The card market of India has shown rapid growth in recent years. According to studies, the total number of credit cards almost doubled in 5 years, from 5.53 crore in December 2021 to 10.80 crore by December 2024.

In this growing card payments market, you get several options beyond regular credit cards. Whether you choose a credit card, a debit card, or a charge card, each card type serves a distinct purpose and operates differently.

In this guide, we break down exactly what charge cards are, how they work, their benefits and limitations, so that you can decide if it’s the right payment solution for your needs. Let’s get started!

A charge card is a payment card that requires you to pay the full outstanding balance each month. Unlike credit cards, charge cards typically don't have preset spending limits and don't allow you to carry balances forward.

The key difference is the payment flexibility. With a credit card, you can pay a minimum amount and carry the rest as debt with interest charges. Charge cards require complete payment by the due date every month.

For example, if you spend ₹50,000 on your charge card in January, you must pay the entire ₹50,000 by the due date, not just a minimum amount. This requirement makes charge cards suitable for people and businesses with predictable cash flow and strong payment discipline.

Here's how charge cards function from purchase to payment:

Charge cards offer distinct characteristics that separate them from other payment methods. These features appeal to specific user types who value spending flexibility over payment flexibility.

Most charge cards don't set fixed spending limits like traditional credit cards. Your spending power depends on your payment history, income, and financial profile. This flexibility helps with large business purchases or unexpected expenses that might exceed normal credit card limits.

Every billing cycle requires a complete balance payment. You cannot carry forward any amount to the next month like credit cards allow. This feature forces disciplined spending and prevents debt accumulation, but requires consistent cash flow management.

Charge cards typically have stricter approval requirements than traditional credit cards. Issuers focus on income stability, credit history, and payment reliability. This selectivity means fewer people qualify, but approved users generally receive better terms and benefits.

Most charge cards include enhanced rewards, travel benefits, concierge services, and business perks. These often include purchase protection, extended warranties, and exclusive access to events or services that justify the higher annual fees.

Charge cards provide several advantages for users who can manage the payment requirements and qualify for approval:

Charge cards also present several challenges that make them unsuitable for many users and business situations:

Here’s a complete comparison of charge cards and credit cards, so that you can choose the right option for your needs:

For businesses needing flexible spending without preset limits, charge cards work well. However, companies requiring payment flexibility during seasonal cash flow variations might find credit cards more suitable for their operations.

Charge cards work best for specific user profiles who can maximize the benefits while managing the payment requirements effectively.

Lawyers, doctors, consultants, and other professionals with stable, substantial income can handle full monthly payments without cash flow issues. Their predictable earnings make charge card requirements manageable while accessing premium benefits.

Companies with steady cash flow and expense management needs benefit from flexible spending limits and detailed expense tracking. Service businesses, consultancies, and established companies often fit this profile well.

Premium travel benefits, concierge services, and travel insurance add significant value for people who travel regularly. Higher spending on travel and entertainment helps maximize rewards and justify annual fees.

People seeking to improve their credit scores through responsible usage benefit from charge cards. However, it is also worth considering the discipline required for full monthly payments and the potential consequences of missed payments.

Getting approved for a charge card requires meeting specific criteria and following a structured application process:

Traditional charge cards solve some payment challenges but create others. Strict approval requirements, high fees, and inflexible payment terms often limit business growth and global expansion opportunities.

PayGlocal helps businesses send and receive payments efficiently without the limitations of traditional payment methods.

Whether you're a freelancer invoicing international clients or a growing company managing global transactions, PayGlocal provides all the payment flexibility you need, along with better control and transparency. Here are some of the ways the platform can help you:

PayGlocal provides modern businesses with reliable, transparent payment collection that adapts to your growth and global reach.

Charge cards offer unique benefits for businesses and individuals who can manage full monthly payments and qualify for strict approval requirements. They provide spending flexibility and premium benefits but require financial discipline and substantial income to use effectively.

For modern businesses operating globally, traditional payment methods often create more obstacles than solutions. The approval process, payment restrictions, and limited global reach can slow business growth and complicate international operations. PayGlocal offers an efficient and easy platform to manage all your global payments.

Ready to simplify your global payment collection? Get started with PayGlocal today and experience transparent, reliable international payment processing that grows with your business.

In this growing card payments market, you get several options beyond regular credit cards. Whether you choose a credit card, a debit card, or a charge card, each card type serves a distinct purpose and operates differently.

In this guide, we break down exactly what charge cards are, how they work, their benefits and limitations, so that you can decide if it’s the right payment solution for your needs. Let’s get started!

Key Takeaways:

- Full payment requirement: Charge cards require complete balance payment each billing cycle, unlike credit cards.

- Business advantages: Ideal for companies needing higher spending flexibility with disciplined payment habits.

- Credit building potential: Regular usage and timely payments can positively impact credit scores.

- Global payment solution: Modern businesses can use PayGlocal for more flexible, scalable global payment collection.

What is a charge card?

A charge card is a payment card that requires you to pay the full outstanding balance each month. Unlike credit cards, charge cards typically don't have preset spending limits and don't allow you to carry balances forward.

The key difference is the payment flexibility. With a credit card, you can pay a minimum amount and carry the rest as debt with interest charges. Charge cards require complete payment by the due date every month.

For example, if you spend ₹50,000 on your charge card in January, you must pay the entire ₹50,000 by the due date, not just a minimum amount. This requirement makes charge cards suitable for people and businesses with predictable cash flow and strong payment discipline.

How does a charge card work?

Here's how charge cards function from purchase to payment:

- Purchase authorization: The card issuer approves transactions based on your spending pattern and payment history.

- No preset limit validation: System checks spending patterns rather than fixed credit limits.

- Monthly statement generation: All transactions get compiled into a single monthly bill.

- Full payment requirement: The entire balance must be paid by the due date.

- Late payment consequences: Penalties and potential account suspension occur for missed payments.

What do you get with a charge card?

Charge cards offer distinct characteristics that separate them from other payment methods. These features appeal to specific user types who value spending flexibility over payment flexibility.

No preset spending limit

Most charge cards don't set fixed spending limits like traditional credit cards. Your spending power depends on your payment history, income, and financial profile. This flexibility helps with large business purchases or unexpected expenses that might exceed normal credit card limits.

Mandatory full payment

Every billing cycle requires a complete balance payment. You cannot carry forward any amount to the next month like credit cards allow. This feature forces disciplined spending and prevents debt accumulation, but requires consistent cash flow management.

Higher acceptance standards

Charge cards typically have stricter approval requirements than traditional credit cards. Issuers focus on income stability, credit history, and payment reliability. This selectivity means fewer people qualify, but approved users generally receive better terms and benefits.

Premium benefits

Most charge cards include enhanced rewards, travel benefits, concierge services, and business perks. These often include purchase protection, extended warranties, and exclusive access to events or services that justify the higher annual fees.

What are the benefits of charge cards?

Charge cards provide several advantages for users who can manage the payment requirements and qualify for approval:

- Flexible spending power: No fixed credit limits enable large purchases when business opportunities arise.

- Credit score benefits: Responsible usage and timely payments can improve credit ratings over time.

- Premium rewards: Higher reward rates and exclusive benefits compared to basic credit cards.

- Business expense management: Detailed statements help track business spending effectively for tax and accounting purposes.

- Purchase protection: Enhanced security features and fraud protection beyond standard credit cards.

- No interest charges: Since balances must be paid in full, no interest accumulates on purchases.

What are the limitations of charge cards?

Charge cards also present several challenges that make them unsuitable for many users and business situations:

- Strict payment requirements: Late payments result in hefty penalties, potential account closure, and credit score damage.

- High annual fees: Charge cards usually carry yearly fees ranging from ₹4,500 to ₹66,000 or more for premium variants that may not justify the benefits for all users.

- Limited payment flexibility: No option to carry balances during temporary cash flow challenges or seasonal business variations.

- Approval difficulty: Stringent income and credit requirements exclude many potential applicants from qualification.

- Acceptance limitations: Some merchants don't accept charge cards, especially smaller vendors or specific online platforms.

- Cash flow pressure: Monthly full payments can create stress during business growth phases or economic uncertainty.

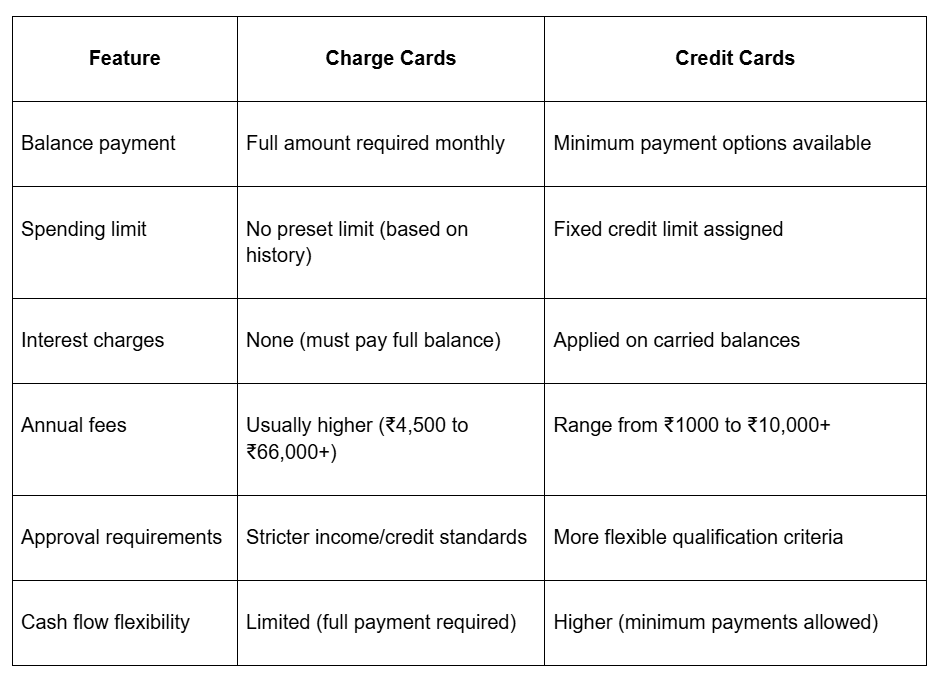

How do charge cards differ from credit cards?

Here’s a complete comparison of charge cards and credit cards, so that you can choose the right option for your needs:

For businesses needing flexible spending without preset limits, charge cards work well. However, companies requiring payment flexibility during seasonal cash flow variations might find credit cards more suitable for their operations.

Who should consider charge cards?

Charge cards work best for specific user profiles who can maximize the benefits while managing the payment requirements effectively.

High-income professionals

Lawyers, doctors, consultants, and other professionals with stable, substantial income can handle full monthly payments without cash flow issues. Their predictable earnings make charge card requirements manageable while accessing premium benefits.

Business owners with predictable revenue

Companies with steady cash flow and expense management needs benefit from flexible spending limits and detailed expense tracking. Service businesses, consultancies, and established companies often fit this profile well.

Frequent business travelers

Premium travel benefits, concierge services, and travel insurance add significant value for people who travel regularly. Higher spending on travel and entertainment helps maximize rewards and justify annual fees.

Credit-building focused individuals

People seeking to improve their credit scores through responsible usage benefit from charge cards. However, it is also worth considering the discipline required for full monthly payments and the potential consequences of missed payments.

How to apply for charge cards?

Getting approved for a charge card requires meeting specific criteria and following a structured application process:

- Check eligibility requirements: Most issuers require minimum annual income thresholds, typically ₹15 lakhs or higher for premium cards.

- Gather required documents: Income proof, bank statements, identity verification, and business registration if applying for business cards.

- Review credit score: Most issuers require credit scores above 750 for approval, with higher scores improving chances for premium variants.

- Compare available options: Research different charge cards, their benefits, fees, and terms to find the best match for your needs.

- Submit application: Complete online or branch applications with all required documentation and accurate information.

- Wait for approval: Processing typically takes 7-14 business days, with premium cards potentially requiring additional verification time.

Get fast and flexible payment solutions with PayGlocal

Traditional charge cards solve some payment challenges but create others. Strict approval requirements, high fees, and inflexible payment terms often limit business growth and global expansion opportunities.

PayGlocal helps businesses send and receive payments efficiently without the limitations of traditional payment methods.

Whether you're a freelancer invoicing international clients or a growing company managing global transactions, PayGlocal provides all the payment flexibility you need, along with better control and transparency. Here are some of the ways the platform can help you:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries with a local presence that reduces conversion costs and speeds up processing for your international clients.

- Dynamic checkout options: Offer 40+ global payment methods, including cards, digital wallets, and local banking options that increase conversion rates by giving customers familiar payment choices.

- One platform management: Control all payment collection, tracking, and settlement from a single dashboard that reduces administrative work while improving financial visibility.

- Instant compliance documentation: Auto-generate FIRC and other required export documents upon settlement, which handles regulatory requirements without manual paperwork delays.

- Transparent pricing structure: Pay only when you transact with no annual fees, setup costs, or hidden charges that keep your payment processing costs predictable and scalable.

PayGlocal provides modern businesses with reliable, transparent payment collection that adapts to your growth and global reach.

Final thoughts

Charge cards offer unique benefits for businesses and individuals who can manage full monthly payments and qualify for strict approval requirements. They provide spending flexibility and premium benefits but require financial discipline and substantial income to use effectively.

For modern businesses operating globally, traditional payment methods often create more obstacles than solutions. The approval process, payment restrictions, and limited global reach can slow business growth and complicate international operations. PayGlocal offers an efficient and easy platform to manage all your global payments.

Ready to simplify your global payment collection? Get started with PayGlocal today and experience transparent, reliable international payment processing that grows with your business.