What if a single wrong digit could derail a ₹10 lakh international transaction?

In global banking, it happens more often than you’d think. Whether you're setting up a salary deposit, managing vendor payments, or collecting funds from overseas clients, getting the correct bank routing code is non-negotiable. In the U.S., that means using a routing number. In India, it's the MICR code that plays a similar role.

Short for Magnetic Ink Character Recognition, the MICR code is printed at the bottom of Indian cheques and identifies banks and branches with precision. It ensures accurate routing and reduces delays or payment failures.

In 2025 alone, the U.S. ACH network processed over 8.5 billion transactions worth $22.1 trillion in just the first quarter. That volume underscores the importance of using the correct banking code, especially when processing high-stakes payments.

In this blog, we’ll break down what a routing number is, how it compares to MICR, SWIFT, IFSC, and IBAN, and provide a guide on how to avoid common pitfalls that can lead to failed or delayed transactions.

Routing numbers are a fundamental component of banking transactions, particularly for businesses that deal with U.S. clients or manage international payments. Knowing how routing numbers work, their differences from other codes, and where to find them can help prevent transaction delays and errors.

In banking, a routing number identifies the specific bank where an account is held, particularly for processing transactions in the U.S. Each routing number is unique to a bank and is critical for direct deposits, wire transfers, and electronic payments. It’s usually a nine-digit code, with the first few digits representing the bank's location within the Federal Reserve system.

However, in India, you’ll need the MICR code instead of a routing number. So if you’re filling out any form for payments and it asks for a Routing Number, you can fill in the MICR code instead, which will serve the same purpose.

MICR is a nine-digit code that serves a similar function by identifying banks and branches in India for payments and cheque processing. You’ll find this code at the bottom middle of Indian cheques. This code system enables banks to process cheques more efficiently and ensures that payments are accurately routed.

Now that you know what a bank routing number is, let’s look at bank routing numbers in a bit more detail.

A bank routing number is a unique nine-digit code used in the United States to identify specific banks during transactions. This number ensures that funds are directed to the correct bank account for each transfer, deposit, or withdrawal.

Also known as an ABA routing number, named after the American Bankers Association that developed it in 1910, this code was initially created to streamline the sorting and processing of paper checks. Today, they are used in digital banking for direct deposits, electronic payments, and wire transfers.

Each U.S. bank has a unique routing number. Large institutions may have multiple routing numbers, based on their regions or the types of services they offer. Now that you know about what bank routing numbers are, let’s look at why they are essential for international transactions.

For Indian businesses that handle transactions with U.S. clients, routing numbers are essential. Here’s why knowing routing numbers is critical:

Direct deposits and wire transfers: A routing number is required to receive funds directly into your bank account from U.S. companies, clients, or service providers.

Automated Clearing House (ACH) payments: ACH payments utilize routing numbers to transfer funds electronically, enabling international businesses to process payments efficiently.

International transactions with U.S. clients: When receiving payments from U.S. clients, the routing number ensures that funds are accurately directed to the correct bank. Misplacing a digit here could lead to delays or failed transactions.

Here’s how you can find your bank routing number, especially if you’ve a US bank account.

(Note: For Indian bank accounts, your MICR Code will work as the Routing Number.)

There are several ways to find your routing number, especially if you need it for processing international payments:

On cheques: The nine-digit routing number is printed at the bottom left of most U.S. cheques.

Online banking platforms: Many banks display the routing number in your account details, accessible through their website or mobile app.

Customer service: You can call your bank’s customer service line or visit a branch to verify the routing number.

Bank statements: Some banks list the routing number on their monthly statements, making it easy to reference.

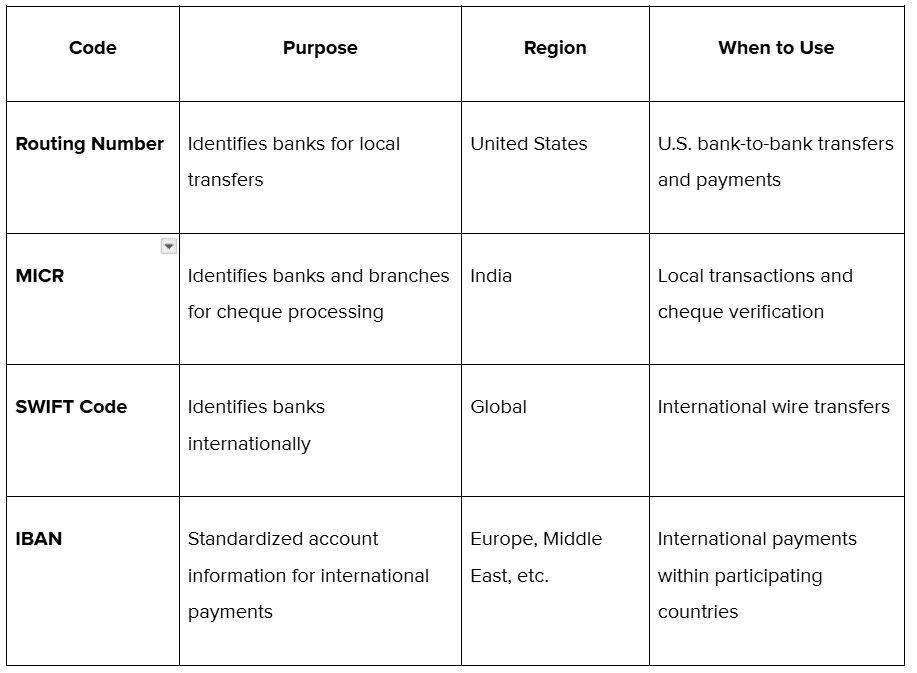

Knowing your Bank Routing number is essential, but it’s also important to know the difference between routing numbers and other codes for error-free transactions.

Using the correct code for each transaction type ensures that your payments are processed without errors. In the case of international transactions, PayGlocal can handle these details, managing payments in multiple currencies and ensuring compliance for international transfers.

Knowing the difference between various codes is essential, but knowing why MICR codes play a crucial role in the Indian Banking System is equally essential.

MICR codes play a crucial role in India’s banking system, particularly in cheque processing and verification. Here’s why they matter:

Speed in processing cheques: The MICR code enables faster processing of cheques, allowing banks to read and route information accurately. This helps you avoid delays, which is essential for businesses that rely on quick payment cycles.

Reduced errors: Since the MICR code is standardized, it reduces the chances of errors in routing payments. This is particularly helpful for exporters, freelancers, and e-commerce sellers managing multiple transactions.

Secure transactions: MICR technology is safe and prevents fraud, as it is printed in magnetic ink that is not easily tampered with. This feature gives added security to payments and protects your funds.

In many ways, MICR codes are central to India’s financial transactions. For global transactions, platforms like PayGlocal simplify international payments, supporting SWIFT, IBAN, and local payment options, so you can process payments efficiently and securely without the risk of mismatched codes.

Now, let’s look at some of the common mistakes that occur while using Routing Number or MICR codes and how you can avoid them.

1. Mixing up routing number with SWIFT code: For international transactions, use the SWIFT Code. Using the routing number alone may not be sufficient for global transactions.

2. Using the wrong code for the transaction type: MICR codes are specific to cheque processing and local transfers in India. Using it in place of a SWIFT or IBAN code for international payments may cause delays or transaction failures. Ensure you use the correct code for each payment type.

3. Confusing MICR with IFSC codes: While both MICR and IFSC codes identify banks in India, they serve different purposes. MICR is for cheque processing, while IFSC is used for electronic payments. Verify which code is needed to ensure smooth processing.

4. Not double-checking the MICR code: Always verify the MICR code on cheques or official documents. Using outdated or incorrect code may result in rejected payments or delays in processing.

Checking and confirming your MICR code before processing payments is essential. It helps prevent unnecessary disruptions, especially in situations where timely payments are critical.

Platforms like PayGlocal make it easier to handle these details, especially for those handling both local and international payments.

For businesses that handle payments with both Indian and international clients, PayGlocal offers a simplified solution that supports multiple currencies and payment methods. With PayGlocal, you don’t have to worry about the complexities of using different codes, such as MICR, SWIFT, or IBAN—PayGlocal’s system integrates these needs within a unified platform.

1. Multiple currency support: With support for 33+ currencies, PayGlocal simplifies multi-currency transactions, allowing you to receive payments in your clients’ local currency. This is especially useful for freelancers, exporters, and small businesses handling international transactions.

2. Enhanced security and compliance: PayGlocal’s built-in security measures, such as SamruddhiX, handle sanctions screening and adhere to AML regulations. These features ensure that every transaction is secure and compliant with global standards, giving you peace of mind.

3. Seamless integration for recurring payments: For businesses that handle regular international transactions, PayGlocal supports recurring billing and multiple payment methods. This flexibility ensures higher approval rates and helps avoid disruptions that often occur with international transactions.

Knowing what a bank routing number is and how it relates to MICR codes is essential for anyone navigating modern banking, particularly when handling cross-border or high-volume transactions. These codes ensure that payments, including cheque-based and international transfers, are processed accurately and without delay.

Whether you're a business owner working with U.S. clients, a freelancer accepting global payments, or a finance team managing multiple accounts, knowing the difference between MICR, bank routing numbers, SWIFT, and IBAN codes gives you the control to route every transaction correctly.

PayGlocal offers a solution that manages currency conversion, ensures compliance, and handles a variety of payment types, helping you avoid the typical headaches that come with international payments. Sign up with PayGlocal now for secure global payments and management!

In global banking, it happens more often than you’d think. Whether you're setting up a salary deposit, managing vendor payments, or collecting funds from overseas clients, getting the correct bank routing code is non-negotiable. In the U.S., that means using a routing number. In India, it's the MICR code that plays a similar role.

Short for Magnetic Ink Character Recognition, the MICR code is printed at the bottom of Indian cheques and identifies banks and branches with precision. It ensures accurate routing and reduces delays or payment failures.

In 2025 alone, the U.S. ACH network processed over 8.5 billion transactions worth $22.1 trillion in just the first quarter. That volume underscores the importance of using the correct banking code, especially when processing high-stakes payments.

In this blog, we’ll break down what a routing number is, how it compares to MICR, SWIFT, IFSC, and IBAN, and provide a guide on how to avoid common pitfalls that can lead to failed or delayed transactions.

Key Takeaways:

Routing numbers are a fundamental component of banking transactions, particularly for businesses that deal with U.S. clients or manage international payments. Knowing how routing numbers work, their differences from other codes, and where to find them can help prevent transaction delays and errors.

- Routing numbers are unique nine-digit codes used in the U.S. to identify banks and ensure accurate fund transfers, including ACH payments and wire transfers.

- In India, the MICR code serves a similar function for cheque processing and is located at the bottom of cheques to identify banks and branches.

- Mixing up routing numbers with SWIFT, IBAN, or IFSC codes can result in failed or delayed payments, especially during cross-border transactions.

- Routing numbers can be found on checks, bank statements, and digital banking platforms or confirmed through customer service for safe and accurate usage.

What is a bank routing number?

In banking, a routing number identifies the specific bank where an account is held, particularly for processing transactions in the U.S. Each routing number is unique to a bank and is critical for direct deposits, wire transfers, and electronic payments. It’s usually a nine-digit code, with the first few digits representing the bank's location within the Federal Reserve system.

However, in India, you’ll need the MICR code instead of a routing number. So if you’re filling out any form for payments and it asks for a Routing Number, you can fill in the MICR code instead, which will serve the same purpose.

MICR is a nine-digit code that serves a similar function by identifying banks and branches in India for payments and cheque processing. You’ll find this code at the bottom middle of Indian cheques. This code system enables banks to process cheques more efficiently and ensures that payments are accurately routed.

Now that you know what a bank routing number is, let’s look at bank routing numbers in a bit more detail.

How do bank routing numbers work in the U.S.?

A bank routing number is a unique nine-digit code used in the United States to identify specific banks during transactions. This number ensures that funds are directed to the correct bank account for each transfer, deposit, or withdrawal.

Also known as an ABA routing number, named after the American Bankers Association that developed it in 1910, this code was initially created to streamline the sorting and processing of paper checks. Today, they are used in digital banking for direct deposits, electronic payments, and wire transfers.

Each U.S. bank has a unique routing number. Large institutions may have multiple routing numbers, based on their regions or the types of services they offer. Now that you know about what bank routing numbers are, let’s look at why they are essential for international transactions.

Why is it important to know your routing number?

For Indian businesses that handle transactions with U.S. clients, routing numbers are essential. Here’s why knowing routing numbers is critical:

Direct deposits and wire transfers: A routing number is required to receive funds directly into your bank account from U.S. companies, clients, or service providers.

Automated Clearing House (ACH) payments: ACH payments utilize routing numbers to transfer funds electronically, enabling international businesses to process payments efficiently.

International transactions with U.S. clients: When receiving payments from U.S. clients, the routing number ensures that funds are accurately directed to the correct bank. Misplacing a digit here could lead to delays or failed transactions.

Here’s how you can find your bank routing number, especially if you’ve a US bank account.

(Note: For Indian bank accounts, your MICR Code will work as the Routing Number.)

How can you find your bank routing number?

There are several ways to find your routing number, especially if you need it for processing international payments:

On cheques: The nine-digit routing number is printed at the bottom left of most U.S. cheques.

Online banking platforms: Many banks display the routing number in your account details, accessible through their website or mobile app.

Customer service: You can call your bank’s customer service line or visit a branch to verify the routing number.

Bank statements: Some banks list the routing number on their monthly statements, making it easy to reference.

Knowing your Bank Routing number is essential, but it’s also important to know the difference between routing numbers and other codes for error-free transactions.

How are routing numbers different from other banking codes?

Using the correct code for each transaction type ensures that your payments are processed without errors. In the case of international transactions, PayGlocal can handle these details, managing payments in multiple currencies and ensuring compliance for international transfers.

Knowing the difference between various codes is essential, but knowing why MICR codes play a crucial role in the Indian Banking System is equally essential.

What is the role of MICR codes in Indian banking?

MICR codes play a crucial role in India’s banking system, particularly in cheque processing and verification. Here’s why they matter:

Speed in processing cheques: The MICR code enables faster processing of cheques, allowing banks to read and route information accurately. This helps you avoid delays, which is essential for businesses that rely on quick payment cycles.

Reduced errors: Since the MICR code is standardized, it reduces the chances of errors in routing payments. This is particularly helpful for exporters, freelancers, and e-commerce sellers managing multiple transactions.

Secure transactions: MICR technology is safe and prevents fraud, as it is printed in magnetic ink that is not easily tampered with. This feature gives added security to payments and protects your funds.

In many ways, MICR codes are central to India’s financial transactions. For global transactions, platforms like PayGlocal simplify international payments, supporting SWIFT, IBAN, and local payment options, so you can process payments efficiently and securely without the risk of mismatched codes.

Now, let’s look at some of the common mistakes that occur while using Routing Number or MICR codes and how you can avoid them.

What are the most common mistakes people make with routing and MICR codes?

1. Mixing up routing number with SWIFT code: For international transactions, use the SWIFT Code. Using the routing number alone may not be sufficient for global transactions.

2. Using the wrong code for the transaction type: MICR codes are specific to cheque processing and local transfers in India. Using it in place of a SWIFT or IBAN code for international payments may cause delays or transaction failures. Ensure you use the correct code for each payment type.

3. Confusing MICR with IFSC codes: While both MICR and IFSC codes identify banks in India, they serve different purposes. MICR is for cheque processing, while IFSC is used for electronic payments. Verify which code is needed to ensure smooth processing.

4. Not double-checking the MICR code: Always verify the MICR code on cheques or official documents. Using outdated or incorrect code may result in rejected payments or delays in processing.

Checking and confirming your MICR code before processing payments is essential. It helps prevent unnecessary disruptions, especially in situations where timely payments are critical.

Platforms like PayGlocal make it easier to handle these details, especially for those handling both local and international payments.

How can PayGlocal help with international transactions?

For businesses that handle payments with both Indian and international clients, PayGlocal offers a simplified solution that supports multiple currencies and payment methods. With PayGlocal, you don’t have to worry about the complexities of using different codes, such as MICR, SWIFT, or IBAN—PayGlocal’s system integrates these needs within a unified platform.

1. Multiple currency support: With support for 33+ currencies, PayGlocal simplifies multi-currency transactions, allowing you to receive payments in your clients’ local currency. This is especially useful for freelancers, exporters, and small businesses handling international transactions.

2. Enhanced security and compliance: PayGlocal’s built-in security measures, such as SamruddhiX, handle sanctions screening and adhere to AML regulations. These features ensure that every transaction is secure and compliant with global standards, giving you peace of mind.

3. Seamless integration for recurring payments: For businesses that handle regular international transactions, PayGlocal supports recurring billing and multiple payment methods. This flexibility ensures higher approval rates and helps avoid disruptions that often occur with international transactions.

Final thoughts

Knowing what a bank routing number is and how it relates to MICR codes is essential for anyone navigating modern banking, particularly when handling cross-border or high-volume transactions. These codes ensure that payments, including cheque-based and international transfers, are processed accurately and without delay.

Whether you're a business owner working with U.S. clients, a freelancer accepting global payments, or a finance team managing multiple accounts, knowing the difference between MICR, bank routing numbers, SWIFT, and IBAN codes gives you the control to route every transaction correctly.

PayGlocal offers a solution that manages currency conversion, ensures compliance, and handles a variety of payment types, helping you avoid the typical headaches that come with international payments. Sign up with PayGlocal now for secure global payments and management!