You closed the deal, sent the invoice, and delivered the work. But two weeks later, the payment still hasn't landed in your account. If you collect from international clients, you know how frustrating it is to wait with no visibility into the status of your funds.

B2B cross-border payment solutions are built to fix this issue. Nearly 87% of organizations today process payments globally as part of their regular operations. The ones collecting fastest use modern platforms that offer quicker settlements, lower fees, and real-time tracking.

This guide covers what B2B cross-border payment solutions are, how they work, and how to choose the right one for your business.

B2B cross-border payment solutions are platforms and services that help businesses send and receive payments across international borders. They handle the complexities of international payments.

These solutions include currency conversion, routing transactions through banking networks, meeting compliance requirements across different countries, and settling funds into your local bank account.

For instance, if you run an IT services company in India and your client in the US pays you in US dollars, a B2B cross-border payment solution processes that transaction, converts the currency, and deposits Indian rupees into your account.

Traditional bank wires can do this too, but they are often slow, expensive, and hard to track. Modern B2B cross-border payment solutions offer faster processing, lower fees, and real-time visibility into payment status.

International trade is growing, and so is the volume of cross-border B2B payments. If your business serves global clients, you need a reliable way to collect payments without delays eating into your cash flow.

Here’s why these solutions matter for your business

Tip: If you are spending more than a day each month chasing payment status updates or reconciling international transactions manually, a dedicated B2B payment solution will likely pay for itself quickly.

Cross-border B2B payments are part of daily operations for many businesses. The specific use case depends on your industry and business model, but the need for reliable international payment collection is common across all of them.

Here are the most common scenarios:

For example, a SaaS company in India billing clients in the US, UK, and Germany needs a system that handles USD, GBP, and EUR payments, applies the right compliance checks, and settles everything into one Indian bank account.

Every cross-border B2B payment follows a series of steps, even if the process looks instant from the outside. Knowing how it works helps you spot where delays and extra costs come from. Here’s the typical flow of a B2B cross-border payment.

1. Payment initiation: Your client starts the payment using their preferred method, such as a card, bank transfer, or online platform.

2. Currency conversion: If your client pays in their local currency and you receive in yours, the payment is converted at the current exchange rate. The rate and any markup depend on the provider.

3. Compliance and fraud checks: The transaction passes through fraud screening, sanctions checks, and other verifications. This happens on both the sending and receiving sides.

4. Routing through banking networks: The payment moves through one or more intermediary banks or payment networks to reach your country. Each intermediary can add time and cost.

5. Settlement into your account: Once the payment clears all checks and reaches your local bank, the funds are deposited in your account, usually in your local currency.

The number of intermediaries and the payment method both affect how fast and how expensive this process is. Modern payment platforms reduce the number of intermediaries, speeding things up and lowering costs.

Both B2B and B2C cross-border payments move money across borders, but they work differently in practice. Knowing the difference helps you pick the right solution for your business model. Here’s a side-by-side comparison.

B2B payments tend to involve more back-and-forth. You might send an invoice, wait for approval, and then receive payment weeks later. The amounts are larger, so the cost of currency conversion and intermediary fees hits harder.

B2C payments, on the other hand, happen at the point of sale. A customer buys something, pays instantly, and the merchant receives the funds after processing.

Tip: For businesses selling services or products to other businesses globally, B2B-specific solutions are a better fit because they handle invoicing workflows, larger transaction amounts, and the compliance documentation you need for cross-border trade.

There are several ways businesses pay each other across borders. Each method has different strengths, and the right choice depends on your transaction size, frequency, and where your clients are located.

Here’s a quick comparison of the most common methods:

Here’ss a closer look at each.

Bank wire transfers are the oldest method for international B2B payments. Your client sends money through their bank, and it travels through one or more correspondent banks before reaching yours. They are reliable for large amounts, but each bank in the chain can charge a fee, and the exchange rate markup adds up.

For example, a wire from a US bank to an Indian bank can involve two or three intermediary banks, each deducting a fee before the money reaches you.

Card payments are common for subscription-based businesses, SaaS platforms, and recurring billing. The payment is authorized almost instantly, and funds typically settle within one to three days. Processing fees usually range from two to three percent per transaction.

For instance, if you run a SaaS product with monthly subscriptions, card payments give your global clients a familiar and fast way to pay.

These are dedicated platforms built specifically for cross-border payment collection. They offer features like multi-currency accounts, local payment methods, automated compliance documents, and real-time tracking. They tend to have lower fees and faster settlements than traditional banks.

ACH (Automated Clearing House) is used in the US, and SEPA (Single Euro Payments Area) covers Europe. These are low-cost, bank-to-bank transfer systems that work well for regular payments from clients in those regions. They are cheaper than wire transfers but are limited to specific geographies.

Digital wallets like Apple Pay and similar services are growing in B2B payments, especially for smaller transaction amounts. They offer fast authorization and strong security through tokenization. They work best when your clients already use these wallets for business purchases.

Tip: You do not have to pick just one method. The best approach is often to offer multiple payment options so your clients can pay using whatever is most convenient for them.

Many businesses still rely on bank wire transfers for international collections simply because it is what they have always used. But the difference between traditional banking and modern payment platforms is significant.

Here’s how they compare on the factors that matter most:

The difference is most noticeable when you process payments regularly. A one-time large wire might work fine through your bank. But if you collect payments weekly or monthly from multiple countries, the manual effort, hidden fees, and lack of tracking add up fast.

For example, if you collect ten payments a month from five different countries through bank wires, you are likely spending hours on reconciliation and losing money on each transaction through intermediary fees and poor exchange rates. A dedicated platform handles all of that automatically.

Note: Switching from bank wires to a modern platform does not mean you stop using banks entirely. Most platforms settle into your existing bank account. The platform handles everything before that final settlement step.

Cross-border payments are more complex than domestic ones. Knowing the common challenges helps you choose the right solution and avoid costly surprises. Here are the most common issues worth considering:

Many payment providers charge fees that are not obvious upfront. These include intermediary bank charges, currency conversion markups, and processing fees that only show up on your statement. Over time, these hidden costs add up significantly.

For example, a bank wire that looks like a flat $25 fee can actually cost much more once intermediary bank deductions and FX markups are applied.

Traditional bank transfers can take three to five business days, and sometimes longer if the payment gets flagged for additional checks. For businesses that depend on steady cash flow, waiting days for each payment creates real operational problems.

Every time a payment involves currency conversion, someone is paying for it. The exchange rate you get depends on your provider, and the difference between the mid-market rate and the rate you actually receive is a direct cost to your business. Exchange rates also move between the time your client initiates the payment and when it settles, which means the final amount you receive can vary from what you expected.

With traditional banking channels, you often have no idea where your payment is between initiation and settlement. This lack of visibility makes it hard to follow up with clients and plan your finances.

International card payments fail more often than domestic ones. Different countries have different banking rules, card network policies, and fraud screening standards. When a payment fails, you lose revenue, and your client has a poor experience.

If your payment solution does not connect with your accounting software, invoicing tools, or ERP system, you end up doing manual data entry. This wastes time and increases the chance of errors.

Note: Most payment failures and delays are preventable. They usually come down to the provider's routing, compliance handling, and messaging to issuing banks.

Not all payment providers are the same, and the cheapest option is not always the best one. The right choice depends on your business size, where your clients are, and how often you collect payments.

Here are the key criteria that matter most:

Look for providers that show you the full cost upfront, including processing fees, currency conversion rates, and any monthly or setup charges. If the pricing page is hard to find or hard to read, that is usually a warning sign.

Check how many currencies the provider supports and which countries they cover. If most of your clients are in the US, UK, and EU, make sure the platform handles USD, GBP, and EUR well. If you sell globally, look for providers that support 30 or more currencies.

Ask how long it takes from when your client pays to when the money reaches your bank account. One to two business days is a good standard for modern platforms. Anything longer than that means your provider is not optimizing the process.

You should be able to see the status of every payment in real time. Good providers offer dashboards, notifications, and downloadable reports that make reconciliation easy.

Your provider should handle fraud screening, sanctions checks, and compliance documentation on your behalf. Look for end-to-end encryption, strong authentication, and automated compliance features like FIRC generation.

Check whether the platform offers APIs, plugins for popular e-commerce platforms, and no-code options. The easier it is to connect with your existing tools, the less manual work you will have.

Tip: Ask potential providers how they handle failed transactions. A good provider does not just report failures. They actively work to prevent them through smart routing and optimized transaction messaging.

The way businesses move money across borders is shifting fast. If you are choosing a payment provider today, it helps to know where the industry is heading so you pick a solution that won't become outdated in a year or two.

Here are the key shifts to watch:

The businesses that benefit most from these changes are the ones that choose providers already building on these trends, rather than adding them as afterthoughts.

Managing international B2B payments across multiple currencies, countries, and payment methods can get complicated fast. Failed transactions, slow settlements, and poor visibility into payment status cost you revenue and client trust.

PayGlocal is built for businesses that collect payments from global clients. It brings together everything you need in one platform. Here is what PayGlocal offers.

Stop chasing banks and start scaling. PayGlocal removes the red tape from global collections, giving you the high approval rates and transparent pricing your business deserves. Join the fastest-growing exporters who have already fixed their payment flow.

B2B cross-border payment solutions are no longer optional if your business serves international clients. The right platform gives you faster settlements, lower costs, better tracking, and higher payment success rates. The wrong one costs you revenue and client relationships every month.

Start by mapping your biggest challenges, whether it is speed, cost, visibility, or failed payments, and then evaluate providers against the key criteria like pricing transparency, settlement speed, and security.

Businesses that act on this early gain a real advantage in how fast they grow internationally. Ready to simplify your global payment collection? Get started with PayGlocal today.

B2B cross-border payment solutions are built to fix this issue. Nearly 87% of organizations today process payments globally as part of their regular operations. The ones collecting fastest use modern platforms that offer quicker settlements, lower fees, and real-time tracking.

This guide covers what B2B cross-border payment solutions are, how they work, and how to choose the right one for your business.

Key takeaways

- Multiple moving parts: B2B cross-border payments involve currency conversion, compliance checks, and intermediary banks, all adding time and cost.

- Modern platforms are faster: Online payment solutions offer quicker settlements, lower fees, and real-time tracking compared to traditional bank wires.

- Payment method choice matters: Wire transfers, cards, and digital platforms each work best for different transaction types and client locations.

- PayGlocal simplifies global collections: It brings multi-currency accounts, card processing, and 40+ local payment methods into one platform for Indian businesses.

- Key factors defining the right provider: Fee transparency, currency coverage, settlement speed, tracking, security, and integration with your existing tools.

What are B2B cross-border payment solutions?

B2B cross-border payment solutions are platforms and services that help businesses send and receive payments across international borders. They handle the complexities of international payments.

These solutions include currency conversion, routing transactions through banking networks, meeting compliance requirements across different countries, and settling funds into your local bank account.

For instance, if you run an IT services company in India and your client in the US pays you in US dollars, a B2B cross-border payment solution processes that transaction, converts the currency, and deposits Indian rupees into your account.

Traditional bank wires can do this too, but they are often slow, expensive, and hard to track. Modern B2B cross-border payment solutions offer faster processing, lower fees, and real-time visibility into payment status.

Why do businesses need B2B cross-border payment solutions?

International trade is growing, and so is the volume of cross-border B2B payments. If your business serves global clients, you need a reliable way to collect payments without delays eating into your cash flow.

Here’s why these solutions matter for your business

- Faster access to funds: Traditional wire transfers can take three to five business days or longer. Modern solutions often settle within one to two days.

- Lower transaction costs: Bank-to-bank international transfers involve multiple intermediaries, each adding fees. Payment platforms reduce or remove many of these charges.

- Better cash flow planning: When you know exactly when payments will arrive, you can plan expenses, payroll, and growth with more confidence.

- Wider customer reach: Accepting multiple currencies and local payment methods makes it easier for international clients to pay you.

- Less manual work: Automated invoicing, payment tracking, and compliance documentation save hours of back-office effort each week.

Tip: If you are spending more than a day each month chasing payment status updates or reconciling international transactions manually, a dedicated B2B payment solution will likely pay for itself quickly.

When do businesses use B2B cross-border payments?

Cross-border B2B payments are part of daily operations for many businesses. The specific use case depends on your industry and business model, but the need for reliable international payment collection is common across all of them.

Here are the most common scenarios:

- Collecting from global clients for exported goods or services: If you export products or deliver services to clients in other countries, you need a way to receive payments in their currency and settle in yours.

- Billing international customers for SaaS subscriptions: Software companies with global users need recurring payment collection across multiple currencies and card networks.

- Receiving marketplace payouts: If you sell through international marketplaces, your payouts often come in foreign currencies and need to be settled into your Indian bank account.

- Getting paid by global freelance platforms: Freelancers and independent professionals working with international clients or platforms need fast, low-cost ways to receive their earnings.

- Settling payments between group companies: Businesses with offices or subsidiaries in different countries regularly move funds between entities for operations, salaries, or vendor payments.

For example, a SaaS company in India billing clients in the US, UK, and Germany needs a system that handles USD, GBP, and EUR payments, applies the right compliance checks, and settles everything into one Indian bank account.

How do B2B cross-border payments work?

Every cross-border B2B payment follows a series of steps, even if the process looks instant from the outside. Knowing how it works helps you spot where delays and extra costs come from. Here’s the typical flow of a B2B cross-border payment.

1. Payment initiation: Your client starts the payment using their preferred method, such as a card, bank transfer, or online platform.

2. Currency conversion: If your client pays in their local currency and you receive in yours, the payment is converted at the current exchange rate. The rate and any markup depend on the provider.

3. Compliance and fraud checks: The transaction passes through fraud screening, sanctions checks, and other verifications. This happens on both the sending and receiving sides.

4. Routing through banking networks: The payment moves through one or more intermediary banks or payment networks to reach your country. Each intermediary can add time and cost.

5. Settlement into your account: Once the payment clears all checks and reaches your local bank, the funds are deposited in your account, usually in your local currency.

The number of intermediaries and the payment method both affect how fast and how expensive this process is. Modern payment platforms reduce the number of intermediaries, speeding things up and lowering costs.

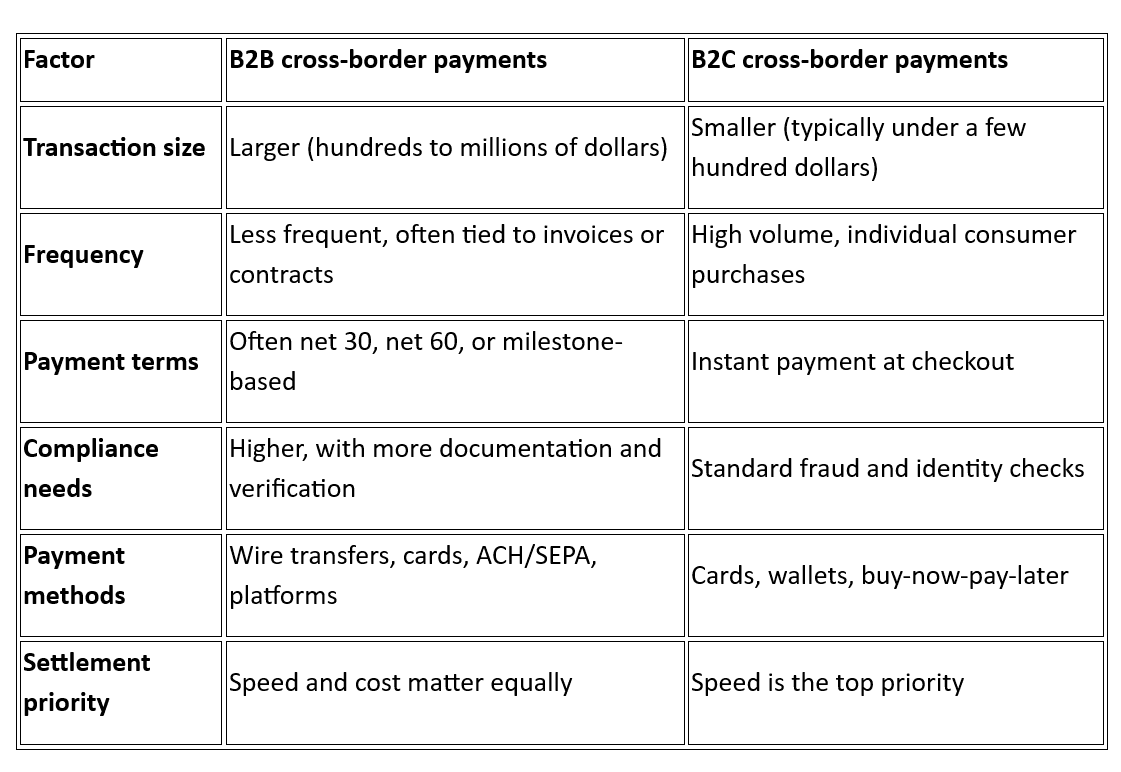

What is the difference between B2B and B2C cross-border payments?

Both B2B and B2C cross-border payments move money across borders, but they work differently in practice. Knowing the difference helps you pick the right solution for your business model. Here’s a side-by-side comparison.

B2B payments tend to involve more back-and-forth. You might send an invoice, wait for approval, and then receive payment weeks later. The amounts are larger, so the cost of currency conversion and intermediary fees hits harder.

B2C payments, on the other hand, happen at the point of sale. A customer buys something, pays instantly, and the merchant receives the funds after processing.

Tip: For businesses selling services or products to other businesses globally, B2B-specific solutions are a better fit because they handle invoicing workflows, larger transaction amounts, and the compliance documentation you need for cross-border trade.

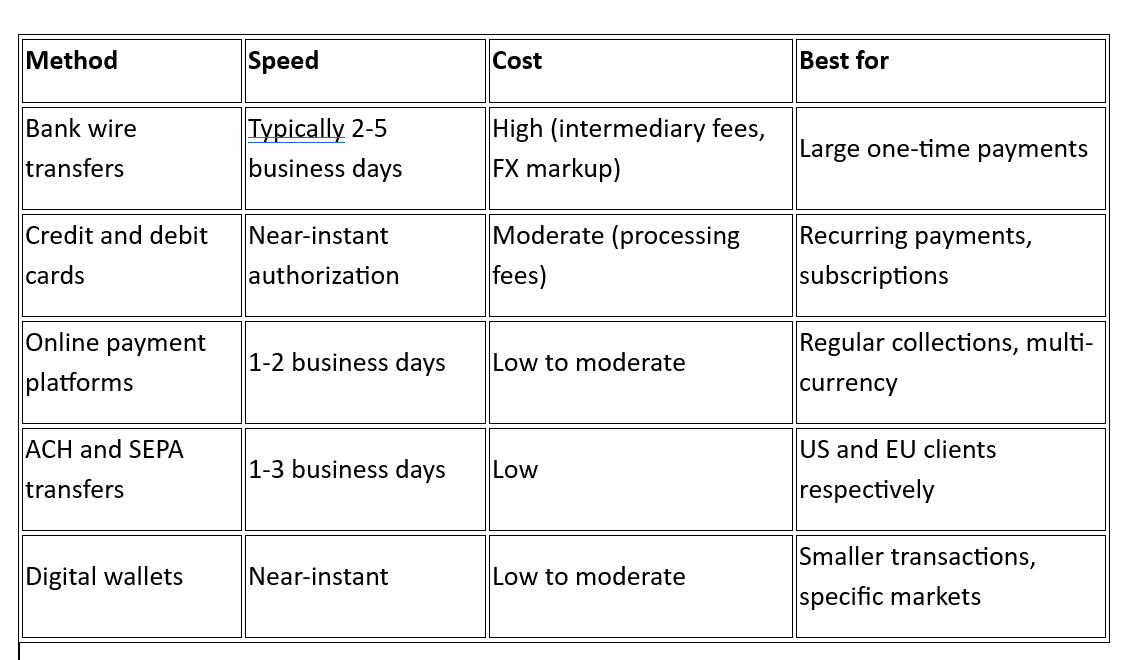

What are the common methods for B2B cross-border payments?

There are several ways businesses pay each other across borders. Each method has different strengths, and the right choice depends on your transaction size, frequency, and where your clients are located.

Here’s a quick comparison of the most common methods:

Here’ss a closer look at each.

1. Bank wire transfers

Bank wire transfers are the oldest method for international B2B payments. Your client sends money through their bank, and it travels through one or more correspondent banks before reaching yours. They are reliable for large amounts, but each bank in the chain can charge a fee, and the exchange rate markup adds up.

For example, a wire from a US bank to an Indian bank can involve two or three intermediary banks, each deducting a fee before the money reaches you.

2. Credit and debit card payments

Card payments are common for subscription-based businesses, SaaS platforms, and recurring billing. The payment is authorized almost instantly, and funds typically settle within one to three days. Processing fees usually range from two to three percent per transaction.

For instance, if you run a SaaS product with monthly subscriptions, card payments give your global clients a familiar and fast way to pay.

3. Online payment platforms

These are dedicated platforms built specifically for cross-border payment collection. They offer features like multi-currency accounts, local payment methods, automated compliance documents, and real-time tracking. They tend to have lower fees and faster settlements than traditional banks.

4. ACH and SEPA transfers

ACH (Automated Clearing House) is used in the US, and SEPA (Single Euro Payments Area) covers Europe. These are low-cost, bank-to-bank transfer systems that work well for regular payments from clients in those regions. They are cheaper than wire transfers but are limited to specific geographies.

5. Digital wallets

Digital wallets like Apple Pay and similar services are growing in B2B payments, especially for smaller transaction amounts. They offer fast authorization and strong security through tokenization. They work best when your clients already use these wallets for business purchases.

Tip: You do not have to pick just one method. The best approach is often to offer multiple payment options so your clients can pay using whatever is most convenient for them.

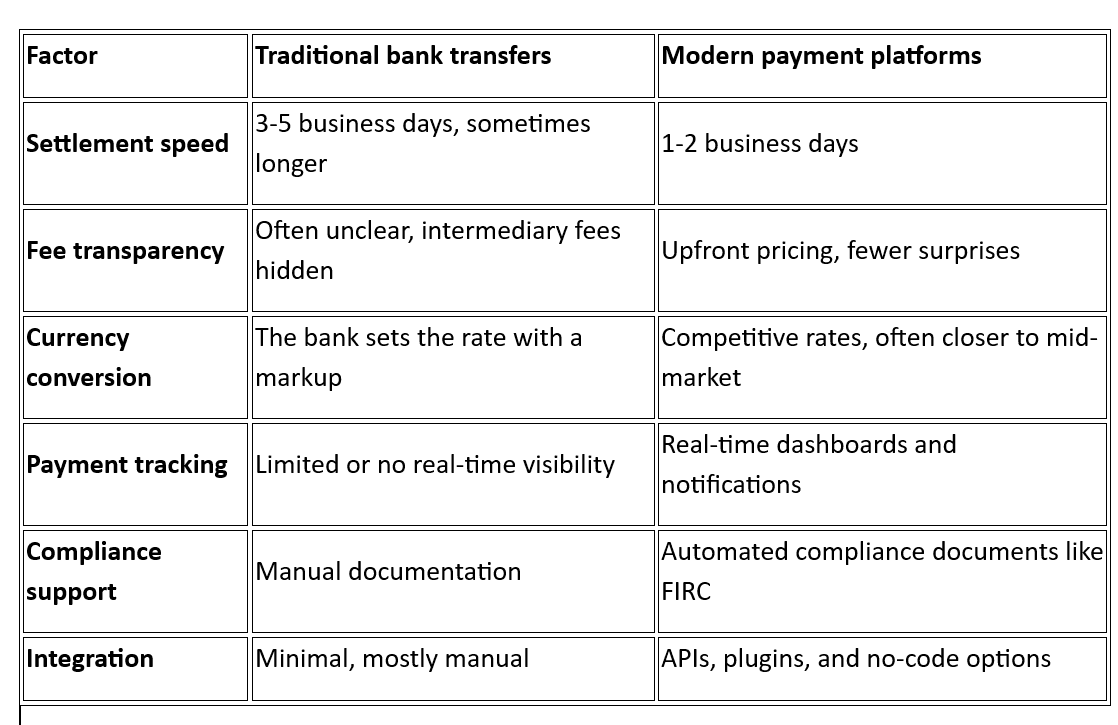

How do modern B2B payment solutions compare to traditional bank transfers?

Many businesses still rely on bank wire transfers for international collections simply because it is what they have always used. But the difference between traditional banking and modern payment platforms is significant.

Here’s how they compare on the factors that matter most:

The difference is most noticeable when you process payments regularly. A one-time large wire might work fine through your bank. But if you collect payments weekly or monthly from multiple countries, the manual effort, hidden fees, and lack of tracking add up fast.

For example, if you collect ten payments a month from five different countries through bank wires, you are likely spending hours on reconciliation and losing money on each transaction through intermediary fees and poor exchange rates. A dedicated platform handles all of that automatically.

Note: Switching from bank wires to a modern platform does not mean you stop using banks entirely. Most platforms settle into your existing bank account. The platform handles everything before that final settlement step.

What challenges do businesses face with B2B cross-border payments?

Cross-border payments are more complex than domestic ones. Knowing the common challenges helps you choose the right solution and avoid costly surprises. Here are the most common issues worth considering:

1. High and hidden fees

Many payment providers charge fees that are not obvious upfront. These include intermediary bank charges, currency conversion markups, and processing fees that only show up on your statement. Over time, these hidden costs add up significantly.

For example, a bank wire that looks like a flat $25 fee can actually cost much more once intermediary bank deductions and FX markups are applied.

2. Slow settlement times

Traditional bank transfers can take three to five business days, and sometimes longer if the payment gets flagged for additional checks. For businesses that depend on steady cash flow, waiting days for each payment creates real operational problems.

3. Currency conversion costs

Every time a payment involves currency conversion, someone is paying for it. The exchange rate you get depends on your provider, and the difference between the mid-market rate and the rate you actually receive is a direct cost to your business. Exchange rates also move between the time your client initiates the payment and when it settles, which means the final amount you receive can vary from what you expected.

4. Limited payment tracking

With traditional banking channels, you often have no idea where your payment is between initiation and settlement. This lack of visibility makes it hard to follow up with clients and plan your finances.

5. Failed transactions and declines

International card payments fail more often than domestic ones. Different countries have different banking rules, card network policies, and fraud screening standards. When a payment fails, you lose revenue, and your client has a poor experience.

6. Integration with existing systems

If your payment solution does not connect with your accounting software, invoicing tools, or ERP system, you end up doing manual data entry. This wastes time and increases the chance of errors.

Note: Most payment failures and delays are preventable. They usually come down to the provider's routing, compliance handling, and messaging to issuing banks.

How to choose the right B2B cross-border payment provider?

Not all payment providers are the same, and the cheapest option is not always the best one. The right choice depends on your business size, where your clients are, and how often you collect payments.

Here are the key criteria that matter most:

1. Fee transparency

Look for providers that show you the full cost upfront, including processing fees, currency conversion rates, and any monthly or setup charges. If the pricing page is hard to find or hard to read, that is usually a warning sign.

2. Currency and country coverage

Check how many currencies the provider supports and which countries they cover. If most of your clients are in the US, UK, and EU, make sure the platform handles USD, GBP, and EUR well. If you sell globally, look for providers that support 30 or more currencies.

3. Settlement speed

Ask how long it takes from when your client pays to when the money reaches your bank account. One to two business days is a good standard for modern platforms. Anything longer than that means your provider is not optimizing the process.

4. Payment tracking and reporting

You should be able to see the status of every payment in real time. Good providers offer dashboards, notifications, and downloadable reports that make reconciliation easy.

5. Security and compliance

Your provider should handle fraud screening, sanctions checks, and compliance documentation on your behalf. Look for end-to-end encryption, strong authentication, and automated compliance features like FIRC generation.

6. Integration options

Check whether the platform offers APIs, plugins for popular e-commerce platforms, and no-code options. The easier it is to connect with your existing tools, the less manual work you will have.

Tip: Ask potential providers how they handle failed transactions. A good provider does not just report failures. They actively work to prevent them through smart routing and optimized transaction messaging.

What is changing in B2B cross-border payments?

The way businesses move money across borders is shifting fast. If you are choosing a payment provider today, it helps to know where the industry is heading so you pick a solution that won't become outdated in a year or two.

Here are the key shifts to watch:

- API-first platforms: Modern providers offer APIs that connect directly to your website or apps. This removes manual steps and makes payment collection part of your existing workflow.

- Real-time payment networks: Countries are building faster domestic payment rails, and these networks are starting to connect across borders. This means settlement times will keep getting shorter.

- Local payment method adoption: More businesses are offering region-specific payment methods alongside cards. Accepting the payment methods your clients already trust leads to higher success rates and fewer abandoned checkouts.

- AI-powered fraud screening: Newer platforms use machine learning to screen transactions in real time. This catches fraudulent payments without blocking genuine ones, which directly improves your approval rates.

- Embedded payments: Payment functionality is being built directly into business software like accounting tools, invoicing platforms, and e-commerce systems. This reduces the need to switch between tools and keeps everything in one place.

The businesses that benefit most from these changes are the ones that choose providers already building on these trends, rather than adding them as afterthoughts.

Accept global B2B payments with confidence using PayGlocal

Managing international B2B payments across multiple currencies, countries, and payment methods can get complicated fast. Failed transactions, slow settlements, and poor visibility into payment status cost you revenue and client trust.

PayGlocal is built for businesses that collect payments from global clients. It brings together everything you need in one platform. Here is what PayGlocal offers.

- Multi-currency accounts: Collect payments locally in USD, GBP, EUR, CAD, AUD, and globally in 33+ currencies from 180+ countries.

- Card payments: Accept international credit and debit cards with optimized approval rates through smart routing and enhanced issuer messaging.

- Global payment methods: Offer 40+ local payment methods so your clients can pay using what they already trust.

- Recurring payments: Set up subscriptions and recurring billing on international cards with network-compliant standing instructions.

- Dynamic checkout: Give your global clients a seamless, localized checkout experience that improves conversion rates.

Stop chasing banks and start scaling. PayGlocal removes the red tape from global collections, giving you the high approval rates and transparent pricing your business deserves. Join the fastest-growing exporters who have already fixed their payment flow.

Final thoughts

B2B cross-border payment solutions are no longer optional if your business serves international clients. The right platform gives you faster settlements, lower costs, better tracking, and higher payment success rates. The wrong one costs you revenue and client relationships every month.

Start by mapping your biggest challenges, whether it is speed, cost, visibility, or failed payments, and then evaluate providers against the key criteria like pricing transparency, settlement speed, and security.

Businesses that act on this early gain a real advantage in how fast they grow internationally. Ready to simplify your global payment collection? Get started with PayGlocal today.