According to recent data, the total GST collections have grown by 9.4% annually, which indicates the growing tax compliance across various industries. If you run a business with multiple registrations, you've probably wondered how to properly allocate shared expenses between your head office and branches.

A cross charge under GST offers an effective solution for businesses that need to distribute costs efficiently across different GST-registered units. This mechanism helps you maintain compliance while ensuring proper cost allocation between your business entities.

In this guide, we break down everything about cross charge under GST, from how it works to its benefits, helping you make informed decisions for your multi-location business operations.

Cross charge under GST refers to the mechanism where a business entity charges another unit within the same organization for goods or services provided. This happens when you have multiple GST registrations for different business locations or units.

For example, if your head office in Mumbai provides marketing services to your branch office in Delhi, the head office can cross charge the Delhi branch for these services. Even though both entities belong to the same business, the GST law treats them as separate taxable persons due to their different registrations.

The key point here is that the cross charge applies GST on internal transactions between your own business units. This ensures proper cost allocation and helps maintain accurate financial records across all your registered locations.

Cross charge operates on a simple principle where internal services are treated as taxable supplies between distinct persons under the GST law. Here's how the process typically works:

For instance, if your Mumbai office provides ₹1,00,000 worth of administrative services to your Delhi office, you'll charge ₹18,000 as GST (assuming 18% rate). The Delhi office can claim this ₹18,000 as input tax credit, effectively making the transaction cost-neutral from a tax perspective.

Cross charge offers several practical advantages for businesses operating across multiple locations:

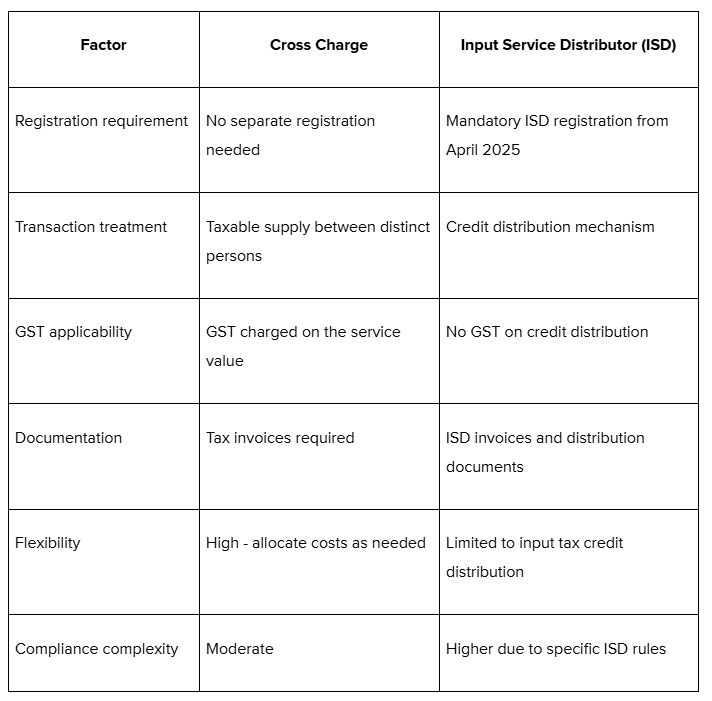

When exploring cross charge, it's also essential to know how it compares to the Input Service Distributor (ISD). Both mechanisms help businesses manage costs across multiple locations, but they work differently.

Cross charge treats internal transactions as taxable supplies between separate entities, while ISD focuses on distributing input tax credits without creating taxable transactions. The choice between these mechanisms depends on your business structure, cost allocation needs, and compliance preferences.

Here's how cross charge and ISD compare across key factors:

The right choice depends on your specific business requirements and operational preferences.

Proper documentation and compliance procedures are essential for successful cross charge implementation. GST authorities require specific documentation and processes to validate cross charge transactions:

Multi-location businesses often struggle with managing international payments while allocating costs across different units. Export businesses particularly face challenges collecting payments from global clients and distributing these costs efficiently between their registered entities.

PayGlocal offers an all-in-one payment solution that makes international payment collection simple and cost-effective for businesses managing multiple locations:

Whether you're allocating international payment processing costs or managing shared services across locations, PayGlocal helps you collect payments efficiently while maintaining clear cost allocation records.

The cross charge under GST helps businesses that need flexible cost allocation across multiple registered units. The key to successful cross charge implementation lies in maintaining proper documentation, following correct valuation methods, and ensuring accurate GST return filing across all your business units.

PayGlocal makes international payment collections more efficient, giving you complete transaction records that simplify cost allocation between different business entities.

Many growing businesses are already using integrated payment solutions to manage their multi-location operations more effectively. Get started with PayGlocal today and focus on growing your business instead of dealing with payment and cost allocation issues.

A cross charge under GST offers an effective solution for businesses that need to distribute costs efficiently across different GST-registered units. This mechanism helps you maintain compliance while ensuring proper cost allocation between your business entities.

In this guide, we break down everything about cross charge under GST, from how it works to its benefits, helping you make informed decisions for your multi-location business operations.

Key Takeaways:

- Cost allocation made simple: The cross charge under GST allows businesses to allocate shared costs between different GST-registered units legally and efficiently.

- Separate entity treatment: Unlike ISD registration, cross charge treats each business unit as a separate entity for GST purposes, requiring proper invoicing procedures.

- Input tax credit benefits: The cross charge transactions qualify for input tax credit, helping businesses avoid double taxation on shared expenses.

- Global payment solutions: PayGlocal helps export businesses manage international payments seamlessly while maintaining compliance across multiple business units.

What is a cross charge under GST?

Cross charge under GST refers to the mechanism where a business entity charges another unit within the same organization for goods or services provided. This happens when you have multiple GST registrations for different business locations or units.

For example, if your head office in Mumbai provides marketing services to your branch office in Delhi, the head office can cross charge the Delhi branch for these services. Even though both entities belong to the same business, the GST law treats them as separate taxable persons due to their different registrations.

The key point here is that the cross charge applies GST on internal transactions between your own business units. This ensures proper cost allocation and helps maintain accurate financial records across all your registered locations.

How does the cross charge work under GST?

Cross charge operates on a simple principle where internal services are treated as taxable supplies between distinct persons under the GST law. Here's how the process typically works:

- Service identification: Your head office or one business unit provides services like IT support, HR services, or administrative functions to other registered units.

- Invoice generation: The service-providing unit raises a tax invoice to the receiving unit, charging GST on the service value.

- Payment processing: The receiving unit pays the invoice amount, including GST, to the providing unit.

- Input tax credit claiming: The receiving unit can claim input tax credit on the GST paid, while the providing unit pays the collected GST to the government.

- Return filing: Both units report these transactions in their respective GST returns, maintaining proper documentation for compliance.

For instance, if your Mumbai office provides ₹1,00,000 worth of administrative services to your Delhi office, you'll charge ₹18,000 as GST (assuming 18% rate). The Delhi office can claim this ₹18,000 as input tax credit, effectively making the transaction cost-neutral from a tax perspective.

What are the key benefits of the cross charge under GST?

Cross charge offers several practical advantages for businesses operating across multiple locations:

- Accurate cost allocation: Distribute shared expenses proportionally across business units based on actual usage or benefit received.

- Input tax credit availability: Receiving units can claim full input tax credit on GST paid, preventing double taxation on internal transactions.

- Simplified compliance: Maintain clear audit trails and documentation for internal cost transfers without complex ISD registration requirements.

- Operational flexibility: Allocate costs dynamically based on changing business needs without restructuring your registration setup.

- Financial transparency: Create clear accountability for shared resources and services across different business locations.

Cross charge vs. Input Service Distributor: Which should you choose?

When exploring cross charge, it's also essential to know how it compares to the Input Service Distributor (ISD). Both mechanisms help businesses manage costs across multiple locations, but they work differently.

Cross charge treats internal transactions as taxable supplies between separate entities, while ISD focuses on distributing input tax credits without creating taxable transactions. The choice between these mechanisms depends on your business structure, cost allocation needs, and compliance preferences.

Here's how cross charge and ISD compare across key factors:

The right choice depends on your specific business requirements and operational preferences.

- Cross charge works best when: You need flexible cost allocation beyond just input tax credits, your business units have varying service requirements, and you want to avoid additional ISD registration compliance.

- ISD suits businesses that: Primarily need to distribute input tax credits, have shared costs mainly involving common input services, and are comfortable with mandatory registration requirements.

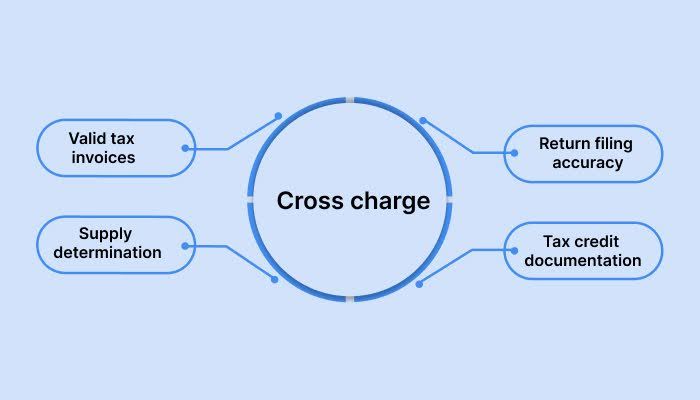

What documentation do you need for the cross charge?

Proper documentation and compliance procedures are essential for successful cross charge implementation. GST authorities require specific documentation and processes to validate cross charge transactions:

- Valid tax invoices: Issue proper GST invoices for all cross charge transactions with complete details, including GSTIN, service description, and tax amounts.

- Place of supply determination: Correctly identify the place of supply to apply appropriate GST rates and comply with interstate or intrastate supply rules.

- Return filing accuracy: Report cross charge transactions correctly in GSTR-1 (outward supplies) and GSTR-3B (summary returns) for both providing and receiving units.

- Input tax credit documentation: Maintain proper records to support input tax credit claims on the receiving end of cross charge transactions.

Manage global payments easily and scale your business

Multi-location businesses often struggle with managing international payments while allocating costs across different units. Export businesses particularly face challenges collecting payments from global clients and distributing these costs efficiently between their registered entities.

PayGlocal offers an all-in-one payment solution that makes international payment collection simple and cost-effective for businesses managing multiple locations:

- Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries, making it easier to allocate foreign exchange costs across business units.

- Easy payment tracking: Monitor all international payments with instant notifications, making cost allocation between units more accurate and timely.

- Global payment methods: Support 40+ international payment options, ensuring smooth collections regardless of your client's location or preferences.

- One platform management: Manage all payment operations from one dashboard, simplifying cost calculations and allocation processes across multiple business units.

- Zero setup fees: Start with no fixed costs and pay only per transaction, making it cost-effective for businesses managing multiple registrations.

Whether you're allocating international payment processing costs or managing shared services across locations, PayGlocal helps you collect payments efficiently while maintaining clear cost allocation records.

Final thoughts

The cross charge under GST helps businesses that need flexible cost allocation across multiple registered units. The key to successful cross charge implementation lies in maintaining proper documentation, following correct valuation methods, and ensuring accurate GST return filing across all your business units.

PayGlocal makes international payment collections more efficient, giving you complete transaction records that simplify cost allocation between different business entities.

Many growing businesses are already using integrated payment solutions to manage their multi-location operations more effectively. Get started with PayGlocal today and focus on growing your business instead of dealing with payment and cost allocation issues.