Your European client says they'll pay via SEPA. You nod, but you aren’t entirely sure what that means for your Indian bank account. You aren't alone. Most Indian exporters only discover SEPA once they scale into the European market.

Europe’s single payment area handles billions of Euro transactions every year. As India-EU trade hit nearly $136 billion in 2024-25, using SEPA has become the standard way for Indian businesses to collect revenue from Europe without the high fees of traditional wire transfers.

This guide explains what SEPA is, how the 41-country network works, and how you can use a virtual IBAN to collect Euro payments directly from India.

The full form of SEPA is Single Euro Payments Area. It is a European initiative that makes moving Euros across 41 different countries as easy and cheap as a local bank transfer.

Before SEPA, every European country had its own banking rules and high fees for cross-border moves. SEPA created a single highway for Euros. Now, a transfer from a client in Germany to a supplier in Spain follows the exact same rules as a transfer within Berlin.

For Indian businesses, SEPA is the local way to get paid in Europe. By using a platform that provides a European virtual IBAN, you can let your clients pay you via SEPA instead of making them send an expensive international wire.

Most payment systems you deal with today were built decades ago. SEPA is relatively recent, and knowing its timeline helps you see why European buyers trust it and prefer it over older transfer methods. Here are the key milestones:

Today, SEPA handles billions of transactions every year. It's no longer a new initiative. It's the standard infrastructure for moving euros across Europe.

Each SEPA payment type works differently, and picking the wrong one for your business model can slow down collections or create reconciliation headaches down the line. SEPA has the following main payment schemes:

Here's how each type works in practice.

This is the most common SEPA payment type. The sender (your buyer) initiates a transfer from their bank to your account. It typically settles within one business day.

SCT works well for invoice-based payments. Your European client receives an invoice, enters your IBAN, and sends the euros. It's a push payment: the buyer controls when the money is sent. For Indian exporters handling business invoices, this is the most familiar format.

SCT Inst is the faster version of SCT. Funds arrive in the recipient's account in under 10 seconds, and it works 24/7. It's especially useful for e-commerce, where buyers expect instant confirmation.

If your European customers pay through a checkout that supports instant SEPA transfers, the payment confirmation is nearly immediate. That speeds up delivery timelines and reduces the risk of payment failure.

Direct debit flips the flow. Instead of the buyer pushing funds to you, you pull funds from the buyer's account. This requires a signed mandate (authorization) from the buyer beforehand.

SDD comes in two variants: Core (for consumers) and B2B (for businesses). It's the standard approach for recurring payments in Europe, including subscriptions, memberships, and installment plans. If you run a SaaS product or subscription service with European customers, SDD is worth knowing about.

Note: SDD mandates have specific rules around notification timelines and chargebacks. The Core scheme gives buyers an eight-week refund window, while B2B does not.

Every day your payment sits in transit is a day your cash flow takes a hit. Traditional international wires are often slow and expensive. SEPA changes that by making your business look local to European buyers.

Here is why SEPA matters for Indian exporters:

These benefits add up when you're collecting payments regularly from Europe. Lower costs per transaction, faster access to funds, and a payment experience your buyers already trust.

Tip: Don't just ask for a wire transfer. Explicitly tell your European clients that they can pay via SEPA to your Euro IBAN. This small change in wording signals that you have a modern, cost-effective setup.

You've confirmed that your European buyer can pay through SEPA. But if you're not sure which countries it covers, you might send the wrong payment instructions and delay the whole transaction. SEPA currently includes 41 countries. Here's the full list, grouped by category.

If your customers are anywhere in the EU, the UK, or the handful of non-EU countries listed above, they can send you euros through SEPA.

It’s essential to note that not all of these countries use the euro as their official currency. Countries like Denmark, Sweden, and Poland have their own currencies. SEPA still applies to euro-denominated international transactions originating from banks in those countries. The currency of the transfer is what matters, not the country's official currency.

Tip: If you're building a checkout for European buyers, don't limit your SEPA-friendly payment options to eurozone countries only. Buyers in the UK, Switzerland, and Scandinavia can also send euros through SEPA.

Your European buyer is ready to pay, but they need the right details from you. Missing even one piece of information can bounce the transfer or delay it by days. Here's what your buyer needs from you, and what you should confirm on their end.

The best approach is to list your IBAN, BIC, and a clear payment reference on every invoice you send to a European client. That way, your buyer has everything they need in one place.

Tip: Create a standard payment details block for your European invoices. Include your IBAN, BIC, preferred currency (EUR), and a reference format. Reuse it across every invoice to avoid errors.

Indian businesses can't hold a SEPA account directly. You need a receiving setup that connects between the SEPA network in Europe and your bank account in India. Here's how to get that in place, step by step:

1. Choose a payment provider with European receiving capability: Your provider should give you access to a euro-denominated account (or virtual IBAN) within the SEPA zone. This is where your buyer's SEPA transfer lands before it's settled to you. Look for providers that support multi-currency accounts with EUR collection.

2. Get your IBAN or virtual IBAN: Once your provider sets up your receiving account, you'll get an IBAN to share with European buyers. This is what they'll enter in their bank to send the payment.

3. Add payment details to your invoices and checkout: List your IBAN, BIC (if required), and a clear payment reference on every invoice going to a European client. If you sell online, make sure your checkout page includes SEPA-friendly payment options.

4. Set up a settlement with your Indian bank: Confirm how and when your provider converts the euros to INR and settles funds to your Indian bank account. Check the conversion rate, settlement frequency, and any per-transaction charges.

5.Test with a small transaction first: Before routing large payments through your new setup, send a small test transfer from a European account. Verify the IBAN, confirm settlement timing, and check that the payment reference comes through correctly.

Once this setup is live, your European buyers can pay you through SEPA the same way they pay any local supplier. The experience on their end is fast and familiar. On your end, the euros convert and settle to your Indian account on a predictable schedule.

Tip: Ask your payment provider for a sample invoice template that includes all the SEPA-required fields. It saves time and reduces the chance of a buyer sending incomplete payment details.

Transfer fees affect your margins on every European transaction. If you're used to paying SWIFT intermediary charges, SEPA's cost structure will feel like a relief.

The main principle behind SEPA pricing is that a cross-border euro transfer within SEPA costs the same as a domestic one. For your European buyer, that typically means the transfer is either free or costs under EUR 1, depending on their bank and account type.

Here's how the costs break down across the payment chain:

Compared to SWIFT transfer fees, which can include sender charges, intermediary bank fees, and receiver charges that total $25-50 per transfer, SEPA is significantly cheaper for euro payments.

Note: Always check the total cost of receiving, not just the transfer fee. The real expense for Indian businesses is usually in the conversion and settlement step, not the SEPA transfer itself.

Most Indian businesses already collect from overseas clients through SWIFT transfers. When a European buyer mentions SEPA, it's natural to wonder which option is better and when to use each one.

So, is SEPA or SWIFT better for you? If a buyer in France wants to send you euros, SEPA is cheaper and faster. If a buyer in the US wants to send you USD, that goes through SWIFT. Both systems are suitable for different needs.

For Indian businesses, the main thing to consider is that when your European buyers have the option to pay via SEPA, they'll likely prefer it because it costs them less and settles faster. So, it’s essential to ensure your payment gateway can handle the funds on the receiving end, regardless of how they're sent.

You've done the work to win a European customer. The last thing you need is a slow or clunky payment process that stalls the money after the sale is made.

PayGlocal helps Indian businesses easily collect payments from customers worldwide, including Europe. Here's what you get:

From freelancers collecting from a client in Berlin to enterprises shipping products across the EU, PayGlocal is built to help Indian businesses collect globally with less friction and more confidence.

SEPA is how Europe moves euros. If your business sells to European customers, it directly affects how fast and affordably you get paid. Knowing how it works gives you an edge when setting up your payment collection.

Review your current payment setup and check if your provider can receive SEPA-originated payments. It’s also important to confirm that your invoices carry the right IBAN and payment details.

If you're ready to collect from European buyers and customers in 180+ countries, PayGlocal gives you the payment infrastructure to do it from one platform. European buyers get the payment experience they expect. You get faster settlements.

Get started with PayGlocal today before your next European invoice sits waiting longer than it should.

Europe’s single payment area handles billions of Euro transactions every year. As India-EU trade hit nearly $136 billion in 2024-25, using SEPA has become the standard way for Indian businesses to collect revenue from Europe without the high fees of traditional wire transfers.

This guide explains what SEPA is, how the 41-country network works, and how you can use a virtual IBAN to collect Euro payments directly from India.

Key takeaways

- Full form of SEPA: Single Euro Payments Area, a system that makes euro transfers across 41 European countries as simple as domestic payments.

- Three payment types: SEPA credit transfer, SEPA instant credit transfer, and SEPA direct debit, each serve a different use case for moving euros.

- 41 countries covered: 27 EU member states plus the UK, Iceland, Norway, Liechtenstein, Switzerland, Monaco, San Marino, Andorra, and countries applying for EU membership are all covered in SEPA.

- SEPA vs. SWIFT: SEPA is euro-only and works within Europe, while SWIFT handles multi-currency transfers globally.

- Global payments made easy: Platforms like PayGlocal help Indian businesses collect payments from 180+ countries, including Europe, in 33+ currencies.

What is SEPA?

The full form of SEPA is Single Euro Payments Area. It is a European initiative that makes moving Euros across 41 different countries as easy and cheap as a local bank transfer.

Before SEPA, every European country had its own banking rules and high fees for cross-border moves. SEPA created a single highway for Euros. Now, a transfer from a client in Germany to a supplier in Spain follows the exact same rules as a transfer within Berlin.

For Indian businesses, SEPA is the local way to get paid in Europe. By using a platform that provides a European virtual IBAN, you can let your clients pay you via SEPA instead of making them send an expensive international wire.

How did SEPA start and evolve over time?

Most payment systems you deal with today were built decades ago. SEPA is relatively recent, and knowing its timeline helps you see why European buyers trust it and prefer it over older transfer methods. Here are the key milestones:

- 2008: SEPA credit transfer (SCT) launched, giving banks across Europe a single format for euro transfers.

- 2009: SEPA direct debit (SDD) went live, allowing businesses to collect recurring euro payments across borders.

- 2014: The migration timeline arrived. Banks in eurozone countries were required to replace their old domestic transfer systems with SEPA formats.

- 2017: SEPA instant credit transfer (SCT Inst) launched, enabling real-time payments in under 10 seconds.

- 2025: Adoption of SCT Inst continued to expand, with more European banks and payment service providers joining the instant scheme.

Today, SEPA handles billions of transactions every year. It's no longer a new initiative. It's the standard infrastructure for moving euros across Europe.

What are the types of SEPA payments?

Each SEPA payment type works differently, and picking the wrong one for your business model can slow down collections or create reconciliation headaches down the line. SEPA has the following main payment schemes:

Here's how each type works in practice.

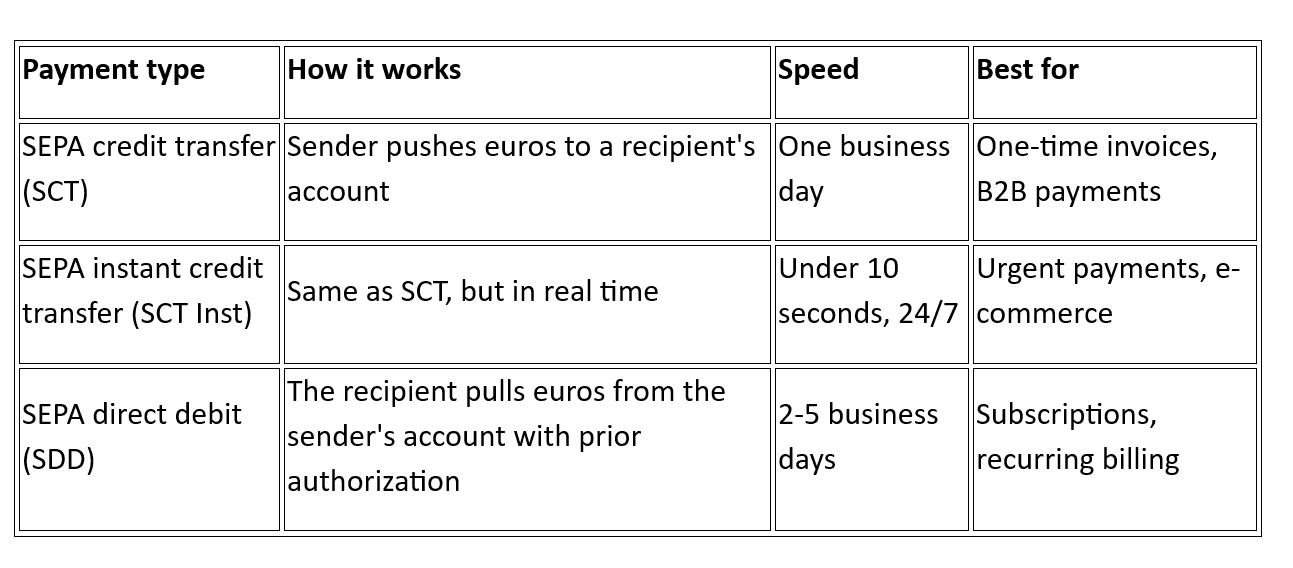

1. SEPA credit transfer (SCT)

This is the most common SEPA payment type. The sender (your buyer) initiates a transfer from their bank to your account. It typically settles within one business day.

SCT works well for invoice-based payments. Your European client receives an invoice, enters your IBAN, and sends the euros. It's a push payment: the buyer controls when the money is sent. For Indian exporters handling business invoices, this is the most familiar format.

2. SEPA instant credit transfer (SCT Inst)

SCT Inst is the faster version of SCT. Funds arrive in the recipient's account in under 10 seconds, and it works 24/7. It's especially useful for e-commerce, where buyers expect instant confirmation.

If your European customers pay through a checkout that supports instant SEPA transfers, the payment confirmation is nearly immediate. That speeds up delivery timelines and reduces the risk of payment failure.

3. SEPA direct debit (SDD)

Direct debit flips the flow. Instead of the buyer pushing funds to you, you pull funds from the buyer's account. This requires a signed mandate (authorization) from the buyer beforehand.

SDD comes in two variants: Core (for consumers) and B2B (for businesses). It's the standard approach for recurring payments in Europe, including subscriptions, memberships, and installment plans. If you run a SaaS product or subscription service with European customers, SDD is worth knowing about.

Note: SDD mandates have specific rules around notification timelines and chargebacks. The Core scheme gives buyers an eight-week refund window, while B2B does not.

Why SEPA payments matter for your business?

Every day your payment sits in transit is a day your cash flow takes a hit. Traditional international wires are often slow and expensive. SEPA changes that by making your business look local to European buyers.

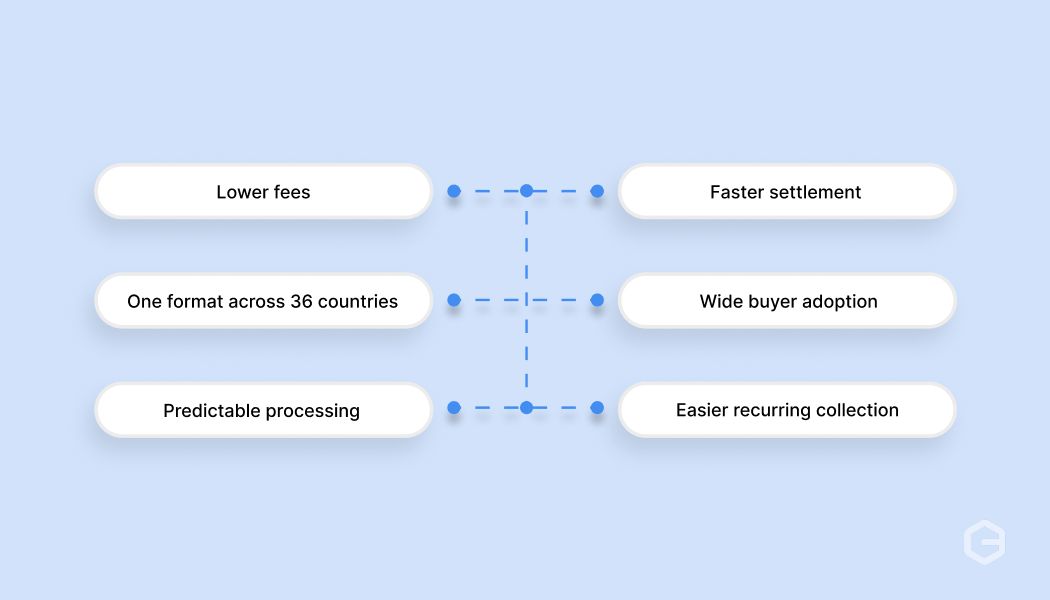

Here is why SEPA matters for Indian exporters:

- Lower fees: Because a cross-border SEPA transfer costs the same as a domestic one, your buyers are more likely to pay you on time. They don't have to worry about the $20–$30 fees associated with international SWIFT wires.

- Faster settlement: Standard transfers arrive within one business day. SEPA Instant settles in seconds. That's faster than most international transfers.

- One format across 41 countries: The payment format stays the same from Spain to Sweden. That makes reconciliation simpler on your end.

- Wide buyer adoption: SEPA is how most Europeans already pay. Offering SEPA-compatible payment options at checkout removes a barrier you might not even know exists.

- Predictable processing: SEPA follows standardized rules, which means fewer surprises around timing, fees, or rejected payments compared to SWIFT charges.

- Easier recurring collection: SEPA direct debit (SDD) makes it possible to set up automated, recurring euro collections from European customers who've authorized a mandate.

These benefits add up when you're collecting payments regularly from Europe. Lower costs per transaction, faster access to funds, and a payment experience your buyers already trust.

Tip: Don't just ask for a wire transfer. Explicitly tell your European clients that they can pay via SEPA to your Euro IBAN. This small change in wording signals that you have a modern, cost-effective setup.

Which countries are part of SEPA?

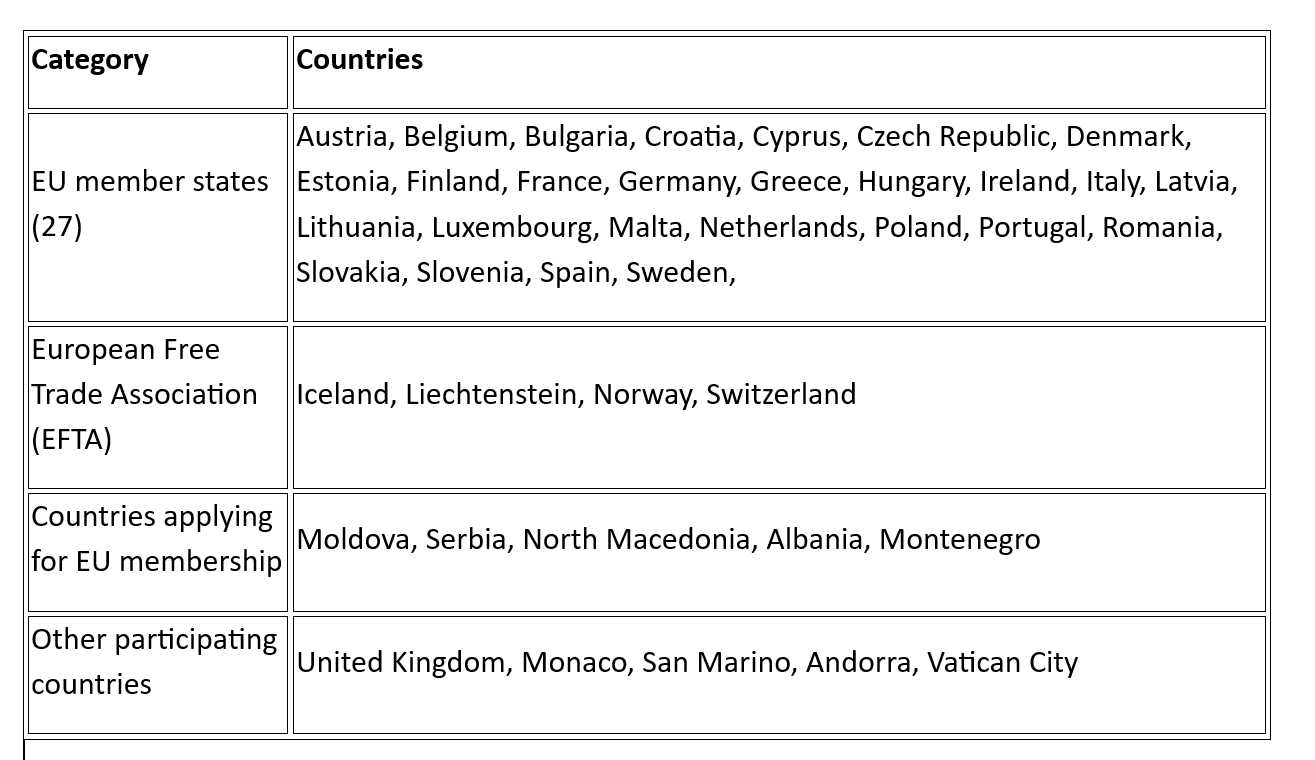

You've confirmed that your European buyer can pay through SEPA. But if you're not sure which countries it covers, you might send the wrong payment instructions and delay the whole transaction. SEPA currently includes 41 countries. Here's the full list, grouped by category.

If your customers are anywhere in the EU, the UK, or the handful of non-EU countries listed above, they can send you euros through SEPA.

It’s essential to note that not all of these countries use the euro as their official currency. Countries like Denmark, Sweden, and Poland have their own currencies. SEPA still applies to euro-denominated international transactions originating from banks in those countries. The currency of the transfer is what matters, not the country's official currency.

Tip: If you're building a checkout for European buyers, don't limit your SEPA-friendly payment options to eurozone countries only. Buyers in the UK, Switzerland, and Scandinavia can also send euros through SEPA.

What do you need for a SEPA payment?

Your European buyer is ready to pay, but they need the right details from you. Missing even one piece of information can bounce the transfer or delay it by days. Here's what your buyer needs from you, and what you should confirm on their end.

- International bank account number (IBAN): This is the primary identifier for SEPA. Your buyer enters your IBAN (or your payment provider's IBAN) to route the transfer. Every SEPA country uses IBANs, and the format varies by country, but the structure is standardized.

- Business identifier code (BIC): Also called a SWIFT code. Some banks still ask for a BIC alongside the IBAN, though it's no longer required for most SEPA transfers within the EU. It's good practice to share both on your export documentation.

- Payment amount in euros: SEPA only processes euro-denominated transfers. If your invoice is in another currency, your buyer will need to convert before sending, or use a different transfer method.

- Payment reference: A structured reference number that ties the payment to a specific invoice or order. This is optional but highly recommended. It makes bank reconciliation faster on your side.

- Buyer's bank must be SEPA-participating: The sender's bank needs to be part of the SEPA network. Nearly all banks in the 41 SEPA countries are, but it's worth confirming for first-time buyers.

The best approach is to list your IBAN, BIC, and a clear payment reference on every invoice you send to a European client. That way, your buyer has everything they need in one place.

Tip: Create a standard payment details block for your European invoices. Include your IBAN, BIC, preferred currency (EUR), and a reference format. Reuse it across every invoice to avoid errors.

How can you receive SEPA payments as an Indian business?

Indian businesses can't hold a SEPA account directly. You need a receiving setup that connects between the SEPA network in Europe and your bank account in India. Here's how to get that in place, step by step:

1. Choose a payment provider with European receiving capability: Your provider should give you access to a euro-denominated account (or virtual IBAN) within the SEPA zone. This is where your buyer's SEPA transfer lands before it's settled to you. Look for providers that support multi-currency accounts with EUR collection.

2. Get your IBAN or virtual IBAN: Once your provider sets up your receiving account, you'll get an IBAN to share with European buyers. This is what they'll enter in their bank to send the payment.

3. Add payment details to your invoices and checkout: List your IBAN, BIC (if required), and a clear payment reference on every invoice going to a European client. If you sell online, make sure your checkout page includes SEPA-friendly payment options.

4. Set up a settlement with your Indian bank: Confirm how and when your provider converts the euros to INR and settles funds to your Indian bank account. Check the conversion rate, settlement frequency, and any per-transaction charges.

5.Test with a small transaction first: Before routing large payments through your new setup, send a small test transfer from a European account. Verify the IBAN, confirm settlement timing, and check that the payment reference comes through correctly.

Once this setup is live, your European buyers can pay you through SEPA the same way they pay any local supplier. The experience on their end is fast and familiar. On your end, the euros convert and settle to your Indian account on a predictable schedule.

Tip: Ask your payment provider for a sample invoice template that includes all the SEPA-required fields. It saves time and reduces the chance of a buyer sending incomplete payment details.

How much do SEPA payments cost?

Transfer fees affect your margins on every European transaction. If you're used to paying SWIFT intermediary charges, SEPA's cost structure will feel like a relief.

The main principle behind SEPA pricing is that a cross-border euro transfer within SEPA costs the same as a domestic one. For your European buyer, that typically means the transfer is either free or costs under EUR 1, depending on their bank and account type.

Here's how the costs break down across the payment chain:

- Sender's side (your buyer): Most European banks include SEPA credit transfers as part of their standard account. Your buyer rarely pays a separate fee for sending a SEPA payment.

- SEPA instant transfers: Some banks charge a small premium for SCT Inst (usually EUR 0.50 to EUR 1). Others include it for free. It depends on the buyer's bank.

- Receiving side (your end): If you collect through a payment provider with a European receiving account, they may charge a processing or conversion fee when settling funds to your Indian bank. This is where you should compare providers carefully.

- Currency conversion: SEPA moves euros. When those euros are converted to INR for settlement, the exchange rate markup becomes your biggest cost variable. Some providers offer transparent pricing with no hidden markups. Others add a spread on top of the mid-market rate.

Compared to SWIFT transfer fees, which can include sender charges, intermediary bank fees, and receiver charges that total $25-50 per transfer, SEPA is significantly cheaper for euro payments.

Note: Always check the total cost of receiving, not just the transfer fee. The real expense for Indian businesses is usually in the conversion and settlement step, not the SEPA transfer itself.

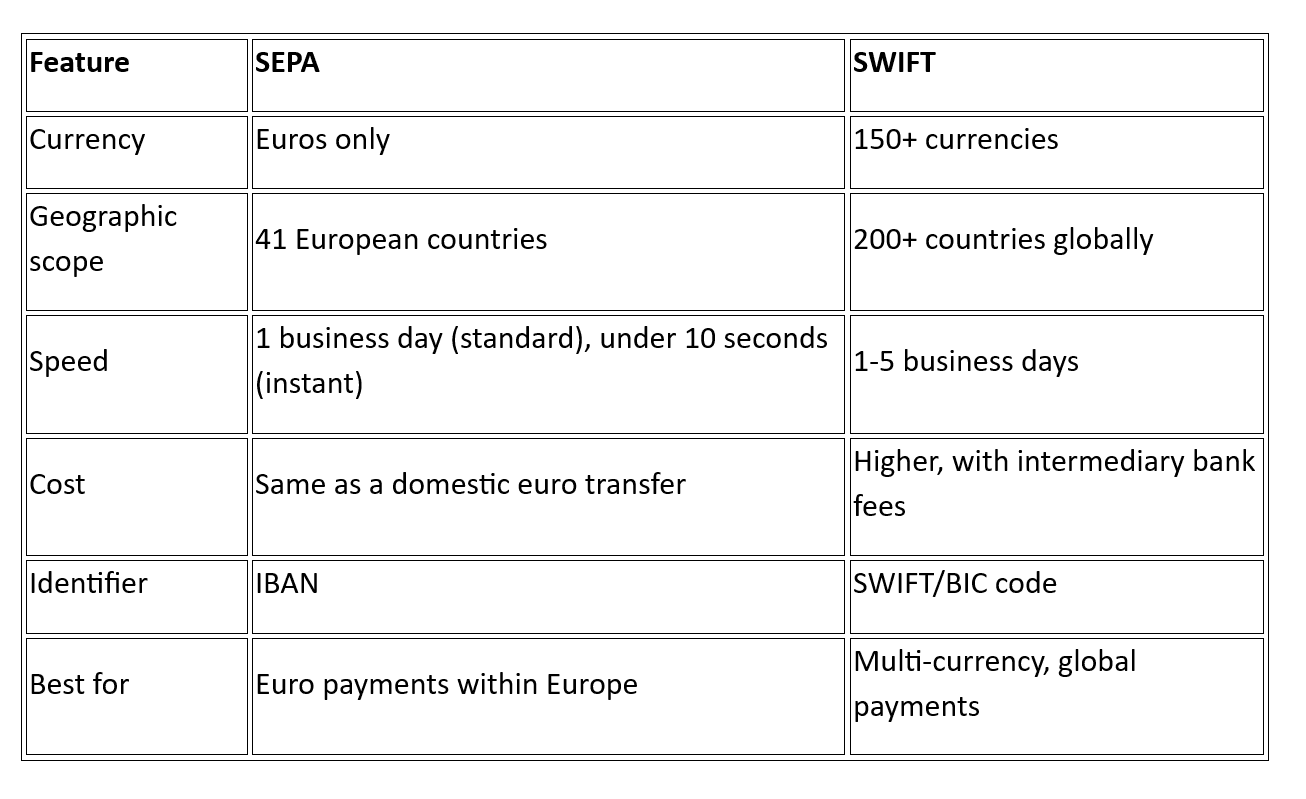

How is SEPA different from SWIFT?

Most Indian businesses already collect from overseas clients through SWIFT transfers. When a European buyer mentions SEPA, it's natural to wonder which option is better and when to use each one.

So, is SEPA or SWIFT better for you? If a buyer in France wants to send you euros, SEPA is cheaper and faster. If a buyer in the US wants to send you USD, that goes through SWIFT. Both systems are suitable for different needs.

For Indian businesses, the main thing to consider is that when your European buyers have the option to pay via SEPA, they'll likely prefer it because it costs them less and settles faster. So, it’s essential to ensure your payment gateway can handle the funds on the receiving end, regardless of how they're sent.

Get paid by European buyers faster with PayGlocal

You've done the work to win a European customer. The last thing you need is a slow or clunky payment process that stalls the money after the sale is made.

PayGlocal helps Indian businesses easily collect payments from customers worldwide, including Europe. Here's what you get:

- Multi-currency accounts: Your European buyers pay in EUR, USD, GBP, CAD, AUD, or any of 33+ currencies from 180+ countries, all collected into one account you control.

- Global payment methods: More completed purchases at checkout, thanks to 40+ local payment options that your buyers already know and trust.

- Card payments: Fewer international card transactions get declined, which means more of your customers finish their purchase without running into a failed payment.

- Dynamic checkout: A checkout experience that feels local to your global customers, built with the right payment options and flow for their region.

- One platform: Full visibility into your international payments, settlements, and reports from a single dashboard instead of separate tools for each currency or region.

From freelancers collecting from a client in Berlin to enterprises shipping products across the EU, PayGlocal is built to help Indian businesses collect globally with less friction and more confidence.

Final thoughts

SEPA is how Europe moves euros. If your business sells to European customers, it directly affects how fast and affordably you get paid. Knowing how it works gives you an edge when setting up your payment collection.

Review your current payment setup and check if your provider can receive SEPA-originated payments. It’s also important to confirm that your invoices carry the right IBAN and payment details.

If you're ready to collect from European buyers and customers in 180+ countries, PayGlocal gives you the payment infrastructure to do it from one platform. European buyers get the payment experience they expect. You get faster settlements.

Get started with PayGlocal today before your next European invoice sits waiting longer than it should.