If you've ever sent or received money within India, you know it's instant and transparent. Our country handles nearly 49% of the world's real-time payments, making us a leader in digital banking.

But as soon as you step outside your borders to work with international clients, that speed and clarity disappear. Suddenly, you're back to waiting days for transfers and seeing "short" payments land in your account. The reality is that international payments still move through an old, expensive system of global banks, and each one takes a cut of your profit.

This guide breaks down what cross-border payment fees actually are, the different types of fees you'll face, and how you can keep more of your earnings.

Cross-border payment fees are charges applied when you send or receive money across international borders. These fees cover the cost of moving money between different countries, currencies, and banking systems.

When a client in the US pays you in India, that transaction crosses borders. As the money has to travel through different banks and regulations, every 'stop' it makes along the way takes a small bite out of the total amount. While some fees are visible as line items, others hide inside exchange rates.

For example, if a European client pays you €1,000, you might see a 2% transaction fee listed clearly. But the currency conversion happens at a rate that's 1.5% worse than the actual market rate. In this case, your total cost was 3.5%, even though the bank made it look like only 2%.

Most businesses focus on the transaction fee percentage. The real cost includes everything that reduces what you actually receive. That's why knowing the full fee structure matters more than comparing single numbers.

Cross-border fees apply the moment a transaction moves between two different countries. It doesn't matter if you are being paid in Dollars, Euros, or Rupees; the fee is triggered by where the money starts its journey and where it ends up.

Here are the most common times you'll encounter these fees:

The location of the card issuer, bank, or payment account determines if fees apply, not just the currency used. This means a European client paying you in EUR still triggers cross-border fees because the payment travels from their European bank to your Indian account.

When your client clicks "pay," it might feel like the money should arrive instantly. But behind the scenes, that payment is taking a long journey through several different systems. Each stop along the way is where the fees you see on your statement are created.

Here's what happens during that journey:

This entire process can take seconds for card payments or several days for wire transfers. The complexity is why multiple parties charge fees. Every institution involved in moving your money takes a fee for its role in the chain.

When you receive an international payment, you aren't just paying one fee. Several different charges are often stacked on top of each other. For example, a single $5,000 payment can be hit by a processing fee, a currency markup, and bank charges all at once.

Here is a breakdown of what these fees actually cost you:

Tip: Don't just look at the transaction fee. A provider might offer a "low" 1% fee, but then take an extra 2% through a poor exchange rate. Always check the total amount that actually hits your bank account.

The countries you deal with also play a role. Converting USD to INR is usually cheaper than other currencies because it is a very common route.

The biggest factor, however, is your provider. Traditional banks often hide a 2% to 3% charge inside their exchange rates, while modern platforms stay much closer to the real market rate. A 2% difference might not seem like much on one invoice, but it can easily add up to lakhs of rupees in lost profit over a year.

Sometimes it's easier to see the impact of fees by looking at actual numbers. Here are four common situations showing what a business invoices versus what they actually get to keep.

Freelancer receiving $3,000 from a US client via an international card

Your client pays $3,000 through an international card payment. The payment processor charges 3% transaction fee ($90) and applies a 1.5% FX markup on the USD to INR conversion ($45). You receive $2,865 in your account. You lost $135 (4.5%) on a single invoice.

Exporter receiving €20,000 from European buyer via wire transfer

Your buyer sends €20,000 through their bank. Their bank charges a €25 sending fee, your bank charges a $30 receiving fee, and an intermediary bank deducts $20. The exchange rate applied has a 1.2% markup (€240). After all deductions, you receive approximately €19,685 worth in INR. You lost €315 (1.6%) to various banks.

SaaS company with $8,000 monthly recurring revenue from global customers

Your payment platform charges 2.5% per transaction and includes a 0.8% FX markup in its bundled rate. On your $8,000 monthly recurring revenue, you pay $264 in combined fees. Over a year, that's $3,168 in costs. By switching to an all-in provider at 2%, you would only pay $1,920, saving you $1,248 annually.

Service exporter receiving a $50,000 project payment via a payment platform

Your client pays through a modern payment platform with transparent pricing. The platform fee is 1.5% ($750), and the FX markup is 0.6% ($300). You receive $48,950 after fees. Total cost: $1,050 or 2.1%. Compared to traditional bank wire, you save approximately $500 to $800 on this single transaction.

These examples show how fees compound quickly. The payment method, provider choice, and transaction size all impact what you actually keep. Small differences in fee percentages mean significant amounts on larger or more frequent transactions.

Note: Small, frequent payments lose more to fixed fees. Large, occasional payments lose more to percentage-based charges. Match your payment method to your transaction pattern for the lowest total cost.

Not all international payments cost the same. A $1,000 card payment from the US will have a completely different fee structure than a $10,000 bank transfer from Europe. Understanding these variables helps you choose the right method for every invoice.

Here is what decides your final cost:

By knowing these factors, you can stop guessing and start choosing the payment methods that keep the most money in your pocket.

Cutting your costs doesn't require a complex strategy. Small changes in how you receive money and which providers you choose can save you thousands of dollars every year. Here is what actually works:

Before you sign up, check if a provider shows you their exchange rate upfront. Compare it to the "mid-market rate" you see on Google. If the markup is more than 1%, you are likely overpaying.

This is one of the most effective ways to save. Having a USD account allows a US client to pay you as if they were sending money to a local neighbor. This removes the "cross-border" trigger and lets you control exactly when you want to convert that money into INR.

If you are receiving less than $5,000, avoid bank wire transfers; the fixed fees will eat too much of your profit. For smaller, frequent amounts, use a payment platform. Save wire transfers for very large, one-time payments.

Many payment providers have tiered pricing. If your monthly volume increases, for example, moving from $20,000 to $50,000, don't be afraid to ask for a lower rate. A 0.5% drop in fees can save you a significant amount over a year.

If you can invoice in INR and let the client handle conversion, you avoid FX markup. This works when you have pricing power. Not always possible, but worth considering for long-term clients.

Some providers advertise low transaction fees but add monthly fees, setup costs, or withdrawal charges. Calculate the total monthly cost, not just the per-transaction rate. A provider charging 2% with no other fees is often better than one charging 1.5% plus a $200 monthly fee unless you process high volumes consistently.

High fees shouldn't be the "tax" you pay for winning international clients. When banks hit you with poor exchange rates and hidden charges, you can easily lose 3% to 5% of your invoice before the money even touches your account.

PayGlocal is built specifically for Indian businesses and exporters who need a faster, fairer way to get paid. We replace the "black box" of traditional banking with a transparent system designed to protect your margins.

Here's how PayGlocal reduces your cross-border payment costs:

PayGlocal helps you collect exactly what you invoiced. With lower fees and better rates, we make sure that your global growth actually shows up in your bottom line.

Cross-border payment fees are part of doing business globally, but they shouldn't be a mystery. The difference between losing 5% of your invoice and losing 2% is a significant amount of money that should be staying in your business.

The first step is knowing exactly what you're currently paying. Take a moment to add up your transaction fees, exchange rate markups, and fixed bank charges to find your "total cost." Once you see that number, you can compare it against more transparent providers to find a better deal.

The right payment partner does more than just move money; it simplifies your entire operation. You spend less time chasing compliance documents and less money on hidden fees. This allows you to stop worrying about the mechanics of getting paid and focus on what you do best: growing your business.

Ready to keep more of what you earn on international payments? Get started with PayGlocal today.

But as soon as you step outside your borders to work with international clients, that speed and clarity disappear. Suddenly, you're back to waiting days for transfers and seeing "short" payments land in your account. The reality is that international payments still move through an old, expensive system of global banks, and each one takes a cut of your profit.

This guide breaks down what cross-border payment fees actually are, the different types of fees you'll face, and how you can keep more of your earnings.

Key Takeaways

- Multiple fee types stack up: Cross-border payment fees include transaction charges, currency conversion markups, processing fees, and intermediary bank charges that reduce the amount you receive.

- Typical cost range: Transaction fees typically range from 1% to 3% for cards and 0.6% to 1.4% for international processing, while FX markups add another 0.5% to 2% on top.

- Wire transfers have fixed fees: Wire transfers through banks involve fixed fees of $15 to $50 plus intermediary charges, making them costly for smaller transactions.

- Cost reduction strategies: Choosing providers with transparent FX rates, local currency accounts, competitive processing fees, and no hidden charges significantly reduces costs.

- Cross-border payments platform: PayGlocal offers multi-currency collection with clear pricing and instant compliance documentation.

What are Cross-Border Payment Fees?

Cross-border payment fees are charges applied when you send or receive money across international borders. These fees cover the cost of moving money between different countries, currencies, and banking systems.

When a client in the US pays you in India, that transaction crosses borders. As the money has to travel through different banks and regulations, every 'stop' it makes along the way takes a small bite out of the total amount. While some fees are visible as line items, others hide inside exchange rates.

For example, if a European client pays you €1,000, you might see a 2% transaction fee listed clearly. But the currency conversion happens at a rate that's 1.5% worse than the actual market rate. In this case, your total cost was 3.5%, even though the bank made it look like only 2%.

Most businesses focus on the transaction fee percentage. The real cost includes everything that reduces what you actually receive. That's why knowing the full fee structure matters more than comparing single numbers.

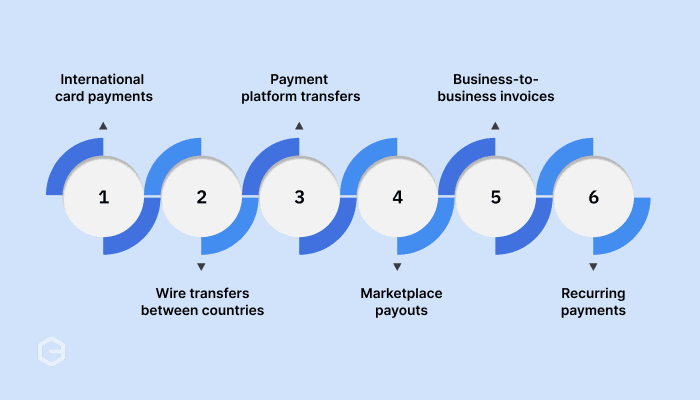

When do Cross-Border Payment Fees Apply?

Cross-border fees apply the moment a transaction moves between two different countries. It doesn't matter if you are being paid in Dollars, Euros, or Rupees; the fee is triggered by where the money starts its journey and where it ends up.

Here are the most common times you'll encounter these fees:

- International card payments: When a customer uses a card issued in one country to pay a business in another country. A US-issued card paying an Indian merchant triggers cross-border fees, even if the transaction is in USD.

- Wire transfers between countries: Any bank-to-bank transfer that crosses borders through the SWIFT network. Sending money from a UK bank to an Indian bank account incurs cross-border charges regardless of currency.

- Payment platform transfers: When you receive payments through payment platforms from international clients. The platform processes the cross-border element and applies its fee structure.

- Marketplace payouts: Receiving earnings from global marketplaces like Amazon, Upwork, or Fiverr. These platforms collect from worldwide customers and pay you internationally, triggering conversion and transfer fees.

- Business-to-business invoices: When you invoice a foreign company, and they pay via international transfer. Both the sending and receiving banks may apply charges.

- Subscription or recurring payments: Automated monthly charges from international customers. Each recurring payment crosses borders and incurs fees every billing cycle.

The location of the card issuer, bank, or payment account determines if fees apply, not just the currency used. This means a European client paying you in EUR still triggers cross-border fees because the payment travels from their European bank to your Indian account.

How do Cross-Border Payments Work?

When your client clicks "pay," it might feel like the money should arrive instantly. But behind the scenes, that payment is taking a long journey through several different systems. Each stop along the way is where the fees you see on your statement are created.

Here's what happens during that journey:

- Payment initiation: Your client authorizes the payment through their bank, card, or payment platform. Their financial institution validates that the account has sufficient funds and approves the transaction.

- Currency conversion: The payment is converted from your client's currency (like USD) to yours (INR). Most providers add a "markup" here, which is a hidden fee on top of the real exchange rate.

- Network routing: The money moves through global networks like SWIFT (for bank wires) or Visa/Mastercard (for cards). These networks connect the foreign bank to your bank in India.

- Intermediary bank processing: For wire transfers, the payment often passes through one or more intermediary banks that facilitate the cross-border movement. Each bank can deduct its handling fee.

- Compliance and fraud checks: To keep the payment safe, it is screened for fraud and legal regulations. This is why some payments take a few extra days to clear.

- Settlement to your account: After all checks and conversions, the remaining amount lands in your business account. You receive a notification and can access the funds based on your provider's settlement schedule.

This entire process can take seconds for card payments or several days for wire transfers. The complexity is why multiple parties charge fees. Every institution involved in moving your money takes a fee for its role in the chain.

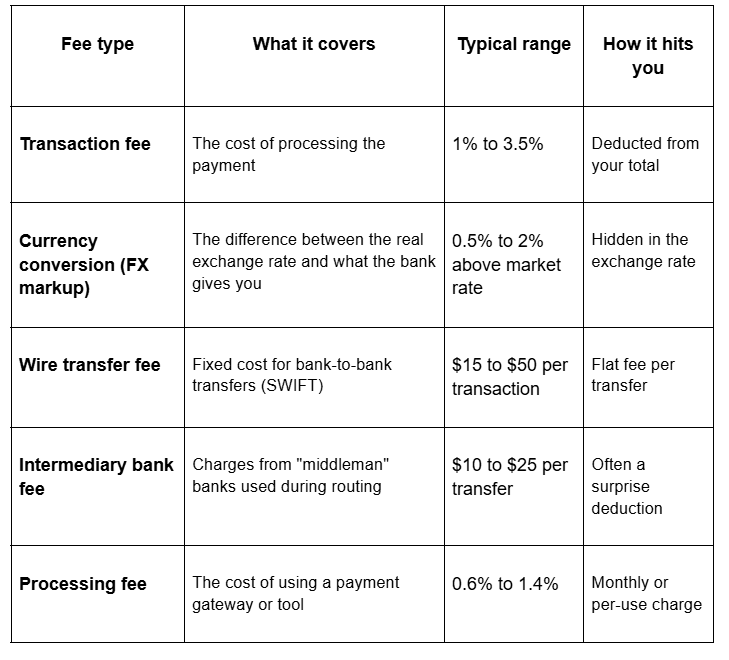

What are the Types of Cross-Border Payment Fees?

When you receive an international payment, you aren't just paying one fee. Several different charges are often stacked on top of each other. For example, a single $5,000 payment can be hit by a processing fee, a currency markup, and bank charges all at once.

Here is a breakdown of what these fees actually cost you:

Tip: Don't just look at the transaction fee. A provider might offer a "low" 1% fee, but then take an extra 2% through a poor exchange rate. Always check the total amount that actually hits your bank account.

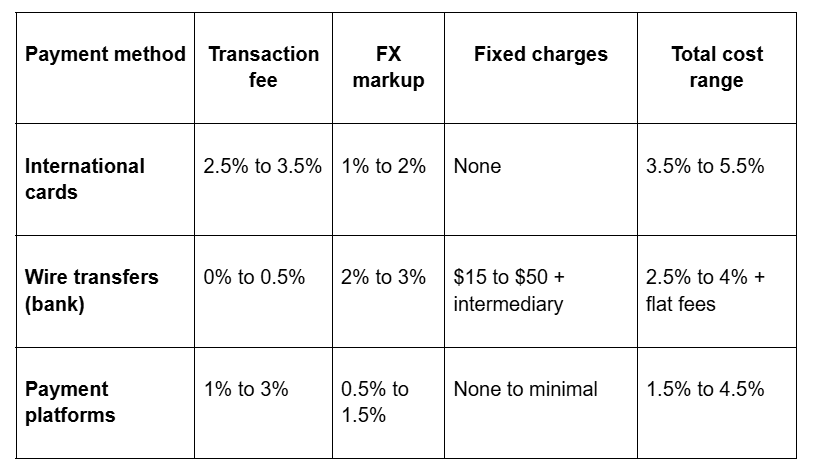

How Much do Cross-Border Payment Fees Actually Cost?

The countries you deal with also play a role. Converting USD to INR is usually cheaper than other currencies because it is a very common route.

The biggest factor, however, is your provider. Traditional banks often hide a 2% to 3% charge inside their exchange rates, while modern platforms stay much closer to the real market rate. A 2% difference might not seem like much on one invoice, but it can easily add up to lakhs of rupees in lost profit over a year.

How do Cross-Border Payment Fees Look in Real Life?

Sometimes it's easier to see the impact of fees by looking at actual numbers. Here are four common situations showing what a business invoices versus what they actually get to keep.

Freelancer receiving $3,000 from a US client via an international card

Your client pays $3,000 through an international card payment. The payment processor charges 3% transaction fee ($90) and applies a 1.5% FX markup on the USD to INR conversion ($45). You receive $2,865 in your account. You lost $135 (4.5%) on a single invoice.

Exporter receiving €20,000 from European buyer via wire transfer

Your buyer sends €20,000 through their bank. Their bank charges a €25 sending fee, your bank charges a $30 receiving fee, and an intermediary bank deducts $20. The exchange rate applied has a 1.2% markup (€240). After all deductions, you receive approximately €19,685 worth in INR. You lost €315 (1.6%) to various banks.

SaaS company with $8,000 monthly recurring revenue from global customers

Your payment platform charges 2.5% per transaction and includes a 0.8% FX markup in its bundled rate. On your $8,000 monthly recurring revenue, you pay $264 in combined fees. Over a year, that's $3,168 in costs. By switching to an all-in provider at 2%, you would only pay $1,920, saving you $1,248 annually.

Service exporter receiving a $50,000 project payment via a payment platform

Your client pays through a modern payment platform with transparent pricing. The platform fee is 1.5% ($750), and the FX markup is 0.6% ($300). You receive $48,950 after fees. Total cost: $1,050 or 2.1%. Compared to traditional bank wire, you save approximately $500 to $800 on this single transaction.

These examples show how fees compound quickly. The payment method, provider choice, and transaction size all impact what you actually keep. Small differences in fee percentages mean significant amounts on larger or more frequent transactions.

Note: Small, frequent payments lose more to fixed fees. Large, occasional payments lose more to percentage-based charges. Match your payment method to your transaction pattern for the lowest total cost.

What Factors Affect Your Cross-Border Payment Fees?

Not all international payments cost the same. A $1,000 card payment from the US will have a completely different fee structure than a $10,000 bank transfer from Europe. Understanding these variables helps you choose the right method for every invoice.

Here is what decides your final cost:

- Payment method: Cards are usually more expensive for large payments, while bank transfers are expensive for small ones because of fixed fees. Specialized payment platforms often provide a middle ground that works for both.

- Currency route: Popular routes (like USD to INR) are cheaper because there is more competition. If you are dealing with less common currencies, expect to pay a bit more.

- Provider markup: Every bank or platform adds a bit to the exchange rate. Banks often add 2% to 3%, while modern platforms stay much closer to the real market rate. This difference is small on one invoice, but it adds up quickly as you grow.

- Transaction size: Fixed fees (like a $25 bank charge) hurt small payments the most. If you receive $500, a $25 fee is 5% of your total. On a $10,000 payment, that same $25 is only 0.25%.

- Payment frequency: If your business is processing large amounts every month, you often have more room to negotiate. Many providers offer better rates for businesses that move $50,000 or $100,000 monthly.

By knowing these factors, you can stop guessing and start choosing the payment methods that keep the most money in your pocket.

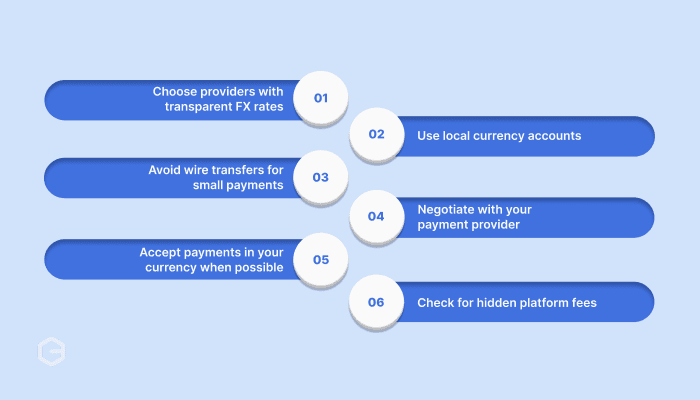

How to Reduce Cross-Border Payment Fees?

Cutting your costs doesn't require a complex strategy. Small changes in how you receive money and which providers you choose can save you thousands of dollars every year. Here is what actually works:

- Choose providers with transparent FX rates

Before you sign up, check if a provider shows you their exchange rate upfront. Compare it to the "mid-market rate" you see on Google. If the markup is more than 1%, you are likely overpaying.

- Use local currency accounts

This is one of the most effective ways to save. Having a USD account allows a US client to pay you as if they were sending money to a local neighbor. This removes the "cross-border" trigger and lets you control exactly when you want to convert that money into INR.

- Avoid wire transfers for small payments

If you are receiving less than $5,000, avoid bank wire transfers; the fixed fees will eat too much of your profit. For smaller, frequent amounts, use a payment platform. Save wire transfers for very large, one-time payments.

- Negotiate with your payment provider

Many payment providers have tiered pricing. If your monthly volume increases, for example, moving from $20,000 to $50,000, don't be afraid to ask for a lower rate. A 0.5% drop in fees can save you a significant amount over a year.

- Accept payments in your currency when possible

If you can invoice in INR and let the client handle conversion, you avoid FX markup. This works when you have pricing power. Not always possible, but worth considering for long-term clients.

- Check for hidden platform fees

Some providers advertise low transaction fees but add monthly fees, setup costs, or withdrawal charges. Calculate the total monthly cost, not just the per-transaction rate. A provider charging 2% with no other fees is often better than one charging 1.5% plus a $200 monthly fee unless you process high volumes consistently.

Accept Cross-Border Payments with Lower Fees Using PayGlocal

High fees shouldn't be the "tax" you pay for winning international clients. When banks hit you with poor exchange rates and hidden charges, you can easily lose 3% to 5% of your invoice before the money even touches your account.

PayGlocal is built specifically for Indian businesses and exporters who need a faster, fairer way to get paid. We replace the "black box" of traditional banking with a transparent system designed to protect your margins.

Here's how PayGlocal reduces your cross-border payment costs:

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, and CAD. Give your international clients local bank details so they can pay you the same way they pay their local service providers and suppliers.

- Global payment methods: Accept payments through 40+ local payment methods across 180+ countries. Give clients their preferred payment option and reduce failed transactions.

- Card payments: Process international cards with higher approval rates. PayGlocal's payment orchestration engine improves success rates, meaning fewer failed payments and less revenue lost.

- One platform: Manage all payments, track status, download compliance documents, and view detailed reports from one dashboard. No switching between multiple systems.

- Transparent pricing: Pay only when you transact. No setup fees, no monthly charges, no hidden costs. You see exactly what you're paying upfront.

PayGlocal helps you collect exactly what you invoiced. With lower fees and better rates, we make sure that your global growth actually shows up in your bottom line.

Final Thoughts

Cross-border payment fees are part of doing business globally, but they shouldn't be a mystery. The difference between losing 5% of your invoice and losing 2% is a significant amount of money that should be staying in your business.

The first step is knowing exactly what you're currently paying. Take a moment to add up your transaction fees, exchange rate markups, and fixed bank charges to find your "total cost." Once you see that number, you can compare it against more transparent providers to find a better deal.

The right payment partner does more than just move money; it simplifies your entire operation. You spend less time chasing compliance documents and less money on hidden fees. This allows you to stop worrying about the mechanics of getting paid and focus on what you do best: growing your business.

Ready to keep more of what you earn on international payments? Get started with PayGlocal today.