Introduction

According to recent data, more than 7.28 crore income tax returns were filed in 2024–25, which is 7.5% higher than the previous assessment year.

This indicates that more businesses and individuals are dealing with tax filing requirements.

If you're a small business owner earning under ₹2–3 crore annually, Section 44AD of the Income Tax Act can help you avoid maintaining detailed books of account and undergoing tax audits.

It’s a taxation scheme designed to simplify compliance by allowing you to declare income at a fixed rate without tracking every expense.

In this guide, we cover everything about Section 44AD — from eligibility and turnover limits to benefits and filing requirements — so you can decide if it's the right fit for your business.

Key Takeaways

- What Section 44AD offers: A presumptive taxation scheme for small businesses to declare income at 8% (or 6% for digital transactions) of turnover without maintaining detailed books.

- Who can use it: Resident individuals, HUFs, and partnership firms (not LLPs) with turnover up to ₹2 crore, or ₹3 crore if cash receipts are under 5%.

- Digital payment incentive: If 95% or more receipts are through digital modes, you declare only 6% as taxable income instead of 8%.

- Five-year commitment: Once opted, you must continue for 5 years or face restrictions and audit requirements.

- For global businesses: If you're collecting payments internationally, PayGlocal simplifies global transactions and compliance.

What is Section 44AD of the Income Tax Act?

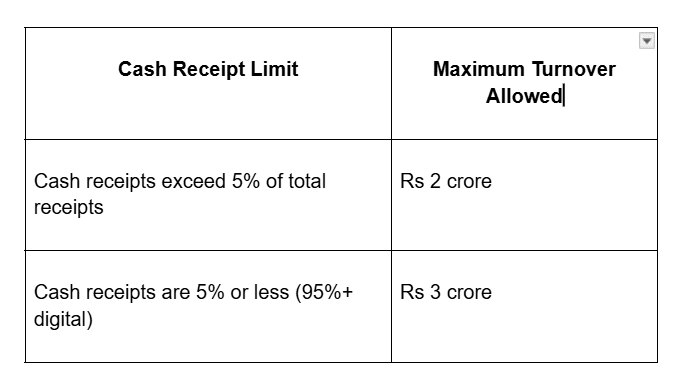

Section 44AD is a presumptive taxation scheme for small taxpayers running businesses with turnover below ₹2 crore (or ₹3 crore under specific conditions).

Instead of maintaining detailed books of account and calculating actual profits, you declare a fixed percentage of your turnover as taxable income.

Example:

If your business turnover is ₹50 lakh, you declare ₹4 lakh (8% of ₹50 lakh) as taxable income.

No need to track every expense or hire an accountant to maintain complex records.

This scheme was introduced to reduce compliance burdens on small businesses, helping them save time and focus on growth.

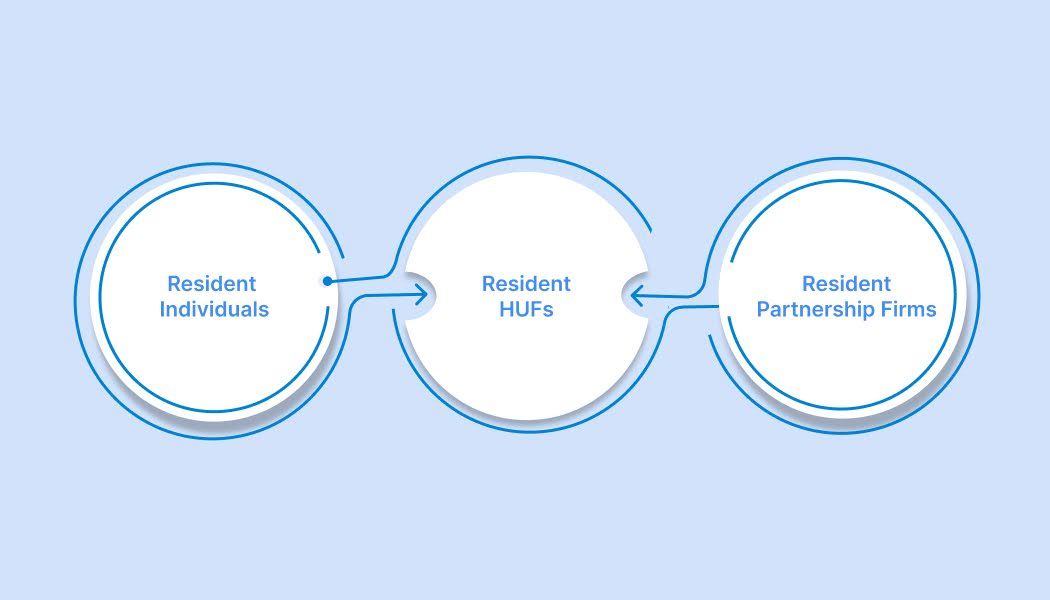

Who is Eligible for Section 44AD?

Not every business owner can use Section 44AD. Here’s who qualifies:

- Resident individuals: Solo business owners who are Indian residents.

- Resident HUFs (Hindu Undivided Families): Family-run businesses under HUF structure.

- Resident partnership firms: Traditional partnership firms (not LLPs).

Your business must meet the turnover criteria, and you should not have claimed deductions under Sections 10A, 10AA, 10B, 10BA, or 80HH to 80RRB in the same year.

What are the Turnover Limits under Section 44AD?

- If your cash receipts are 5% or less, you qualify for a higher turnover limit of ₹3 crore.

- This encourages digital payments and helps you qualify even with higher revenue.

- Non-account payee cheques or bank drafts count as cash receipts, so prioritize digital transactions to maximize benefits.

Which Businesses Cannot Use Section 44AD?

You cannot use this scheme if you:

- Run a goods carriage business (covered under Section 44AE).

- Earn commission or brokerage income (e.g., insurance agents, brokers).

- Operate an agency business acting on behalf of others.

- Work in specified professions such as doctors, lawyers, engineers, architects, accountants, consultants, or designers (covered under Section 44ADA).

Example:

An insurance agent earning commission cannot opt for 44AD.

Similarly, a logistics company owning goods vehicles should refer to Section 44AE instead.

How is Income Calculated under Section 44AD?

- 8% of turnover: If receipts are through any mode (cash or digital).

- 6% of turnover: If 95% or more receipts are through digital modes like UPI, NEFT, RTGS, cards, or account payee cheques.

Example:

If turnover = ₹80 lakh

- With ₹76 lakh (95%) digital receipts → taxable income = ₹4.8 lakh (6%)

- With <95% digital receipts → taxable income = ₹6.4 lakh (8%)

You may declare a higher income voluntarily, but not lower unless you maintain books and undergo an audit.

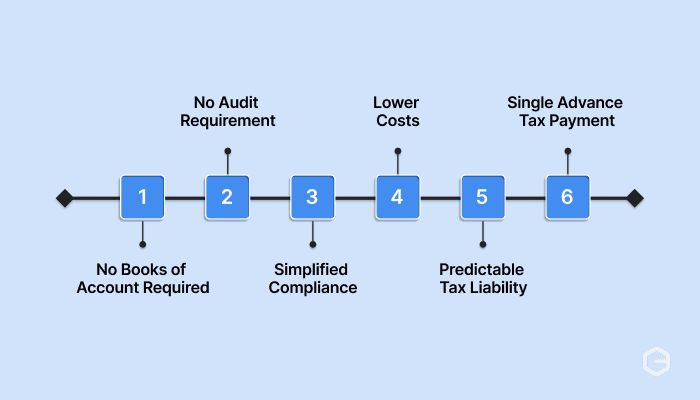

What are the Benefits of Section 44AD?

- No books required: Exemption from maintaining detailed accounting records.

- No audit requirement: Save on audit fees and compliance stress.

- Simplified filing: File returns using ITR-4 (Sugam) form.

- Lower costs: No need for year-round accountant support.

- Predictable tax liability: Easier planning based on turnover.

- Single advance tax payment: Pay full advance tax by March 15th instead of quarterly installments.

Example:

A retailer with ₹1.5 crore turnover can declare ₹12 lakh (8%) or ₹9 lakh (6%) and file ITR-4 without maintaining sales or expense registers.

Key Considerations under Section 44AD

- No expense deductions: 8% or 6% is final taxable income — no further deductions allowed.

- Partnership remuneration: Firms can deduct partner salary and interest per Income Tax limits.

- No separate depreciation claim: Depreciation is included in presumptive income.

- Five-year lock-in: Must continue for 5 years once opted.

* Opting out early disqualifies you for next 5 years and requires books & audit.

- Higher tax for low-margin businesses: If your actual profit margin <8%, presumptive tax may increase your tax burden.

Example:

A restaurant with 5% actual profit will pay tax on 8% income — resulting in higher tax than actual profits.

What Happens if You Opt Out of Section 44AD?

- Mandatory for 5 years: Once chosen, must continue for the next 5 years.

- Restrictions for early exit: Declaring lower profits (<8%/6%) ends eligibility for 5 years.

- Books & audit required: After opting out, you must maintain books under Section 44AA and get audited under Section 44AB if income exceeds exemption limits.

- Exception: If turnover exceeds ₹2–3 crore, the restriction doesn’t apply (scheme ineligible anyway).

How to File ITR Under Section 44AD

- Form: Use ITR-4 (Sugam) for presumptive taxpayers.

- Declare presumptive income: Enter turnover and calculate 8% or 6%.

- Advance tax: Pay full by March 15th.

- Due date: File by July 31st of the assessment year.

- No audit report needed: No need to attach statements or reports.

Manage Global Payments Easily with PayGlocal

Running a business is about growth — not paperwork.

While Section 44AD simplifies domestic filing, international payments add complexity.

If you’re a freelancer, exporter, or global service provider, managing multiple currencies and compliance can be tough.

That’s where PayGlocal helps.

How PayGlocal Supports Your Business

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries with local USD, GBP, EUR, and CAD accounts.

- Unified dashboard: Manage all transactions, settlements, and reports in one place.

- Sanction screening: Stay compliant with global AML regulations.

- Global payment options: Accept international cards, local methods, and digital payments.

- Zero fixed costs: Pay only when you transact — no setup or platform fees.

PayGlocal makes cross-border transactions seamless, helping you accept payments globally and settle locally.

Final Thoughts

Section 44AD offers an efficient way for small businesses to reduce compliance effort and simplify tax filing.

It’s ideal for traders, retailers, and service providers with turnover under ₹2–3 crore who prefer predictable taxation and less paperwork.

However, if your margins are low or you expect rapid growth, evaluate if the five-year commitment and expense limitations suit your business.

If you’re expanding internationally, pair Section 44AD with PayGlocal’s global payment solution to stay compliant while scaling efficiently.

👉 Get started with PayGlocal today to simplify international payments and keep your business tax-ready.