As businesses grow, having a reliable and efficient payment system becomes essential. The global digital payments market is set to reach $20.37 trillion by 2025, with an annual growth rate of 15.9%. To keep up with this growth, businesses need to offer a range of payment methods, such as credit cards, mobile wallets, and e-commerce platforms, to meet customer needs.

However, managing secure and seamless transactions, particularly for international payments, is vital for smooth operations. This blog will explore how merchant payment services work and how they support efficient business transaction processing.

Merchant payment services are financial solutions that help businesses accept various forms of payment from customers in exchange for goods or services.

The basics of merchant processing are straightforward: Businesses sign up with a merchant payment provider to accept credit cards, debit cards, e-cheques, and mobile payments.

These services are essential for businesses engaged in retail, e-commerce, or any commercial activity involving payment transactions.

From payment processing to point-of-sale (POS) systems, merchant payment services allow businesses to process transactions securely, customers to pay easily, and businesses to receive payments efficiently.

Various providers offer Merchant services, each specializing in different aspects of payment processing. Payment processors and POS system providers provide merchant services and transaction hardware. Additionally, many e-commerce platforms integrate payment processing into their systems, offering merchant services directly through their platforms.

As crucial as merchant payment services are, the process wouldn’t function without the involvement of key players in the payment ecosystem.

Merchant payment processing involves several key players who work together to facilitate smooth and secure transactions, whether for domestic or international payments. Here’s a breakdown of each player’s role:

If you are an exporter or a business owner, you are the merchant in the transaction, selling goods or services to customers. The payment provider company enables you to receive payment for your products or services through various payment methods such as credit cards, debit cards, and mobile payments.

Customers are the buyers who initiate the payment transaction. They make payments for goods or services using their preferred payment method, such as credit cards, debit cards, cheques, or mobile payment platforms. Customers interact directly with the payment services through online payment gateways or point-of-sale (POS) systems. That’s how the business gets paid for the goods or services provided.

Acquiring or merchant banks are financial institutions (like HDFC, ICICI) that partner with merchants to process payment transactions. They provide the infrastructure for merchants to accept payments and facilitate the transfer of funds from the customer’s bank to the merchant’s account.

Issuing banks are the financial institutions that provide customers with payment cards (credit or debit cards). Their role is to approve or decline payment transactions based on the customer’s available credit or funds. The issuing bank verifies the transaction, checks the account balance or credit limit, and ensures that the customer has sufficient funds before authorizing the transaction.

The point-of-sale (POS) system is the interface where the customer’s payment information is captured and transmitted for processing. In physical stores, this could be card readers or mobile payment devices, while in online settings, the payment gateway encrypts the cardholder’s information. Examples: e-commerce platforms, mobile apps, or websites that facilitate transactions.

Payment processors are intermediaries that connect all the players in the transaction, including the merchant, customer, acquiring bank, and issuing bank. They handle the technical and security aspects of processing payments, such as encrypting payment information, verifying transaction details, seamless cross-border payments, and routing the payment request to the appropriate financial institutions for approval.

PayGlocal is the one-stop payment service provider for cross-border transaction needs. It simplifies handling multiple currencies and offers the highest level of security with its Samruddhi X screening protocol, which guarantees secure transaction processing and provides privacy and fraud prevention.

As you have explored the key players involved in merchant payment processing, let's examine how the payment flow works and how all the players collaborate to complete a transaction from initiation to final payment.

If a customer buys a product from an online store, the transaction starts when the customer selects a payment method, such as a credit card or mobile wallet.

The payment request is then sent through a series of steps involving payment processors, banks, and sometimes third-party services for verification and authorization before the business receives the funds. Here are the steps that will help you better understand how payment processing works.

When you're ready to make a purchase in a physical store or online, the first step is to provide your payment details. This could be your card number, bank account information, or another form of payment. You enter these details in the business’s point-of-sale (POS) system or through the checkout page on an e-commerce site.

Your payment information is securely sent to a payment gateway, where it is encrypted to safeguard your sensitive data. This encrypted data is then forwarded to the payment processor using encryption protocols such as TLS (Transport Layer Security) or SSL (Secure Sockets Layer).

Next, the payment processor sends the transaction details to the acquiring bank (the business’s bank). The acquiring bank forwards the details to your issuing bank (your bank) through the relevant card network.

Your bank then checks if you have enough funds or credit to complete the transaction. It sends an approval or decline message, which travels to the payment processor through the card networks and the acquiring bank.

The payment processor communicates the transaction's approval or decline to the business. The company can provide the goods or services if the transaction is approved. If the transaction is declined, the business will receive a decline code explaining why the payment wasn’t successful and will inform you accordingly.

Once authorized, the clearing process begins. Your bank transfers the transaction amount, minus any fees, to the acquiring bank through the card network. All the details are recorded and reconciled between the banks involved.

In this step, the acquiring bank deposits the funds into the business’s account, completing the transaction. The company has received the payment, and the transaction is considered final.

Finally, businesses and financial institutions review and reconcile transaction records to ensure accuracy. If there are any discrepancies, they are addressed during this stage.

While these steps are generally the same for domestic and international payments, cross-border transactions introduce additional elements such as multi-currency accounts, screening, and stringent compliance checks for Anti Money Laundering.

To learn what is included in merchant payment services, read this: Merchant Terms of Use @PayGlocal.

The latest trend in merchant services is focused on providing faster and more seamless payment experiences. As shoppers seek convenience, merchants adopt innovations like one-click payments, dynamic checkouts, e-wallets on mobile and wearable devices, cryptocurrencies, and services tailored for nonprofits.

Additionally, merchants are exploring loyalty programs, gift cards, and touchless, autonomous retail to enhance customer satisfaction and streamline transactions. The future of merchant services will continue prioritizing speed, security, and customer-centric features, driving the evolution of payment technologies.

Merchant payment services provide businesses with secure, efficient, and convenient ways to process transactions.

Simplified Record-Keeping: Automated systems generate transaction records, making inventory management, financial tracking, and reporting much easier for businesses.

Building on the benefits of merchant payment services, several key factors must be considered before choosing the right solution for your business.

These considerations will help ensure that your selected payment system aligns with your needs and supports seamless, secure transactions.

1. Transaction Fees & Costs: Compare fees for domestic and international transactions. Domestic transactions usually charge a fixed percentage fee plus a flat fee per transaction. Cross-border payments incur higher costs due to currency conversion and foreign bank charges.

2. Security Features & Compliance: Ensure strong encryption, fraud protection, and adherence to standards like PCI DSS. For international transactions, check for compliance with regional regulations (e.g., GDPR) and zero-knowledge proof protocols.

3. Seamless Integration: Look for payment services that integrate easily with your existing POS systems, e-commerce platforms, and accounting tools. Multi-currency support and international payment compatibility are key for global businesses.

4. Customer Support: Ensure 24/7 support with multilingual assistance, especially for international transactions across time zones.

5. Fraud Prevention: Look for additional security measures, such as 2FA (Two-Factor Authentication) and real-time fraud detection tools, which are essential for protecting your business and your customers.

PayGlocal offers transparent and standard pricing with no markup, hidden charges, or monthly/annual fees. Transparent pricing, no surprises.

As you evaluate the essential considerations for choosing the right merchant payment service, it's important to know how these factors directly contribute to a secure process. With these elements in mind, let's summarize how the right payment platform can support your business growth.

Merchant payment services have become vital to modern business operations, enabling smooth, secure, and efficient transactions for businesses and customers.

These services offer numerous benefits that help businesses thrive, from improving customer convenience to expanding sales opportunities. However, selecting the right payment platform is crucial as it meets the needs of today’s transactions and scales with future growth.

PayGlocal stands out as a leader in payment processing, offering seamless, secure, and multi-currency solutions for businesses globally. With support for 33 currencies and coverage in 180+ countries, PayGlocal guarantees that businesses can effortlessly manage cross-border transactions and cater to customers worldwide.

Whether expanding into new markets or streamlining your payments, PayGlocal provides a robust, scalable solution to meet your international and domestic payment needs. Get Started Today!

A merchant account is a dedicated bank account for processing payments. Funds are held there before being transferred to your regular business account.

Merchant services encompass various solutions, including payment processing, e-commerce support, loyalty programs, and more. These services help manage transactions and enhance payment capabilities.

An example of a merchant payment is when a customer buys a product or service and pays using a credit card, debit card, or another electronic payment method.

A merchant fee is a charge businesses incur whenever a customer purchases using a card. These fees are part of the overall cost for payment processing services merchants provide.

However, managing secure and seamless transactions, particularly for international payments, is vital for smooth operations. This blog will explore how merchant payment services work and how they support efficient business transaction processing.

What is Merchant Payment Services?

Merchant payment services are financial solutions that help businesses accept various forms of payment from customers in exchange for goods or services.

The basics of merchant processing are straightforward: Businesses sign up with a merchant payment provider to accept credit cards, debit cards, e-cheques, and mobile payments.

These services are essential for businesses engaged in retail, e-commerce, or any commercial activity involving payment transactions.

From payment processing to point-of-sale (POS) systems, merchant payment services allow businesses to process transactions securely, customers to pay easily, and businesses to receive payments efficiently.

Who Offers Merchant Payment Services?

Various providers offer Merchant services, each specializing in different aspects of payment processing. Payment processors and POS system providers provide merchant services and transaction hardware. Additionally, many e-commerce platforms integrate payment processing into their systems, offering merchant services directly through their platforms.

As crucial as merchant payment services are, the process wouldn’t function without the involvement of key players in the payment ecosystem.

Who are the Key Players in Merchant Payment Processing?

Merchant payment processing involves several key players who work together to facilitate smooth and secure transactions, whether for domestic or international payments. Here’s a breakdown of each player’s role:

1. Role of Merchants and Their Importance in Transactions

If you are an exporter or a business owner, you are the merchant in the transaction, selling goods or services to customers. The payment provider company enables you to receive payment for your products or services through various payment methods such as credit cards, debit cards, and mobile payments.

2. Role of Customers and Their Interaction with Payment Services

Customers are the buyers who initiate the payment transaction. They make payments for goods or services using their preferred payment method, such as credit cards, debit cards, cheques, or mobile payment platforms. Customers interact directly with the payment services through online payment gateways or point-of-sale (POS) systems. That’s how the business gets paid for the goods or services provided.

3. Role of Acquiring Banks in Facilitating Transactions

Acquiring or merchant banks are financial institutions (like HDFC, ICICI) that partner with merchants to process payment transactions. They provide the infrastructure for merchants to accept payments and facilitate the transfer of funds from the customer’s bank to the merchant’s account.

4. Role of Issuing Banks in Transaction Approval

Issuing banks are the financial institutions that provide customers with payment cards (credit or debit cards). Their role is to approve or decline payment transactions based on the customer’s available credit or funds. The issuing bank verifies the transaction, checks the account balance or credit limit, and ensures that the customer has sufficient funds before authorizing the transaction.

5. Point-of-Sale (POS) System

The point-of-sale (POS) system is the interface where the customer’s payment information is captured and transmitted for processing. In physical stores, this could be card readers or mobile payment devices, while in online settings, the payment gateway encrypts the cardholder’s information. Examples: e-commerce platforms, mobile apps, or websites that facilitate transactions.

6. Role of Payment Processors in Connecting All Participants

Payment processors are intermediaries that connect all the players in the transaction, including the merchant, customer, acquiring bank, and issuing bank. They handle the technical and security aspects of processing payments, such as encrypting payment information, verifying transaction details, seamless cross-border payments, and routing the payment request to the appropriate financial institutions for approval.

PayGlocal is the one-stop payment service provider for cross-border transaction needs. It simplifies handling multiple currencies and offers the highest level of security with its Samruddhi X screening protocol, which guarantees secure transaction processing and provides privacy and fraud prevention.

As you have explored the key players involved in merchant payment processing, let's examine how the payment flow works and how all the players collaborate to complete a transaction from initiation to final payment.

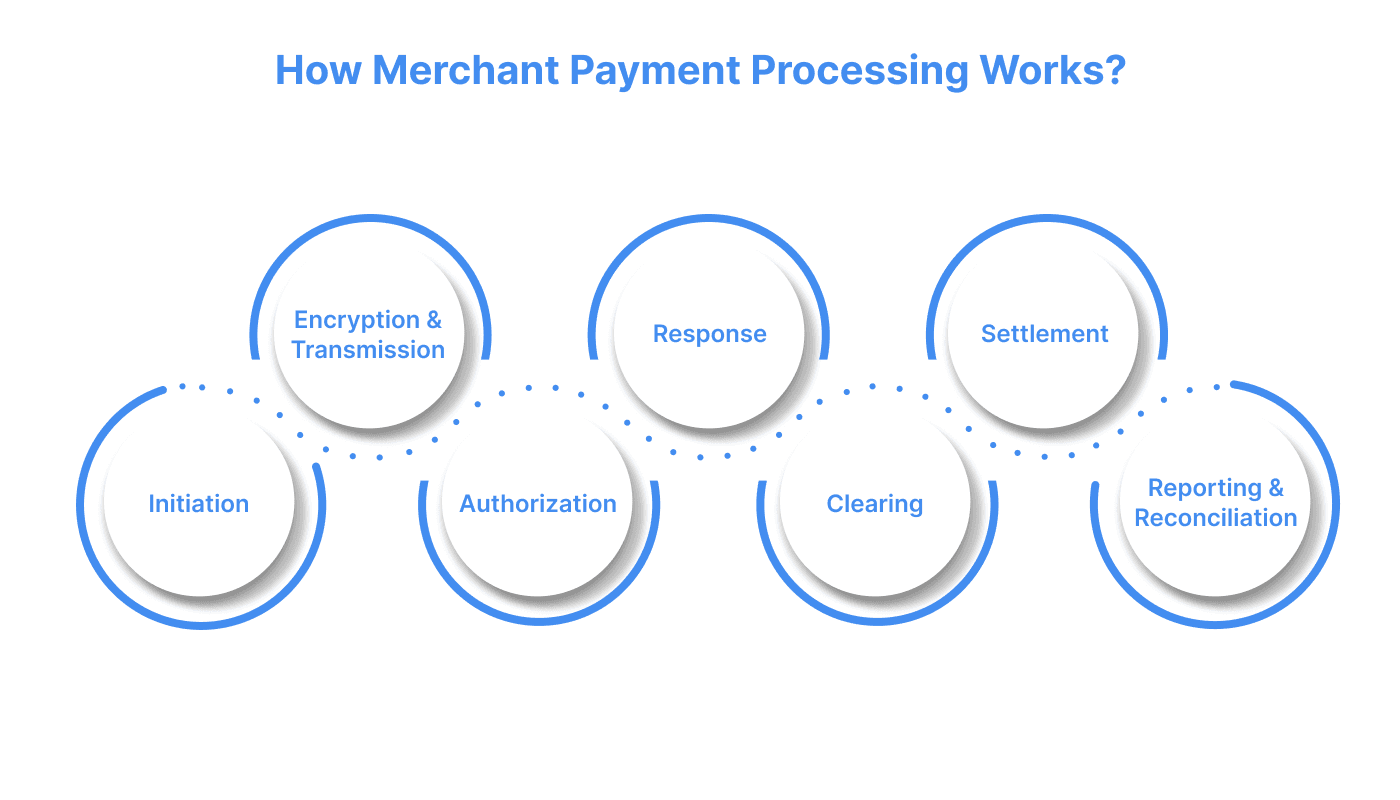

How Merchant Payment Processing Works?

If a customer buys a product from an online store, the transaction starts when the customer selects a payment method, such as a credit card or mobile wallet.

The payment request is then sent through a series of steps involving payment processors, banks, and sometimes third-party services for verification and authorization before the business receives the funds. Here are the steps that will help you better understand how payment processing works.

1. Initiation

When you're ready to make a purchase in a physical store or online, the first step is to provide your payment details. This could be your card number, bank account information, or another form of payment. You enter these details in the business’s point-of-sale (POS) system or through the checkout page on an e-commerce site.

2. Encryption and Transmission

Your payment information is securely sent to a payment gateway, where it is encrypted to safeguard your sensitive data. This encrypted data is then forwarded to the payment processor using encryption protocols such as TLS (Transport Layer Security) or SSL (Secure Sockets Layer).

3. Authorization

Next, the payment processor sends the transaction details to the acquiring bank (the business’s bank). The acquiring bank forwards the details to your issuing bank (your bank) through the relevant card network.

Your bank then checks if you have enough funds or credit to complete the transaction. It sends an approval or decline message, which travels to the payment processor through the card networks and the acquiring bank.

4. Response

The payment processor communicates the transaction's approval or decline to the business. The company can provide the goods or services if the transaction is approved. If the transaction is declined, the business will receive a decline code explaining why the payment wasn’t successful and will inform you accordingly.

5. Clearing

Once authorized, the clearing process begins. Your bank transfers the transaction amount, minus any fees, to the acquiring bank through the card network. All the details are recorded and reconciled between the banks involved.

6. Settlement

In this step, the acquiring bank deposits the funds into the business’s account, completing the transaction. The company has received the payment, and the transaction is considered final.

7. Reporting and Reconciliation

Finally, businesses and financial institutions review and reconcile transaction records to ensure accuracy. If there are any discrepancies, they are addressed during this stage.

While these steps are generally the same for domestic and international payments, cross-border transactions introduce additional elements such as multi-currency accounts, screening, and stringent compliance checks for Anti Money Laundering.

To learn what is included in merchant payment services, read this: Merchant Terms of Use @PayGlocal.

What is the Future of Merchant Payment Services?

The latest trend in merchant services is focused on providing faster and more seamless payment experiences. As shoppers seek convenience, merchants adopt innovations like one-click payments, dynamic checkouts, e-wallets on mobile and wearable devices, cryptocurrencies, and services tailored for nonprofits.

Additionally, merchants are exploring loyalty programs, gift cards, and touchless, autonomous retail to enhance customer satisfaction and streamline transactions. The future of merchant services will continue prioritizing speed, security, and customer-centric features, driving the evolution of payment technologies.

Benefits of Merchant Payment Services

Merchant payment services provide businesses with secure, efficient, and convenient ways to process transactions.

- Customer Convenience: Payment services ensure a smooth, hassle-free customer experience, building trust and loyalty with easy, user-friendly payment methods.

- Expanded Sales Opportunities: Accepting multiple payment methods, including cashless options, online payments, and international transactions, opens up a broader customer base and increases sales and revenue.

- Facilitates Global Sales: Digital payment systems enable businesses to accept payments from international customers, promoting global expansion and opening new market opportunities.

- Improved Cash Flow and Payment Flexibility: Electronic payments are processed quickly, enhancing cash flow management with timely transfers. Additionally, offering multiple payment methods, such as credit/debit cards, e-wallets, and bank transfers, caters to diverse customer preferences and improves sales.

- Security: Advanced security measures, such as encryption and fraud detection, protect sensitive customer data and minimize the risk of unauthorized transactions.

Simplified Record-Keeping: Automated systems generate transaction records, making inventory management, financial tracking, and reporting much easier for businesses.

- Scalability: Automated payment processing reduces the risk of manual errors, enables handling higher transaction volumes, and ensures greater accuracy in financial transactions.

- Regulatory Compliance: Payment processors ensure businesses comply with industry regulations like PCI DSS, maintaining data security standards for cardholder information.

Building on the benefits of merchant payment services, several key factors must be considered before choosing the right solution for your business.

What Should You Consider Before Choosing Merchant Payment Services?

These considerations will help ensure that your selected payment system aligns with your needs and supports seamless, secure transactions.

1. Transaction Fees & Costs: Compare fees for domestic and international transactions. Domestic transactions usually charge a fixed percentage fee plus a flat fee per transaction. Cross-border payments incur higher costs due to currency conversion and foreign bank charges.

2. Security Features & Compliance: Ensure strong encryption, fraud protection, and adherence to standards like PCI DSS. For international transactions, check for compliance with regional regulations (e.g., GDPR) and zero-knowledge proof protocols.

3. Seamless Integration: Look for payment services that integrate easily with your existing POS systems, e-commerce platforms, and accounting tools. Multi-currency support and international payment compatibility are key for global businesses.

4. Customer Support: Ensure 24/7 support with multilingual assistance, especially for international transactions across time zones.

5. Fraud Prevention: Look for additional security measures, such as 2FA (Two-Factor Authentication) and real-time fraud detection tools, which are essential for protecting your business and your customers.

PayGlocal offers transparent and standard pricing with no markup, hidden charges, or monthly/annual fees. Transparent pricing, no surprises.

As you evaluate the essential considerations for choosing the right merchant payment service, it's important to know how these factors directly contribute to a secure process. With these elements in mind, let's summarize how the right payment platform can support your business growth.

Conclusion

Merchant payment services have become vital to modern business operations, enabling smooth, secure, and efficient transactions for businesses and customers.

These services offer numerous benefits that help businesses thrive, from improving customer convenience to expanding sales opportunities. However, selecting the right payment platform is crucial as it meets the needs of today’s transactions and scales with future growth.

PayGlocal stands out as a leader in payment processing, offering seamless, secure, and multi-currency solutions for businesses globally. With support for 33 currencies and coverage in 180+ countries, PayGlocal guarantees that businesses can effortlessly manage cross-border transactions and cater to customers worldwide.

Whether expanding into new markets or streamlining your payments, PayGlocal provides a robust, scalable solution to meet your international and domestic payment needs. Get Started Today!

FAQs

1. What’s the difference between merchant services and a merchant account?

A merchant account is a dedicated bank account for processing payments. Funds are held there before being transferred to your regular business account.

Merchant services encompass various solutions, including payment processing, e-commerce support, loyalty programs, and more. These services help manage transactions and enhance payment capabilities.

2. What is an example of a merchant payment?

An example of a merchant payment is when a customer buys a product or service and pays using a credit card, debit card, or another electronic payment method.

. What is a merchant fee?

A merchant fee is a charge businesses incur whenever a customer purchases using a card. These fees are part of the overall cost for payment processing services merchants provide.