GST collections in India reached ₹22.08 lakh crore in 2024-25, growing 9.4% from the previous year. This growth indicates more businesses filing GST to ensure proper compliance with all regulations.

When it comes to GST, e-invoicing is one of the most important components. But what exactly is the e-invoice limit, and does it apply to you?

In this guide, we break down the e-invoice limit in detail, covering who needs to follow the e-invoicing limit, when to report your invoices, and which documents are required to stay compliant. So, let’s get started.

The e-invoice limit refers to two compliance requirements: the turnover threshold and the time limit. Let’s learn more about each of them.

The e-invoicing turnover threshold determines whether your business must generate e-invoices at all. Currently, any business with an Annual Aggregate Turnover (AATO) exceeding ₹5 crore in any financial year from 2017-18 onwards must use e-invoicing for eligible transactions.

This threshold applies at the PAN level, which means you add up the turnover across all your GSTINs nationwide. Once you cross this limit in any year, you stay in the e-invoicing system unless you qualify for a specific exemption.

For example, if you have three GSTINs with ₹2 crore, ₹2 crore, and ₹1.5 crore, respectively, your total AATO is ₹5.5 crore, which means e-invoicing applies.

From April 1, 2025, businesses with an AATO of ₹10 crore or more must report their e-invoices to the Invoice Registration Portal within 30 days of the invoice date. If you miss this window, the IRP system will reject your invoice submission. This rule previously applied only to businesses above ₹100 crore, but now covers a much larger group.

For instance, if you run a software export business that earned ₹8 crore in FY 2022-23, you must generate e-invoices for all your B2B transactions. If your turnover is ₹12 crore, you also need to report each invoice within 30 days. These limits work together to define your compliance obligations.

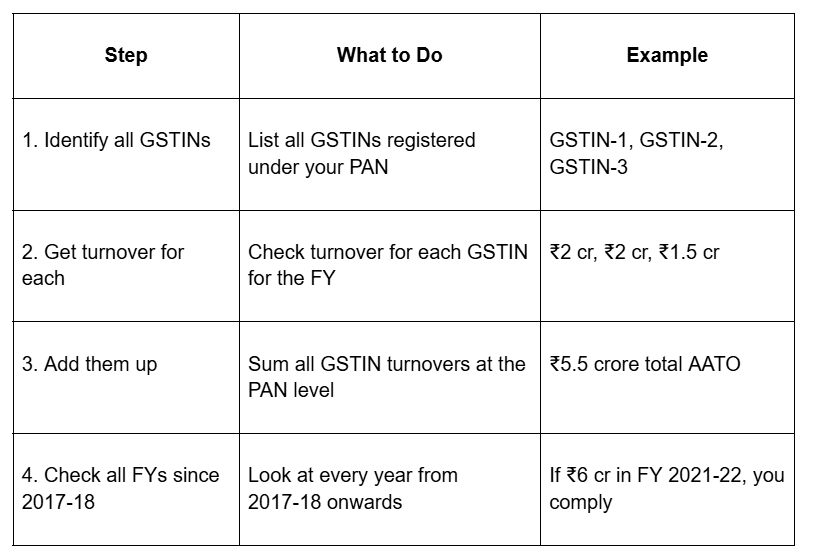

Calculating AATO correctly is the first step in knowing whether you need to comply with e-invoicing.

Annual Aggregate Turnover means the total value of all taxable supplies, exempt supplies, exports, and inter-state supplies made by you under a single PAN. Here's how to calculate it:

Tip: You can verify your AATO through the GST portal by logging into your account and checking your turnover details across all registered GSTINs. Make sure you monitor your turnover throughout the year, especially as you approach the limit, so you can plan your compliance setup in advance.

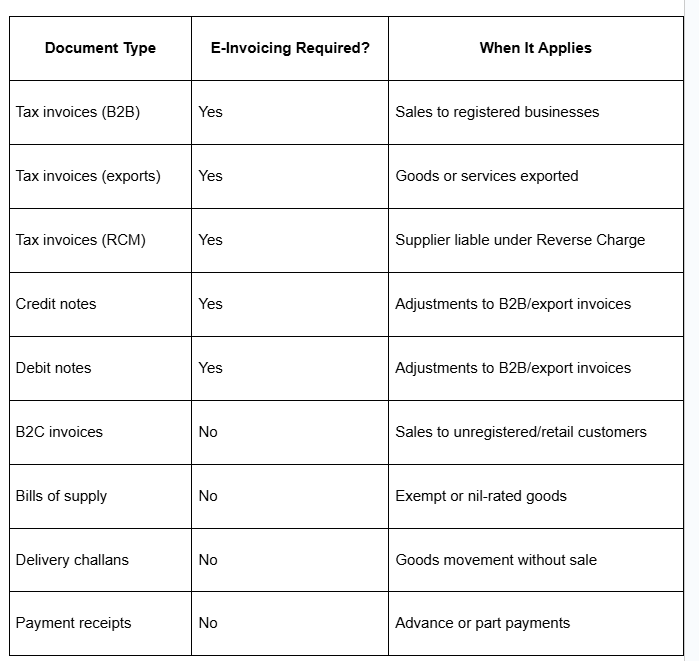

Not every invoice or document requires e-invoicing, so knowing the scope helps you comply efficiently. Here's a quick view of what does and doesn't need e-invoicing:

For example, if you run a D2C e-commerce business and sell directly to individual consumers, those invoices don't need IRNs even if your turnover exceeds ₹5 crore. But if you also supply to other businesses or export products, those B2B and export invoices require e-invoicing.

Even if your turnover exceeds the ₹5 crore threshold, you may be exempt from e-invoicing if your business falls under specific categories.

Here are the exemptions that apply regardless of turnover:

One important clarification is the SEZ distinction. If you're a notified taxpayer supplying goods or services to an SEZ unit, you still need to generate e-invoices for those transactions because they qualify as B2B or export supplies from your perspective.

For instance, if you operate a logistics company providing goods transport services and your annual turnover is ₹8 crore, you're exempt from e-invoicing. However, if you run an IT services company with the same turnover exporting software to clients abroad, you must generate e-invoices because IT services are not on the exemption list.

For businesses doing international trade, e-invoicing adds another layer to your export documentation process.

Export invoices are covered under the e-invoicing mandate if your business turnover exceeds ₹5 crore. When you export goods or services, you need to generate an e-invoice with the IRN and QR code just as you would for a domestic B2B transaction.

The e-invoice then gets reported automatically to the GST system, which helps with your export documentation and GSTR-1 filing.

One key benefit is that the e-invoice data flows directly into the GST portal, which can make it easier to claim refunds or track export transactions for compliance purposes. However, you still need to manage your FIRC (Foreign Inward

Remittance Certificate) separately when you receive payment from your international client. The e-invoice doesn't automatically generate FIRC documentation.

This is where payment infrastructure becomes critical. If you're collecting payments from clients in the US, UK, Europe, or other countries, you need a system that can handle multi-currency payments and provide instant compliance documentation.

E-invoicing keeps you compliant in India, but what about when payments come from overseas clients?

If you're exporting services or goods, you're dealing with multiple challenges at once. You need to generate e-invoices for compliance, collect payments in foreign currencies, convert those payments to INR, get FIRC documentation for your records, and track everything for filing your returns.

Doing this manually across different platforms leads to errors, delays, and hours spent on reconciliation.

PayGlocal brings all your international payment management processes, including compliance documentation and verification, under one platform. Here's how PayGlocal can help you:

PayGlocal brings together advanced payment collection and compliance documentation in one place. You spend less time managing different systems and more time serving your global clients.

To follow the e-invoice limit, it is essential to know when you must comply, which documents need to be e-invoiced, and how quickly you need to report them to avoid penalties and operational problems.

The best approach is to set up your e-invoicing system now if you haven't already, integrate it with your accounting software, and build verification steps into your workflow to catch errors within the 24-hour cancellation window.

For businesses handling international payments, choosing a solution that combines payment collection with automatic compliance documentation and verification can save hours of manual work and reduce errors.

Stay compliant, stay efficient, and keep growing with faster international payment management. Get started with PayGlocal today.

When it comes to GST, e-invoicing is one of the most important components. But what exactly is the e-invoice limit, and does it apply to you?

In this guide, we break down the e-invoice limit in detail, covering who needs to follow the e-invoicing limit, when to report your invoices, and which documents are required to stay compliant. So, let’s get started.

Key takeaways

- Turnover threshold: E-invoicing is mandatory for businesses with Annual Aggregate Turnover (AATO) above ₹5 crore in any financial year from 2017-18 onwards, calculated at PAN level across all GSTINs.

- Time limit rule: From April 1, 2025, businesses with an AATO of ₹10 crore or more must report e-invoices to the IRP within 30 days of the invoice date, or the system will reject them.

- Scope of coverage: E-invoicing applies to B2B transactions, exports, and supplies where the supplier is liable under the Reverse Charge Mechanism (RCM), but not to B2C invoices or bills of supply.

- Key exemptions: SEZ units, banks, insurance companies, NBFCs, passenger transport services, and government departments are exempt even if they cross the turnover threshold.

- Faster global payments: PayGlocal helps exporters and global businesses collect payments in 33+ currencies with instant FIRC generation, making compliance easier while you focus on growth.

What is the e-invoice limit?

The e-invoice limit refers to two compliance requirements: the turnover threshold and the time limit. Let’s learn more about each of them.

E-invoicing turnover threshold

The e-invoicing turnover threshold determines whether your business must generate e-invoices at all. Currently, any business with an Annual Aggregate Turnover (AATO) exceeding ₹5 crore in any financial year from 2017-18 onwards must use e-invoicing for eligible transactions.

This threshold applies at the PAN level, which means you add up the turnover across all your GSTINs nationwide. Once you cross this limit in any year, you stay in the e-invoicing system unless you qualify for a specific exemption.

For example, if you have three GSTINs with ₹2 crore, ₹2 crore, and ₹1.5 crore, respectively, your total AATO is ₹5.5 crore, which means e-invoicing applies.

E-invoicing time limit

From April 1, 2025, businesses with an AATO of ₹10 crore or more must report their e-invoices to the Invoice Registration Portal within 30 days of the invoice date. If you miss this window, the IRP system will reject your invoice submission. This rule previously applied only to businesses above ₹100 crore, but now covers a much larger group.

For instance, if you run a software export business that earned ₹8 crore in FY 2022-23, you must generate e-invoices for all your B2B transactions. If your turnover is ₹12 crore, you also need to report each invoice within 30 days. These limits work together to define your compliance obligations.

How do you calculate your Annual Aggregate Turnover?

Calculating AATO correctly is the first step in knowing whether you need to comply with e-invoicing.

Annual Aggregate Turnover means the total value of all taxable supplies, exempt supplies, exports, and inter-state supplies made by you under a single PAN. Here's how to calculate it:

Tip: You can verify your AATO through the GST portal by logging into your account and checking your turnover details across all registered GSTINs. Make sure you monitor your turnover throughout the year, especially as you approach the limit, so you can plan your compliance setup in advance.

What documents need e-invoicing?

Not every invoice or document requires e-invoicing, so knowing the scope helps you comply efficiently. Here's a quick view of what does and doesn't need e-invoicing:

For example, if you run a D2C e-commerce business and sell directly to individual consumers, those invoices don't need IRNs even if your turnover exceeds ₹5 crore. But if you also supply to other businesses or export products, those B2B and export invoices require e-invoicing.

What are the key e-invoicing exemptions?

Even if your turnover exceeds the ₹5 crore threshold, you may be exempt from e-invoicing if your business falls under specific categories.

Here are the exemptions that apply regardless of turnover:

- SEZ units: Special Economic Zone units operating within SEZs are exempt, but SEZ developers are not exempt.

- Insurance companies: All insurance service providers are exempt from e-invoicing requirements.

- Banking and financial institutions: Banks, NBFCs, and financial institutions are exempt from generating e-invoices.

- Goods transport agencies: GTAs providing road transportation of goods are exempt.

- Passenger transport services: Suppliers of passenger transportation are exempt.

- Multiplex operators: Admission to cinematographic films in multiplexes is exempt.

- Government entities: Government departments and local authorities are exempt.

One important clarification is the SEZ distinction. If you're a notified taxpayer supplying goods or services to an SEZ unit, you still need to generate e-invoices for those transactions because they qualify as B2B or export supplies from your perspective.

For instance, if you operate a logistics company providing goods transport services and your annual turnover is ₹8 crore, you're exempt from e-invoicing. However, if you run an IT services company with the same turnover exporting software to clients abroad, you must generate e-invoices because IT services are not on the exemption list.

How does e-invoicing work with international transactions?

For businesses doing international trade, e-invoicing adds another layer to your export documentation process.

Export invoices are covered under the e-invoicing mandate if your business turnover exceeds ₹5 crore. When you export goods or services, you need to generate an e-invoice with the IRN and QR code just as you would for a domestic B2B transaction.

The e-invoice then gets reported automatically to the GST system, which helps with your export documentation and GSTR-1 filing.

One key benefit is that the e-invoice data flows directly into the GST portal, which can make it easier to claim refunds or track export transactions for compliance purposes. However, you still need to manage your FIRC (Foreign Inward

Remittance Certificate) separately when you receive payment from your international client. The e-invoice doesn't automatically generate FIRC documentation.

This is where payment infrastructure becomes critical. If you're collecting payments from clients in the US, UK, Europe, or other countries, you need a system that can handle multi-currency payments and provide instant compliance documentation.

Get paid globally with built-in compliance through PayGlocal

E-invoicing keeps you compliant in India, but what about when payments come from overseas clients?

If you're exporting services or goods, you're dealing with multiple challenges at once. You need to generate e-invoices for compliance, collect payments in foreign currencies, convert those payments to INR, get FIRC documentation for your records, and track everything for filing your returns.

Doing this manually across different platforms leads to errors, delays, and hours spent on reconciliation.

PayGlocal brings all your international payment management processes, including compliance documentation and verification, under one platform. Here's how PayGlocal can help you:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries, giving your international clients a seamless payment experience while you collect in their preferred currency.

- Recurring payments: Set up subscription billing and automatic debits for international cards, ensuring consistent revenue flow for your SaaS or service business.

- Sanction screening: Stay compliant with global AML regulations through automated screening that checks every transaction against 300+ sanction lists, including OFAC, UNSC, and EU databases.

- One platform management: Handle all payment operations from a single dashboard with customizable user roles, transaction reports, and real-time monitoring instead of juggling multiple systems.

- Instant FIRC generation: Receive FIRC documentation automatically in your inbox after settlement, eliminating the need to chase banks for compliance certificates and keeping your export records audit-ready.

PayGlocal brings together advanced payment collection and compliance documentation in one place. You spend less time managing different systems and more time serving your global clients.

Final thoughts

To follow the e-invoice limit, it is essential to know when you must comply, which documents need to be e-invoiced, and how quickly you need to report them to avoid penalties and operational problems.

The best approach is to set up your e-invoicing system now if you haven't already, integrate it with your accounting software, and build verification steps into your workflow to catch errors within the 24-hour cancellation window.

For businesses handling international payments, choosing a solution that combines payment collection with automatic compliance documentation and verification can save hours of manual work and reduce errors.

Stay compliant, stay efficient, and keep growing with faster international payment management. Get started with PayGlocal today.