Secured online transactions are important for individuals and businesses alike. Whether you're a freelancer, small business owner, or an exporter handling international payments, you need to be confident that your financial information is protected during every purchase.

Card-not-present fraud is expected to reach a staggering $28.1 billion globally by 2026.

One of the most effective ways to prevent unauthorized transactions is through CVV and CVC codes—small but powerful security features on your credit card. These 3 or 4 digit codes play a vital role in protecting you from fraud.

CVV (Card Verification Value) and CVC (Card Validation Code) are unique security features that protect cardholders during online and card-not-present transactions. These codes provide an additional layer of verification, confirming that the card's rightful owner makes the payment.

Although terminology may vary by card network, the function remains the same: they act as a security checkpoint during transactions.

For example:

These codes are necessary in preventing fraud, especially for transactions where the card is not physically present, such as online shopping, phone orders, or mail transactions.

CVV and CVC codes restrict entry to the cardholder, providing vital protection for digital transactions and defending against unauthorized purchases.

CVV and CVC codes are typically found on the back of your credit or debit card, near the magnetic stripe. However, depending on the card network, the location may vary slightly.

Though these codes are easy to find, they must remain confidential. Avoid sharing or storing your CVV/CVC in unsecured places, as they are vital for safeguarding your financial transactions.

Knowing where your CVV/CVC code is located helps streamline online transactions, ensuring you're ready to complete your purchases securely.

Although the CVV, CVC, CID, CVN, and CSC refer to the same security feature across various credit cards, it is used under different terminologies depending on the card network. These terms represent the same concept, an additional layer of security for card-not-present transactions.

Despite these varying terms, their function remains consistent: they are a security checkpoint during transactions.

Let’s understand how these codes work during the payment process.

The CVV (Card Verification Value) and CVC (Card Validation Code) are essential security features for online and card-not-present transactions to prevent fraud. They add a layer of verification, confirming the cardholder's identity and ensuring transaction safety.

Here's how they work in the payment process.

PayGlocal uses the Alternate ID (ALT ID) solution for guest checkout, replacing the card number with a unique payment token to keep sensitive data secure.

Also Read: Stay Ahead of Fraud: Understanding Liability Shift in Card Payments

These verification processes protect individual cardholders and also play a role in larger payment processing systems, particularly for businesses managing multiple payment methods and providers.

In a payment orchestration system, merchants integrate multiple payment providers to improve transaction approval rates while minimizing fraud risks. CVV/CVC validation ensures that legitimate transactions are processed, reducing chargebacks and declined payments.

For businesses looking to enhance transaction success and secure payments, PayGlocal offers payment orchestration services with integrated CVV/CVC verification and multiple payment methods to improve both fraud protection and conversion rates.

While payment systems provide institutional protection, cardholders also have responsibility for safeguarding their security codes.

Also Read: The True Cost of Fraud | Why Businesses Need Fraud Prevention

In payment orchestration, businesses integrate multiple payment providers to optimize transaction approval rates while minimizing fraud risks. CVV and CVC codes play a key role in ensuring that transactions are secure and legitimate.

When processing payments, CVV/CVC codes are verified as part of the transaction process to confirm the cardholder's identity.

By doing so, businesses can:

Using CVV and CVC codes not only secures customer payments but also boosts the efficiency and reliability of the payment system.

Now that we've covered how CVV/CVC codes benefit businesses, let's look at practical steps to protect your codes from misuse and fraud.

To protect your CVC (Card Verification Code) and prevent unauthorized transactions, follow these steps.

CVV and CVC codes are vital for securing online transactions, especially in card-not-present scenarios. These codes add a crucial layer of protection, ensuring that only the legitimate cardholder can complete a transaction.

If you are a freelancer managing payments or a small business owner processing orders, understanding and protecting your CVV/CVC codes is essential to prevent fraud and safeguard your financial information.

At PayGlocal, we prioritize transaction security with strong fraud prevention measures like CVV/CVC verification, encryption, and tokenization. Our payment solutions let you process payments confidently, ensuring your financial data is protected.

Start securing your payments today with PayGlocal's reliable and secure payment solutions. Get Started Today!

Card-not-present fraud is expected to reach a staggering $28.1 billion globally by 2026.

One of the most effective ways to prevent unauthorized transactions is through CVV and CVC codes—small but powerful security features on your credit card. These 3 or 4 digit codes play a vital role in protecting you from fraud.

What are CVC and CVV Codes?

CVV (Card Verification Value) and CVC (Card Validation Code) are unique security features that protect cardholders during online and card-not-present transactions. These codes provide an additional layer of verification, confirming that the card's rightful owner makes the payment.

Although terminology may vary by card network, the function remains the same: they act as a security checkpoint during transactions.

For example:

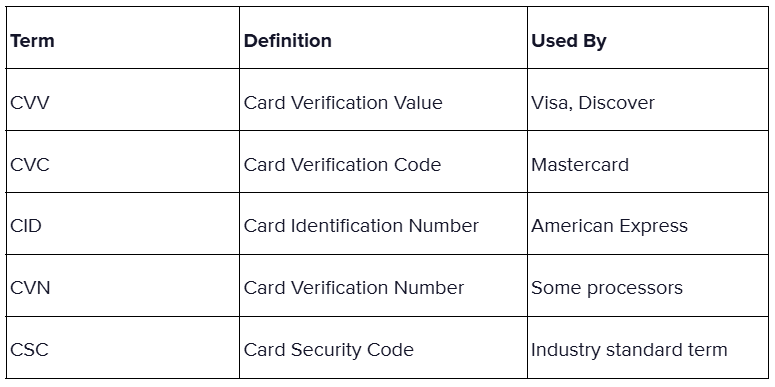

- CVV: Used by Visa and Discover cards, typically a three-digit number located on the back of the card.

- CVC: Used by Mastercard cards, also a three-digit number found on the back of the card.

- CID (Card Identification Number): Used by American Express, which has either a three- or four-digit number typically printed on the front of the card.

These codes are necessary in preventing fraud, especially for transactions where the card is not physically present, such as online shopping, phone orders, or mail transactions.

CVV and CVC codes restrict entry to the cardholder, providing vital protection for digital transactions and defending against unauthorized purchases.

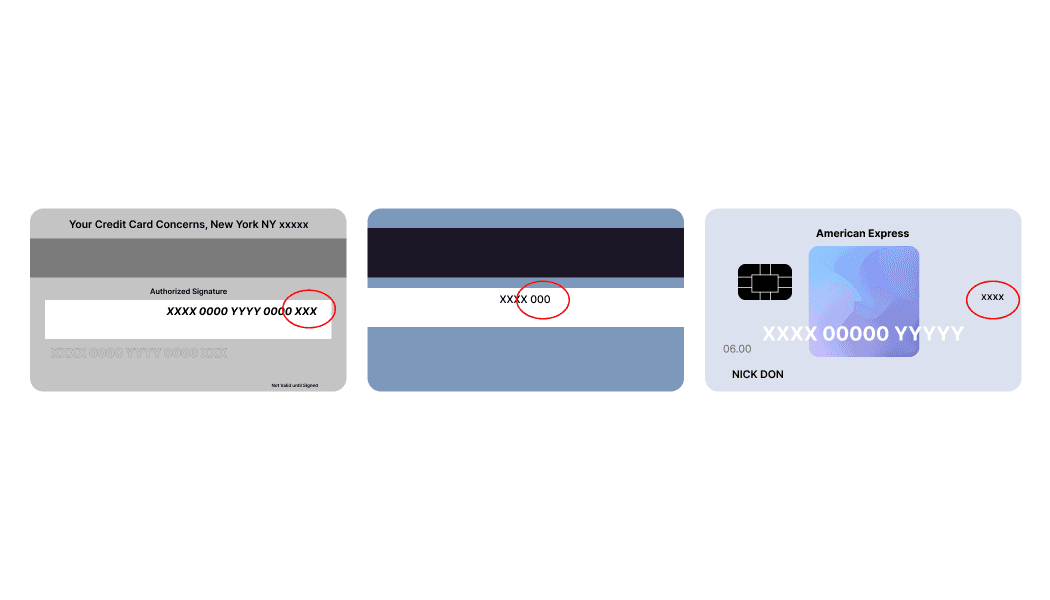

Where are the CVC/CVV Codes Located on the Credit Card?

CVV and CVC codes are typically found on the back of your credit or debit card, near the magnetic stripe. However, depending on the card network, the location may vary slightly.

- Visa, MasterCard, and Discover: These cards have a three-digit CVV/CVC code printed on the back, following the card number. It’s usually located on the right side, after the signature panel.

- American Express: Unlike other cards, American Express cards display the CVV (or CID) as a four-digit code. This code can be found either on the front of the card, above the card number, or on the back, depending on the card's design.

Though these codes are easy to find, they must remain confidential. Avoid sharing or storing your CVV/CVC in unsecured places, as they are vital for safeguarding your financial transactions.

Knowing where your CVV/CVC code is located helps streamline online transactions, ensuring you're ready to complete your purchases securely.

Different Terminology for the Card Security Code

Although the CVV, CVC, CID, CVN, and CSC refer to the same security feature across various credit cards, it is used under different terminologies depending on the card network. These terms represent the same concept, an additional layer of security for card-not-present transactions.

Despite these varying terms, their function remains consistent: they are a security checkpoint during transactions.

Let’s understand how these codes work during the payment process.

How Do the CVV and CVC Codes Work in Transactions?

The CVV (Card Verification Value) and CVC (Card Validation Code) are essential security features for online and card-not-present transactions to prevent fraud. They add a layer of verification, confirming the cardholder's identity and ensuring transaction safety.

Here's how they work in the payment process.

- Functionality: When shopping online, provide the card number, expiration date, and CVV/CVC. This info goes to the payment gateway, which verifies it with the card issuer. The CVV/CVC is compared with securely stored data from the issuing bank, not shared with merchants, ensuring privacy and security.

- Verification: The card network (Visa, MasterCard, American Express) verifies the CVV/CVC against its records. If it matches, the transaction proceeds; if not, it is declined to prevent unauthorized purchases.

- Integration with Payment Gateways: Payment gateways like PayGlocal enhance security with 3D Secure authentication, requiring cardholders to verify their identity. Transactions failing CVV/CVC verification are blocked, reducing fraud risk.

PayGlocal uses the Alternate ID (ALT ID) solution for guest checkout, replacing the card number with a unique payment token to keep sensitive data secure.

Also Read: Stay Ahead of Fraud: Understanding Liability Shift in Card Payments

These verification processes protect individual cardholders and also play a role in larger payment processing systems, particularly for businesses managing multiple payment methods and providers.

Role of CVV or CVC Codes in Payment Orchestration

In a payment orchestration system, merchants integrate multiple payment providers to improve transaction approval rates while minimizing fraud risks. CVV/CVC validation ensures that legitimate transactions are processed, reducing chargebacks and declined payments.

Key Benefits of CVV/CVC Validation in Payment Orchestration

- Improved Fraud Detection: Helps block unauthorized transactions by verifying the cardholder’s authenticity.

- Higher Authorization Rates: Some banks automatically decline transactions without CVV/CVC verification, resulting in lower approval rates.

- PCI DSS Compliance: Ensures that sensitive customer data is securely handled in accordance with industry standards.

- Seamless Integration with Alternative Payment Methods: Provides security when processing digital wallets, BNPL (Buy Now, Pay Later), and other payment methods.

- Better Checkout Experience: Automates security checks, reducing friction for legitimate transactions and improving the overall user experience.

For businesses looking to enhance transaction success and secure payments, PayGlocal offers payment orchestration services with integrated CVV/CVC verification and multiple payment methods to improve both fraud protection and conversion rates.

While payment systems provide institutional protection, cardholders also have responsibility for safeguarding their security codes.

Also Read: The True Cost of Fraud | Why Businesses Need Fraud Prevention

Role of CVV or CVC Codes in Payment Orchestration

In payment orchestration, businesses integrate multiple payment providers to optimize transaction approval rates while minimizing fraud risks. CVV and CVC codes play a key role in ensuring that transactions are secure and legitimate.

When processing payments, CVV/CVC codes are verified as part of the transaction process to confirm the cardholder's identity.

By doing so, businesses can:

- Improve Fraud Detection: Verifying CVV/CVC codes helps block unauthorized transactions, preventing fraud and costly chargebacks.

- Enhance Authorization Rates: Many banks decline transactions lacking a valid CVV/CVC, reducing the chances of declined payments due to incorrect or missing information.

- Ensure PCI DSS Compliance: CVV/CVC codes are crucial for maintaining PCI DSS compliance, ensuring sensitive data is handled securely and not stored on merchants’ servers.

- Integrate with Alternative Payment Methods: CVV/CVC codes also secure digital wallets, BNPL (Buy Now, Pay Later), and other alternative payment options.

- Streamline Checkout: Automating CVV/CVC verification reduces friction in the checkout process, leading to faster transactions and improved user experience.

Using CVV and CVC codes not only secures customer payments but also boosts the efficiency and reliability of the payment system.

Now that we've covered how CVV/CVC codes benefit businesses, let's look at practical steps to protect your codes from misuse and fraud.

How to Protect Your CVC from Fraud and Misuse: Pro Tips

To protect your CVC (Card Verification Code) and prevent unauthorized transactions, follow these steps.

- Contact Your Bank Immediately: If you suspect your CVV is compromised, inform your bank or card issuer as soon as possible. Some banks allow you to block your card directly via their mobile app.

- Monitor Your Account: Check your bank account for any suspicious activity or unauthorized charges. Stay vigilant for unusual messages or calls, especially those involving unexpected bills.

- Keep Your Information Secure: Never share your CVV with anyone, even if they claim to be from your bank. Avoid saving card details on untrusted websites, and regularly check your bank statements for unauthorized transactions.

- Use Secure Websites: When shopping online, ensure the website is secure (look for "HTTPS" in the URL) and avoid sharing sensitive information over unsecured networks.

Conclusion

CVV and CVC codes are vital for securing online transactions, especially in card-not-present scenarios. These codes add a crucial layer of protection, ensuring that only the legitimate cardholder can complete a transaction.

If you are a freelancer managing payments or a small business owner processing orders, understanding and protecting your CVV/CVC codes is essential to prevent fraud and safeguard your financial information.

At PayGlocal, we prioritize transaction security with strong fraud prevention measures like CVV/CVC verification, encryption, and tokenization. Our payment solutions let you process payments confidently, ensuring your financial data is protected.

Start securing your payments today with PayGlocal's reliable and secure payment solutions. Get Started Today!