Key Takeaways:

- UPI transactions remain free for individuals: Bank-to-bank transfers via UPI continue to be cost-free for customers. Only select transactions using Prepaid Payment Instruments (PPIs) exceeding ₹2,000 incur interchange fees, which merchants, not the users, pay.

- Merchants incur fees for PPI-linked UPI payments: A 1.1% interchange fee is charged to merchants on PPI-based UPI transactions exceeding ₹2,000. However, regular UPI transactions through bank accounts remain unaffected by this fee.

- UPI transaction limits vary depending on the use and the bank. The standard UPI daily limit is ₹1 lakh, but it can be increased to ₹5 lakh for specific sectors, such as education and healthcare. Each bank sets its daily cap for users, which affects planning for high-value transactions.

- PayGlocal simplifies domestic and cross-border UPI payments, offering features such as UPI Intent Flow, Dynamic QR, and multi-currency support. This enables businesses to manage high-volume, compliant, and efficient payment workflows across borders.

Unified Payments Interface (UPI) is India’s most widely used digital payment system, developed by the National Payments Corporation of India (NPCI). It enables instant, secure bank-to-bank transfers using a Virtual Payment Address (VPA), UPI ID, or mobile number, eliminating the need for cash, cards, or cheques.

UPI’s rapid adoption stems from its simplicity, zero-cost usage for personal payments, and ability to complete transactions in real-time. From splitting restaurant bills to making high-value purchases at retail outlets, UPI has become the default mode of payment for millions of Indians. While primarily designed for domestic use, it is now evolving to support a broader range of merchant and cross-border applications.

This blog provides comprehensive information on UPI payment surcharges, including the current fee structure for merchants, the role of Prepaid Payment Instruments (PPIs), daily transaction limits, recent updates from NPCI, and how platforms like PayGlocal simplify UPI integrations for businesses.

What are UPI transaction charges?

UPI transactions, including peer-to-merchant (P2M) and peer-to-peer (P2P) transfers between bank accounts, are free for customers.

However, a 1.1% interchange fee is applied to transactions above ₹2,000 made through Prepaid Payment Instruments (PPIs). The fee is exclusively levied on the merchant, not the customer.

For example, if a transaction of ₹2,000 is made through a PPI-linked UPI account, a fee of ₹22 will be charged to the merchant. Regular UPI transactions between bank accounts don't incur any charges, and the 1.1% fee only applies to specific PPI-related payments.

- PPI: Paytm, SODEXO vouchers, Amazon Pay, Freecharge wallet, etc.

- An interchange fee is the fee a merchant pays the payment service provider when using a prepaid wallet.

How do UPI transaction limits impact merchant payments?

According to NPCI, the maximum UPI transaction limit is ₹1 lakh daily. However, for specific categories such as Capital Markets, Collections, Insurance, and Foreign Inward Remittances, the transaction limit can go up to ₹2 lakh.

Additionally, educational institutions, healthcare facilities, and tax payments have a higher daily limit of ₹5 lakh.

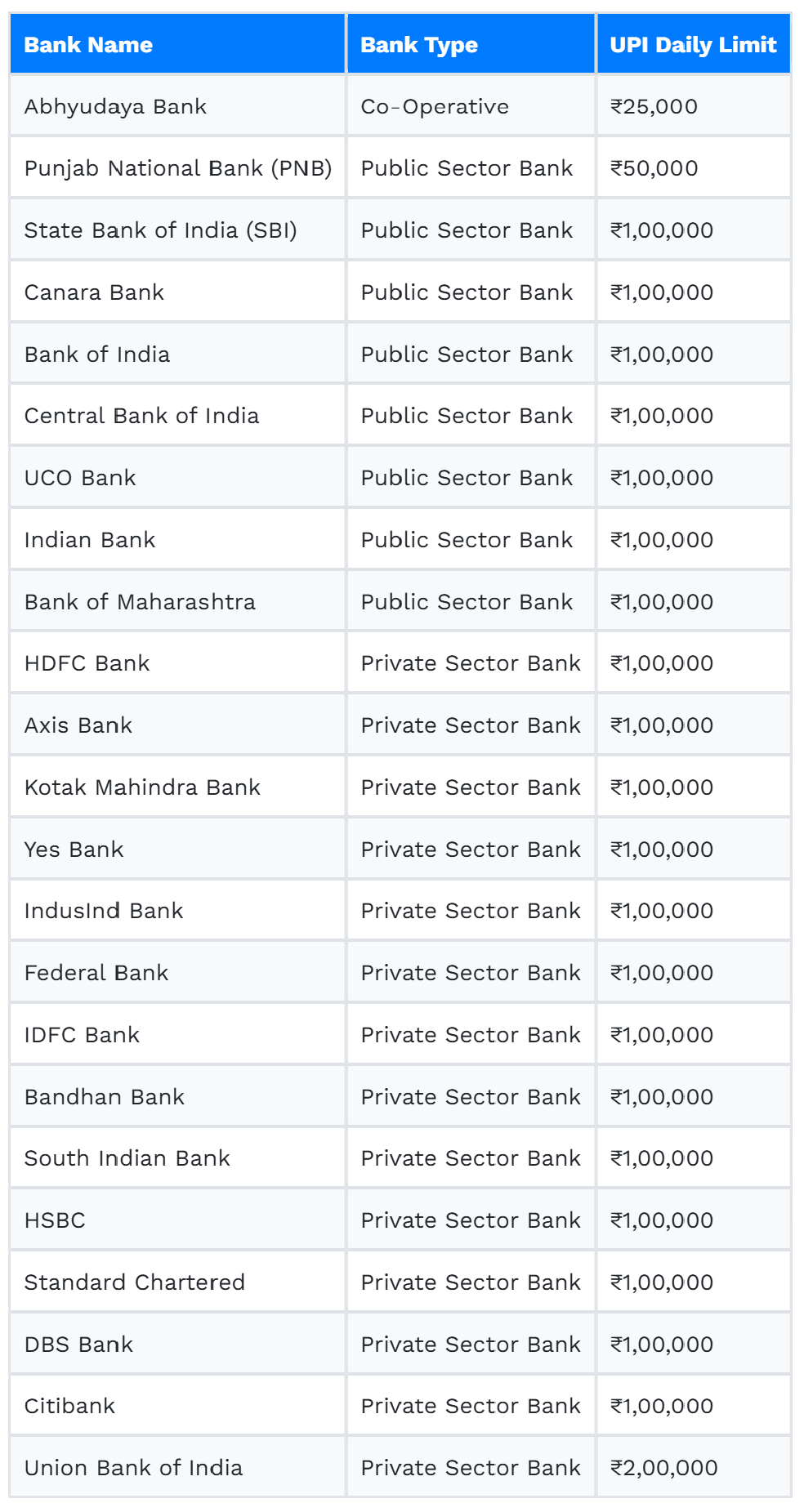

The bank-to-bank transfer limit ranges from ₹25,000 to ₹1 lakh, depending on the bank account linked with your UPI. These limits are set either on a daily or monthly basis, depending on the specific bank.

What happens if you exceed the daily transaction limit? In that case, you must wait for the 24-hour cycle to reset before attempting the transfer.

The actual limit for your UPI transactions will also depend on your bank and the type of account linked to your UPI. For most users, the daily transaction limit for apps like GPay and PhonePe is ₹1 lakh unless the above exceptions apply. For higher-value transactions, PPI is a flexible alternative.

How do Prepaid Payment Instruments (PPIs) benefit businesses?

Prepaid Payment Instruments (PPIs) are highly relevant for businesses, particularly in managing payments and enhancing the customer experience. Here's how PPIs can benefit businesses:

1. Faster payments: PPIs, such as digital wallets (Paytm, PhonePe, etc.), enable businesses to receive payments instantly, reducing the delays associated with traditional payment methods like checks or bank transfers.

2. Convenience: PPIs provide customers with a quick and easy way to make payments, enhancing their overall experience. This convenience can lead to more frequent purchases, especially for businesses with an online or mobile presence.

3. Lower transaction costs: For small-scale businesses, PPIs offer lower transaction fees compared (interchange fee 1.1%) to credit card payments (1.5% - 3.5%) or traditional payment methods, helping businesses save on payment processing costs.

4. Improved cash flow: With instant payment processing and no need to wait for bank transfers to clear, businesses can have more predictable cash flow, thus manage operations more efficiently.

5. Wider reach: PPIs allow businesses to tap into a growing customer base that prefers using digital wallets for everyday transactions. By accepting payments through PPIs, companies can cater to this segment.

6. Cross-border transactions: PPIs are helpful for international businesses and exporters. However, it's important to note that only full-KYC PPIs issued by banks with the required license are allowed for cross-border transactions. These transactions are also subject to the existing FEMA regulations and restrictions.

As UPI remains one of India's most widely used payment methods, PayGlocal enhances the payment experience by offering various UPI checkout options, including UPI Intent Flow, UPI Collect Flow, and UPI Dynamic QR Code. These options enable businesses to accept UPI payments from Indian customers seamlessly.

Additionally, PayGlocal's multi-currency support facilitates cross-border transactions in various currencies, providing businesses with a global solution. This combination of UPI and cross-border payment capabilities enables seamless integration with international markets and payment processes for companies worldwide. Talk to our Experts!

How do UPI charges affect merchants?

Merchants incur UPI transaction charges, also known as interchange fees, when accepting payments via Prepaid Payment Instruments (PPIs), such as digital wallets.

These fees cover the processing, acceptance, and authorization of transactions and can vary based on the transaction type and merchant category, ranging from 0.5% to 1.1% of the transaction amount.

When customers recharge their wallets with amounts exceeding ₹2,000, a wallet-loading service charge of 0.15% applies. The PPI issuers (such as Paytm or PhonePe) pay this charge to the banks to facilitate the wallet loading process.

While merchants may not be directly responsible for this fee, it plays a role in the overall payment ecosystem, affecting the cost of accepting digital payments.

For small merchants, UPI interchange fees generally don’t apply. You'll incur interchange fees only on transactions over ₹2,000 if you're a medium-sized merchant. For larger transactions, you can either absorb the higher fees yourself or pass them on to your customers by increasing product prices to cover the costs.

These measures ensure that merchants and banks are fairly divided among the costs associated with maintaining the UPI infrastructure and enabling smooth transactions. Let's see how these changes continue to shape the digital payments landscape in India.

UPI guidelines 2025: Latest updates from NPCI

NPCI can enhance UPI transaction limits for P2M payments. It provides insights into recent regulatory changes affecting UPI transaction limits, which are crucial for merchants.

- Increased transaction limits: The NPCI can revise transaction limits for UPI payments for Person-to-Merchant (P2M) transactions. This change accommodates user needs and facilitates higher-value transactions.

- Potential benefits for merchants: With higher transaction limits, merchants can experience smoother processing of larger payments, particularly in sectors such as education, healthcare, and retail. Thus, transaction failures may be reduced, improving the overall payment experience for both merchants and customers.

- Safeguards and compliance: NPCI, in consultation with banks and other stakeholders, will implement appropriate safeguards to manage risks associated with increased transaction limits. Merchants should stay informed about these to ensure compliance and adapt to any changes in transaction processing.

You must also consider leveraging these new changes and enhancing payment systems to meet international payment needs.

How does PayGlocal enhance the merchant payment experience with UPI integration?

PayGlocal enhances merchant payment experiences by integrating India's Unified Payments Interface (UPI) into its platforms. It offers several additional benefits that make it easier and more efficient for businesses to accept UPI payments.

1. Seamless integration: PayGlocal makes it simple for businesses to integrate UPI payment methods into their websites or apps. Without a third-party provider, companies would have to build their own UPI integration from scratch, which can be a complex and time-consuming process.

2. Multi-currency support: While UPI is great for domestic transactions, PayGlocal supports multiple currencies for businesses dealing with international customers. This enables enterprises to utilize UPI not only for domestic payments in India but also for cross-border transactions in other currencies, making it a truly global solution.

3. Security and compliance: PayGlocal ensures that all UPI transactions comply with legal regulations and payment security standards with Samruddhi X screening. This helps businesses avoid potential risks related to fraud or legal issues.

4. Streamlined payment management: PayGlocal offers businesses a unified dashboard that tracks all their payments, simplifying transaction management. This saves businesses time and helps them keep better records than managing payments individually through multiple UPI systems.

While UPI is a great tool, PayGlocal simplifies the whole payment process for businesses, making it easier, more secure, and more efficient to manage UPI payments.

Conclusion

UPI remains a highly cost-effective payment solution for personal transactions, providing instant and seamless bank-to-bank transfers. However, merchants must account for the interchange fees applied to PPI transactions over ₹2,000. As the digital payment landscape evolves, merchants and individuals must stay updated on the latest UPI guidelines to ensure smooth and compliant transactions.

With PayGlocal, merchants can simplify cross-border payments, manage multiple currencies, and easily ensure compliance with regulations. Get started with PayGlocal today to streamline digital payment processes and expand your business globally.