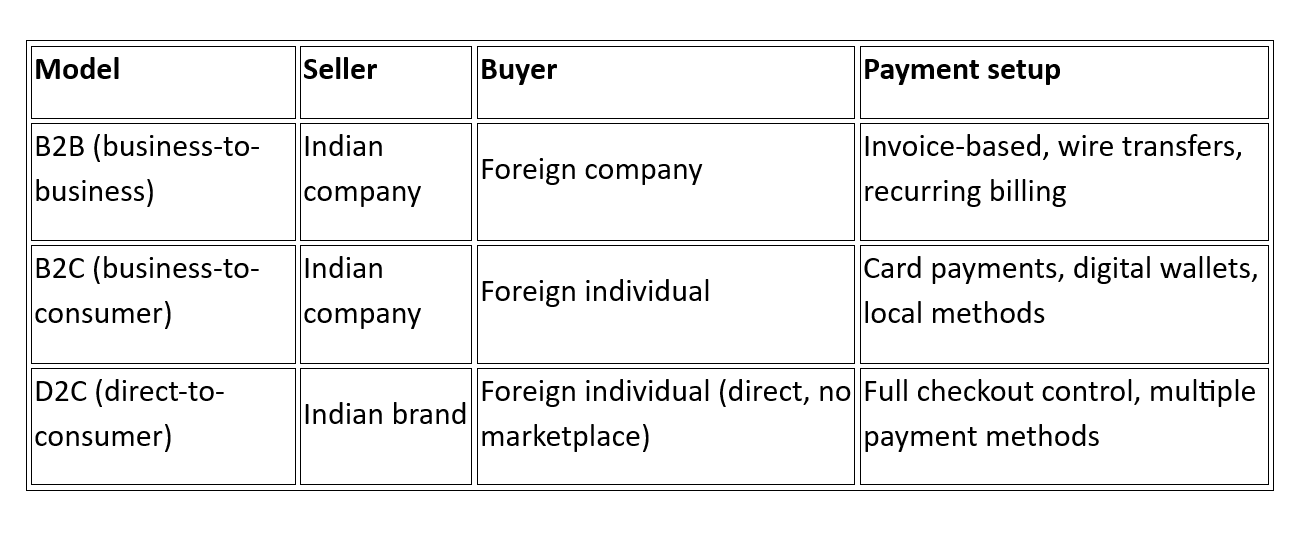

What are the main models of cross-border e-commerce?

Not every international sale follows the same structure. The relationship between the seller and the buyer determines how the transaction works, how payments flow, and what kind of setup you need. Here's a quick comparison of the main models.

Each model has different payment needs, and your choice of model affects how you collect money from international buyers.

1. B2B (business-to-business)

B2B cross-border e-commerce involves one company selling to another company in a different country. Think of an Indian IT services firm providing monthly support to a client in the US, or a textile manufacturer supplying fabric to a retailer in Germany.

Payments in B2B are usually larger and less frequent. They often happen through SWIFT transfers or bank wires, and they can take several days to settle. Recurring billing is common for service-based contracts.

2. B2C (business-to-consumer)

B2C is the most common model in cross-border e-commerce, in which the company sells directly to an individual buyer in another country through a marketplace. For instance, a skincare brand in Delhi could list its products on Amazon US and ship directly to customers in New York.

Payments here are smaller but more frequent. Buyers expect to pay using the methods they already trust, like Visa, Mastercard, or local options like iDEAL in the Netherlands.

3. D2C (direct-to-consumer)

D2C is a subset of B2C where the brand sells through its own website without any marketplace in between. This gives you full control over pricing, branding, and the checkout experience. A home decor brand in Jaipur, for instance, could sell directly to buyers in Australia through its own Shopify store.

The trade-off is that you're responsible for driving traffic and building trust on your own. Your checkout needs to support global payment methods and display prices in the buyer's currency to reduce drop-offs.

Note: Many Indian businesses start with B2C through marketplaces, then move to D2C once they build enough brand recognition to drive direct traffic.

What challenges do Indian businesses face in cross-border e-commerce?

Selling internationally sounds straightforward until your first international card payment gets declined. Or until you realize your international buyer has no way to pay on your website. Here are the problems Indian sellers run into most often.

- Payment failures: International card transactions have a higher decline rate than domestic ones. Issuing banks in the buyer's country may flag the transaction, or the payment message may not carry the right data to get approved.

- Currency confusion: If your store only shows prices in INR, buyers in other countries have to guess what they're paying. That uncertainty leads to abandoned carts.

- Limited payment options: Credit cards aren't the default payment method everywhere. In many markets, buyers prefer bank transfers, digital wallets, or local payment networks. If you only accept cards, you're missing a portion of potential customers.

- High transaction fees: Some payment providers charge large markups on currency conversion and cross-border processing. Those fees add up fast when you're processing hundreds of transactions a month.

- Slow settlements: Getting your money can take anywhere from 2 days to 2 weeks, depending on your payment provider and the payment method used. Slow settlements strain your working capital.

- Fraud risk: Cross-border transactions carry a higher fraud risk than domestic ones. Without proper screening, you could face chargebacks that cost you the product, the revenue, and an extra penalty fee.

Most of these challenges are connected to payments. The product, the shipping, and the marketing all matter. But if the payment doesn't go through, nothing else matters.

Tip: Before expanding to a new country, research which payment methods are most popular there. Offering even one local payment option can noticeably improve your approval rate.

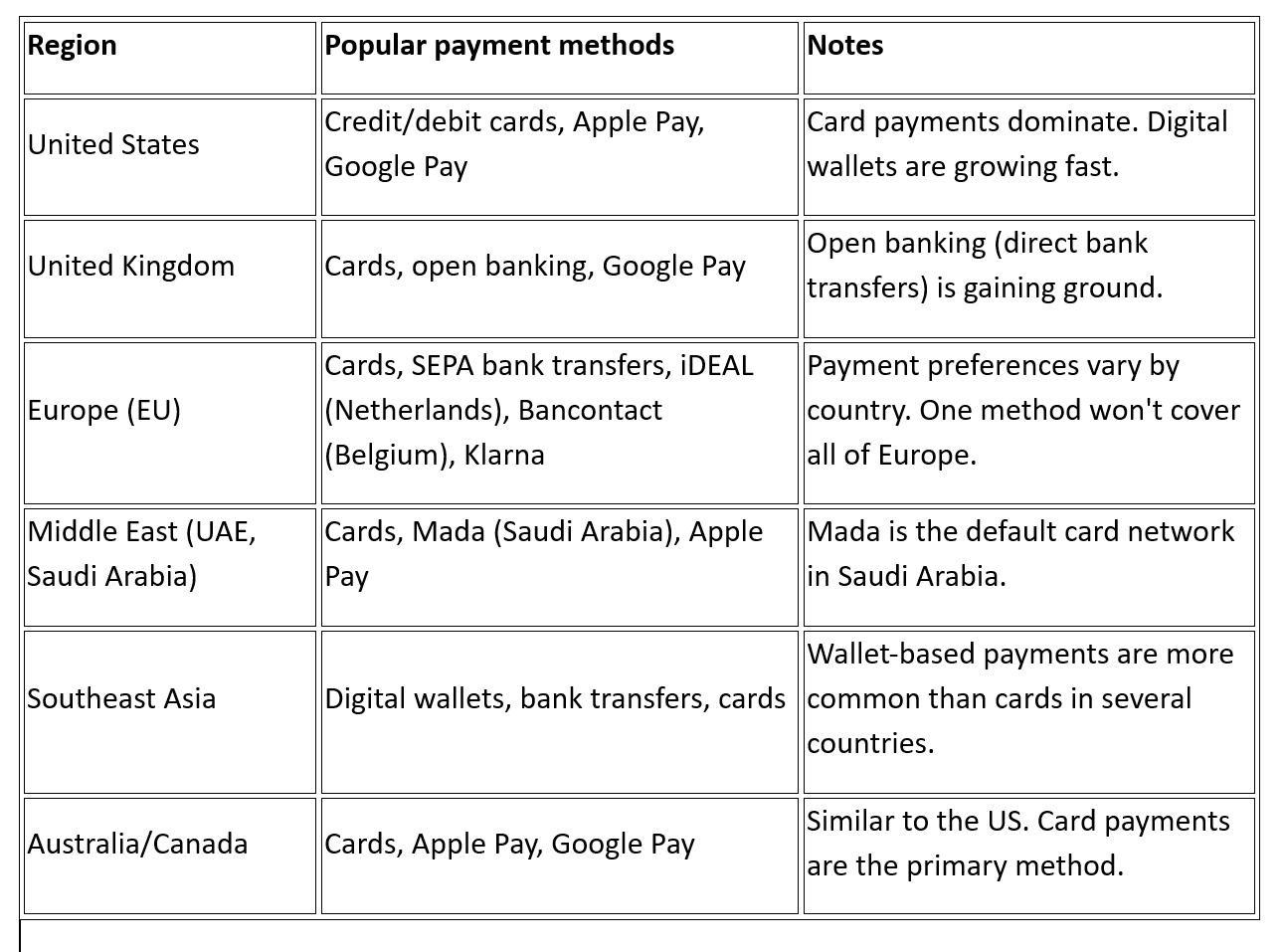

What payment methods do global buyers prefer?

Your checkout is the last step before a sale is complete. If a buyer can't find their preferred way to pay, they'll leave. It doesn't matter how good your product is. Here's what buyers in key markets prefer.

Offering the right mix of payment methods for each target market is one of the highest-impact changes you can make to your cross-border setup. It directly affects how many buyers complete their purchase.

The good news is that you don't need to set up a separate payment provider for each country. A single provider with wide payment method coverage can handle most of this for you.

How do you get started with cross-border e-commerce from India?

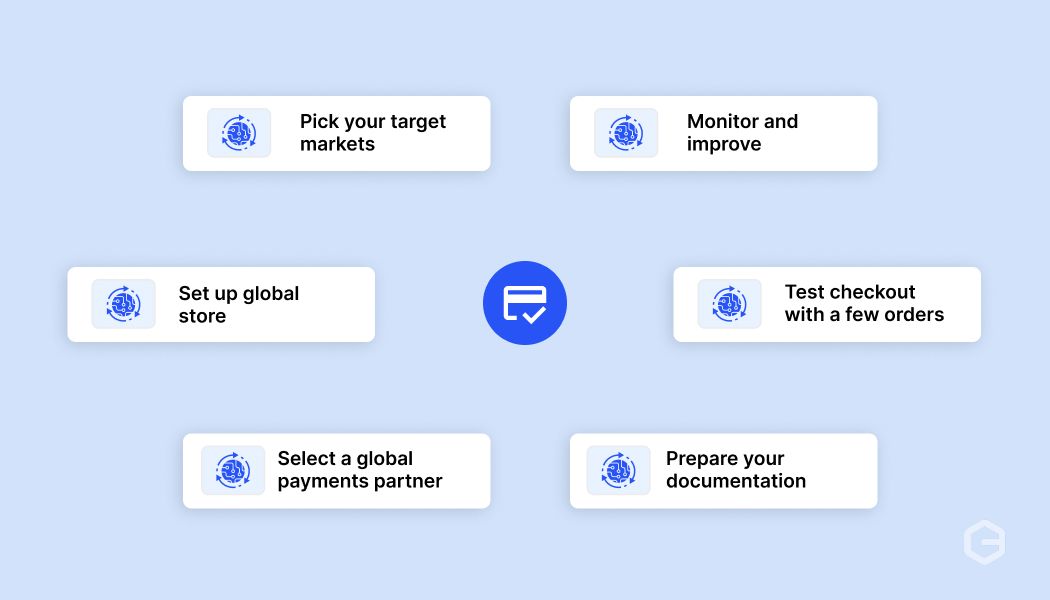

You don't need a global office or a massive budget to start selling internationally. Many Indian businesses begin with what they already have and add the right tools as they grow. Here’s a complete step-by-step guide to get started:

1. Pick your target markets

Look at where demand for your product or service already exists. Check your website analytics for international traffic. Look at competitor brands selling similar products globally. Start with 1-2 countries where you see clear interest.

2. Set up your online store for international buyers

If you're selling through your own website, make sure it supports multi-currency pricing. Your product pages should display prices in the buyer's local currency. If you're using a marketplace like Amazon, check which countries your product category is available in and set up your Amazon global selling account accordingly.

3. Choose a cross-border payment provider

This is the most important decision you'll make. Your payment provider determines which currencies you can accept, which payment methods are available at checkout, how quickly you get settled, and what your approval rates look like. Look for a provider that supports your target markets, offers local payment methods, and has strong fraud screening built in.

4. Prepare your documentation

You'll need an import-export code (IEC) to start exporting from India. Depending on your product, you may also need specific certifications or an IEC code registration. Sort this out before you start accepting international orders.

5. Test your checkout with a small batch of orders

Before you go live at full scale, run a few test transactions from your target countries. Check that the payment goes through, the currency converts correctly, and the buyer gets a confirmation. Fix any issues before you start driving traffic.

6. Monitor and improve

Once you're live, track your payment success rate, average order value, and customer feedback from international buyers. Use this data to decide when to add new countries or payment methods.

Tip: Your payment provider's dashboard should give you a clear view of approvals, declines, and settlements by country. If it doesn't, that's a sign you may need a better provider.

How PayGlocal powers your cross-border e-commerce growth

Every declined transaction is a customer who wanted to buy from you but couldn't. For Indian businesses selling globally, payment failures are one of the biggest reasons for lost revenue. The problem usually isn't your product or your pricing. It's the payment infrastructure behind your checkout.

PayGlocal is a cross-border payment platform built for Indian businesses that sell to global customers. Here's what it offers:

Card payments: Fewer international card transactions get declined because each payment is routed through the best path to the buyer's bank, which means more completed purchases at checkout.

- Global payment methods: Your buyers in 180+ countries can pay using 40+ local payment options they already trust, from digital wallets to bank transfers, which directly improves your checkout completion rate.

- Multi-currency accounts: Collect payments in 33+ currencies, giving you the flexibility to receive funds the way that works best for your business.

- Dynamic checkout: Your checkout page automatically adjusts to show the right payment methods and currency for each buyer's location, and the experience stays consistent with your brand.

- Recurring payments: If you bill clients monthly or run a subscription service, you can set up automatic debits on international cards without asking buyers to re-enter their details every cycle.

D2C brands, SaaS companies, freelancers, travel businesses, and exporters across India already use PayGlocal to collect payments from global customers. The setup is simple, and the platform grows with your business.

Final thoughts

Cross-border e-commerce is how Indian businesses reach customers they'd never find in the domestic market alone. The opportunity is large, the tools exist, and buyers around the world are already looking for what Indian sellers offer.

Your first step is to pick one or two target countries, set up your store for international buyers, and choose a payment provider that can actually support cross-border transactions at scale. Don't wait until you've figured out every detail. Start with a small batch of orders and improve as you go.

PayGlocal is built for exactly this, helping Indian businesses accept payments from 180+ countries in 33+ currencies with 40+ payment methods. The longer you wait to set up global payments, the more sales go to competitors who already have. Get started with PayGlocal today and start collecting payments easily from your global customers.