SWIFT Codes and Routing numbers both facilitate money transfers, but they serve different purposes. It’s essential to understand the differences between these banking codes to prevent errors in transactions.

With the global cross-border payments market projected to reach USD 221.60 billion in 2025, the need for accurate and efficient payment routing is more critical than ever. Selecting the incorrect code can result in delays, failed transactions, or unnecessary fees.

This guide explains the differences between SWIFT Codes and routing numbers, their uses, and how to locate them. Continue reading until the end to gain a comprehensive knowledge of when to use each, ensuring faster and error-free payment processing.

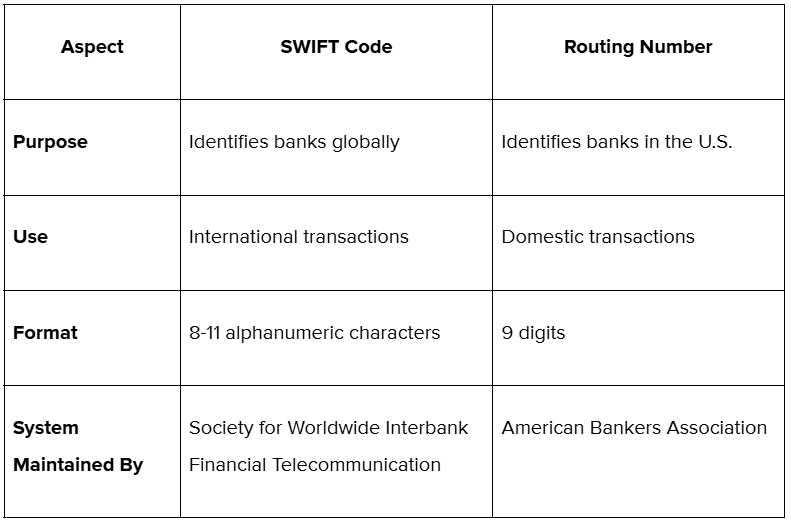

SWIFT codes, also known as Business Identifier Codes (BICs), play a crucial role in facilitating international transactions. They ensure that your money is accurately directed to banks across different countries. Each SWIFT code consists of a combination of characters that represent specific information about the bank: a bank code, country code, location code, and an optional branch code.

For instance, the SWIFT code CHASUS33 identifies Chase Bank in the United States, where "CHAS" is the bank code, "US" indicates the country, and "33" specifies the location.

The structured nature of SWIFT codes is integral to global finance, ensuring that every transfer is processed accurately. When you send money internationally, these codes help banks identify each other, facilitating smooth communication and reducing the risk of errors. For example, businesses rely on SWIFT codes to make and receive payments for international trade, including imports and exports.

In many cases, these transactions are supported by MT103 messages, a standardized format that provides detailed tracking and transparency for cross-border payments. Knowing how SWIFT codes and MT103 work together can help users ensure smoother, more secure transfers.

Having defined SWIFT codes, let’s shift our focus to routing numbers and their specific role in domestic banking:

Routing numbers, on the other hand, serve a distinct purpose. Used exclusively in the United States, these 9-digit codes identify specific banks for domestic transactions. The first two digits correspond to the Federal Reserve Bank location, while the remaining digits pinpoint the particular bank and a check digit for verification.

For example, if you see a routing number like 021000021, it directs funds to JPMorgan Chase Bank.

Routing numbers are essential for various domestic operations, including direct deposits, wire transfers, and automated bill payments. Without these codes, your transactions could face delays or errors, potentially causing inconvenience.

Now that we’ve covered both types of codes, let’s take a look at the essential differences between SWIFT Code and Routing Number.

Experience a better way to manage international payments. PayGlocal ensures secure, low-cost payment collections with excellent success rates

Now, with a complete knowledge of SWIFT Code and Routing Number, let’s explore the differences in their structure and format.

The structural differences between SWIFT codes and routing numbers further clarify their distinct functions. SWIFT codes consist of 8 to 11 alphanumeric characters. The format typically includes:

In contrast, routing numbers are fixed at nine digits in a numeric format. For example, a routing number like 026009593 gives you all the necessary information about the specific U.S. bank in question. This straightforward design allows for easy identification and accuracy in domestic transactions.

Now that you know how these codes differ structurally, let’s look at how to find SWIFT codes and routing numbers easily.

Finding the correct SWIFT code versus the routing Number is essential for ensuring that your transactions are processed smoothly.

Here are the common ways to find a Routing number:

Now, here are the standard methods to find the SWIFT Code:

These methods help ensure you use the correct SWIFT code when sending money internationally. While SWIFT codes are essential for global transfers, domestic banking in India uses IFSC codes to identify individual branches.

Now, let’s consider the situations in which you should use SWIFT codes versus routing numbers.

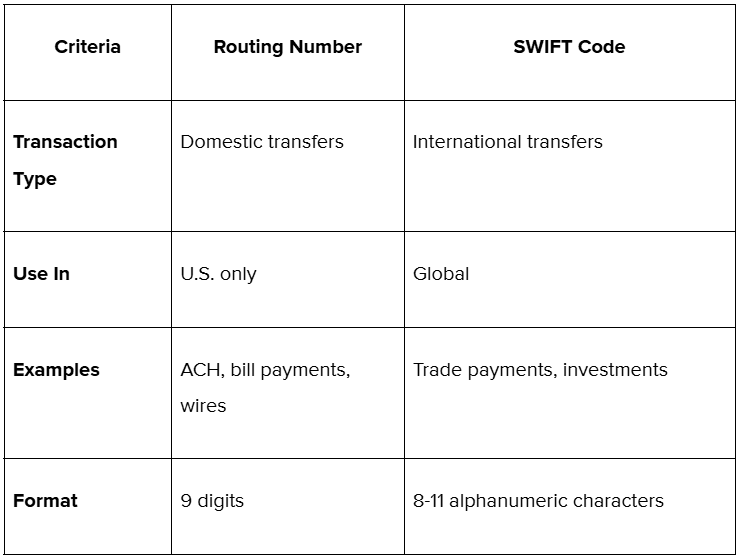

SWIFT codes and routing numbers serve distinct purposes in financial transactions. Knowing when to use each is crucial for ensuring smooth and accurate transfers, whether domestic or international. While both identifiers help route payments, the context in which they are applied makes all the difference.

Routing numbers are tailored for domestic banking within the U.S., whereas SWIFT codes connect banks across international borders. Knowing their specific applications helps prevent errors and avoid unnecessary delays.

Routing numbers are strictly for transactions within the United States. They are used in scenarios that involve U.S. banks and accounts exclusively. These include direct deposits, bill payments, and internal wire transfers. The 9-digit code ensures that funds are routed correctly within the domestic banking network.

Common uses of routing numbers:

In these situations, the routing number is the key to identifying the bank's location within the U.S. financial system. It ensures that money flows efficiently between institutions without involving international channels.

Now, let’s see when to use SWIFT code in transactions.

SWIFT codes are essential for international transactions. They connect banks and financial institutions globally, ensuring that funds are routed accurately across borders. This global identifier is particularly crucial for businesses or individuals engaged in foreign trade, remittances, or investments.

Common uses of SWIFT codes:

Want to simplify your international payments? Sign up with PayGlocal now and experience seamless payment management across multiple currencies.

Now, let’s explore some of the top factors to consider when choosing between the usage of SWIFT Code and Routing Number.

The choice between a routing number and a SWIFT code depends on three key factors: transaction type, geographic location, and the banks involved.

For example, let’s say there’s a U.S.-based company paying a supplier overseas. The payer uses a routing number to initiate the transaction from their local bank and a SWIFT code to route the payment to the supplier’s international bank.

With the basics of when to use the SWIFT code and Routing number, it’s also essential to consider some best practices to avoid common errors in transactions.

For businesses that handle both domestic and international transactions, maintaining accurate records of SWIFT codes and routing numbers is crucial. Mistakes can lead to delays, rejected payments, or even the loss of funds. Here are some best practices to consider while using SWIFT Code and Routing Number:

By following these practices, businesses can minimize payment errors and maintain trust in their financial operations. However, managing these processes manually can still be time-consuming, especially when scaling globally.

That’s where innovative payment solutions come in. Let’s examine how PayGlocal streamlines global and domestic transactions for businesses.

Knowing when to use a SWIFT code or routing number is critical for smooth payment execution. But even with that knowledge, managing cross-border and domestic transactions can be tedious, especially when you’re dealing with multiple banks, currencies, and compliance requirements.

PayGlocal offers a unified platform that streamlines this entire process, making payments faster, safer, and more scalable. Here’s how PayGlocal can help businesses like yours:

By integrating these services, PayGlocal simplifies payment operations, allowing you to focus confidently on scaling your business across borders and currencies.

Knowing the differences between SWIFT codes and routing numbers is essential for anyone engaged in financial transactions, whether domestic or international. Knowing when to use each code can save you time and prevent costly errors.

As global commerce continues to expand, the importance of using these identifiers accurately also increases. So, the next time you’re preparing to send money, remember to double-check the code you need to use. Identifying the SWIFT Code vs. the Routing Number and staying informed makes all the difference in your banking experience.

Ready to make your payment processes hassle-free? Sign up with PayGlocal now and get access to global payment methods, recurring payments, dynamic checkout, and more.

With the global cross-border payments market projected to reach USD 221.60 billion in 2025, the need for accurate and efficient payment routing is more critical than ever. Selecting the incorrect code can result in delays, failed transactions, or unnecessary fees.

This guide explains the differences between SWIFT Codes and routing numbers, their uses, and how to locate them. Continue reading until the end to gain a comprehensive knowledge of when to use each, ensuring faster and error-free payment processing.

Key Takeaways:

- SWIFT code and routing number: SWIFT codes are used for international money transfers, while routing numbers are used only for domestic transactions within the U.S.

- Format matters: SWIFT codes are 8–11 alphanumeric characters long and identify the bank, country, and branch. Routing numbers are 9-digit numerical codes identifying U.S. banks for local transfers.

- Use case determines code: Use a routing number for ACH payments, salary deposits, and bill payments in the U.S. Use a SWIFT code for sending or receiving money across international borders.

- How to find them: You can find routing numbers on checks, bank statements, or bank websites. SWIFT codes are typically available on a bank's website, in bank statements, or in online directories.

- Accuracy is critical: Using the wrong code can delay your transaction, cause rejections, or result in funds being misrouted. Always verify the code before making payments.

What are SWIFT codes?

SWIFT codes, also known as Business Identifier Codes (BICs), play a crucial role in facilitating international transactions. They ensure that your money is accurately directed to banks across different countries. Each SWIFT code consists of a combination of characters that represent specific information about the bank: a bank code, country code, location code, and an optional branch code.

For instance, the SWIFT code CHASUS33 identifies Chase Bank in the United States, where "CHAS" is the bank code, "US" indicates the country, and "33" specifies the location.

The structured nature of SWIFT codes is integral to global finance, ensuring that every transfer is processed accurately. When you send money internationally, these codes help banks identify each other, facilitating smooth communication and reducing the risk of errors. For example, businesses rely on SWIFT codes to make and receive payments for international trade, including imports and exports.

In many cases, these transactions are supported by MT103 messages, a standardized format that provides detailed tracking and transparency for cross-border payments. Knowing how SWIFT codes and MT103 work together can help users ensure smoother, more secure transfers.

Having defined SWIFT codes, let’s shift our focus to routing numbers and their specific role in domestic banking:

What are routing numbers?

Routing numbers, on the other hand, serve a distinct purpose. Used exclusively in the United States, these 9-digit codes identify specific banks for domestic transactions. The first two digits correspond to the Federal Reserve Bank location, while the remaining digits pinpoint the particular bank and a check digit for verification.

For example, if you see a routing number like 021000021, it directs funds to JPMorgan Chase Bank.

Routing numbers are essential for various domestic operations, including direct deposits, wire transfers, and automated bill payments. Without these codes, your transactions could face delays or errors, potentially causing inconvenience.

Now that we’ve covered both types of codes, let’s take a look at the essential differences between SWIFT Code and Routing Number.

SWIFT code vs. routing number

Experience a better way to manage international payments. PayGlocal ensures secure, low-cost payment collections with excellent success rates

Now, with a complete knowledge of SWIFT Code and Routing Number, let’s explore the differences in their structure and format.

Differences in structure and format

The structural differences between SWIFT codes and routing numbers further clarify their distinct functions. SWIFT codes consist of 8 to 11 alphanumeric characters. The format typically includes:

- Bank code: The first four characters identify the bank.

- Country code: The next two characters represent the country.

- Location code: The following two characters indicate the location.

- Branch code (optional): The last three characters specify a particular branch.

In contrast, routing numbers are fixed at nine digits in a numeric format. For example, a routing number like 026009593 gives you all the necessary information about the specific U.S. bank in question. This straightforward design allows for easy identification and accuracy in domestic transactions.

Now that you know how these codes differ structurally, let’s look at how to find SWIFT codes and routing numbers easily.

How to find SWIFT codes and routing numbers?

Finding the correct SWIFT code versus the routing Number is essential for ensuring that your transactions are processed smoothly.

How to find the routing number?

Here are the common ways to find a Routing number:

- On a check: Look at the bottom-left corner of a check. It’s the first nine digits printed.

- Bank statements: Many banks include routing numbers in both online and paper account statements.

- Bank website or app: Banks often list their routing numbers on their official websites or mobile apps under the “Contact” or “Help” sections.

- Contact the bank: Visit a branch or call customer support to get accurate information.

- Search online: Use a verified ABA routing directory to locate a bank’s routing number.

How to find the SWIFT code?

Now, here are the standard methods to find the SWIFT Code:

- Bank account statements: Many banks include their SWIFT code on account statements, especially for accounts that support international transactions.

- Official bank website or app: Financial institutions typically list their SWIFT codes on their websites, usually under the “International Banking” section.

- Customer support: For precise and up-to-date information, contacting the bank directly is a reliable option.

- Online SWIFT directories: Verified online directories provide a searchable database of SWIFT codes for banks worldwide.

These methods help ensure you use the correct SWIFT code when sending money internationally. While SWIFT codes are essential for global transfers, domestic banking in India uses IFSC codes to identify individual branches.

Now, let’s consider the situations in which you should use SWIFT codes versus routing numbers.

When to use SWIFT code vs. routing number?

SWIFT codes and routing numbers serve distinct purposes in financial transactions. Knowing when to use each is crucial for ensuring smooth and accurate transfers, whether domestic or international. While both identifiers help route payments, the context in which they are applied makes all the difference.

Routing numbers are tailored for domestic banking within the U.S., whereas SWIFT codes connect banks across international borders. Knowing their specific applications helps prevent errors and avoid unnecessary delays.

When to use routing numbers?

Routing numbers are strictly for transactions within the United States. They are used in scenarios that involve U.S. banks and accounts exclusively. These include direct deposits, bill payments, and internal wire transfers. The 9-digit code ensures that funds are routed correctly within the domestic banking network.

Common uses of routing numbers:

- Direct deposits: Employers use routing numbers to deposit salaries directly into employee accounts. For example, payroll for a U.S.-based workforce relies on routing numbers to distribute funds.

- ACH transfers: Automated Clearing House (ACH) transfers use routing numbers for recurring transactions such as mortgage payments, vendor invoices, or subscription services.

- Domestic wire transfers: Transferring funds between U.S. accounts requires routing numbers to identify the sender and recipient banks.

- Check processing: When a check is deposited or cashed, the routing number directs the payment to the correct bank.

In these situations, the routing number is the key to identifying the bank's location within the U.S. financial system. It ensures that money flows efficiently between institutions without involving international channels.

Now, let’s see when to use SWIFT code in transactions.

When to use SWIFT codes?

SWIFT codes are essential for international transactions. They connect banks and financial institutions globally, ensuring that funds are routed accurately across borders. This global identifier is particularly crucial for businesses or individuals engaged in foreign trade, remittances, or investments.

Common uses of SWIFT codes:

- International wire transfers: When transferring money to an account in another country, the SWIFT code ensures the funds reach the correct bank. For example, a business making payments to overseas suppliers needs the recipient bank's SWIFT code.

- Foreign trade payments: Importers and exporters rely on SWIFT codes to send or receive payments from international buyers and sellers.

- International investments: Investors moving funds into foreign markets require SWIFT codes to complete transactions securely and efficiently.

- Multi-currency transactions: Transactions involving currency exchanges often require SWIFT codes to ensure that the funds are processed through the appropriate institution.

Want to simplify your international payments? Sign up with PayGlocal now and experience seamless payment management across multiple currencies.

Now, let’s explore some of the top factors to consider when choosing between the usage of SWIFT Code and Routing Number.

How to decide which one to use?

The choice between a routing number and a SWIFT code depends on three key factors: transaction type, geographic location, and the banks involved.

- Transaction type: Domestic payments, such as ACH transfers, bill payments, or salary deposits, require routing numbers. Cross-border wire transfers or payments for international trade necessitate SWIFT codes.

- Geographic location: Transactions within the U.S. use routing numbers, while international transfers rely on SWIFT codes.

- Intermediary banks: International transactions sometimes involve multiple intermediary banks. In such cases, SWIFT codes are required for every bank in the transfer chain to ensure the funds reach their destination.

For example, let’s say there’s a U.S.-based company paying a supplier overseas. The payer uses a routing number to initiate the transaction from their local bank and a SWIFT code to route the payment to the supplier’s international bank.

With the basics of when to use the SWIFT code and Routing number, it’s also essential to consider some best practices to avoid common errors in transactions.

Best practices for using SWIFT code and routing number

For businesses that handle both domestic and international transactions, maintaining accurate records of SWIFT codes and routing numbers is crucial. Mistakes can lead to delays, rejected payments, or even the loss of funds. Here are some best practices to consider while using SWIFT Code and Routing Number:

- Verifying bank details: Always confirm the correct routing number or SWIFT code with the recipient’s bank before processing payments.

- Using payment platforms: Many financial platforms and payment gateways automate this process, selecting the appropriate identifier based on the transaction details.

- Tracking payments: For large or frequent transfers, tracking systems can help monitor the transaction and resolve any issues quickly.

By following these practices, businesses can minimize payment errors and maintain trust in their financial operations. However, managing these processes manually can still be time-consuming, especially when scaling globally.

That’s where innovative payment solutions come in. Let’s examine how PayGlocal streamlines global and domestic transactions for businesses.

How does PayGlocal simplify international and domestic payments?

Knowing when to use a SWIFT code or routing number is critical for smooth payment execution. But even with that knowledge, managing cross-border and domestic transactions can be tedious, especially when you’re dealing with multiple banks, currencies, and compliance requirements.

PayGlocal offers a unified platform that streamlines this entire process, making payments faster, safer, and more scalable. Here’s how PayGlocal can help businesses like yours:

- Dynamic Checkout: Whether you're collecting payments from within India or abroad, PayGlocal’s intelligent checkout adapts in real-time to offer the most suitable local or global payment option, ensuring seamless customer experience.

- Card Payments: Accept card payments from customers across the globe with higher success rates and lower processing friction. PayGlocal supports major card networks with built-in fraud checks and security.

- Global Payment Methods: Go beyond cards. Collect payments via alternative methods preferred in different countries (such as net banking, UPI, wallets, or Buy Now Pay Later), expanding your global reach without additional integration hassle.

- Recurring Payments: For subscription-based businesses or regular invoice cycles, PayGlocal enables easy setup and management of recurring payments, eliminating the need for manual follow-ups and errors.

- Multi-Currency Account: Accept and settle payments in multiple currencies with a single account, reducing conversion losses and simplifying treasury operations.

- One Platform for All: Instead of juggling different banking partners, APIs, and reconciliation tools, PayGlocal offers an all-in-one dashboard to manage everything, from transaction history to chargebacks, across domestic and international payments.

- Sanction Screening & Compliance: With built-in sanction screening and compliance monitoring, PayGlocal helps you stay compliant with international regulations, reducing the risk of delays or blocked transactions.

By integrating these services, PayGlocal simplifies payment operations, allowing you to focus confidently on scaling your business across borders and currencies.

Conclusion

Knowing the differences between SWIFT codes and routing numbers is essential for anyone engaged in financial transactions, whether domestic or international. Knowing when to use each code can save you time and prevent costly errors.

As global commerce continues to expand, the importance of using these identifiers accurately also increases. So, the next time you’re preparing to send money, remember to double-check the code you need to use. Identifying the SWIFT Code vs. the Routing Number and staying informed makes all the difference in your banking experience.

Ready to make your payment processes hassle-free? Sign up with PayGlocal now and get access to global payment methods, recurring payments, dynamic checkout, and more.