Tax Collected at Source on foreign remittances has become a major concern for Indian businesses and individuals sending money abroad. With new thresholds and rates taking effect in 2025, you need proper strategies to keep your international payment costs under control.

Recent changes raised the TCS exemption limit from ₹7 lakh to ₹10 lakh per financial year. This means more room to send money abroad without an additional tax burden. However, once you cross this threshold, TCS rates can reach up to 20% depending on your remittance purpose.

In this guide, we will show you effective methods to avoid or minimize TCS on your foreign transfers. You'll learn timing strategies, purpose-based exemptions, and alternative payment routes that can result in significant savings.

TCS stands for Tax Collected at Source. Banks and authorized dealers collect this tax when you send money abroad under India's LRS (Liberalised Remittance Scheme) - a facility that allows resident individuals to freely remit up to USD 250,000 per financial year for various purposes.

The government introduced TCS to track foreign currency outflows and prevent tax evasion. When you make international transfers, your bank automatically deducts TCS and deposits it with the Income Tax Department.

For instance, if you send ₹12 lakh for education in a financial year, TCS applies only on ₹2 lakh (the amount above the ₹10 lakh threshold). The rate depends on your remittance purpose; education attracts 5% while investments face 20% TCS.

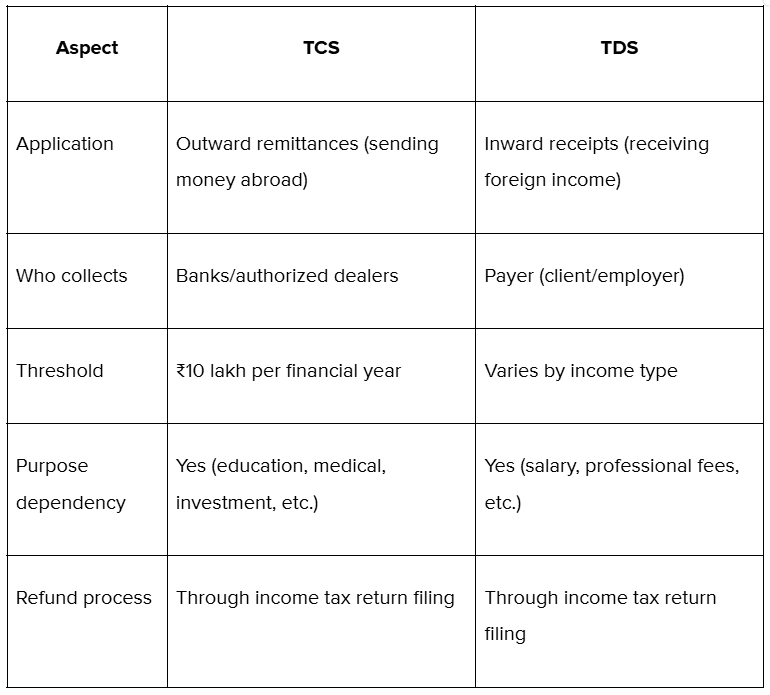

TCS and TDS are two similar terms with distinct tax collection mechanisms and different applications for international transfers.

Here's a quick comparison of TCS and TDS for international transactions:

Both TCS and TDS serve as advance tax payments that you can claim when filing returns.

The latest TCS framework became effective from April 1, 2025. Here's what changed and what you need to know:

New exemption threshold: No TCS applies on foreign remittances up to ₹10 lakh per financial year. This is an increase from the previous ₹7 lakh limit.

TCS calculation method: TCS applies only to amounts exceeding ₹10 lakh in a financial year, not on the entire remittance amount.

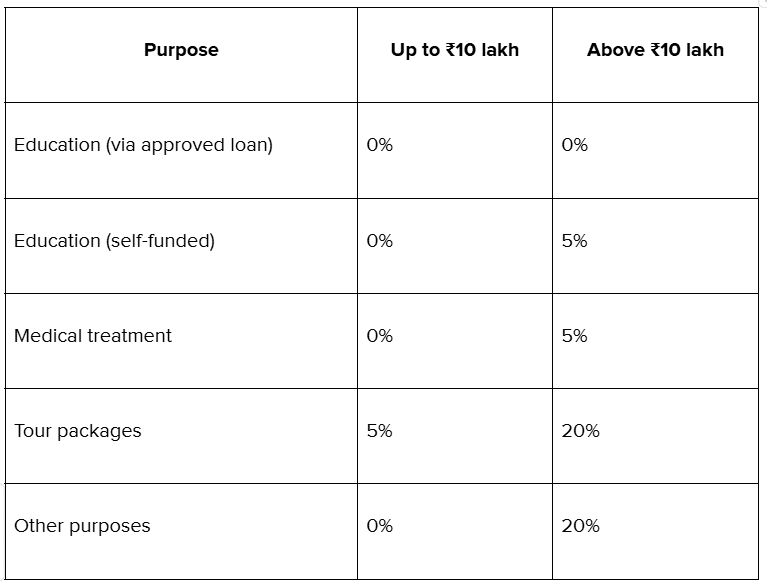

Here’s a quick overview of the current TCS rates for different remittance purposes:

TCS applies progressively, only on amounts above the ₹10 lakh threshold. Here are some examples:

1. Education remittance: You send ₹15 lakh for self-funded education. TCS applies on ₹5 lakh at 5% rate. Your TCS = ₹25,000.

2. Investment purpose: You transfer ₹12 lakh for foreign investments. TCS applies on ₹2 lakh at a 20% rate. Your TCS = ₹40,000.

3. Multiple purposes: You send ₹8 lakh for education and ₹4 lakh for travel in the same year. Total = ₹12 lakh. TCS applies on ₹2 lakh at respective rates.

Your bank tracks all foreign remittances linked to your PAN across the financial year. Once the cumulative amount exceeds ₹10 lakh, TCS is immediately applicable to subsequent transfers.

Looking for faster international payments with better exchange rates? PayGlocal helps businesses complete transfers faster with transparent pricing.

Managing international payments without triggering excessive TCS requires strategic planning and a proper understanding of available exemptions. Multiple methods can help you minimize or completely avoid the TCS burden while staying compliant with regulations.

Here are some effective strategies that businesses and individuals can use to reduce TCS on foreign transfers:

Split large remittances across two financial years to stay within the ₹10 lakh annual limit. This requires careful planning but can save substantial TCS.

For instance, if you need to send ₹18 lakh for education, transfer ₹9 lakh in March and ₹9 lakh in April. This way, both transfers stay below the threshold.

Plan major expenses like education fees or property purchases well in advance. Contact your university or service provider to understand payment schedules and deadlines.

Education loans from banks or NBFCs (Non-Banking Financial Companies) recognized under Section 80E of the Income Tax Act attract zero TCS. This applies regardless of the loan amount.

Even if you have personal funds available, taking an education loan can be cost-effective. The TCS savings often outweigh the loan interest costs.

Similarly, you can explore education financing options through foreign universities or specialized education loan providers. Ensure the lender qualifies under Income Tax regulations.

Each individual gets a separate ₹10 lakh TCS exemption limit. Married couples can effectively transfer ₹20 lakh per year without TCS.

Your spouse, parents, or adult children can make separate remittances for legitimate purposes. However, ensure each person has genuine reasons for the transfer to avoid scrutiny.

This strategy works well for family maintenance, education expenses, or medical treatment abroad. Maintain proper documentation for each family member's remittance purpose.

Different purposes attract different TCS rates. Medical treatment and self-funded education get preferential 5% rates above ₹10 lakh.

Always select the correct purpose code when filling out remittance forms. Wrong classification can lead to higher TCS rates and compliance issues.

For example, if you're paying for medical treatment abroad, don't classify it as "other purposes," which attracts 20% TCS. Proper documentation helps support your purpose declaration.

NRI (Non-Resident Indian) accounts offer certain exemptions for family maintenance remittances. If you're an NRI, use these accounts for recurring transfers to avoid TCS.

NRO (Non-Resident Ordinary) account holders can send back up to USD 1 million per financial year for legitimate purposes. Some of these transfers can qualify for TCS exemptions.

This strategy works best, especially for established NRIs with regular income sources abroad. Consult your bank about specific NRI remittance benefits and forex management options.

Foreign spending through international credit cards may avoid TCS for amounts up to ₹10 lakh annually. This works for education fees, travel expenses, or service payments.

However, credit card transactions still count toward your annual LRS limit. Plan accordingly if you have other foreign remittance needs.

Some payment processing methods offer better exchange rates and lower fees compared to traditional bank transfers.

Tired of high bank charges eating into your transfers? PayGlocal offers competitive rates with no hidden fees for international payments.

Instead of booking complete tour packages that attract higher TCS rates, pay for flights, hotels, and activities separately through different vendors.

This approach can help you avoid the 5% TCS on tour packages up to ₹10 lakh and 20% beyond that limit. Book directly with airlines and hotels when possible.

Ensure your payment structure doesn't appear artificial or solely for tax avoidance purposes. Genuine business reasons should drive your payment choices.

TCS functions as advance tax payment, not an additional cost. You can claim TCS as credit against your final tax liability when filing income tax returns.

Here’s a step-by-step refund process:

Verify TCS credit: Check Form 26AS or Annual Information Statement to confirm TCS amounts.

It is essential to file your income tax return within the due date to claim TCS refunds. Late filings can complicate the refund process.

Maintain all remittance receipts and bank statements as supporting documents. The Income Tax Department may ask for verification during assessment proceedings.

Poor planning and incorrect documentation can lead to unnecessary TCS burden and compliance issues.

Here are the most frequent mistakes that cost businesses and individuals extra money on foreign remittances:

Managing international payments while dealing with TCS complexities can overwhelm growing businesses. Traditional banks often lack transparency in pricing and offer limited guidance on tax optimization strategies.

PayGlocal helps Indian businesses handle international payments with complete transparency and expert support. Here's how we make global transactions easier:

PayGlocal serves exporters, service providers, and businesses across India with reliable international payment solutions that save time and reduce costs.

TCS on foreign remittances doesn't have to drain your international payment budget. The 2025 rule changes provide more flexibility with the increased ₹10 lakh exemption threshold, while education loans offer complete TCS exemption regardless of the amount.

Smart timing, proper purpose classification, and family member distribution can help you minimize TCS costs while staying compliant. Remember that TCS is an advance tax, not a permanent cost, so proper tax filing can recover excess amounts.

Plan your international payments strategically and maintain proper documentation for all transfers. Consider professional payment platforms like PayGlocal that offer transparent pricing and efficient transfer processes for complex international payment requirements.

Ready to simplify your international payments? Get started with PayGlocal now!

Recent changes raised the TCS exemption limit from ₹7 lakh to ₹10 lakh per financial year. This means more room to send money abroad without an additional tax burden. However, once you cross this threshold, TCS rates can reach up to 20% depending on your remittance purpose.

In this guide, we will show you effective methods to avoid or minimize TCS on your foreign transfers. You'll learn timing strategies, purpose-based exemptions, and alternative payment routes that can result in significant savings.

Key Takeaways:

- Zero TCS for education loans: Education loans from recognized institutions attract zero TCS regardless of the amount.

- Planning Tips: Timing and family member distribution can help you stay below thresholds.

- Professional payment solutions: PayGlocal offers cost-effective international payment solutions with transparent pricing.

- Refundable advance tax: TCS is an advance tax; you can claim refunds when filing income tax returns.

What is TCS on foreign remittance?

TCS stands for Tax Collected at Source. Banks and authorized dealers collect this tax when you send money abroad under India's LRS (Liberalised Remittance Scheme) - a facility that allows resident individuals to freely remit up to USD 250,000 per financial year for various purposes.

The government introduced TCS to track foreign currency outflows and prevent tax evasion. When you make international transfers, your bank automatically deducts TCS and deposits it with the Income Tax Department.

For instance, if you send ₹12 lakh for education in a financial year, TCS applies only on ₹2 lakh (the amount above the ₹10 lakh threshold). The rate depends on your remittance purpose; education attracts 5% while investments face 20% TCS.

What is the difference between TCS and TDS on foreign remittances

TCS and TDS are two similar terms with distinct tax collection mechanisms and different applications for international transfers.

- TCS (Tax Collected at Source): It applies when you send money abroad under LRS. Your bank collects this tax and deposits it with the government. TCS rates depend on the remittance purpose and amount.

- TDS (Tax Deducted at Source): It applies when you receive foreign income in India. For instance, if a foreign client pays you for services, TDS may apply on that incoming payment.

Here's a quick comparison of TCS and TDS for international transactions:

Both TCS and TDS serve as advance tax payments that you can claim when filing returns.

What are the current TCS rules and thresholds for 2025?

The latest TCS framework became effective from April 1, 2025. Here's what changed and what you need to know:

New exemption threshold: No TCS applies on foreign remittances up to ₹10 lakh per financial year. This is an increase from the previous ₹7 lakh limit.

TCS calculation method: TCS applies only to amounts exceeding ₹10 lakh in a financial year, not on the entire remittance amount.

Here’s a quick overview of the current TCS rates for different remittance purposes:

How does the TCS calculation work?

TCS applies progressively, only on amounts above the ₹10 lakh threshold. Here are some examples:

1. Education remittance: You send ₹15 lakh for self-funded education. TCS applies on ₹5 lakh at 5% rate. Your TCS = ₹25,000.

2. Investment purpose: You transfer ₹12 lakh for foreign investments. TCS applies on ₹2 lakh at a 20% rate. Your TCS = ₹40,000.

3. Multiple purposes: You send ₹8 lakh for education and ₹4 lakh for travel in the same year. Total = ₹12 lakh. TCS applies on ₹2 lakh at respective rates.

Your bank tracks all foreign remittances linked to your PAN across the financial year. Once the cumulative amount exceeds ₹10 lakh, TCS is immediately applicable to subsequent transfers.

Looking for faster international payments with better exchange rates? PayGlocal helps businesses complete transfers faster with transparent pricing.

How to avoid TCS on foreign remittance while staying compliant?

Managing international payments without triggering excessive TCS requires strategic planning and a proper understanding of available exemptions. Multiple methods can help you minimize or completely avoid the TCS burden while staying compliant with regulations.

Here are some effective strategies that businesses and individuals can use to reduce TCS on foreign transfers:

1. Timing your remittances across financial years

Split large remittances across two financial years to stay within the ₹10 lakh annual limit. This requires careful planning but can save substantial TCS.

For instance, if you need to send ₹18 lakh for education, transfer ₹9 lakh in March and ₹9 lakh in April. This way, both transfers stay below the threshold.

Plan major expenses like education fees or property purchases well in advance. Contact your university or service provider to understand payment schedules and deadlines.

2. Using education loans from recognized institutions

Education loans from banks or NBFCs (Non-Banking Financial Companies) recognized under Section 80E of the Income Tax Act attract zero TCS. This applies regardless of the loan amount.

Even if you have personal funds available, taking an education loan can be cost-effective. The TCS savings often outweigh the loan interest costs.

Similarly, you can explore education financing options through foreign universities or specialized education loan providers. Ensure the lender qualifies under Income Tax regulations.

3. Distributing remittances among family members

Each individual gets a separate ₹10 lakh TCS exemption limit. Married couples can effectively transfer ₹20 lakh per year without TCS.

Your spouse, parents, or adult children can make separate remittances for legitimate purposes. However, ensure each person has genuine reasons for the transfer to avoid scrutiny.

This strategy works well for family maintenance, education expenses, or medical treatment abroad. Maintain proper documentation for each family member's remittance purpose.

4. Choosing the right remittance purpose

Different purposes attract different TCS rates. Medical treatment and self-funded education get preferential 5% rates above ₹10 lakh.

Always select the correct purpose code when filling out remittance forms. Wrong classification can lead to higher TCS rates and compliance issues.

For example, if you're paying for medical treatment abroad, don't classify it as "other purposes," which attracts 20% TCS. Proper documentation helps support your purpose declaration.

5. Leveraging NRI account benefits

NRI (Non-Resident Indian) accounts offer certain exemptions for family maintenance remittances. If you're an NRI, use these accounts for recurring transfers to avoid TCS.

NRO (Non-Resident Ordinary) account holders can send back up to USD 1 million per financial year for legitimate purposes. Some of these transfers can qualify for TCS exemptions.

This strategy works best, especially for established NRIs with regular income sources abroad. Consult your bank about specific NRI remittance benefits and forex management options.

6. Using international credit cards strategically

Foreign spending through international credit cards may avoid TCS for amounts up to ₹10 lakh annually. This works for education fees, travel expenses, or service payments.

However, credit card transactions still count toward your annual LRS limit. Plan accordingly if you have other foreign remittance needs.

Some payment processing methods offer better exchange rates and lower fees compared to traditional bank transfers.

Tired of high bank charges eating into your transfers? PayGlocal offers competitive rates with no hidden fees for international payments.

7. Planning tour package payments separately

Instead of booking complete tour packages that attract higher TCS rates, pay for flights, hotels, and activities separately through different vendors.

This approach can help you avoid the 5% TCS on tour packages up to ₹10 lakh and 20% beyond that limit. Book directly with airlines and hotels when possible.

Ensure your payment structure doesn't appear artificial or solely for tax avoidance purposes. Genuine business reasons should drive your payment choices.

TCS refund process and tax implications

TCS functions as advance tax payment, not an additional cost. You can claim TCS as credit against your final tax liability when filing income tax returns.

Here’s a step-by-step refund process:

- Obtain Form 27D: Collect this document from your bank showing TCS deducted on your remittances.

Verify TCS credit: Check Form 26AS or Annual Information Statement to confirm TCS amounts.

- Include in tax return: Add the TCS amount when filing your income tax return for that financial year.

- Claim refund: Request a refund if TCS exceeds your actual tax liability for the year.

- Receive a refund: Get a refund directly to your bank account after processing and verification.

It is essential to file your income tax return within the due date to claim TCS refunds. Late filings can complicate the refund process.

Maintain all remittance receipts and bank statements as supporting documents. The Income Tax Department may ask for verification during assessment proceedings.

What mistakes should you avoid when planning remittances?

Poor planning and incorrect documentation can lead to unnecessary TCS burden and compliance issues.

Here are the most frequent mistakes that cost businesses and individuals extra money on foreign remittances:

- Wrong purpose classification: Always select the correct remittance purpose to benefit from lower TCS rates. Misclassification can lead to higher taxes and compliance issues.

- Ignoring cumulative limits: Track your total foreign remittances throughout the financial year. Banks calculate TCS based on cumulative amounts, not individual transactions.

- Poor documentation: Maintain proper receipts, medical certificates, education admission letters, and other supporting documents for your remittance purpose.

- Last-minute planning: Plan large remittances well in advance. Rushed transfers leave little room for tax optimization strategies.

- Overlooking hidden costs: Consider exchange rate margins, bank charges, and intermediary fees along with TCS when comparing transfer options.

International payment processes made easy with PayGlocal

Managing international payments while dealing with TCS complexities can overwhelm growing businesses. Traditional banks often lack transparency in pricing and offer limited guidance on tax optimization strategies.

PayGlocal helps Indian businesses handle international payments with complete transparency and expert support. Here's how we make global transactions easier:

- Multi-currency accounts: Accept and manage payments in USD, GBP, EUR, and CAD with transparent pricing and instant settlement.

- Dynamic checkout: Offer your global customers a unified payment experience with multiple currency options and local payment methods.

- Global payment methods: Access 40+ international payment options, including cards, wallets, and bank transfers for worldwide reach.

- One platform management: Control all your international payments from a single dashboard with real-time tracking and reporting.

- Competitive pricing: Transparent fee structure with no hidden charges and volume-based discounts for growing businesses.

PayGlocal serves exporters, service providers, and businesses across India with reliable international payment solutions that save time and reduce costs.

Final thoughts

TCS on foreign remittances doesn't have to drain your international payment budget. The 2025 rule changes provide more flexibility with the increased ₹10 lakh exemption threshold, while education loans offer complete TCS exemption regardless of the amount.

Smart timing, proper purpose classification, and family member distribution can help you minimize TCS costs while staying compliant. Remember that TCS is an advance tax, not a permanent cost, so proper tax filing can recover excess amounts.

Plan your international payments strategically and maintain proper documentation for all transfers. Consider professional payment platforms like PayGlocal that offer transparent pricing and efficient transfer processes for complex international payment requirements.

Ready to simplify your international payments? Get started with PayGlocal now!