When handling international payments, whether you're a freelancer, an SMB, or an exporter, choosing the right method is important. Due to the complexity of cross-border transactions, ACH and wire transfers are commonly used by businesses, each offering distinct benefits based on the transaction type.

The ACH Network has seen a strong growth in the first quarter of 2025, with both standard and Same-day ACH transactions experiencing significant gains. ACH payment volume increased by 4.2%, reaching 8.5 billion.

But which payment method is the best for you? Whether looking for cost-effective payments for recurring bills or fast transactions for urgent business deals, choosing the proper method can save you time and money.

Before diving into specifics, let’s clarify what ACH and wire transfers are, especially in cross-border transactions.

Each method offers unique benefits, so understanding how each works will help you choose the most efficient solution for your business.

ACH transfers are known for their low cost, which makes them ideal for freelancers, small businesses, and exporters handling recurring or bulk payments. However, ACH’s slower processing times (1-3 business days) may not suit urgent transactions.

ACH is ideal for international payments that don’t require urgency, making it perfect for freelancers and small businesses managing regular transactions.

Wire transfers are the ideal choice when speed and security are paramount. They allow for immediate transfers, often completing within the same day or hours, making them ideal for larger payments or urgent business needs.

Here’s why wire transfers work best for high-value transactions:

Wire transfers offer unparalleled speed, making them the go-to method for urgent, high-value payments despite the higher fees.

When deciding between ACH and wire transfers, you must consider your specific needs as an exporter, freelancer, or software developer. Here’s a quick comparison:

Both ACH and wire transfers have distinct advantages, depending on your needs. ACH is ideal for cost-effective, routine payments, while wire transfers are perfect for fast, urgent, or large transactions. The decision ultimately depends on whether speed or cost is more critical to your business.

ACH is best for routine, non-urgent payments. Here are the key scenarios where ACH shines:

ACH provides a reliable, cost-effective method for those managing ongoing international payments to handle transactions without urgency.

Whether you're an exporter, freelancer, or software developer, PayGlocal simplifies the complexities of international payments. By offering competitive exchange rates, lower fees, and easy integration with your existing financial systems, this platform ensures you can send and receive payments globally without unnecessary delays or high costs.

PayGlocal ensures that your international payments are handled smoothly, with lower costs and faster processing speeds than traditional methods.

When comparing ACH vs wire transfers, your choice depends on whether you prioritize speed or cost. ACH is ideal for non-urgent, routine payments, while wire transfers are perfect for high-value, time-sensitive transactions.

For freelancers, exporters, and SMBs looking to streamline their cross-border payments, PayGlocal ensures both cost-effectiveness and speed, making your global payments simpler.

Do you need a seamless payment solution for your international clients?

Contact PayGlocal today and discover how our services can simplify your global payments.

ACH transfers are generally slower and cheaper, ideal for non-urgent, recurring payments. Wire transfers are faster and more expensive, suitable for high-value or urgent transactions.

PayGlocal supports ACH payments for international transactions, ensuring low costs and efficiency.

Wire transfers are irreversible once completed, making them suitable for final, secure transactions.

ACH is more cost-effective for regular payments. Wire transfers are better for urgent, high-value transfers, though they have higher fees.

ACH and wire transfers are secure ways to transfer funds. ACH transfers can be reversed in fraud or error cases, adding protection. Wire transfers are generally irreversible, ensuring security for recipients but demanding accuracy from senders.

The ACH Network has seen a strong growth in the first quarter of 2025, with both standard and Same-day ACH transactions experiencing significant gains. ACH payment volume increased by 4.2%, reaching 8.5 billion.

But which payment method is the best for you? Whether looking for cost-effective payments for recurring bills or fast transactions for urgent business deals, choosing the proper method can save you time and money.

What are ACH and Wire Transfers?

Before diving into specifics, let’s clarify what ACH and wire transfers are, especially in cross-border transactions.

- ACH (Automated Clearing House): A network used primarily in the U.S. to handle bulk electronic payments between financial institutions. It’s cost-effective and ideal for routine transactions like salaries, utility bills, or recurring international payments.

- Wire Transfer: A real-time, direct bank transfer that allows funds to be sent immediately from one bank to another. Wire transfers are often used for larger sums, urgent payments, and international transactions.

Each method offers unique benefits, so understanding how each works will help you choose the most efficient solution for your business.

How ACH Transfers Work for Cross-Border Payments

ACH transfers are known for their low cost, which makes them ideal for freelancers, small businesses, and exporters handling recurring or bulk payments. However, ACH’s slower processing times (1-3 business days) may not suit urgent transactions.

- Batch Processing: ACH transfers are processed in batches, making them efficient for regular payments but slower for urgent needs.

- Low-Cost Fees: ACH payments are often free or have minimal fees, making them a popular option for cost-effective international transactions.

- Best for Freelancers & SMBs: Perfect for freelancers receiving regular payments from international clients or small exporters paying vendors abroad.

ACH is ideal for international payments that don’t require urgency, making it perfect for freelancers and small businesses managing regular transactions.

Wire Transfers for Urgent or High-Value Payments

Wire transfers are the ideal choice when speed and security are paramount. They allow for immediate transfers, often completing within the same day or hours, making them ideal for larger payments or urgent business needs.

Here’s why wire transfers work best for high-value transactions:

- Real-Time Transfers: Unlike ACH, wire transfers are processed instantly, which is critical for urgent payments.

- High Fees: The cost for wire transfers can be steep, ranging from $15 to $50 or more, depending on the bank, especially for international transfers.

- Best for Large Transactions: Wire transfers are best suited for larger sums, urgent deals, or time-sensitive payments.

Wire transfers offer unparalleled speed, making them the go-to method for urgent, high-value payments despite the higher fees.

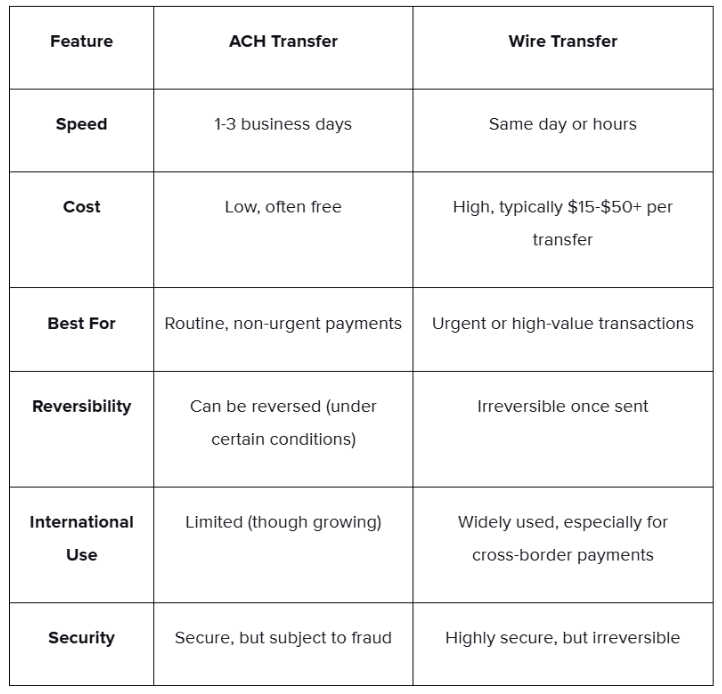

ACH vs Wire Transfer: A Comparison for Global Payments

When deciding between ACH and wire transfers, you must consider your specific needs as an exporter, freelancer, or software developer. Here’s a quick comparison:

Both ACH and wire transfers have distinct advantages, depending on your needs. ACH is ideal for cost-effective, routine payments, while wire transfers are perfect for fast, urgent, or large transactions. The decision ultimately depends on whether speed or cost is more critical to your business.

Who Should Use ACH?

ACH is best for routine, non-urgent payments. Here are the key scenarios where ACH shines:

- Freelancers: Ideal for long-term international contracts where payments are received on a regular basis.

- Exporters: Perfect for consistent payments to international suppliers or receiving regular payments for goods sold.

- Small Businesses: For managing ongoing transactions with clients or vendors abroad.

ACH provides a reliable, cost-effective method for those managing ongoing international payments to handle transactions without urgency.

How PayGlocal Supports Global Transactions

Whether you're an exporter, freelancer, or software developer, PayGlocal simplifies the complexities of international payments. By offering competitive exchange rates, lower fees, and easy integration with your existing financial systems, this platform ensures you can send and receive payments globally without unnecessary delays or high costs.

- Easy Cross-Border Payments: With PayGlocal, you can accept payments from clients worldwide, cutting out the complexity of international banking systems.

- Cost-Effective: Our platform offers lower fees than traditional wire transfers, especially for recurring or bulk payments.

- Fast and Reliable: PayGlocal streamlines payment processing, enabling you to receive funds quickly from clients abroad.

- Quick Processing: Streamlined payments ensure faster transactions for freelancers, exporters, and SMBs.

- International Integration: Easy global payment solutions, no matter where your clients or suppliers are based.

PayGlocal ensures that your international payments are handled smoothly, with lower costs and faster processing speeds than traditional methods.

Conclusion

When comparing ACH vs wire transfers, your choice depends on whether you prioritize speed or cost. ACH is ideal for non-urgent, routine payments, while wire transfers are perfect for high-value, time-sensitive transactions.

For freelancers, exporters, and SMBs looking to streamline their cross-border payments, PayGlocal ensures both cost-effectiveness and speed, making your global payments simpler.

Do you need a seamless payment solution for your international clients?

Contact PayGlocal today and discover how our services can simplify your global payments.

FAQs

1. What’s the difference between ACH and wire transfers for international payments?

ACH transfers are generally slower and cheaper, ideal for non-urgent, recurring payments. Wire transfers are faster and more expensive, suitable for high-value or urgent transactions.

2. Can I use PayGlocal for ACH payments?

PayGlocal supports ACH payments for international transactions, ensuring low costs and efficiency.

3. Are wire transfers reversible?

Wire transfers are irreversible once completed, making them suitable for final, secure transactions.

4. Which method is more cost-effective?

ACH is more cost-effective for regular payments. Wire transfers are better for urgent, high-value transfers, though they have higher fees.

5. How do ACH transfers and wire transfers differ in terms of security?

ACH and wire transfers are secure ways to transfer funds. ACH transfers can be reversed in fraud or error cases, adding protection. Wire transfers are generally irreversible, ensuring security for recipients but demanding accuracy from senders.