Introduction

Every year, more business owners in India are filing their taxes on time.

In fact, recent data shows that over 7.28 crore income tax returns were filed for the 2024–25 assessment year by July 31, 2024, representing a 7.5% increase compared to the previous year.

But while considering your tax return filing, you might have come across the term “presumptive income.”

So, what exactly does it mean, who can qualify for it, and what are its benefits?

In this guide, we break down presumptive income in simple terms along with examples.

By the end, you'll know how this scheme fits into your business.

Key Takeaways

- What presumptive income is: A simplified tax calculation method where you declare a fixed percentage of your revenue as profit instead of maintaining detailed expense records.

- Who qualifies: Small businesses with turnover up to ₹3 crore and professionals with receipts up to ₹75 lakh can use this scheme if they meet digital payment criteria.

- Fixed profit rates: Businesses declare 6–8% of turnover as income, while professionals declare 50% of their receipts as taxable profit.

- Digital payments matter: Businesses that keep cash receipts under 5% of total receipts qualify for higher turnover limits and lower tax rates.

- How PayGlocal helps: Accept digital payments globally and stay compliant with automated records.

What is Presumptive Income?

Presumptive income is a simplified way to calculate your taxable income.

Instead of tracking every single expense throughout the year, you declare a fixed percentage of your annual revenue as profit.

The tax department then applies tax rates to that presumed profit.

This approach saves small businesses and professionals from maintaining detailed books of accounts and undergoing tax audits.

You calculate tax on an estimated profit rather than actual profit after expenses.

Example:

If you run a consulting business earning ₹60 lakh annually, you can declare 50% of that amount (₹30 lakh) as your taxable income.

You pay tax on ₹30 lakh without needing to show receipts for every business expense like travel, software subscriptions, or office supplies.

The scheme assumes your expenses are already accounted for in the remaining 50%.

The idea behind this scheme is practical — small taxpayers don't always have the resources to hire accountants or maintain complex financial records.

This option makes tax compliance accessible while encouraging more businesses to formalize their operations.

What are the Benefits of Presumptive Income?

Small businesses and professionals gain several advantages when they opt for presumptive income taxation:

- Simpler compliance requirements: No need to maintain detailed books or hire expensive accountants.

- No tax audit needed: Exempt from mandatory tax audits, reducing stress and costs.

- Easier tax filing: Use the simplified ITR-4 (Sugam) form instead of complex ones.

- Predictable tax calculation: Know your tax liability in advance for better planning.

- Rewards digital transactions: Higher revenue limits and lower profit rates for digital payments.

- Focus on growth: Spend less time on compliance and more on running your business.

This scheme works particularly well for businesses with healthy profit margins.

If your actual expenses are low compared to revenue, presumptive taxation can be more beneficial than regular taxation.

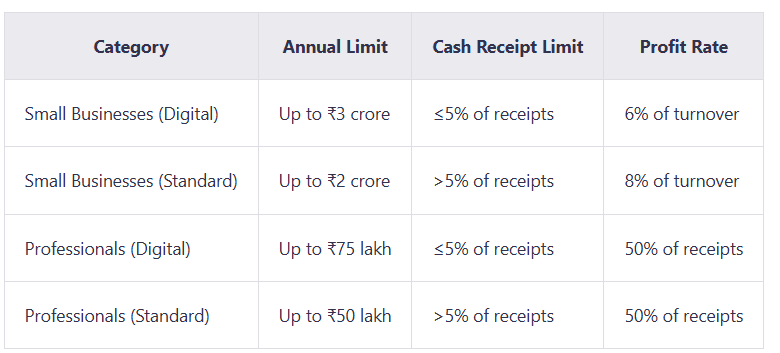

Who Can opt for Presumptive Income?

Here are the main categories of taxpayers who can use the presumptive income scheme, along with their eligibility criteria and limits.

Small Businesses

- Eligible entities: Retail shops, traders, service providers, and similar businesses.

- Turnover limits:

- Standard limit: ₹2 crore

- Enhanced limit: ₹3 crore (if cash receipts ≤5% of total receipts)

Example:

If you run an online clothing store with ₹2.5 crore annual sales and 98% of payments are digital, you qualify for the higher ₹3 crore limit.

Professionals

- Eligible professionals: Freelancers, consultants, doctors, lawyers, architects, engineers, etc.

- Receipts limits:

- Standard limit: ₹50 lakh

- Enhanced limit: ₹75 lakh (if cash receipts ≤5% of total receipts)

Example:

A graphic designer earning ₹65 lakh annually through bank transfers qualifies due to majority digital payments.

A doctor receiving mostly cash payments must stay under ₹50 lakh to qualify.

Presumptive Income Summary Table

Businesses that accept payments through banking channels, payment gateways, or digital wallets automatically qualify for these enhanced benefits.

The government designed these incentives to encourage transparent, traceable transactions.

How Does Presumptive Income Work?

The calculation method depends on whether you’re a business owner or professional.

Here’s how it works:

- For small businesses with mostly digital payments: Declare 6% of turnover as taxable income.

- Example: A retail store with ₹1.5 crore revenue and 97% digital receipts → ₹9 lakh taxable income.

- For small businesses with more cash transactions: Declare 8% of turnover as taxable income.

- Example: ₹1.5 crore revenue with 80% digital receipts → ₹12 lakh taxable income.

- For professionals: Declare 50% of total receipts as taxable income regardless of payment mode.

- Example: Consultant earning ₹60 lakh → ₹30 lakh taxable income.

Once the presumptive income is calculated, standard income tax rates are applied based on your tax slab.

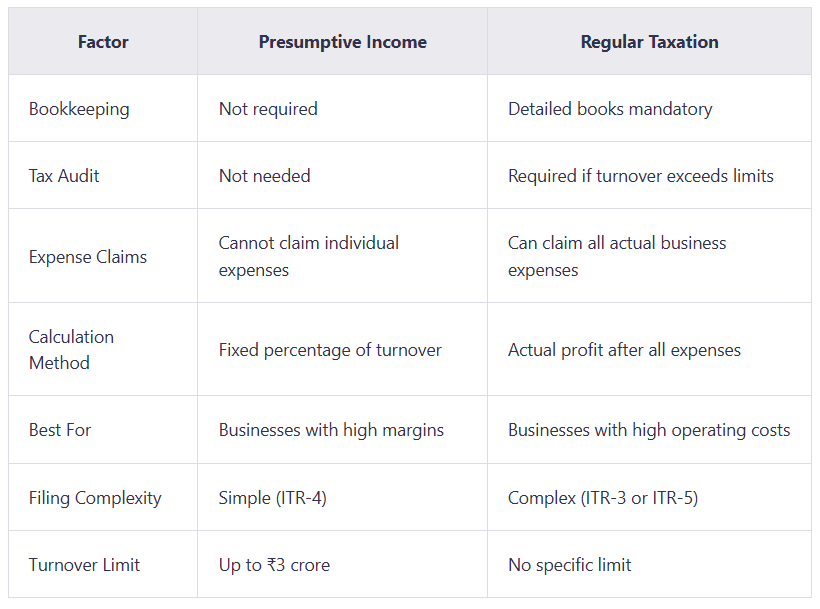

What is the Difference Between Presumptive Income and Regular Taxation?

Choosing between the presumptive income scheme and regular taxation depends on your business model and profit margins.

The presumptive system is simpler and faster, while regular taxation may suit larger businesses with higher expenses that can be claimed for deductions.

Would you like me to also format the “difference between presumptive and regular taxation” section into a comparison table (for Strapi CMS display)?

Here’s your full content formatted cleanly for Strapi, with proper headings, bold emphasis, bullets, and tables — ready to paste directly 👇

Difference Between Presumptive Income and Regular Taxation

When to Choose Regular Taxation

Regular taxation suits businesses with substantial expenses.

If you spend heavily on inventory, marketing, salaries, rent, or equipment, claiming actual expenses might reduce your tax liability more than presumptive rates.

Example:

- A business with ₹2 crore turnover but ₹1.6 crore in actual expenses has a real profit of ₹40 lakh.

- Under presumptive taxation at 8%, taxable income = ₹16 lakh → lower tax payable.

- f actual expenses are only ₹1 crore, real profit = ₹1 crore, while presumptive income = ₹16 lakh → presumptive scheme is more beneficial.

Regular taxation requires maintaining purchase bills, salary records, rent agreements, and receipts.

This demands time, accounting tools, and often professional help.

Presumptive taxation removes this burden entirely.

Tip:

Your decision should depend on your expense ratio.

If your typical profit margin exceeds presumptive rates (6–8% for businesses, 50% for professionals), the simplified scheme works well.

If margins are lower due to high expenses, regular taxation may be more suitable despite added complexity.

Accept Global Payments and Stay Compliant with PayGlocal

Presumptive income simplifies tax compliance — but if you’re doing global transactions, payment collection can be a challenge.

If you're exporting services or goods, you need a reliable solution that handles multiple currencies, provides compliance documentation, and keeps transactions fully digital.

That’s where PayGlocal comes in.

How PayGlocal Helps Businesses

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries. Clients can pay in their local currency while you receive funds in INR.

- Automatic compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) directly in your inbox after settlement — no chasing banks.

- Zero fixed costs: Pay only when you transact — no monthly fees, setup charges, or hidden costs.

- Recurring payments: Automate subscription billing for ongoing services.

- Sanction screening: Built-in checks ensure all transactions meet regulatory compliance.

When you use digital payment solutions like PayGlocal, you automatically meet the 95% digital receipt criteria for presumptive taxation.

This means higher turnover limits, lower profit rates, and audit-ready records.

Whether you're a freelance developer, an exporter, or a consultant, PayGlocal helps you get paid faster and stay compliant.

Final Thoughts

Presumptive income offers an effective way to handle tax compliance while focusing on growth.

The scheme works best when your profit margins are healthy and you want to avoid complex bookkeeping.

Going digital amplifies these benefits:

- Higher turnover limits

- Lower profit rates

- Better record-keeping

- Greater transparency

If you collect international payments, you need more than just a simplified tax scheme — you need a payment infrastructure that works across borders.

PayGlocal delivers exactly that:

Accept global payments, settle in INR, and maintain digital records that make tax compliance effortless.

No complex fees. No setup hassles. Just payments that work.

Get started with PayGlocal today and take your business global while keeping compliance simple.