The Cash Reserve Ratio (CRR) is crucial for anyone navigating the complexities of monetary policy and banking regulations in India. As of mid-2025, India’s banking system is operating with a liquidity surplus of over ₹2.4 trillion, reflecting efforts to stimulate credit flow and maintain financial stability. This surplus environment highlights how regulatory tools, such as the CRR, directly impact the money supply, lending activity, and interest rates.

CRR, a regulatory tool, requires a specified percentage of its total deposits to be held as reserves in cash with the central bank. While this ensures liquidity and financial stability, it also affects the money supply and lending capacity of banks, often leaving businesses and individuals to grapple with higher interest rates or limited credit availability during economic tightening.

In this blog, we’ll explore how CRR is calculated, its purpose and role in controlling inflation and stimulating growth, and how it compares to the Statutory Liquidity Ratio (SLR), another critical reserve requirement that influences asset allocation and liquidity management in banks.

CRR refers to a specified percentage of total deposits that commercial banks are required to hold as reserves with the central bank. For example, if a bank’s total deposits are ₹10,00,000 and the CRR is 8%, it must keep aside ₹80,000 as reserves.

This reserve acts as a safeguard to control the money supply in the economy and regulate inflation. Banks cannot use the funds set aside as CRR to lend to individuals or businesses or invest them elsewhere. Additionally, banks do not earn any interest on the amount held as CRR.

The Cash Reserve Ratio (CRR) serves several key purposes and objectives within the Indian banking and economic system:

These objectives align with how central banks globally use CRR to balance inflation control, economic growth, financial stability, and liquidity management.

The Cash Reserve Ratio plays a significant role in controlling inflation by regulating the money supply in the economy. When the central bank raises the CRR, banks must hold a larger portion of their deposits as reserves, reducing the funds available for lending.

This curtails spending and investment, helping ease inflationary pressures. Conversely, lowering the CRR allows banks to lend more, boosting spending and investment, which can lead to higher inflation if not carefully managed.

For example, when the CRR is increased, banks have less money to lend and may raise interest rates to compensate for the reduced liquidity. Higher interest rates increase loan costs for consumers, including higher EMIs for personal, car, and home loans, reducing borrowing and demand.

The calculation of CRR determines the exact percentage of deposits banks must set aside. Changes in this percentage directly impact the amount of money available for circulation in the economy, influencing inflation control.

If you're interested in how this relates to currency movements and global trade, you can also read more about foreign exchange for better clarity.

The Cash Reserve Ratio (CRR) is calculated as a percentage of a bank's Net Demand and Time Liabilities (NDTL). NDTL includes all types of deposits a bank holds — demand deposits (like current and savings accounts) and time deposits (like fixed or recurring deposits).

Example:

Let’s assume a bank has ₹50 crore in deposits — ₹20 crore in savings accounts, ₹10 crore in fixed deposits, and ₹20 crore in other liabilities. The CRR percentage set by the central bank is 4%.

Formula for CRR calculation:

CRR = (Cash reserves required to be held with the central bank) / (Net Demand and Time Liabilities)

In this case, CRR = ₹50 crore × 4%

So, the bank will need to keep ₹2 crore as cash reserves.

The central bank sets the CRR to control the amount of money circulating in the economy, helping manage inflation and maintain economic stability. The CRR can be adjusted as per the financial scenario, allowing the central bank to either tighten or loosen liquidity in the market.

Net Demand and Time Liabilities (NDTL): Represents the total value of deposits held by the bank, minus any inter-bank deposits (i.e., deposits that the bank holds with other banks).

The calculation of CRR is key to grasping its impact on the banking system. However, failing to comply with these requirements can lead to penalties for banks.

Failure to comply with Cash Reserve Ratio (CRR) regulations can lead to several consequences for banks:

While CRR impacts the money supply by controlling how much banks can lend, SLR ensures that banks maintain a buffer of liquid assets for emergencies. Knowing the differences and compliance requirements of both ratios will help you avoid penalties and operate smoothly in the financial system.

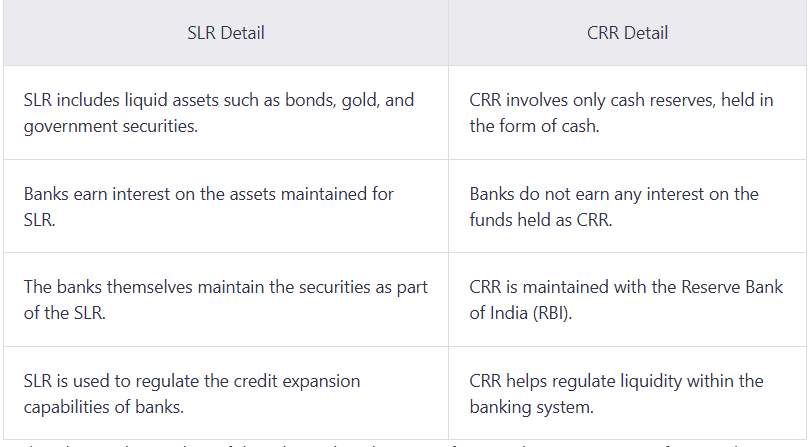

The Statutory Liquidity Ratio (SLR) is the percentage of a commercial bank's Net Demand and Time Liabilities (NDTL) that it must maintain in the form of liquid assets, such as cash, gold, or government-approved securities. Unlike CRR, which is maintained with the central bank, SLR assets are held by the bank itself.

Here's a table outlining the key differences between SLR and CRR. Understanding these distinctions is essential for businesses and financial institutions, as each plays a unique role in managing bank operations and maintaining overall stability.

With a clear understanding of the roles and implications of CRR and SLR, we can now focus on how these policies shape the financial environment for businesses and their operations, particularly when dealing with cross-border payments.

Managing liquidity is crucial for businesses, particularly when engaging in cross-border transactions and managing diverse payment cycles. A sudden change in customer demand, foreign exchange rates, or regulatory compliance can lock up capital and slow down operations.

That’s where PayGlocal can make a difference by helping businesses streamline cash flow, reduce settlement time, and maintain flexibility across markets. Here’s how PayGlocal empowers enterprises to manage liquidity with ease:

1. Dynamic Checkout: PayGlocal’s Dynamic Checkout automatically adapts the payment experience based on the customer’s location and device, ensuring faster conversions and lower cart abandonment. For businesses, this means quicker payments, improved cash inflow, and better liquidity visibility.

2. Card Payments: Accept international and domestic card payments seamlessly with faster settlement timelines. PayGlocal’s support for major card networks ensures a broader customer base and quicker access to funds, helping businesses reduce receivable cycles.

3. Global Payment Methods: From UPI and net banking in India to wallets and bank transfers worldwide, PayGlocal supports 30+ payment methods. This flexibility enables businesses to receive payments quickly from anywhere, ensuring capital isn’t tied up due to payment friction.

4. Recurring Payments: With PayGlocal, businesses can set up automated recurring payments for subscriptions or billing cycles. This predictable cash inflow improves liquidity forecasting and reduces dependency on manual payment follow-ups.

5. Multi-Currency Account: Manage collections in 33+ currencies using a single platform. There is no need to open separate bank accounts across countries. Businesses can hold, convert, and settle funds as needed, minimizing foreign exchange risk and unlocking liquidity across borders.

6. One Unified Platform: PayGlocal provides a single, intuitive platform for handling payments, compliance, reporting, and reconciliation. By consolidating financial operations, businesses gain real-time visibility into cash flow and reduce delays caused by scattered tools or systems.

7. Sanction Screening: All transactions are screened for compliance with global sanctions and AML regulations. This ensures secure processing while avoiding delays or fund freezes that could strain liquidity during critical operations.

With PayGlocal, businesses can accept payments globally while maintaining control of their local cash position — improving operational efficiency, reducing credit risks, and unlocking capital when it matters most.

The Cash Reserve Ratio (CRR) plays a crucial role in managing liquidity within the economy, impacting the lending capacity of banks. For businesses, especially those involved in cross-border transactions, effective liquidity management ensures funds are available for international payments and investments.

Since CRR influences the amount of money banks can lend, it can directly affect the ease and cost of handling international transactions. When dealing with cross-border payments, you need a reliable, efficient solution that can handle multi-currency transactions and comply with global standards. This is where PayGlocal, an online payment aggregator, can make a significant difference for your business. Sign up with PayGlocal now!

CRR, a regulatory tool, requires a specified percentage of its total deposits to be held as reserves in cash with the central bank. While this ensures liquidity and financial stability, it also affects the money supply and lending capacity of banks, often leaving businesses and individuals to grapple with higher interest rates or limited credit availability during economic tightening.

In this blog, we’ll explore how CRR is calculated, its purpose and role in controlling inflation and stimulating growth, and how it compares to the Statutory Liquidity Ratio (SLR), another critical reserve requirement that influences asset allocation and liquidity management in banks.

Key Takeaways

- CRR (Cash Reserve Ratio) is the percentage of a bank’s total deposits that must be held in cash with the Reserve Bank of India (RBI). This reserve cannot be used for lending or investment and earns no interest.

- CRR is a monetary policy tool to control inflation, regulate liquidity, and influence interest rates. A higher CRR reduces the money available for lending, while a lower CRR increases liquidity in the economy.

- CRR is calculated as a percentage of a bank’s Net Demand and Time Liabilities (NDTL). Banks must comply with the prescribed ratio, or they may face monetary penalties, interest charges, or operational restrictions.

- CRR differs from SLR (Statutory Liquidity Ratio), which involves liquid assets such as gold and government securities. Unlike CRR, banks earn interest on SLR holdings and maintain them within the bank.

What is the Cash Reserve Ratio (CRR)?

CRR refers to a specified percentage of total deposits that commercial banks are required to hold as reserves with the central bank. For example, if a bank’s total deposits are ₹10,00,000 and the CRR is 8%, it must keep aside ₹80,000 as reserves.

This reserve acts as a safeguard to control the money supply in the economy and regulate inflation. Banks cannot use the funds set aside as CRR to lend to individuals or businesses or invest them elsewhere. Additionally, banks do not earn any interest on the amount held as CRR.

Why is CRR important for the economy?

The Cash Reserve Ratio (CRR) serves several key purposes and objectives within the Indian banking and economic system:

- Controlling inflation: If inflation is rising and the central bank wants to reduce the amount of money circulating in the economy, it may increase the CRR. By doing so, banks must keep a larger portion of their deposits with the central bank, reducing lending capacity and slowing down inflation.

- Stimulating economic growth: During slowdowns, the central bank may decrease the CRR. Lower CRR means banks keep less money as reserves and can lend more to businesses and consumers, encouraging spending and investment.

- Managing interest rates: By adjusting the CRR, the central bank influences the interest rates in the economy. Higher CRR leads to higher lending rates; lower CRR can reduce rates and boost borrowing.

- Managing liquidity: CRR ensures banks maintain sufficient reserves to meet obligations and avoid liquidity crises.

These objectives align with how central banks globally use CRR to balance inflation control, economic growth, financial stability, and liquidity management.

How does CRR help in controlling inflation?

The Cash Reserve Ratio plays a significant role in controlling inflation by regulating the money supply in the economy. When the central bank raises the CRR, banks must hold a larger portion of their deposits as reserves, reducing the funds available for lending.

This curtails spending and investment, helping ease inflationary pressures. Conversely, lowering the CRR allows banks to lend more, boosting spending and investment, which can lead to higher inflation if not carefully managed.

For example, when the CRR is increased, banks have less money to lend and may raise interest rates to compensate for the reduced liquidity. Higher interest rates increase loan costs for consumers, including higher EMIs for personal, car, and home loans, reducing borrowing and demand.

The calculation of CRR determines the exact percentage of deposits banks must set aside. Changes in this percentage directly impact the amount of money available for circulation in the economy, influencing inflation control.

If you're interested in how this relates to currency movements and global trade, you can also read more about foreign exchange for better clarity.

How is the Cash Reserve Ratio (CRR) calculated?

The Cash Reserve Ratio (CRR) is calculated as a percentage of a bank's Net Demand and Time Liabilities (NDTL). NDTL includes all types of deposits a bank holds — demand deposits (like current and savings accounts) and time deposits (like fixed or recurring deposits).

Example:

Let’s assume a bank has ₹50 crore in deposits — ₹20 crore in savings accounts, ₹10 crore in fixed deposits, and ₹20 crore in other liabilities. The CRR percentage set by the central bank is 4%.

Formula for CRR calculation:

CRR = (Cash reserves required to be held with the central bank) / (Net Demand and Time Liabilities)

In this case, CRR = ₹50 crore × 4%

So, the bank will need to keep ₹2 crore as cash reserves.

The central bank sets the CRR to control the amount of money circulating in the economy, helping manage inflation and maintain economic stability. The CRR can be adjusted as per the financial scenario, allowing the central bank to either tighten or loosen liquidity in the market.

Net Demand and Time Liabilities (NDTL): Represents the total value of deposits held by the bank, minus any inter-bank deposits (i.e., deposits that the bank holds with other banks).

The calculation of CRR is key to grasping its impact on the banking system. However, failing to comply with these requirements can lead to penalties for banks.

What are the penalties for not following CRR rules?

Failure to comply with Cash Reserve Ratio (CRR) regulations can lead to several consequences for banks:

- Monetary fines: Failure to comply with reserve requirements may result in regulatory penalties as outlined in applicable guidelines. These fines are typically based on the shortfall amount and can be either a percentage of the deficit or a fixed sum.

- Interest charges: Banks may be required to pay interest on the deficiency at a penalty rate set by the RBI. This interest is calculated for the period during which the bank fails to maintain the required CRR.

- Operational restrictions: Repeated non-compliance with CRR norms may result in restrictions on a bank’s operations, such as limiting its lending or investment activities until the deficiency is rectified.

- Regulatory actions: Persistent CRR shortfalls can lead to stricter regulatory actions, including additional oversight, restrictions on dividend distributions, and more intensive supervisory measures until the issue is resolved.

- Legal consequences: In cases of severe and continuous non-compliance, regulatory bodies may initiate legal action, potentially resulting in legal proceedings or more severe financial penalties.

While CRR impacts the money supply by controlling how much banks can lend, SLR ensures that banks maintain a buffer of liquid assets for emergencies. Knowing the differences and compliance requirements of both ratios will help you avoid penalties and operate smoothly in the financial system.

What is SLR?

The Statutory Liquidity Ratio (SLR) is the percentage of a commercial bank's Net Demand and Time Liabilities (NDTL) that it must maintain in the form of liquid assets, such as cash, gold, or government-approved securities. Unlike CRR, which is maintained with the central bank, SLR assets are held by the bank itself.

What is the difference between CRR and SLR?

Here's a table outlining the key differences between SLR and CRR. Understanding these distinctions is essential for businesses and financial institutions, as each plays a unique role in managing bank operations and maintaining overall stability.

With a clear understanding of the roles and implications of CRR and SLR, we can now focus on how these policies shape the financial environment for businesses and their operations, particularly when dealing with cross-border payments.

How can PayGlocal help businesses manage their liquidity?

Managing liquidity is crucial for businesses, particularly when engaging in cross-border transactions and managing diverse payment cycles. A sudden change in customer demand, foreign exchange rates, or regulatory compliance can lock up capital and slow down operations.

That’s where PayGlocal can make a difference by helping businesses streamline cash flow, reduce settlement time, and maintain flexibility across markets. Here’s how PayGlocal empowers enterprises to manage liquidity with ease:

1. Dynamic Checkout: PayGlocal’s Dynamic Checkout automatically adapts the payment experience based on the customer’s location and device, ensuring faster conversions and lower cart abandonment. For businesses, this means quicker payments, improved cash inflow, and better liquidity visibility.

2. Card Payments: Accept international and domestic card payments seamlessly with faster settlement timelines. PayGlocal’s support for major card networks ensures a broader customer base and quicker access to funds, helping businesses reduce receivable cycles.

3. Global Payment Methods: From UPI and net banking in India to wallets and bank transfers worldwide, PayGlocal supports 30+ payment methods. This flexibility enables businesses to receive payments quickly from anywhere, ensuring capital isn’t tied up due to payment friction.

4. Recurring Payments: With PayGlocal, businesses can set up automated recurring payments for subscriptions or billing cycles. This predictable cash inflow improves liquidity forecasting and reduces dependency on manual payment follow-ups.

5. Multi-Currency Account: Manage collections in 33+ currencies using a single platform. There is no need to open separate bank accounts across countries. Businesses can hold, convert, and settle funds as needed, minimizing foreign exchange risk and unlocking liquidity across borders.

6. One Unified Platform: PayGlocal provides a single, intuitive platform for handling payments, compliance, reporting, and reconciliation. By consolidating financial operations, businesses gain real-time visibility into cash flow and reduce delays caused by scattered tools or systems.

7. Sanction Screening: All transactions are screened for compliance with global sanctions and AML regulations. This ensures secure processing while avoiding delays or fund freezes that could strain liquidity during critical operations.

With PayGlocal, businesses can accept payments globally while maintaining control of their local cash position — improving operational efficiency, reducing credit risks, and unlocking capital when it matters most.

Conclusion

The Cash Reserve Ratio (CRR) plays a crucial role in managing liquidity within the economy, impacting the lending capacity of banks. For businesses, especially those involved in cross-border transactions, effective liquidity management ensures funds are available for international payments and investments.

Since CRR influences the amount of money banks can lend, it can directly affect the ease and cost of handling international transactions. When dealing with cross-border payments, you need a reliable, efficient solution that can handle multi-currency transactions and comply with global standards. This is where PayGlocal, an online payment aggregator, can make a significant difference for your business. Sign up with PayGlocal now!