In India, 7.7 crore people now hold credit cards, which is more than 5.5% of the population. The use of credit cards is increasing steadily, but many credit card users also face some issues, especially with the charges.

Credit card markup fees are among the most confusing charges businesses and individuals face when dealing with international transactions. These fees can quietly affect your profits, especially if you're a freelancer receiving payments from overseas clients or an exporter managing multiple currencies.

In this guide, we break down everything you need to know about credit card markup fees, including what they are, how they're calculated, and most importantly, how you can reduce or avoid them entirely. Let’s get into it!

A markup fee on credit cards is an additional charge your bank adds when you make transactions in foreign currencies.

For example, if you buy software from a US company for $100, your bank doesn't just convert $100 to rupees at the current exchange rate. Instead, they add a markup fee, typically 1.5% to 3.5%, on top of the conversion.

The tricky part is that you don't always get to see this fee separately on your statement. Often, the rates build it into the exchange rate, making it harder for you to spot exactly how much extra you're paying.

Credit card markup fees work through a multi-step process every time you make an international transaction.

When you swipe your card for an international purchase, your bank first processes the transaction at the wholesale exchange rate (the rate banks use when trading currencies with each other). Then, they add their markup percentage to this rate before charging your account.

Here's what happens at each step:

For instance, if you spend €50 on a European website and the wholesale rate is ₹90 per euro, your base amount would be ₹4,500. With a 3% markup fee, you'd pay an additional ₹135, plus ₹24.30 as GST on the markup, bringing your total to ₹4,659.30.

Calculating markup fees helps you know the true cost of your international transactions and compare different payment options effectively.

The basic formula is straightforward: Markup Fee = Transaction Amount × Markup Percentage

But the real calculation includes GST: Total Markup Cost = (Transaction Amount × Markup Percentage) + (Markup Fee × 18% GST)

Let's work through an example. Say you're a freelancer receiving a $500 payment through an international payment processor that charges your credit card:

This means your effective markup rate is actually 4.13%, not the advertised 3.5%, once you factor in GST.

Different banks have varying markup fee structures, and choosing the right bank can save you significant money on international transactions.

Here's a comparison of markup fees charged by major Indian banks:

While Axis Bank and HDFC often offer the lowest rates, it is worth noting that they usually apply only to premium credit cards with high annual fees. Most standard credit cards from these banks still charge around 3.5%.

Some banks also offer zero markup fee credit cards. For example, IDFC Bank First Wow Credit Card and HDFC Bank Regalia ForexPlus Credit Card.

But these zero markup fee credit cards typically come with higher annual fees that might offset the markup savings unless you make frequent international transactions above a certain threshold.

Here are some effective strategies that can help you minimize or avoid these markup costs on your credits:

Managing international transactions through traditional credit cards often means dealing with hidden markup fees, complex calculations, and unpredictable costs. For freelancers, exporters, and growing businesses, these charges can add up quickly and make financial planning challenging.

PayGlocal offers a complete payment platform that brings transparency and control to your international transactions. Instead of worrying about markup fees on every transaction, you get clear pricing and better rates that help you keep more of what you earn.

Here’s how PayGlocal can help you:

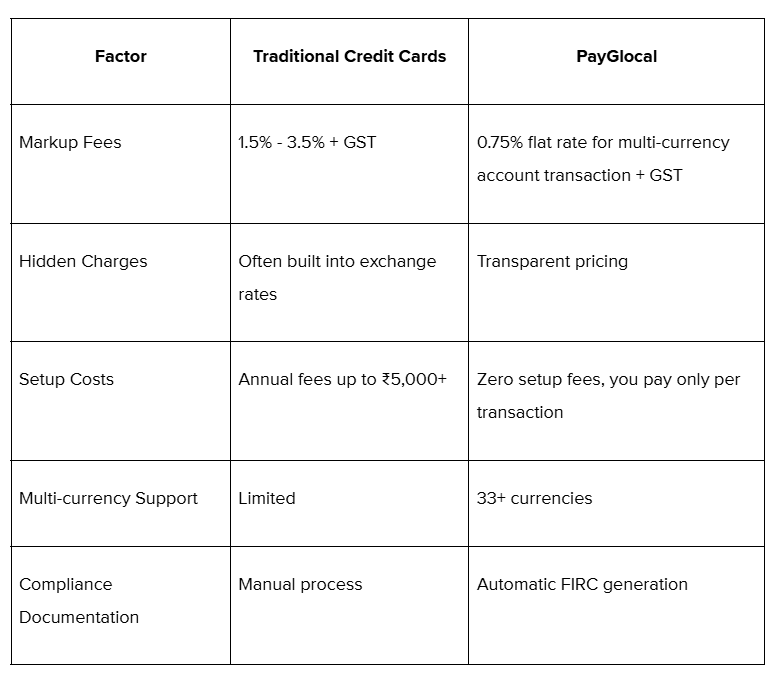

Here's how PayGlocal compares to traditional credit card processing for international transactions:

Whether you're invoicing a client in the US or receiving payments from Europe, PayGlocal helps you collect international payments efficiently while keeping your costs predictable and transparent.

Credit card markup fees are a cost you face when using traditional banking methods for international transactions, but knowing how they work helps you manage your costs better. With markup rates ranging from 1.5% to 3.5% plus GST, these fees can significantly impact your bottom line over time.

The key is choosing the right payment method for your specific needs. While premium credit cards with lower markup rates work for occasional international purchases, businesses dealing with regular global transactions benefit from a more cost-effective solution like PayGlocal.

Stop losing money due to complex costs or hidden charges. Get started with PayGlocal today and have better control over your global payments.

Credit card markup fees are among the most confusing charges businesses and individuals face when dealing with international transactions. These fees can quietly affect your profits, especially if you're a freelancer receiving payments from overseas clients or an exporter managing multiple currencies.

In this guide, we break down everything you need to know about credit card markup fees, including what they are, how they're calculated, and most importantly, how you can reduce or avoid them entirely. Let’s get into it!

Key Takeaways

- Markup fees range from 1.5% to 3.5%: Most Indian banks charge between 1.5% to 3.5% on international credit card transactions, plus 18% GST on the markup amount.

- Hidden in exchange rates: Banks don't always show markup fees separately — they're often built into the exchange rate you see on your statement.

- Applies to all foreign currency transactions: Whether you're shopping online from a US website or receiving payments from international clients, markup fees apply.

- PayGlocal offers a better payment solution: With PayGlocal’s multi-currency accounts and clear pricing, you can avoid hidden markup fees and get better exchange rates for international transactions.

What does the markup fee on a credit card mean?

A markup fee on credit cards is an additional charge your bank adds when you make transactions in foreign currencies.

For example, if you buy software from a US company for $100, your bank doesn't just convert $100 to rupees at the current exchange rate. Instead, they add a markup fee, typically 1.5% to 3.5%, on top of the conversion.

The tricky part is that you don't always get to see this fee separately on your statement. Often, the rates build it into the exchange rate, making it harder for you to spot exactly how much extra you're paying.

How does the credit card markup fee work?

Credit card markup fees work through a multi-step process every time you make an international transaction.

When you swipe your card for an international purchase, your bank first processes the transaction at the wholesale exchange rate (the rate banks use when trading currencies with each other). Then, they add their markup percentage to this rate before charging your account.

Here's what happens at each step:

- Transaction initiated: You make a purchase in foreign currency.

- Currency conversion: Your bank converts the amount using the wholesale exchange rate.

- Markup applied: The bank adds its markup fee (1.5% to 3.5%).

- GST calculation: 18% GST is applied to the markup amount.

- Final debit: The total amount is debited from your account.

For instance, if you spend €50 on a European website and the wholesale rate is ₹90 per euro, your base amount would be ₹4,500. With a 3% markup fee, you'd pay an additional ₹135, plus ₹24.30 as GST on the markup, bringing your total to ₹4,659.30.

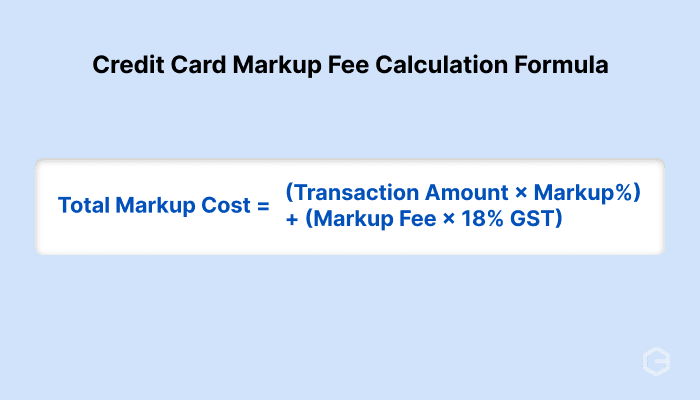

How to calculate credit card markup fees?

Calculating markup fees helps you know the true cost of your international transactions and compare different payment options effectively.

The basic formula is straightforward: Markup Fee = Transaction Amount × Markup Percentage

But the real calculation includes GST: Total Markup Cost = (Transaction Amount × Markup Percentage) + (Markup Fee × 18% GST)

Let's work through an example. Say you're a freelancer receiving a $500 payment through an international payment processor that charges your credit card:

- Transaction amount: $500 (₹41,500 at ₹83 per dollar)

- Bank markup fee: 3.5%

- Markup amount: ₹41,500 × 3.5% = ₹1,452.50

- GST on markup: ₹1,452.50 × 18% = ₹261.45

- Total markup cost: ₹1,452.50 + ₹261.45 = ₹1,713.95

- Final amount debited: ₹41,500 + ₹1,713.95 = ₹43,213.95

This means your effective markup rate is actually 4.13%, not the advertised 3.5%, once you factor in GST.

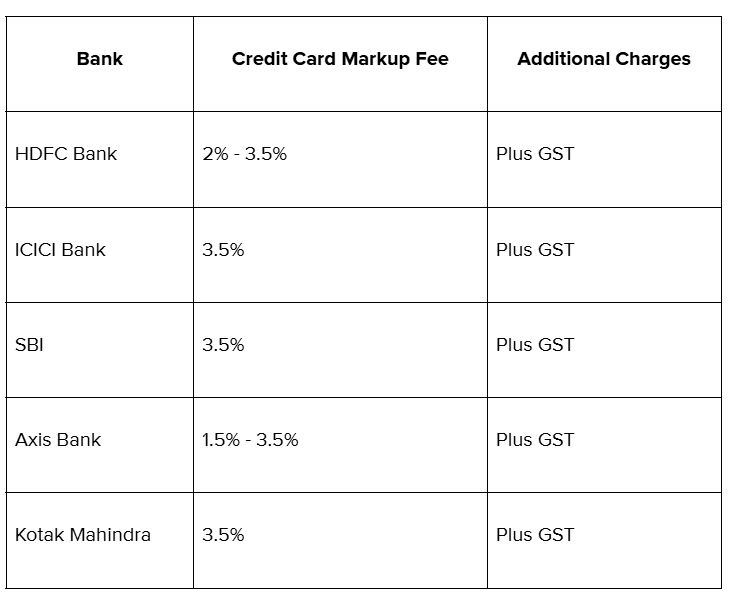

What banks charge the lowest markup fees in India?

Different banks have varying markup fee structures, and choosing the right bank can save you significant money on international transactions.

Here's a comparison of markup fees charged by major Indian banks:

While Axis Bank and HDFC often offer the lowest rates, it is worth noting that they usually apply only to premium credit cards with high annual fees. Most standard credit cards from these banks still charge around 3.5%.

Some banks also offer zero markup fee credit cards. For example, IDFC Bank First Wow Credit Card and HDFC Bank Regalia ForexPlus Credit Card.

But these zero markup fee credit cards typically come with higher annual fees that might offset the markup savings unless you make frequent international transactions above a certain threshold.

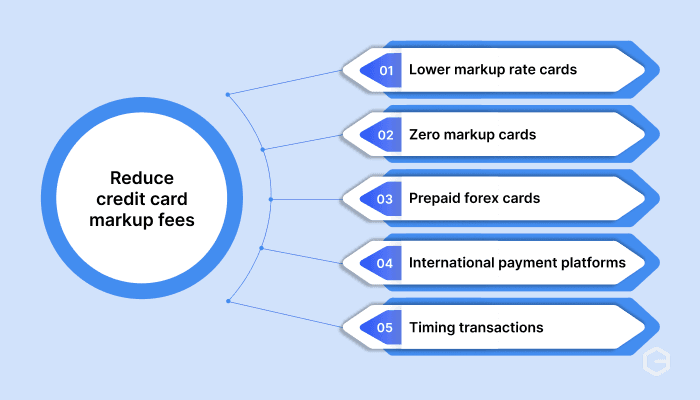

How to avoid or recduce credit card markup fees?

Here are some effective strategies that can help you minimize or avoid these markup costs on your credits:

- Choose cards with lower markup rates: Premium credit cards often have lower markup fees, sometimes as low as 1.5%. Calculate whether the annual fee justifies the savings based on your international spending.

- Use zero markup fee cards strategically: Some banks offer zero markup fee credit cards. These work well if your annual international spending exceeds the break-even point against the annual fee.

- Consider prepaid forex cards: For planned international expenses, forex cards often offer better exchange rates and lower fees compared to credit cards.

- Use international payment platforms: Services that offer multi-currency accounts can help you receive international payments without traditional banking markup fees.

- Time your transactions: Exchange rates fluctuate daily. For large transactions, monitor rates and time your payments when the rupee is stronger.

Manage global transactions with better rates using PayGlocal

Managing international transactions through traditional credit cards often means dealing with hidden markup fees, complex calculations, and unpredictable costs. For freelancers, exporters, and growing businesses, these charges can add up quickly and make financial planning challenging.

PayGlocal offers a complete payment platform that brings transparency and control to your international transactions. Instead of worrying about markup fees on every transaction, you get clear pricing and better rates that help you keep more of what you earn.

Here’s how PayGlocal can help you:

- Multi-currency accounts in USD, GBP, EUR, CAD: Collect payments directly in major currencies without conversion markups, then settle to INR when rates work in your favor.

- Transparent pricing with no hidden fees: Pay a flat 0.75% for multi-currency account transactions with no surprise charges or complex markup calculations.

- Global payment method support: Accept payments through 40+ international payment methods, making it easier for clients worldwide to pay you.

- Real-time payment tracking: Monitor your international payments with instant notifications and clear status updates at every step.

- One platform management: Easily manage all your international payment needs from a single dashboard, from payment collection to compliance documentation.

Here's how PayGlocal compares to traditional credit card processing for international transactions:

Whether you're invoicing a client in the US or receiving payments from Europe, PayGlocal helps you collect international payments efficiently while keeping your costs predictable and transparent.

Final thoughts

Credit card markup fees are a cost you face when using traditional banking methods for international transactions, but knowing how they work helps you manage your costs better. With markup rates ranging from 1.5% to 3.5% plus GST, these fees can significantly impact your bottom line over time.

The key is choosing the right payment method for your specific needs. While premium credit cards with lower markup rates work for occasional international purchases, businesses dealing with regular global transactions benefit from a more cost-effective solution like PayGlocal.

Stop losing money due to complex costs or hidden charges. Get started with PayGlocal today and have better control over your global payments.