Your international buyer just requested TT payment terms. You have seen the term on invoices and emails, but you are not sure what it means or how to set the right terms. One misplaced digit or a poorly structured advance can trap your working capital for weeks.

India's exports hit $634.26 billion in just nine months of 2025, and a large share of those payments also moved through payment terms like TT. But for modern businesses, just knowing TT isn't enough. You need to know how to structure these terms to protect your margins from hidden bank fees and your shipment from payment failures.

This guide provides a complete breakdown of payment terms TT, from the most secure structures for new deals to the hidden costs of intermediary banks, and how to choose the right terms to keep your global cash flow moving.

A wrong assumption about payment terms can hold up your entire shipment. Most disputes in international trade start not with the product, but with how and when money changes hands.

TT stands for telegraphic transfer. The name comes from the old telegraph system that banks once used to send payment instructions across borders. Today, TT simply means an electronic bank-to-bank transfer. It is also referred to as a wire transfer or bank wire.

In practice, when someone says "TT payment terms," they mean the agreed schedule and breakdown for sending funds via a bank wire in a trade deal. TT is the method. The "terms" part refers to when and how much the buyer pays at each stage. That is what you negotiate with your buyer or supplier.

For example, if you are an Indian exporter selling textiles to a buyer in the US, your TT payment terms might say "30% advance, 70% before shipment." This means the buyer sends 30% of the total order value to your bank before production starts, and pays the remaining 70% after inspection but before you ship the goods. The money moves through the SWIFT network, which connects banks globally to process these transfers.

Despite newer payment methods entering the market, TT remains the preferred choice for cross-border trade. There are clear reasons why businesses on both sides of a deal keep using it.

Here are the main benefits of TT payments:

TT works best when both parties have a clear agreement on terms and trust each other enough to skip document-heavy methods. The simplicity is its biggest advantage.

Tip: Always confirm TT payment terms in writing before starting production. A clear written agreement protects both sides if a dispute comes up later.

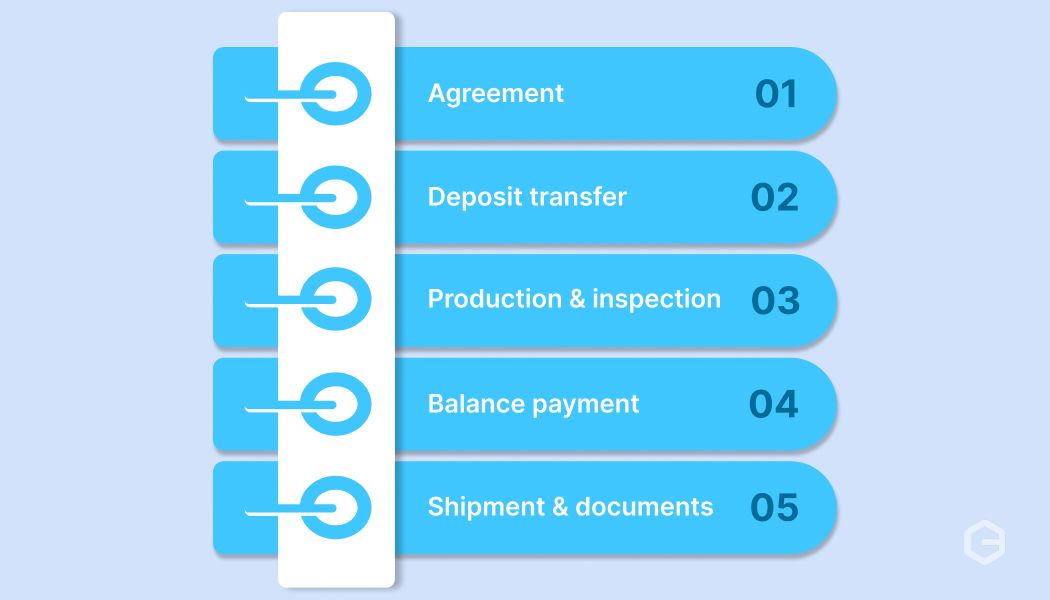

One missing detail in a bank transfer can hold your funds for days. Most delays happen not because of the bank, but because the sender filled in the wrong fields. Here's how a TT payment works from start to finish.

1. Agreement: Buyer and seller agree on the payment structure, timeline, and total amount. For instance, 30% deposit before production and 70% before shipment.

2. Deposit transfer: The buyer goes to their bank (or uses online banking) and initiates a wire transfer for the deposit amount using the seller's bank details.

3. Production and inspection: Once the deposit clears, the seller starts production. The buyer can arrange a third-party inspection before the final payment.

4. Balance payment: After inspection (or at the agreed milestone), the buyer sends the remaining balance through another TT transfer.

5. Shipment and documents: Once the full payment clears, the seller ships the goods and sends original documents like the bill of lading, packing list, and commercial invoice to the buyer.

The entire process from deposit to final payment usually takes 1 to 5 business days per transfer, depending on the banks and countries involved.

Note: Intermediary banks (also called correspondent banks) sometimes sit between the sending and receiving banks. Each intermediary can add time and deduct a small fee from the transfer amount.

A rejected transfer almost always comes down to incorrect or incomplete bank details. Getting this right the first time saves you days of back-and-forth with your bank. Before you initiate a TT payment, collect these details from the recipient.

Check every detail before you hit send. One wrong digit in the account number or SWIFT code can route your payment to the wrong bank or bounce it back entirely.

Tip: Always verify bank details through a phone call or a second trusted channel, especially if the details are sent over email. This is one of the simplest ways to protect your payment.

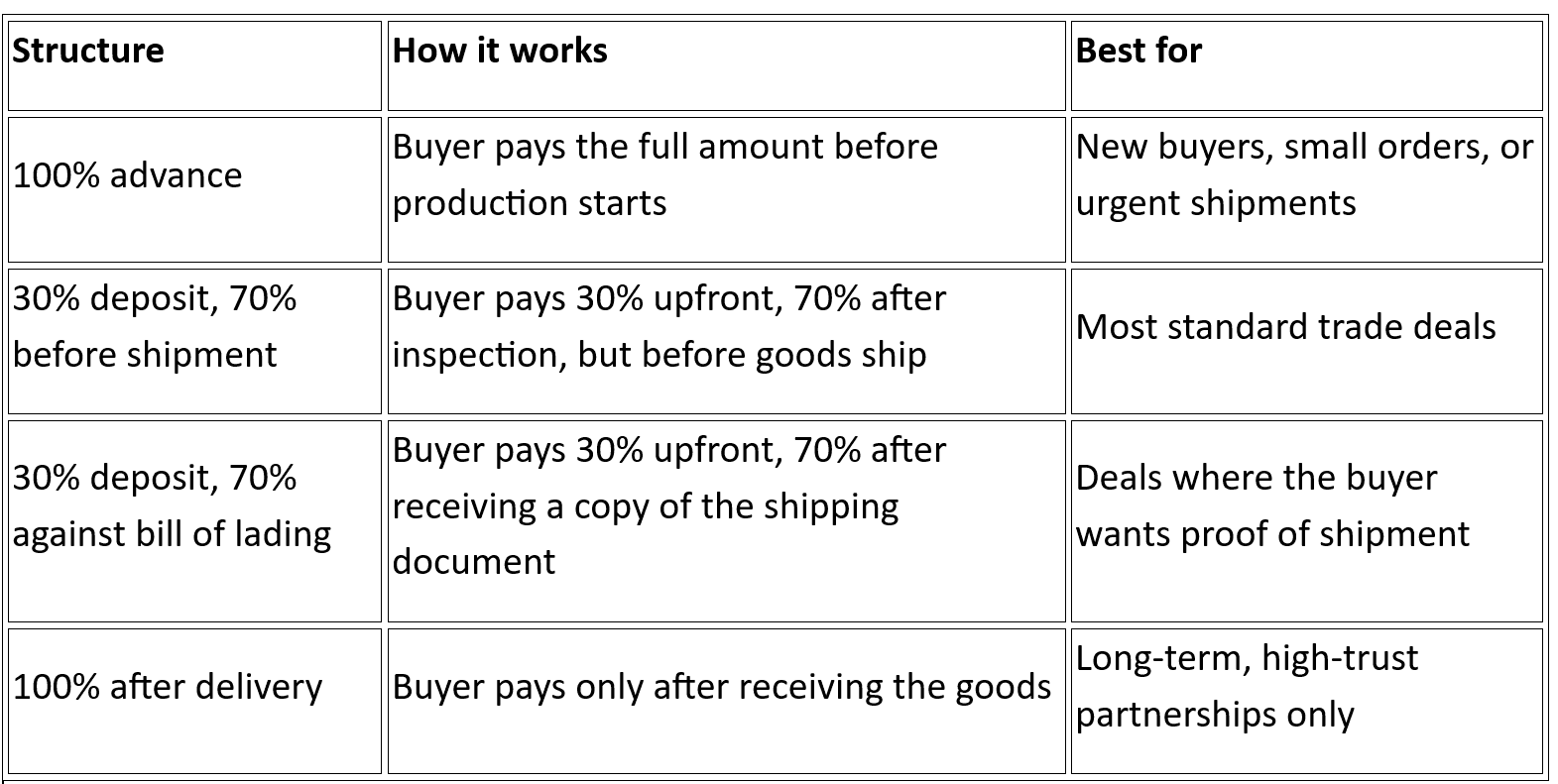

Picking the wrong payment structure can put your cash flow at risk or scare off a good buyer. The terms you choose should match the trust level and order size of each deal. Here's a quick comparison of the most common TT payment structures.

Each structure shifts risk differently between buyer and seller. Here's what each one looks like in practice.

The buyer pays the entire order value before production begins. This is the safest option for sellers because you have all the funds before spending anything on materials or labor. For buyers, it carries the most risk.

This structure is common for first-time orders, sample orders, or very small deals where the amount is low enough that the buyer is comfortable paying upfront.

This is the most widely used TT structure in global trade. The buyer sends 30% to start production. After the goods are ready (and sometimes inspected), the buyer sends the remaining 70% before the seller ships.

For instance, if your order is worth $10,000, the buyer sends $3,000 first. Once production is done and both sides are satisfied, the buyer sends $7,000. Only then do you ship the goods.

This works like the previous structure, but the final 70% is paid after the buyer receives a copy of the bill of lading (a shipping document proving the goods are on their way). It gives the buyer slightly more assurance that the goods have actually shipped.

The risk for the seller here is that the goods are already in transit when the final payment comes. If the buyer delays payment, recovering the goods becomes difficult.

The buyer pays the full amount only after receiving the goods. This is rare and carries a high risk for the seller. It is typically reserved for long-standing relationships where both sides have built deep trust over many successful transactions.

A transfer fee sounds reasonable until the hidden charges stack up. Hidden charges from intermediary banks and unfavorable exchange rates are the two biggest surprises. Here are the typical costs involved in a TT payment.

The total cost of a single TT transaction can range from $30 to over $100, depending on the banks, countries, and currencies involved.

Note: Always ask your bank for a breakdown of all charges before initiating a transfer. Some banks bundle fees in a way that makes it hard to see the true cost.

A TT payment moves fast, but it offers little protection once the money leaves your account. Unlike a letter of credit, there is no bank in the middle to guarantee that either side follows through. Here are the main risks to watch for.

Tip: For high-value transactions with new partners, consider starting with smaller test orders and higher advance percentages to limit your exposure.

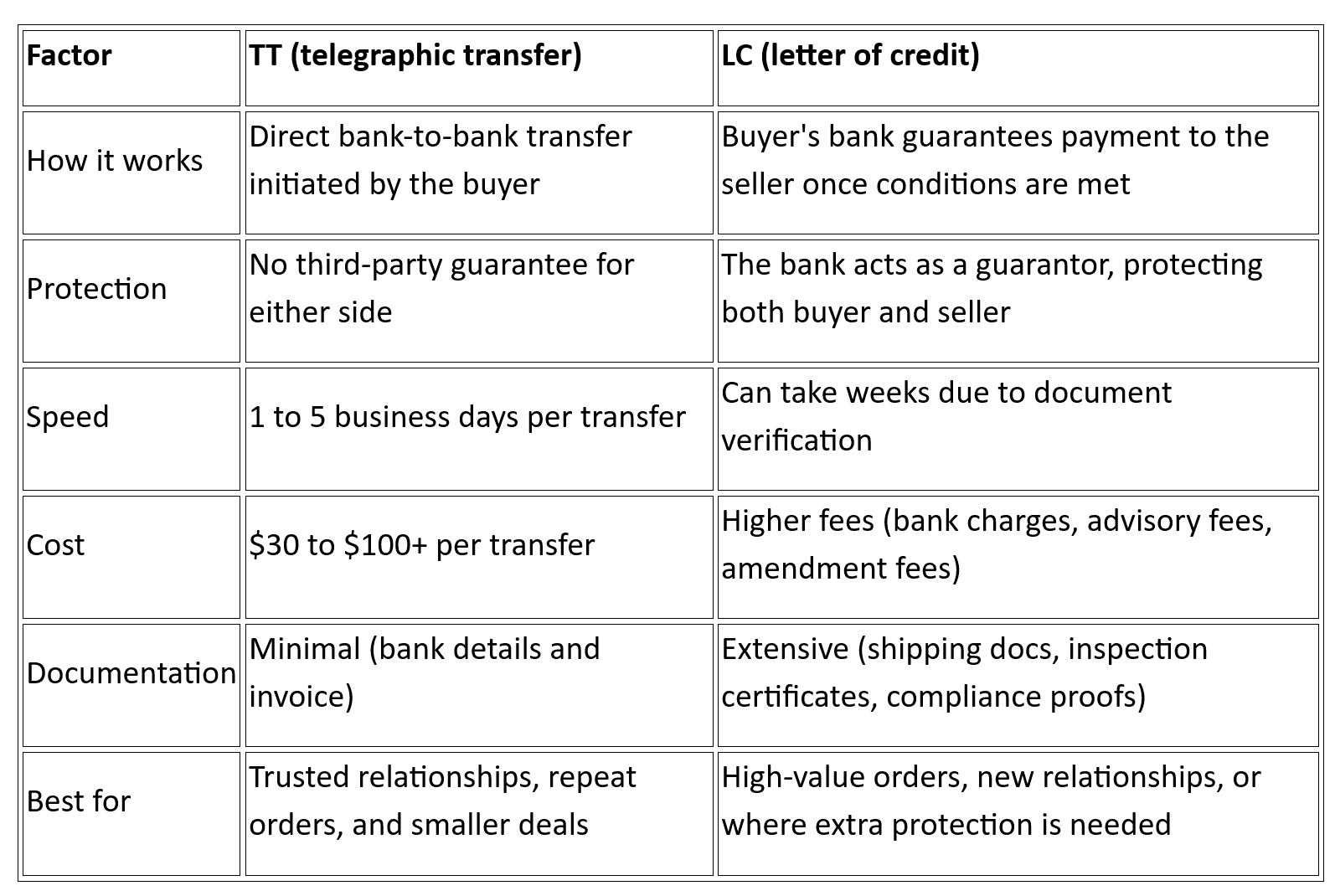

Choosing between TT and a letter of credit (LC) is one of the first decisions you face in any international deal. Both move money across borders, but they work very differently in terms of protection and process. Here's a side-by-side comparison.

TT is simpler, faster, and cheaper. LC offers more protection but takes longer and costs more. Most businesses start with LC for the first few orders and move to TT once trust is built.

If your deal involves a new buyer and a large order value, LC gives you a safety net. For repeat buyers with a good payment history, TT keeps the process quick and the costs low.

The best payment terms are the ones both sides can agree on without putting either at unnecessary risk. Your choice should depend on a few practical factors.

When negotiating, start with industry-standard terms. If you are placing a larger order or committing to repeat business, use that as a reason to ask for better terms. Most suppliers and buyers expect some back-and-forth on payment structures.

Bank wires and TT transfers work, but they come with delays, hidden fees, and limited visibility into where your money is at any given moment. For Indian businesses selling to global buyers, these friction points add up with every transaction.

PayGlocal gives you a simpler way to collect international payments. Here's what you get:

Whether you export goods, sell services, or run an online store, PayGlocal helps you collect payments from global customers with less friction and more control. No more chasing bank wires across time zones.

TT payment terms are a core part of international trade. They give buyers and sellers a clear, structured way to move money across borders through bank-to-bank transfers. The key is choosing the right payment structure based on your relationship, order size, and risk tolerance.

Start with higher advances for new partners. Move to flexible terms as trust builds. Always verify bank details before every transfer, and keep your payment terms in writing.

If you want to move beyond traditional TT bank wires and collect international payments with less friction, PayGlocal can help. Several Indian businesses are already using it to accept payments in 33+ currencies with transparent pricing and no setup fees. Get started with PayGlocal today before your next deal hits a payment delay.

India's exports hit $634.26 billion in just nine months of 2025, and a large share of those payments also moved through payment terms like TT. But for modern businesses, just knowing TT isn't enough. You need to know how to structure these terms to protect your margins from hidden bank fees and your shipment from payment failures.

This guide provides a complete breakdown of payment terms TT, from the most secure structures for new deals to the hidden costs of intermediary banks, and how to choose the right terms to keep your global cash flow moving.

Key takeaways

- TT stands for telegraphic transfer: It is an electronic bank-to-bank payment method used widely in international trade to send and receive funds across borders.

- Transfers typically take 1 to 5 business days: The timeline depends on the banks involved, intermediary banks in the chain, and the currencies being transferred.

- Costs include bank fees and currency conversion charges: Expect to pay around $20 to $50 per transfer, plus exchange rate markups that vary by bank.

- TT offers speed but limited protection: Unlike a letter of credit (LC), TT does not have built-in safeguards, so the payment structure you choose matters.

- PayGlocal simplifies international payment collection: With multi-currency accounts and transparent pricing, PayGlocal helps Indian businesses easily collect payments from global customers.

What are the TT payment terms?

A wrong assumption about payment terms can hold up your entire shipment. Most disputes in international trade start not with the product, but with how and when money changes hands.

TT stands for telegraphic transfer. The name comes from the old telegraph system that banks once used to send payment instructions across borders. Today, TT simply means an electronic bank-to-bank transfer. It is also referred to as a wire transfer or bank wire.

In practice, when someone says "TT payment terms," they mean the agreed schedule and breakdown for sending funds via a bank wire in a trade deal. TT is the method. The "terms" part refers to when and how much the buyer pays at each stage. That is what you negotiate with your buyer or supplier.

For example, if you are an Indian exporter selling textiles to a buyer in the US, your TT payment terms might say "30% advance, 70% before shipment." This means the buyer sends 30% of the total order value to your bank before production starts, and pays the remaining 70% after inspection but before you ship the goods. The money moves through the SWIFT network, which connects banks globally to process these transfers.

What are the benefits of TT payments?

Despite newer payment methods entering the market, TT remains the preferred choice for cross-border trade. There are clear reasons why businesses on both sides of a deal keep using it.

Here are the main benefits of TT payments:

- Fast processing: TT payments typically clear in 1 to 5 business days, which is faster than cheques, demand drafts, or most document-based payment methods.

- Wide global acceptance: Almost every bank in every country can send and receive TT payments. You do not need a special account or platform to use it.

- Works with most currencies: You can send TT payments in USD, EUR, GBP, AED, and dozens of other currencies. Your bank handles the conversion at the time of transfer.

- Simple process: TT does not require complex documentation like a letter of credit. You need the recipient's bank details, and the transfer can be initiated online or at a branch.

- Good for recurring trade: Once you set up the payment details with your bank, repeat transfers to the same supplier or buyer are quick and straightforward.

TT works best when both parties have a clear agreement on terms and trust each other enough to skip document-heavy methods. The simplicity is its biggest advantage.

Tip: Always confirm TT payment terms in writing before starting production. A clear written agreement protects both sides if a dispute comes up later.

How does a TT payment work?

One missing detail in a bank transfer can hold your funds for days. Most delays happen not because of the bank, but because the sender filled in the wrong fields. Here's how a TT payment works from start to finish.

1. Agreement: Buyer and seller agree on the payment structure, timeline, and total amount. For instance, 30% deposit before production and 70% before shipment.

2. Deposit transfer: The buyer goes to their bank (or uses online banking) and initiates a wire transfer for the deposit amount using the seller's bank details.

3. Production and inspection: Once the deposit clears, the seller starts production. The buyer can arrange a third-party inspection before the final payment.

4. Balance payment: After inspection (or at the agreed milestone), the buyer sends the remaining balance through another TT transfer.

5. Shipment and documents: Once the full payment clears, the seller ships the goods and sends original documents like the bill of lading, packing list, and commercial invoice to the buyer.

The entire process from deposit to final payment usually takes 1 to 5 business days per transfer, depending on the banks and countries involved.

Note: Intermediary banks (also called correspondent banks) sometimes sit between the sending and receiving banks. Each intermediary can add time and deduct a small fee from the transfer amount.

What do you need to send a TT payment?

A rejected transfer almost always comes down to incorrect or incomplete bank details. Getting this right the first time saves you days of back-and-forth with your bank. Before you initiate a TT payment, collect these details from the recipient.

- Beneficiary full name: The exact name on the recipient's bank account. Even a small mismatch can cause the bank to reject or delay the transfer.

- Bank name and branch address: The full name and physical address of the recipient's bank branch.

- Account number: The recipient's bank account number where the funds should be credited.

- SWIFT or BIC code: A unique code that identifies the recipient's bank in the global SWIFT network. Every international bank transfer needs this.

- IBAN (if applicable): Some countries in Europe and the Middle East require an international bank account number (IBAN) in addition to the regular account number.

- Payment reference or invoice number: Include your invoice or order number so the recipient can match the payment to the correct transaction.

- Currency and amount: Confirm the exact currency and amount to avoid conversion confusion at either end.

Check every detail before you hit send. One wrong digit in the account number or SWIFT code can route your payment to the wrong bank or bounce it back entirely.

Tip: Always verify bank details through a phone call or a second trusted channel, especially if the details are sent over email. This is one of the simplest ways to protect your payment.

What are the common TT payment structures?

Picking the wrong payment structure can put your cash flow at risk or scare off a good buyer. The terms you choose should match the trust level and order size of each deal. Here's a quick comparison of the most common TT payment structures.

Each structure shifts risk differently between buyer and seller. Here's what each one looks like in practice.

1. 100% advance payment

The buyer pays the entire order value before production begins. This is the safest option for sellers because you have all the funds before spending anything on materials or labor. For buyers, it carries the most risk.

This structure is common for first-time orders, sample orders, or very small deals where the amount is low enough that the buyer is comfortable paying upfront.

2. 30% deposit, 70% before shipment

This is the most widely used TT structure in global trade. The buyer sends 30% to start production. After the goods are ready (and sometimes inspected), the buyer sends the remaining 70% before the seller ships.

For instance, if your order is worth $10,000, the buyer sends $3,000 first. Once production is done and both sides are satisfied, the buyer sends $7,000. Only then do you ship the goods.

3. 30% deposit, 70% against bill of lading

This works like the previous structure, but the final 70% is paid after the buyer receives a copy of the bill of lading (a shipping document proving the goods are on their way). It gives the buyer slightly more assurance that the goods have actually shipped.

The risk for the seller here is that the goods are already in transit when the final payment comes. If the buyer delays payment, recovering the goods becomes difficult.

4. 100% after delivery

The buyer pays the full amount only after receiving the goods. This is rare and carries a high risk for the seller. It is typically reserved for long-standing relationships where both sides have built deep trust over many successful transactions.

What does a TT payment cost?

A transfer fee sounds reasonable until the hidden charges stack up. Hidden charges from intermediary banks and unfavorable exchange rates are the two biggest surprises. Here are the typical costs involved in a TT payment.

- Bank transfer fees: Most banks generally charge a flat fee of $20 to $50 per outgoing international wire transfer. Receiving banks can also charge a smaller fee on the incoming side.

- Currency conversion charges: If the payment involves converting one currency to another, the bank applies its own exchange rate, which usually includes a markup of 1% to 3% over the mid-market rate.

- Intermediary bank fees: When the sending and receiving banks do not have a direct relationship, one or more intermediary banks process the transfer. Each can deduct $10 to $30 from the payment amount before it reaches you.

The total cost of a single TT transaction can range from $30 to over $100, depending on the banks, countries, and currencies involved.

Note: Always ask your bank for a breakdown of all charges before initiating a transfer. Some banks bundle fees in a way that makes it hard to see the true cost.

What are the risks of TT payments?

A TT payment moves fast, but it offers little protection once the money leaves your account. Unlike a letter of credit, there is no bank in the middle to guarantee that either side follows through. Here are the main risks to watch for.

- No built-in buyer or seller protection: Once a TT payment is sent, reversing it is very difficult. If the seller does not ship the goods after receiving payment, the buyer has limited options to recover the funds.

- Fraud risk from fake bank details: Email scams where someone poses as your supplier and sends fake bank details are common in international trade. Always verify details through a second trusted channel.

- Currency fluctuation: If there is a gap between when you agree on the price and when payment is sent, exchange rate changes can affect how much either side actually receives.

- Payment delays from errors: A wrong account number, incorrect SWIFT code, or misspelled beneficiary name can delay the transfer by days or even cause it to bounce back entirely.

Tip: For high-value transactions with new partners, consider starting with smaller test orders and higher advance percentages to limit your exposure.

How do TT payment terms compare to a letter of credit?

Choosing between TT and a letter of credit (LC) is one of the first decisions you face in any international deal. Both move money across borders, but they work very differently in terms of protection and process. Here's a side-by-side comparison.

TT is simpler, faster, and cheaper. LC offers more protection but takes longer and costs more. Most businesses start with LC for the first few orders and move to TT once trust is built.

If your deal involves a new buyer and a large order value, LC gives you a safety net. For repeat buyers with a good payment history, TT keeps the process quick and the costs low.

How to choose the right TT payment terms for your business

The best payment terms are the ones both sides can agree on without putting either at unnecessary risk. Your choice should depend on a few practical factors.

- Relationship history: For first-time buyers or suppliers, ask for a higher advance (50% to 100%). For repeat partners with a proven track record, you can offer more flexible terms.

- Order value: Larger orders carry more risk. A 30/70 structure works well for mid-size orders, but for very large shipments, consider milestone-based payments tied to production stages.

- Product type: Custom or perishable goods are harder to resell if the deal falls apart. Ask for stronger terms when the product cannot easily be sold to another buyer.

- Payment speed needs: If you need funds quickly to start production, negotiate for a larger upfront deposit. This keeps your cash flow healthy while the order is in progress.

- Your role in the deal: Exporters (sellers) benefit from higher advances. Importers (buyers) benefit from paying later. Find a middle ground that keeps the deal moving.

When negotiating, start with industry-standard terms. If you are placing a larger order or committing to repeat business, use that as a reason to ask for better terms. Most suppliers and buyers expect some back-and-forth on payment structures.

Switch from slow TT payments to faster global payments with PayGlocal

Bank wires and TT transfers work, but they come with delays, hidden fees, and limited visibility into where your money is at any given moment. For Indian businesses selling to global buyers, these friction points add up with every transaction.

PayGlocal gives you a simpler way to collect international payments. Here's what you get:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD, and globally in 33+ currencies from 180+ countries without opening separate bank accounts in each country.

- Dynamic checkout: Offer your customers a fast, secure checkout experience that works across devices and payment methods, reducing drop-offs at the final step.

- Transparent pricing with no hidden costs: No setup fees, platform fees, or documentation charges. You pay only when you perform the transaction.

- Instant FIRC on settlement: Get your foreign inward remittance certificate (FIRC) delivered right to your inbox after every settlement, keeping your compliance on track.

- Real-time payment tracking: Stay informed with frequent notifications on your fund status at every step, so you always know the status of your funds.

Whether you export goods, sell services, or run an online store, PayGlocal helps you collect payments from global customers with less friction and more control. No more chasing bank wires across time zones.

Final thoughts

TT payment terms are a core part of international trade. They give buyers and sellers a clear, structured way to move money across borders through bank-to-bank transfers. The key is choosing the right payment structure based on your relationship, order size, and risk tolerance.

Start with higher advances for new partners. Move to flexible terms as trust builds. Always verify bank details before every transfer, and keep your payment terms in writing.

If you want to move beyond traditional TT bank wires and collect international payments with less friction, PayGlocal can help. Several Indian businesses are already using it to accept payments in 33+ currencies with transparent pricing and no setup fees. Get started with PayGlocal today before your next deal hits a payment delay.