You've got international customers ready to buy. But when they pull out a credit card, your checkout can't process it. That's a lost sale and revenue.

The global credit card payment market was worth $736.58 billion in 2025 and is on track to nearly double by 2034. Cards are how the world pays online. If your business can't accept them, your competitors will.

This guide breaks down in detail how to accept payment from a credit card. You'll learn the methods, the fees, what to look for in a provider, and how to set up and get started.

Credit card payments: A customer shares their card details, a payment gateway sends the request to the credit card network and issuing bank, and funds settle into your account after approval.

Accepting credit card payments means giving your customers the option to pay using their Visa, Mastercard, or other card at your checkout. To make this happen, you need a payment gateway that sits between your website and the banking network. The gateway collects the card details, checks with the buyer's bank, and confirms whether the payment went through.

For example, say you run an online store in India, and a customer in Canada buys a product. They type in their Visa card number at checkout. Your payment gateway sends the request, the bank in Canada approves it, and you receive the funds in your multi-currency account within the agreed timeline. The customer sees a confirmation, and you see a new order.

A customer who can't pay with their preferred method at checkout will almost always leave. For businesses selling internationally, credit cards are often the only payment option buyers trust.

Here’s why accepting credit card payments matters for your business:

If your business serves customers outside India, accepting credit cards is essential. It directly affects whether buyers complete their purchase or walk away. This is especially true for freelancers and service exporters who invoice international clients regularly.

Tip: Even if most of your current customers pay through bank transfers, adding a card option can attract a new segment of international buyers who prefer to pay by card.

Failed payments often trace back to not knowing how the process works. When you see each step clearly, you can pick the right setup and troubleshoot issues faster.

1. Customer enters card details: The buyer fills in their card number, expiry date, and security code on your checkout page or payment link.

2. Payment gateway encrypts and sends the data: Your gateway secures the information and forwards it to the acquiring bank (your bank or your provider's bank).

3. Card network routes the request: The acquiring bank sends the transaction to the card network (Visa, Mastercard, etc.), which passes it to the customer's issuing bank.

4. Issuing bank approves or declines: The customer's bank checks the card balance, fraud signals, and authentication. It sends back an approval or a decline.

5. Confirmation reaches the customer: If approved, the customer sees a success message. If declined, they're prompted to try again or use another method.

6. Settlement happens: The approved amount, minus fees, is deposited into your merchant account within the settlement period (usually 2-7 business days, depending on the provider).

Note: Declined transactions don't always mean the customer lacks funds. Sometimes the issuing bank flags the payment due to a location mismatch or missing authentication. A good provider helps reduce these payment failures automatically.

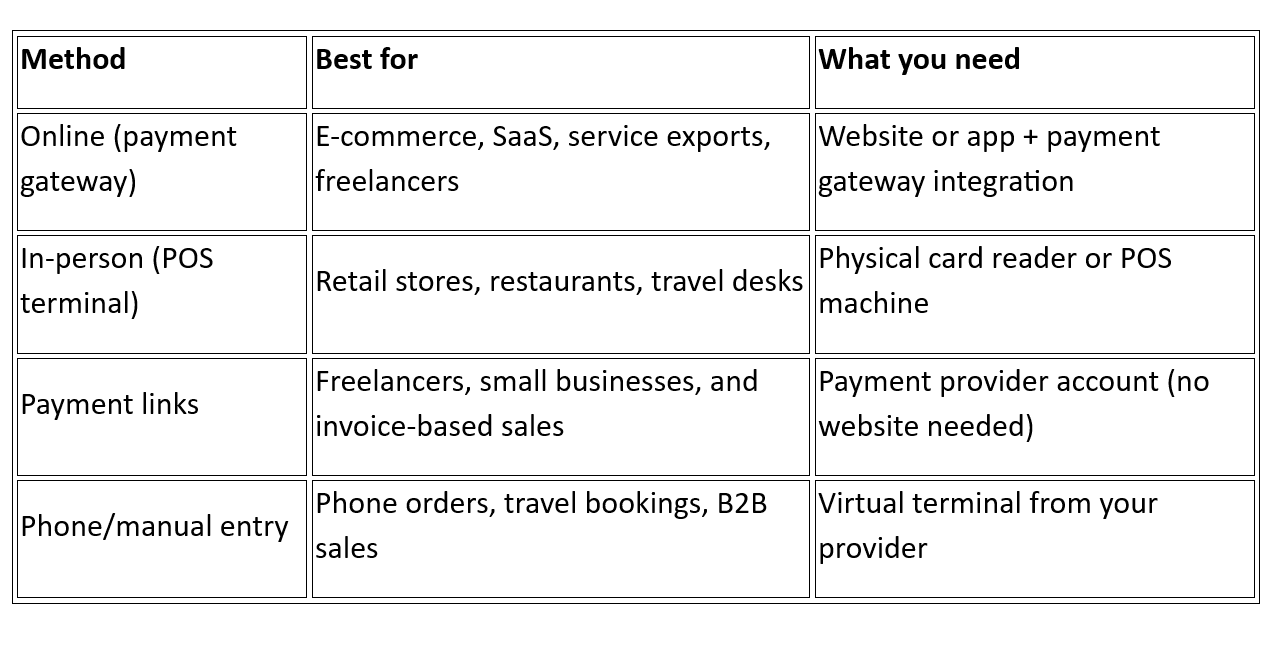

Every business collects payments differently. The best way to accept credit card payments depends on your selling model. Here’s a quick overview of the top methods:

Let’s take a closer look at each method:

This is the most common way for businesses in India to accept credit card payments from global customers. You integrate a payment gateway into your website or app. Customers enter their card details on a checkout page, and the gateway handles the rest.

Most gateways offer plugins for popular platforms like Shopify, WooCommerce, and Magento. If you're using a custom-built site, you'll need to connect through your provider's set of tools. Either way, you can go live within days.

For businesses selling services, software, or products internationally, this is the go-to method. It handles international transaction fees transparently and works 24/7 across time zones.

If you don't have a website, payment links are a fast alternative. Your provider generates a unique link for a specific amount. You share it over email, WhatsApp, or any messaging app. The customer clicks, enters their card details, and pays.

This method works well for freelancers, consultants, and small businesses that invoice clients directly. No coding needed.

For businesses with a physical presence, a point-of-sale (POS) terminal or mobile card reader lets customers tap, insert, or swipe their credit card. The reader connects to your payment provider and processes the transaction on the spot.

This method is common in retail, hospitality, and travel. Setup takes a bit longer because you need hardware.

Some businesses take orders over the phone. In this method, you can type in the customer's card details in the system to process the payment manually. This is useful for travel agencies, B2B companies, and any business where the buyer isn't present at checkout.

Tip: If you sell online to international buyers, a payment gateway with multi-currency support should be your first choice. It covers the widest range of customers and scales with your business.

Picking the wrong provider causes issues that show up months later, such as declined payments, slow settlements, hidden charges, and poor support when something breaks. Here are some of the key factors to consider while choosing the best credit card payment provider:

Don't choose a provider based only on the lowest fee. A provider that costs slightly more but approves 15% more transactions will earn you more money in the long run.

Note: Ask potential providers about their approval rates for international cards specifically. Domestic and international card processing are very different, and not every provider performs well across both.

Every credit card transaction costs you something. The key is knowing exactly what you're paying for, so there are no surprises on your invoice.

For businesses comparing SWIFT charges or wire transfer costs alongside cards, looking at total cost across methods helps you find the right mix.

Always ask for a full fee schedule before signing up. The cheapest-looking provider may have charges buried in fine print.

Tip: If your monthly volume is high, ask your provider about volume-based discounts. Many offer lower rates once you cross a certain transaction threshold.

Most payment problems aren't caused by technology. They come from decisions made during setup or blind spots that go unnoticed until customers complain.

Review your payment setup every quarter. What worked six months ago may need adjusting as your customer base grows or shifts to new regions.

Setting up credit card payments takes less time than most people expect. Here's a complete step-by-step process.

1. Pick your payment method: Decide whether you need an online gateway, payment links, a POS terminal, or a combination. Your selling model determines the answer.

2. Choose a provider: Compare providers on approval rates, multi-currency support, fees, integration options, and support quality. Shortlist two or three and request demos.

3. Create your merchant account: Sign up with your chosen provider. You'll need your business registration, bank account details, and basic KYC documents. Most providers complete this in 1-3 business days.

4. Integrate with your website or platform: If you're selling online, connect the payment gateway to your website. Use a ready-made plugin for platforms like Shopify or WooCommerce. For custom sites, follow your provider's setup documentation.

5. Configure your settings: Set your accepted currencies, enable fraud screening, and customize the checkout page to match your brand.

6. Test before going live: Run test transactions to confirm everything works. Check card approvals, refunds, error messages, and confirmation emails.

7. Go live and monitor: Once everything checks out, flip the switch. Monitor your first few transactions closely and review your dashboard daily for the first week.

The entire setup, from sign-up to first live transaction, can take as little as one day with a modern provider that offers no-code or plugin-based integration.

International card payments are harder to get right than domestic ones. Declined transactions, currency conversion headaches, and slow settlements add up quickly when you're selling to customers across borders.

PayGlocal is built specifically for businesses in India that collect payments from global customers. Here's what it brings to the table.

For businesses selling globally, PayGlocal handles the payment complexity so that you can focus on growing your business.

Accepting credit card payments is one of the most direct ways to grow your international sales. The process involves choosing a method, picking a provider, integrating it with your website or platform, and monitoring your transactions for improvements.

If you're looking for a provider built for cross-border card payments from day one, PayGlocal is worth considering. Businesses already using it have seen high international approval rates.

The longer you wait to fix your payment setup, the more completed sales you lose to declined transactions and checkout drop-offs. Get started with PayGlocal today.

The global credit card payment market was worth $736.58 billion in 2025 and is on track to nearly double by 2034. Cards are how the world pays online. If your business can't accept them, your competitors will.

This guide breaks down in detail how to accept payment from a credit card. You'll learn the methods, the fees, what to look for in a provider, and how to set up and get started.

Key takeaways

Credit card payments: A customer shares their card details, a payment gateway sends the request to the credit card network and issuing bank, and funds settle into your account after approval.

- Online is the primary channel: For businesses selling globally, accepting credit cards online through a payment gateway is the most practical and scalable method.

- Fees are part of the deal: Expect per-transaction fees, currency conversion charges, and possible monthly costs depending on your provider.

- Provider choice matters: Look for high approval rates, multi-currency support, fraud protection, and simple setup when picking a payment partner.

- PayGlocal supports 180+ currencies: With 40+ payment methods across 180+ countries, it's built for businesses accepting payments from global customers.

What does accepting credit card payments actually involve?

Accepting credit card payments means giving your customers the option to pay using their Visa, Mastercard, or other card at your checkout. To make this happen, you need a payment gateway that sits between your website and the banking network. The gateway collects the card details, checks with the buyer's bank, and confirms whether the payment went through.

For example, say you run an online store in India, and a customer in Canada buys a product. They type in their Visa card number at checkout. Your payment gateway sends the request, the bank in Canada approves it, and you receive the funds in your multi-currency account within the agreed timeline. The customer sees a confirmation, and you see a new order.

Why does accepting credit cards matter for your business?

A customer who can't pay with their preferred method at checkout will almost always leave. For businesses selling internationally, credit cards are often the only payment option buyers trust.

Here’s why accepting credit card payments matters for your business:

- Wider customer reach: Credit cards are accepted and used in nearly every country, giving your business access to buyers who wouldn't pay through bank transfers or local wallets.

- Faster purchase decisions: Customers with a card on hand can pay instantly, reducing the time between interest and completed sale.

- Higher order values: Card buyers tend to spend more per transaction than customers paying through other methods, which lifts your average revenue per sale.

- Credibility and trust: Displaying card logos like Visa and Mastercard on your checkout signals that your business is legitimate and secure.

- Recurring payment support: Cards make it easy to set up subscriptions, memberships, and repeat billing without asking customers to act each cycle.

If your business serves customers outside India, accepting credit cards is essential. It directly affects whether buyers complete their purchase or walk away. This is especially true for freelancers and service exporters who invoice international clients regularly.

Tip: Even if most of your current customers pay through bank transfers, adding a card option can attract a new segment of international buyers who prefer to pay by card.

How does a credit card payment work?

Failed payments often trace back to not knowing how the process works. When you see each step clearly, you can pick the right setup and troubleshoot issues faster.

1. Customer enters card details: The buyer fills in their card number, expiry date, and security code on your checkout page or payment link.

2. Payment gateway encrypts and sends the data: Your gateway secures the information and forwards it to the acquiring bank (your bank or your provider's bank).

3. Card network routes the request: The acquiring bank sends the transaction to the card network (Visa, Mastercard, etc.), which passes it to the customer's issuing bank.

4. Issuing bank approves or declines: The customer's bank checks the card balance, fraud signals, and authentication. It sends back an approval or a decline.

5. Confirmation reaches the customer: If approved, the customer sees a success message. If declined, they're prompted to try again or use another method.

6. Settlement happens: The approved amount, minus fees, is deposited into your merchant account within the settlement period (usually 2-7 business days, depending on the provider).

Note: Declined transactions don't always mean the customer lacks funds. Sometimes the issuing bank flags the payment due to a location mismatch or missing authentication. A good provider helps reduce these payment failures automatically.

What are the ways to accept credit card payments?

Every business collects payments differently. The best way to accept credit card payments depends on your selling model. Here’s a quick overview of the top methods:

Let’s take a closer look at each method:

1. Online through a payment gateway

This is the most common way for businesses in India to accept credit card payments from global customers. You integrate a payment gateway into your website or app. Customers enter their card details on a checkout page, and the gateway handles the rest.

Most gateways offer plugins for popular platforms like Shopify, WooCommerce, and Magento. If you're using a custom-built site, you'll need to connect through your provider's set of tools. Either way, you can go live within days.

For businesses selling services, software, or products internationally, this is the go-to method. It handles international transaction fees transparently and works 24/7 across time zones.

2. Through payment links

If you don't have a website, payment links are a fast alternative. Your provider generates a unique link for a specific amount. You share it over email, WhatsApp, or any messaging app. The customer clicks, enters their card details, and pays.

This method works well for freelancers, consultants, and small businesses that invoice clients directly. No coding needed.

3. In-person with a card reader

For businesses with a physical presence, a point-of-sale (POS) terminal or mobile card reader lets customers tap, insert, or swipe their credit card. The reader connects to your payment provider and processes the transaction on the spot.

This method is common in retail, hospitality, and travel. Setup takes a bit longer because you need hardware.

4. By phone or manual entry

Some businesses take orders over the phone. In this method, you can type in the customer's card details in the system to process the payment manually. This is useful for travel agencies, B2B companies, and any business where the buyer isn't present at checkout.

Tip: If you sell online to international buyers, a payment gateway with multi-currency support should be your first choice. It covers the widest range of customers and scales with your business.

What should you look for in a credit card payment provider?

Picking the wrong provider causes issues that show up months later, such as declined payments, slow settlements, hidden charges, and poor support when something breaks. Here are some of the key factors to consider while choosing the best credit card payment provider:

- High approval rates: Your provider should have strong relationships with card networks and issuing banks worldwide to reduce false declines. This is especially important given the international payment challenges that come with cross-border sales.

- Multi-currency support: If you sell globally, your provider should accept payments in the currencies your customers prefer. Forcing buyers to pay in INR adds friction.

- Fraud and risk protection: Look for built-in fraud screening that catches suspicious transactions without blocking real customers. Features like payment tokenization add another layer of security.

- Simple integration: The setup process should be straightforward, with ready-made plugins for popular e-commerce platforms and clear documentation for custom builds.

- Transparent pricing: Fees should be clearly listed. Watch for hidden charges on currency conversion, refunds, or chargebacks.

- Fast settlements: How quickly does money reach your bank account? Some providers settle in 2 days; others take a week or more.

- Responsive support: When a payment issue comes up at 2 AM for a customer in a different time zone, you need help fast.

Don't choose a provider based only on the lowest fee. A provider that costs slightly more but approves 15% more transactions will earn you more money in the long run.

Note: Ask potential providers about their approval rates for international cards specifically. Domestic and international card processing are very different, and not every provider performs well across both.

What fees come with accepting credit card payments?

Every credit card transaction costs you something. The key is knowing exactly what you're paying for, so there are no surprises on your invoice.

- Transaction fee: A percentage of each payment, typically 1.5% to 3.5%, depending on the provider and whether the transaction is domestic or international.

- Currency conversion fee: If your customer pays in a foreign currency and you settle in INR, there's usually a markup on the foreign exchange rate, which can be up to 3%.

- Setup or monthly fee: Some providers charge a one-time setup fee or a monthly subscription. Others have zero fixed costs and only charge per transaction.

- Chargeback fee: If a customer disputes a charge and the card network reverses it, you'll typically pay a fee on top of losing the transaction amount.

- Refund processing fee: Some providers charge a small fee when you issue a refund, even though the original transaction fee isn't always returned.

For businesses comparing SWIFT charges or wire transfer costs alongside cards, looking at total cost across methods helps you find the right mix.

Always ask for a full fee schedule before signing up. The cheapest-looking provider may have charges buried in fine print.

Tip: If your monthly volume is high, ask your provider about volume-based discounts. Many offer lower rates once you cross a certain transaction threshold.

What mistakes should you avoid when accepting credit cards?

Most payment problems aren't caused by technology. They come from decisions made during setup or blind spots that go unnoticed until customers complain.

- Offering only one payment method: Not every international customer has a Visa or Mastercard. Some prefer local payment options as well. So, offering only cards limits your reach.

- Ignoring declined transaction data: Declines happen. What matters is whether you're tracking why. Is it fraud flags? Incorrect card details? Issuing bank blocks? Your provider's dashboard should give you this data.

- Not testing the checkout experience: If your checkout page loads slowly, asks for too much information, or looks unfamiliar to international buyers, they'll leave. Test it from a customer's perspective before going live.

- Forgetting about recurring billing: If your business model includes subscriptions or repeat payments, make sure your provider supports automated billing on international cards.

Review your payment setup every quarter. What worked six months ago may need adjusting as your customer base grows or shifts to new regions.

How do you set up credit card payments for your business?

Setting up credit card payments takes less time than most people expect. Here's a complete step-by-step process.

1. Pick your payment method: Decide whether you need an online gateway, payment links, a POS terminal, or a combination. Your selling model determines the answer.

2. Choose a provider: Compare providers on approval rates, multi-currency support, fees, integration options, and support quality. Shortlist two or three and request demos.

3. Create your merchant account: Sign up with your chosen provider. You'll need your business registration, bank account details, and basic KYC documents. Most providers complete this in 1-3 business days.

4. Integrate with your website or platform: If you're selling online, connect the payment gateway to your website. Use a ready-made plugin for platforms like Shopify or WooCommerce. For custom sites, follow your provider's setup documentation.

5. Configure your settings: Set your accepted currencies, enable fraud screening, and customize the checkout page to match your brand.

6. Test before going live: Run test transactions to confirm everything works. Check card approvals, refunds, error messages, and confirmation emails.

7. Go live and monitor: Once everything checks out, flip the switch. Monitor your first few transactions closely and review your dashboard daily for the first week.

The entire setup, from sign-up to first live transaction, can take as little as one day with a modern provider that offers no-code or plugin-based integration.

Accept credit card payments from 180+ countries with PayGlocal

International card payments are harder to get right than domestic ones. Declined transactions, currency conversion headaches, and slow settlements add up quickly when you're selling to customers across borders.

PayGlocal is built specifically for businesses in India that collect payments from global customers. Here's what it brings to the table.

- Card payments: Fewer international credit card transactions get declined because each payment is automatically routed through the best path to the buyer's bank, so more of your sales go through successfully.

- Global payment methods: Your customers can pay using 40+ payment methods across 180+ countries, which means buyers in every region find a familiar way to check out.

- Multi-currency accounts: You collect payments in 33+ currencies and get funds settled with a downloadable foreign inward remittance certificate (FIRC) right from your dashboard, keeping compliance simple.

- Dynamic checkout: The checkout page adapts to each customer's location and preferred payment method, resulting in fewer drop-offs at the final step.

- One platform: You manage every payment, refund, and report from a single dashboard, removing the need to handle separate tools for different payment types.

For businesses selling globally, PayGlocal handles the payment complexity so that you can focus on growing your business.

Final thoughts

Accepting credit card payments is one of the most direct ways to grow your international sales. The process involves choosing a method, picking a provider, integrating it with your website or platform, and monitoring your transactions for improvements.

If you're looking for a provider built for cross-border card payments from day one, PayGlocal is worth considering. Businesses already using it have seen high international approval rates.

The longer you wait to fix your payment setup, the more completed sales you lose to declined transactions and checkout drop-offs. Get started with PayGlocal today.