You send an invoice, and your international client confirms the payment. But after all deductions, you receive less than you calculated. You check the exchange rate and review the invoice, but the numbers still don't add up. This often occurs from GST on processing fees and forex conversion that you didn't account for in your initial estimate.

With GST revenue hitting ₹22.08 lakh crore in 2024-25, tax authorities are more vigilant than ever, making it critical for you to account for every rupee deducted during the remittance process. GST on foreign remittance isn't a straightforward tax on the total amount you receive; it’s a nuanced charge on the cost of moving that money across borders. Knowing exactly how GST applies to your international transactions helps you budget accurately.

This guide breaks down exactly how GST applies to your inward and outward payments, how to calculate it without the headache, and when you are eligible for exemptions.

GST on foreign remittance is the 18% tax applied to the service charges involved in sending or receiving international payments. This includes bank processing fees, currency conversion margins, and any intermediary charges that happen during the transaction.

The GST applies to both inward remittances (money coming into India) and outward remittances (money going out of India). The key is knowing what exactly gets taxed, so you can calculate your true transaction cost and compare different payment providers fairly.

GST calculation on foreign remittance depends on the type of charge being applied. The 18% rate is standard, but what that 18% applies to varies based on how the service provider structures their fees.

Here's what you need to know about the calculation:

When banks or payment providers charge a clear processing fee (say ₹1,000 for handling your remittance), GST is straightforward. You pay 18% of ₹1,000, which is ₹180. Total charge becomes ₹1,180.

This is where the slab-based method comes in. The taxable value is calculated based on the gross amount of currency exchanged:

Here's how this works in practice:

Most payment providers bundle multiple charges together (processing fee + forex margin + intermediary fees). GST applies to the total of these charges. The calculation method they use should be transparent in your transaction statement.

Note: Always check your transaction statement to see which calculation method your bank or payment provider uses. Some apply the slab method, others charge a flat service fee with GST on top.

GST and TCS often appear together on the same bank advice, but they serve two completely different masters. One is a fee for a service; the other is a pre-payment of your income tax.

Here’s how they compare:

GST is what you pay for the service of processing your international payment. If your payment provider charges ₹2,000 in fees, you pay ₹360 as GST (18% of ₹2,000). This is the cost of using their service.

TCS is different. It applies under the Liberalized Remittance Scheme (LRS) when you send money abroad for specific purposes like overseas education, travel, or investments. For example, if you're paying a foreign software vendor ₹12 lakhs for licensed tools under the Liberalized Remittance Scheme, TCS applies to the ₹12 lakhs itself, not just the service fee. The TCS rate varies (5% to 20%) depending on the purpose and amount.

You can face both in the same transaction. For instance, paying an overseas consultant ₹8 lakhs for professional services can attract TCS on the remittance amount plus 18% GST on the bank's processing charges. These are separate charges calculated independently.

Tip: TCS is refundable when you file your income tax return if your actual tax liability is lower. GST paid on services can be claimed as input tax credit if you're GST registered and the service is for business use.

Inward remittances work differently from outward ones. For Indian exporters and freelancers, the tax treatment depends entirely on the nature of the transaction.

If you are receiving payment for services or goods provided to a client outside India, the transaction is classified as a zero-rated supply under GST regulations. This means no GST applies to the money coming in.

For example, if you're a freelance developer receiving $5,000 from a US client for software development work, that $5,000 is exempt from GST because it's a payment for exported services.

However, GST still applies to the service charges your bank or payment provider charges for processing that inward remittance. If the bank deducts ₹800 as their processing fee and forex conversion margin, you pay 18% GST on that ₹800 (which is ₹144).

Here's what typically attracts GST on inward remittances:

The payment amount itself remains GST-free for exports. This distinction matters because it affects how you invoice international clients and what you report in your GST returns.

Note: Keep your export invoices and documentation ready. Proper records prove your inward remittance qualifies as a zero-rated supply, which keeps GST off the actual payment amount.

Outward remittances always attract GST on the service charges, regardless of why you're sending money abroad. This includes processing fees, forex conversion charges, and any intermediary bank fees.

The calculation follows the same slab-based method or explicit service charge structure as inward remittances. If you're sending ₹15 lakhs abroad, the forex conversion taxable value is ₹5,500 + 0.1% of (₹15 lakhs - ₹10 lakhs = ₹5 lakhs) = ₹5,500 + ₹500 = ₹6,000. GST at 18% = ₹1,080.

Here's what gets taxed on outward remittances:

For business payments (like paying a foreign vendor for imported services or goods), GST is just one component of your total cost. You also need to factor in TCS if the payment falls under LRS and the amount crosses the threshold.

For example, if you're paying a foreign consultant ₹8 lakhs for services, and your bank charges 1.5% as total fees (₹12,000), you pay ₹2,160 as GST on those fees. The ₹8 lakhs payment itself might also attract TCS depending on the nature of the transaction.

Fixing GST compliance issues after they're flagged takes more time and money than getting it right from the start. Notice responses, penalty calculations, and credit reversals drain resources you could spend growing your business.

Here are the practices that keep you ahead of compliance requirements:

Compliance gets easier when you choose payment providers who handle documentation automatically and show clear GST breakdowns. Proper systems reduce manual work and keep you audit-ready without extra effort.

International payments involve multiple layers of fees and charges. To scale globally, you need a payment partner that breaks down every cost clearly so you can budget accurately and compare options fairly.

PayGlocal helps Indian businesses manage foreign remittances with full transparency on all charges. Here's how we make international payments clearer and more cost-effective:

PayGlocal processes your foreign remittances with instant FIRC generation, transparent pricing, and full compliance support.

GST on foreign remittance affects every international transaction you make, but it doesn't have to complicate your payment decisions. The 18% rate applies to service charges and forex conversion fees, not your actual remittance amounts. Knowing this helps you evaluate payment providers based on true costs and avoid platforms that hide charges in complex fee structures.

The slab-based calculation method means your GST liability changes with transaction size. Larger conversions generally work out more efficiently than multiple small ones when you factor in the minimum taxable values and GST impact. For businesses handling regular international payments, choosing a provider with transparent pricing saves money over time.

Ready to handle foreign remittances with complete cost clarity? Get started with PayGlocal today and see exactly what you pay on every international transaction.

With GST revenue hitting ₹22.08 lakh crore in 2024-25, tax authorities are more vigilant than ever, making it critical for you to account for every rupee deducted during the remittance process. GST on foreign remittance isn't a straightforward tax on the total amount you receive; it’s a nuanced charge on the cost of moving that money across borders. Knowing exactly how GST applies to your international transactions helps you budget accurately.

This guide breaks down exactly how GST applies to your inward and outward payments, how to calculate it without the headache, and when you are eligible for exemptions.

Key Takeaways

- GST applies at 18%: GST is charged on service fees, processing charges, and currency conversion margins, not on the total remittance amount.

- Inward remittances for exports: Generally exempt from GST when you're exporting goods or services, as these are zero-rated supplies.

- GST is different from TCS: TCS is an income tax advance on certain outward remittances, while GST is a service tax on fees.

- Calculation varies by amount: The forex conversion base changes depending on transaction size (up to ₹1 lakh, ₹1-10 lakhs, over ₹10 lakhs).

- Global payments with transparent pricing: PayGlocal provides clear pricing, helping you see exactly what you pay without hidden markups.

What is GST on foreign remittance?

GST on foreign remittance is the 18% tax applied to the service charges involved in sending or receiving international payments. This includes bank processing fees, currency conversion margins, and any intermediary charges that happen during the transaction.

The GST applies to both inward remittances (money coming into India) and outward remittances (money going out of India). The key is knowing what exactly gets taxed, so you can calculate your true transaction cost and compare different payment providers fairly.

How is GST calculated on foreign remittance?

GST calculation on foreign remittance depends on the type of charge being applied. The 18% rate is standard, but what that 18% applies to varies based on how the service provider structures their fees.

Here's what you need to know about the calculation:

- For explicit service charges:

When banks or payment providers charge a clear processing fee (say ₹1,000 for handling your remittance), GST is straightforward. You pay 18% of ₹1,000, which is ₹180. Total charge becomes ₹1,180.

- For currency conversion:

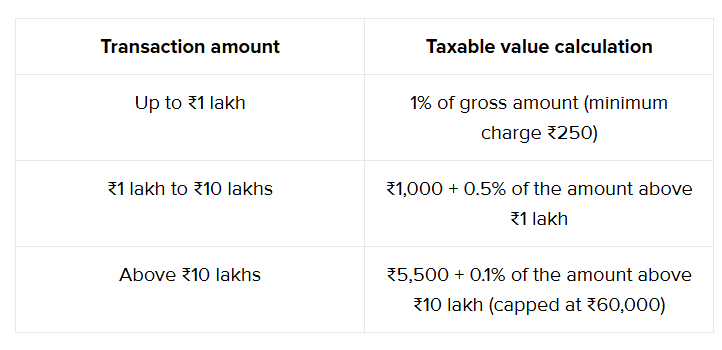

This is where the slab-based method comes in. The taxable value is calculated based on the gross amount of currency exchanged:

Here's how this works in practice:

- For instance, if you're converting ₹5 lakhs from USD to INR, the taxable value is calculated as ₹1,000 + 0.5% of (₹5 lakhs - ₹1 lakhs = ₹4 lakhs) = ₹1,000 + ₹2,000 = ₹3,000. GST at 18% on ₹3,000 comes to ₹540.

- If you're converting ₹50,000, the taxable value is 1% of ₹50,000 = ₹500. Since this is above the minimum of ₹250, the taxable value becomes ₹500. GST at 18% = ₹90.

- For combined charges:

Most payment providers bundle multiple charges together (processing fee + forex margin + intermediary fees). GST applies to the total of these charges. The calculation method they use should be transparent in your transaction statement.

Note: Always check your transaction statement to see which calculation method your bank or payment provider uses. Some apply the slab method, others charge a flat service fee with GST on top.

What is the difference between GST and TCS on foreign remittance?

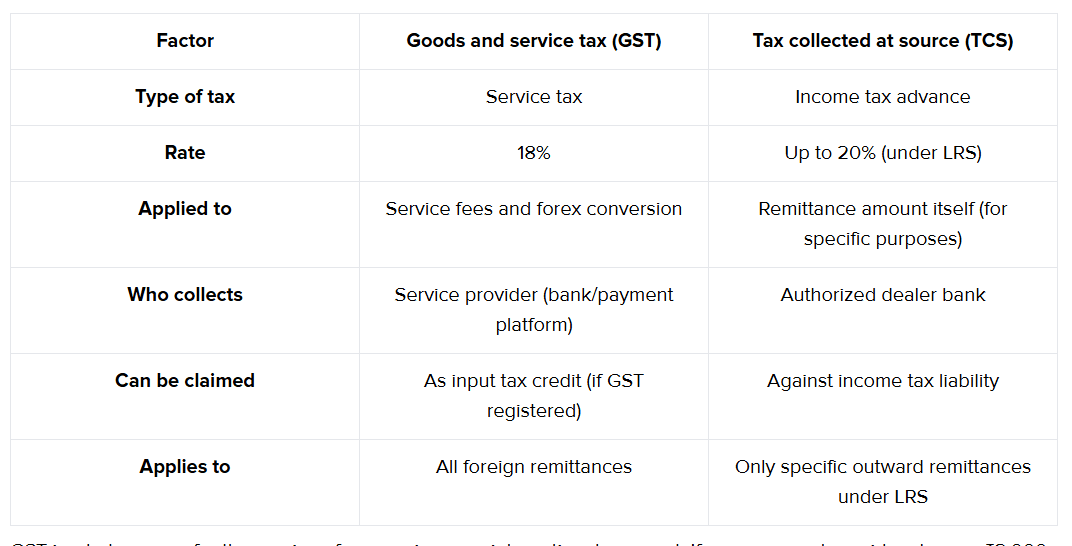

GST and TCS often appear together on the same bank advice, but they serve two completely different masters. One is a fee for a service; the other is a pre-payment of your income tax.

Here’s how they compare:

GST is what you pay for the service of processing your international payment. If your payment provider charges ₹2,000 in fees, you pay ₹360 as GST (18% of ₹2,000). This is the cost of using their service.

TCS is different. It applies under the Liberalized Remittance Scheme (LRS) when you send money abroad for specific purposes like overseas education, travel, or investments. For example, if you're paying a foreign software vendor ₹12 lakhs for licensed tools under the Liberalized Remittance Scheme, TCS applies to the ₹12 lakhs itself, not just the service fee. The TCS rate varies (5% to 20%) depending on the purpose and amount.

You can face both in the same transaction. For instance, paying an overseas consultant ₹8 lakhs for professional services can attract TCS on the remittance amount plus 18% GST on the bank's processing charges. These are separate charges calculated independently.

Tip: TCS is refundable when you file your income tax return if your actual tax liability is lower. GST paid on services can be claimed as input tax credit if you're GST registered and the service is for business use.

When does GST apply to inward remittances?

Inward remittances work differently from outward ones. For Indian exporters and freelancers, the tax treatment depends entirely on the nature of the transaction.

If you are receiving payment for services or goods provided to a client outside India, the transaction is classified as a zero-rated supply under GST regulations. This means no GST applies to the money coming in.

For example, if you're a freelance developer receiving $5,000 from a US client for software development work, that $5,000 is exempt from GST because it's a payment for exported services.

However, GST still applies to the service charges your bank or payment provider charges for processing that inward remittance. If the bank deducts ₹800 as their processing fee and forex conversion margin, you pay 18% GST on that ₹800 (which is ₹144).

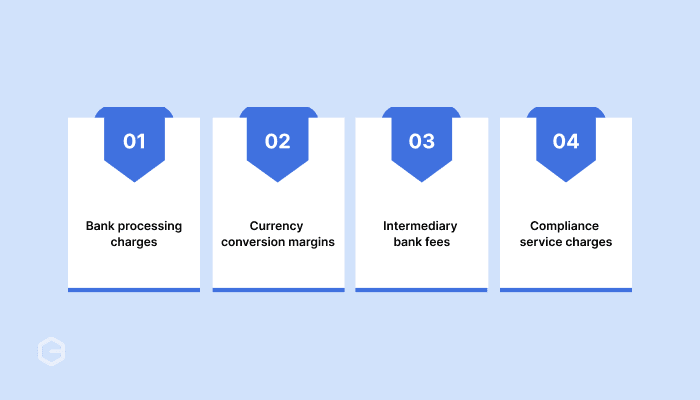

Here's what typically attracts GST on inward remittances:

- Bank processing charges: Fees charged by your bank for crediting the foreign payment to your account.

- Currency conversion margins: The spread between interbank rates and what you actually receive.

- Intermediary bank fees: Charges from correspondent banks involved in routing the payment.

- Compliance service charges: Fees for documentation like Foreign Inward Remittance Certificate (FIRC), if charged separately.

The payment amount itself remains GST-free for exports. This distinction matters because it affects how you invoice international clients and what you report in your GST returns.

Note: Keep your export invoices and documentation ready. Proper records prove your inward remittance qualifies as a zero-rated supply, which keeps GST off the actual payment amount.

When does GST apply to outward remittances?

Outward remittances always attract GST on the service charges, regardless of why you're sending money abroad. This includes processing fees, forex conversion charges, and any intermediary bank fees.

The calculation follows the same slab-based method or explicit service charge structure as inward remittances. If you're sending ₹15 lakhs abroad, the forex conversion taxable value is ₹5,500 + 0.1% of (₹15 lakhs - ₹10 lakhs = ₹5 lakhs) = ₹5,500 + ₹500 = ₹6,000. GST at 18% = ₹1,080.

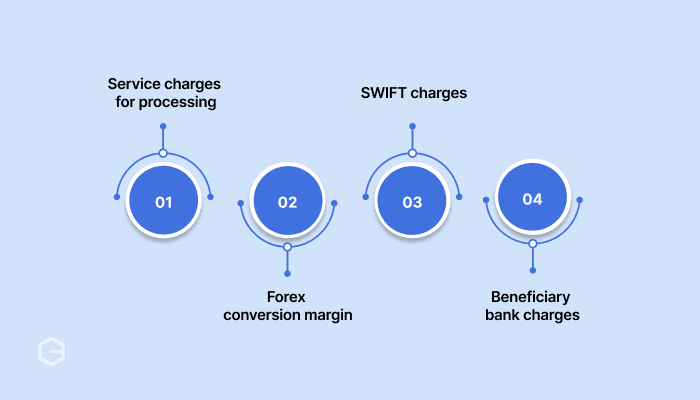

Here's what gets taxed on outward remittances:

- Service charges for processing: What your bank charges to execute the international transfer.

- Forex conversion margin: The difference between what you pay and the actual interbank exchange rate.

- SWIFT charges: Fees for routing the payment through the SWIFT network.

- Beneficiary bank charges: If you choose to cover charges on the receiving end, GST applies to those, too.

For business payments (like paying a foreign vendor for imported services or goods), GST is just one component of your total cost. You also need to factor in TCS if the payment falls under LRS and the amount crosses the threshold.

For example, if you're paying a foreign consultant ₹8 lakhs for services, and your bank charges 1.5% as total fees (₹12,000), you pay ₹2,160 as GST on those fees. The ₹8 lakhs payment itself might also attract TCS depending on the nature of the transaction.

What are some best practices for GST compliance on foreign remittance?

Fixing GST compliance issues after they're flagged takes more time and money than getting it right from the start. Notice responses, penalty calculations, and credit reversals drain resources you could spend growing your business.

Here are the practices that keep you ahead of compliance requirements:

- Maintain transaction documentation: Keep all invoices, payment confirmations, and bank statements showing GST charged separately. These prove your payments and support input tax credit claims.

- Get FIRC for all inward remittances: Foreign Inward Remittance Certificate validates your export income and GST exemption claims. Request it from your bank or payment provider immediately after settlement.

- File LUT if you're exporting services: Letter of Undertaking lets you receive export payments without paying IGST upfront, improving your cash flow. File it annually through the GST portal.

- Claim input tax credit on business remittances: If you're GST registered and the remittance is for business purposes, claim the 18% GST paid on service charges. Don't let these credits expire unused.

- Report forex gains and losses correctly: Currency fluctuation impacts your books. Maintain clear records of exchange rates at transaction time versus settlement to handle accounting accurately.

- Separate personal and business remittances: Don't mix LRS-covered personal transfers with business payments. Keep clear categorization to avoid confusion during audits or return filing.

- Review provider GST breakdowns monthly: Check that your payment provider's GST calculation matches the prescribed slab method. Discrepancies caught early save disputes later.

Compliance gets easier when you choose payment providers who handle documentation automatically and show clear GST breakdowns. Proper systems reduce manual work and keep you audit-ready without extra effort.

Handle foreign remittances with clear costs at PayGlocal

International payments involve multiple layers of fees and charges. To scale globally, you need a payment partner that breaks down every cost clearly so you can budget accurately and compare options fairly.

PayGlocal helps Indian businesses manage foreign remittances with full transparency on all charges. Here's how we make international payments clearer and more cost-effective:

- Transparent pricing: See exactly what you pay with no hidden markups or surprise charges, all fees and applicable taxes shown upfront.

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with transparent forex conversion and clear cost breakdown on service fees.

- Dynamic checkout: Offer your global customers a seamless payment experience while you get complete visibility into transaction costs.

- Recurring payments: Manage subscription billing for international customers with predictable costs.

- One platform: Track all your international transactions, see detailed fee breakdowns, and download compliance documents from a single dashboard.

PayGlocal processes your foreign remittances with instant FIRC generation, transparent pricing, and full compliance support.

Final Thoughts

GST on foreign remittance affects every international transaction you make, but it doesn't have to complicate your payment decisions. The 18% rate applies to service charges and forex conversion fees, not your actual remittance amounts. Knowing this helps you evaluate payment providers based on true costs and avoid platforms that hide charges in complex fee structures.

The slab-based calculation method means your GST liability changes with transaction size. Larger conversions generally work out more efficiently than multiple small ones when you factor in the minimum taxable values and GST impact. For businesses handling regular international payments, choosing a provider with transparent pricing saves money over time.

Ready to handle foreign remittances with complete cost clarity? Get started with PayGlocal today and see exactly what you pay on every international transaction.