Electronic payments are rapidly growing in India. According to recent data, around 48.5% of the worldwide real-time payments happen from India alone (which is almost half of the entire global real-time payments).

In fact, the volume of digital transactions in India is expected to grow nearly seven times, reaching up to 210 billion by 2026, from just 35 billion in 2021.

But are electronic payment systems really worth implementing for your business? What are their advantages?

In this guide, we break down the top 12 benefits of electronic payment systems in detail, along with challenges, and tips to choose the right solution for your business needs. Let’s get started.

An electronic payment system processes financial transactions digitally without physical cash or paper cheque. These systems use computer networks, mobile devices, and internet connections to transfer money between parties instantly or near-instantly.

Common examples include credit card terminals at retail stores, online payment gateways for e-commerce, mobile wallet apps like Apple Pay, and bank transfer systems like UPI (Unified Payments Interface) in India. The key feature is the digital processing of payment instruments, rather than manual handling of physical ones.

Electronic systems work through secure networks that encrypt transaction data, verify account information, and transfer funds between financial institutions. This happens automatically without human intervention once the payment is initiated.

Electronic payment processing follows a standardized flow that ensures security and accuracy. The process involves multiple parties working together to complete transactions safely. Here's how the system operates:

Electronic payment systems come in various forms, each designed for specific use cases and customer preferences. Modern businesses benefit from offering multiple options to cater to diverse customer needs.

Let’s take a detailed look at some of the main types of electronic payment systems:

Credit and debit cards remain the most widely accepted electronic payment method globally. Card processors handle transactions through established networks that connect merchants, banks, and customers worldwide.

Modern card systems support contactless payments, recurring billing, and international transactions with automatic currency conversion. For example, a restaurant can accept payments from tourists using foreign cards without worrying about currency exchange rates.

* Bank transfer systems:

Direct bank-to-bank transfers include wire transfers, ACH (Automated Clearing House) payments, and country-specific systems like UPI in India or SEPA (Single Euro Payments Area) in Europe. These methods typically offer lower transaction fees but can take longer to process.

For instance, international wire transfers can take 3-5 business days, while domestic systems often settle same-day. A software company receiving payment from enterprise clients often prefers bank transfers for large invoice amounts.

Digital wallets store payment information securely on smartphones and enable quick transactions through apps or contactless terminals. Popular options include Apple Pay, Google Pay, and regional solutions like Paytm.

Mobile wallets often integrate loyalty programs and offer additional features beyond basic payments. For example, a coffee shop can process payments and automatically apply loyalty points through a single mobile wallet transaction.

Internet banking allows customers to initiate payments directly from their bank accounts through secure web portals or mobile apps. This method works well for recurring payments like subscriptions or utility bills.

For instance, a SaaS (Software as a Service) company can set up automatic monthly charges through customers' online banking systems, reducing payment failure rates.

Electronic payment systems deliver measurable advantages that directly impact business performance and customer satisfaction. These benefits compound over time as businesses scale their operations.

* Speed and efficiency gains:

Electronic payments process instantly or within minutes, compared to days or weeks for traditional methods. This speed advantage affects cash flow positively. Businesses receive funds faster and can reinvest in operations sooner.

For example, a consulting firm receiving payment via electronic transfer can access funds the same day rather than waiting for a cheque to clear. Small businesses particularly benefit from this quick access to working capital.

Transaction fees for electronic payments often cost less than processing a paper cheque or handling cash. Electronic payment processing typically costs 2% to 3.5% per transaction, while cheque processing can cost more, especially when considering bank fees, postage, and staff time.

For example, in an office processing 200 customer payments monthly, electronic payments could save significant amounts every month in combined fees and labor costs. Administrative costs drop significantly when payments are processed automatically.

Electronic systems use encryption, tokenization, and real-time fraud monitoring to protect transactions. These security layers provide better protection than physical cash or cheques.

Payment processors also maintain compliance with industry standards like PCI DSS (Payment Card Industry Data Security Standard) to ensure data protection. For example, card transactions can be monitored and blocked instantly when suspicious activity is detected, while lost cash provides no recovery options.

Electronic payments enable businesses to accept payments from customers worldwide without setting up local banking relationships in each country. This capability opens new revenue streams and customer segments that were previously inaccessible due to payment barriers.

For instance, a web design agency can easily accept payments from clients in Europe, Asia, and the Americas using the same payment system.

Digital transactions automatically generate detailed records with timestamps, amounts, customer information, and tax data. This automation reduces manual bookkeeping errors and simplifies tax preparation, compliance reporting, and financial analysis.

For example, an e-commerce store can instantly generate sales reports by product, customer location, or time period without manual data entry.

Customers prefer payment methods that are convenient, fast, and secure. Electronic options meet these expectations while offering features like saved payment information, subscription management, and mobile-friendly checkout processes.

For instance, returning customers can complete purchases with one-click payments, eliminating the need to re-enter card details each time.

Electronic systems automatically verify payment amounts, account numbers, and other transaction details, significantly reducing human errors common with manual processing.

For example, automated systems prevent issues like transposed numbers or incorrect amounts that often occur with handwritten cheques or cash counting.

Unlike traditional banking hours, electronic payment systems operate 24/7, allowing businesses to collect payments at any time. This is particularly valuable for online businesses serving customers across different time zones.

For instance, a digital course provider can receive payments from students worldwide regardless of local banking hours.

Electronic payments create detailed transaction trails that speed up dispute resolution and chargeback processes. Banks and payment processors can quickly access transaction history, making it easier to resolve customer complaints.

For example, when a customer disputes a charge, the merchant can provide instant transaction details rather than searching through paper records.

Electronic payment systems integrate with accounting software to automatically match payments with invoices, reducing manual reconciliation work. This feature saves significant time for finance teams.

For instance, a subscription business can automatically mark invoices as paid when electronic payments are received.

Electronic systems excel at handling subscription payments, installment plans, and other recurring billing scenarios. This capability is essential for SaaS companies, membership sites, and service providers.

For example, a gym can automatically charge monthly membership fees without requiring customers to remember payment dates.

Digital payments reduce paper usage from cheques, receipts, and manual records, supporting sustainability goals. Many customers appreciate businesses that offer paperless payment options.

For instance, a company can reduce printing costs and environmental impact by encouraging electronic bill payments.

The comparison between electronic and traditional payment methods shows significant differences in efficiency, cost, and capability. Here’s how they compare:

Despite clear advantages, electronic payment adoption involves overcoming specific challenges that vary by business size and industry. Smart implementation strategies address these concerns effectively.

Businesses need compatible software, hardware, and internet connectivity to process electronic payments. This requirement can seem daunting for traditional businesses or those with limited technical resources. However, modern payment solutions offer plug-and-play options that minimize technical barriers.

Electronic payments involve percentage-based fees that can add up for high-volume businesses. Companies must balance these costs against the benefits of faster processing, improved cash flow, and reduced manual handling expenses.

Accepting electronic payments requires maintaining security standards and compliance with regulations like PCI DSS. While this adds responsibility, payment service providers typically handle most compliance requirements, reducing the burden on individual businesses.

Some customer segments prefer traditional payment methods due to familiarity or concerns about security. Businesses address this by offering multiple payment options while encouraging the adoption of electronic methods through incentives or improved user experience.

Electronic payments require reliable internet connectivity, which can be challenging in areas with poor network coverage. Businesses can address this with backup connectivity options like mobile hotspots or offline-capable payment terminals that store transactions until connection is restored.

Electronic payment technology continues to advance rapidly, with new innovations reshaping how businesses and consumers handle transactions. The payment industry is moving toward more integrated, smart, and user-friendly solutions that adapt to changing consumer behaviors and business needs:

Selecting an appropriate payment system requires evaluating business needs, customer preferences, and growth plans to ensure a suitable solution. The right choice balances functionality, cost, and ease of implementation.

*- Review security and compliance: Ensure chosen providers maintain appropriate security certifications, offer fraud protection, and handle compliance requirements. This protects both business and customer data while reducing liability risks.

Traditional payment systems work for local transactions, but they create barriers when businesses expand internationally. Managing multiple currencies, handling different banking systems, and ensuring payment acceptance across diverse markets requires specialized solutions.'=

PayGlocal removes these complexities by providing a complete international payment platform designed specifically for businesses targeting global markets.

Here’s how PayGlocal supports your international payment processes:

PayGlocal provides businesses with a complete payment infrastructure needed for scaling globally with a fast, reliable, and secure payment solution.

Electronic payment systems have evolved from convenience features to business necessities. Some of the main benefits of electronic payment systems include faster processing, lower costs, enhanced security, and global reach, directly impacting business growth and customer satisfaction.

Smart businesses use electronic payments strategically, choosing solutions that match their current needs while supporting future expansion. PayGlocal offers all the tools and solutions you need to manage your international payment processes.

Ready to enhance your payment processes and expand globally? Get started with PayGlocal today.

In fact, the volume of digital transactions in India is expected to grow nearly seven times, reaching up to 210 billion by 2026, from just 35 billion in 2021.

But are electronic payment systems really worth implementing for your business? What are their advantages?

In this guide, we break down the top 12 benefits of electronic payment systems in detail, along with challenges, and tips to choose the right solution for your business needs. Let’s get started.

Key Takeaways:

- Cost reduction: Electronic payments cut transaction fees, reduce cheque processing costs, and lower manual labor expenses.

- Speed advantage: Instant processing means faster cash flow and quicker access to funds compared to traditional methods.

- Global reach: PayGlocal and similar platforms enable businesses to collect payments in 33+ currencies from 180+ countries seamlessly.

- Process efficiency: Automated record-keeping, real-time tracking, and integrated accounting improve business processes.

What is an electronic payment system?

An electronic payment system processes financial transactions digitally without physical cash or paper cheque. These systems use computer networks, mobile devices, and internet connections to transfer money between parties instantly or near-instantly.

Common examples include credit card terminals at retail stores, online payment gateways for e-commerce, mobile wallet apps like Apple Pay, and bank transfer systems like UPI (Unified Payments Interface) in India. The key feature is the digital processing of payment instruments, rather than manual handling of physical ones.

Electronic systems work through secure networks that encrypt transaction data, verify account information, and transfer funds between financial institutions. This happens automatically without human intervention once the payment is initiated.

How do electronic payment systems work?

Electronic payment processing follows a standardized flow that ensures security and accuracy. The process involves multiple parties working together to complete transactions safely. Here's how the system operates:

- Payment initiation: Customer enters payment details through a website, mobile app, or card terminal. The system captures encrypted transaction data, including amount, merchant information, and payment method.

- Authentication and authorization: The payment processor verifies the customer's account balance or credit limit with the issuing bank to ensure the transaction is authorized. Security checks run automatically to detect any suspicious activity.

- Transaction routing: The system routes the payment request through appropriate networks like Visa or Mastercard for card payments, or banking networks for direct transfers.

- Approval or decline: The issuing bank approves or declines the transaction based on available funds, account status, and risk assessment. This response travels back through the network to the merchant.

- Settlement and confirmation: Approved transactions trigger a fund transfer from the customer's account to the merchant's account. Both parties receive confirmation notices, and the transaction appears in account statements.

What are the main types of electronic payment systems?

Electronic payment systems come in various forms, each designed for specific use cases and customer preferences. Modern businesses benefit from offering multiple options to cater to diverse customer needs.

Let’s take a detailed look at some of the main types of electronic payment systems:

- Card-based payments:

Credit and debit cards remain the most widely accepted electronic payment method globally. Card processors handle transactions through established networks that connect merchants, banks, and customers worldwide.

Modern card systems support contactless payments, recurring billing, and international transactions with automatic currency conversion. For example, a restaurant can accept payments from tourists using foreign cards without worrying about currency exchange rates.

* Bank transfer systems:

Direct bank-to-bank transfers include wire transfers, ACH (Automated Clearing House) payments, and country-specific systems like UPI in India or SEPA (Single Euro Payments Area) in Europe. These methods typically offer lower transaction fees but can take longer to process.

For instance, international wire transfers can take 3-5 business days, while domestic systems often settle same-day. A software company receiving payment from enterprise clients often prefers bank transfers for large invoice amounts.

- Mobile wallet solutions:

Digital wallets store payment information securely on smartphones and enable quick transactions through apps or contactless terminals. Popular options include Apple Pay, Google Pay, and regional solutions like Paytm.

Mobile wallets often integrate loyalty programs and offer additional features beyond basic payments. For example, a coffee shop can process payments and automatically apply loyalty points through a single mobile wallet transaction.

- Online banking platforms:

Internet banking allows customers to initiate payments directly from their bank accounts through secure web portals or mobile apps. This method works well for recurring payments like subscriptions or utility bills.

For instance, a SaaS (Software as a Service) company can set up automatic monthly charges through customers' online banking systems, reducing payment failure rates.

What are the key benefits of electronic payment systems?

Electronic payment systems deliver measurable advantages that directly impact business performance and customer satisfaction. These benefits compound over time as businesses scale their operations.

* Speed and efficiency gains:

Electronic payments process instantly or within minutes, compared to days or weeks for traditional methods. This speed advantage affects cash flow positively. Businesses receive funds faster and can reinvest in operations sooner.

For example, a consulting firm receiving payment via electronic transfer can access funds the same day rather than waiting for a cheque to clear. Small businesses particularly benefit from this quick access to working capital.

- Significant cost reductions:

Transaction fees for electronic payments often cost less than processing a paper cheque or handling cash. Electronic payment processing typically costs 2% to 3.5% per transaction, while cheque processing can cost more, especially when considering bank fees, postage, and staff time.

For example, in an office processing 200 customer payments monthly, electronic payments could save significant amounts every month in combined fees and labor costs. Administrative costs drop significantly when payments are processed automatically.

- Enhanced security measures:

Electronic systems use encryption, tokenization, and real-time fraud monitoring to protect transactions. These security layers provide better protection than physical cash or cheques.

Payment processors also maintain compliance with industry standards like PCI DSS (Payment Card Industry Data Security Standard) to ensure data protection. For example, card transactions can be monitored and blocked instantly when suspicious activity is detected, while lost cash provides no recovery options.

- Global market access:

Electronic payments enable businesses to accept payments from customers worldwide without setting up local banking relationships in each country. This capability opens new revenue streams and customer segments that were previously inaccessible due to payment barriers.

For instance, a web design agency can easily accept payments from clients in Europe, Asia, and the Americas using the same payment system.

- Improved record keeping:

Digital transactions automatically generate detailed records with timestamps, amounts, customer information, and tax data. This automation reduces manual bookkeeping errors and simplifies tax preparation, compliance reporting, and financial analysis.

For example, an e-commerce store can instantly generate sales reports by product, customer location, or time period without manual data entry.

- Better customer experience:

Customers prefer payment methods that are convenient, fast, and secure. Electronic options meet these expectations while offering features like saved payment information, subscription management, and mobile-friendly checkout processes.

For instance, returning customers can complete purchases with one-click payments, eliminating the need to re-enter card details each time.

- Reduced transaction errors:

Electronic systems automatically verify payment amounts, account numbers, and other transaction details, significantly reducing human errors common with manual processing.

For example, automated systems prevent issues like transposed numbers or incorrect amounts that often occur with handwritten cheques or cash counting.

- 24/7 availability:

Unlike traditional banking hours, electronic payment systems operate 24/7, allowing businesses to collect payments at any time. This is particularly valuable for online businesses serving customers across different time zones.

For instance, a digital course provider can receive payments from students worldwide regardless of local banking hours.

- Faster dispute resolution:

Electronic payments create detailed transaction trails that speed up dispute resolution and chargeback processes. Banks and payment processors can quickly access transaction history, making it easier to resolve customer complaints.

For example, when a customer disputes a charge, the merchant can provide instant transaction details rather than searching through paper records.

- Automatic record matching:

Electronic payment systems integrate with accounting software to automatically match payments with invoices, reducing manual reconciliation work. This feature saves significant time for finance teams.

For instance, a subscription business can automatically mark invoices as paid when electronic payments are received.

- Support for recurring revenue:

Electronic systems excel at handling subscription payments, installment plans, and other recurring billing scenarios. This capability is essential for SaaS companies, membership sites, and service providers.

For example, a gym can automatically charge monthly membership fees without requiring customers to remember payment dates.

- Environmental benefits:

Digital payments reduce paper usage from cheques, receipts, and manual records, supporting sustainability goals. Many customers appreciate businesses that offer paperless payment options.

For instance, a company can reduce printing costs and environmental impact by encouraging electronic bill payments.

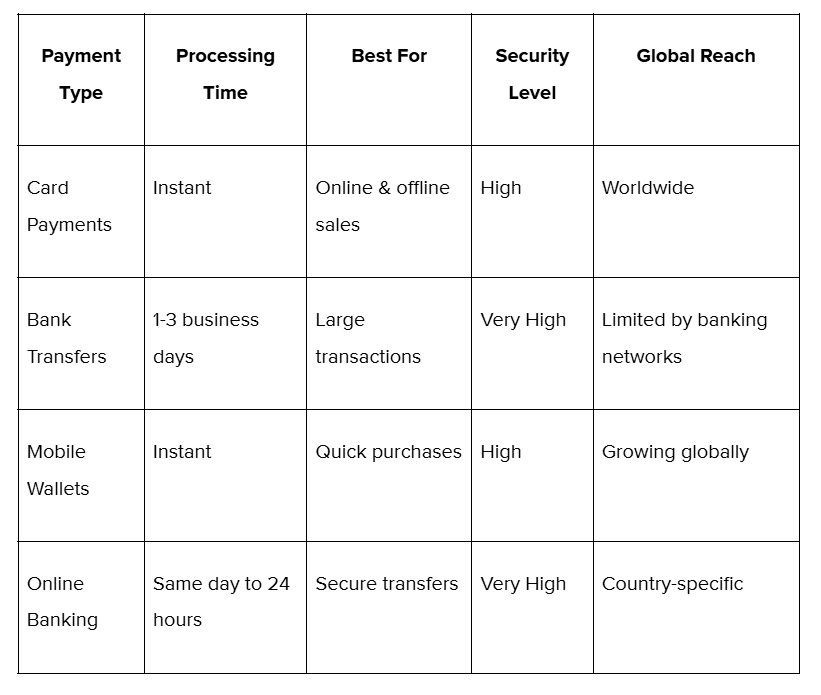

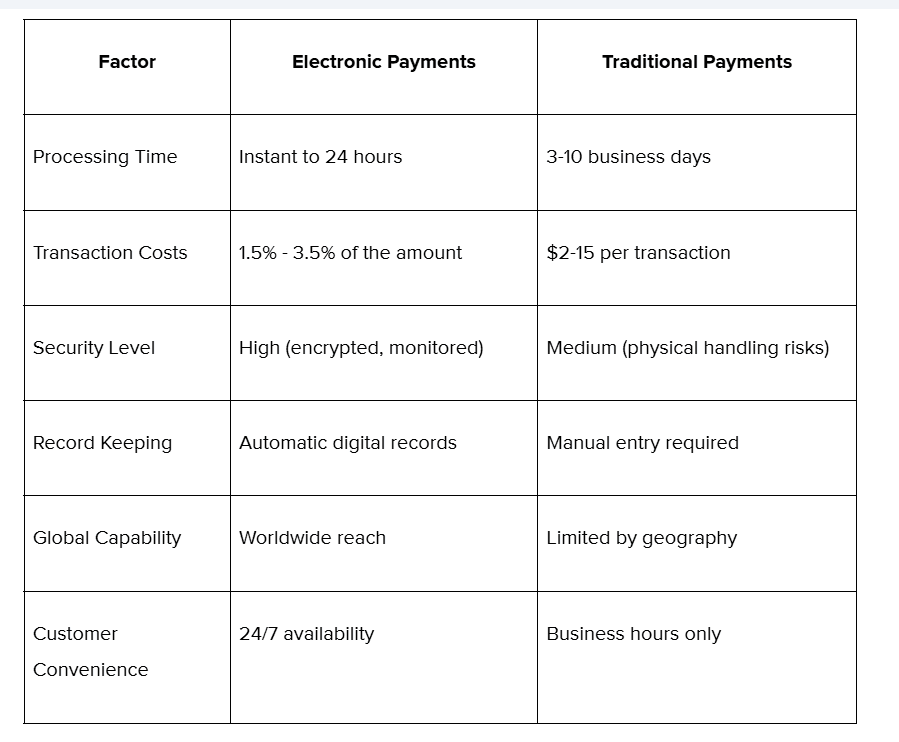

How do electronic payments compare to traditional methods?

The comparison between electronic and traditional payment methods shows significant differences in efficiency, cost, and capability. Here’s how they compare:

What challenges do businesses face with electronic payments?

Despite clear advantages, electronic payment adoption involves overcoming specific challenges that vary by business size and industry. Smart implementation strategies address these concerns effectively.

- Technical integration requirements:

Businesses need compatible software, hardware, and internet connectivity to process electronic payments. This requirement can seem daunting for traditional businesses or those with limited technical resources. However, modern payment solutions offer plug-and-play options that minimize technical barriers.

- Transaction fee considerations:

Electronic payments involve percentage-based fees that can add up for high-volume businesses. Companies must balance these costs against the benefits of faster processing, improved cash flow, and reduced manual handling expenses.

- Security and compliance responsibilities:

Accepting electronic payments requires maintaining security standards and compliance with regulations like PCI DSS. While this adds responsibility, payment service providers typically handle most compliance requirements, reducing the burden on individual businesses.

- Customer adoption variations:

Some customer segments prefer traditional payment methods due to familiarity or concerns about security. Businesses address this by offering multiple payment options while encouraging the adoption of electronic methods through incentives or improved user experience.

- Internet dependency concerns:

Electronic payments require reliable internet connectivity, which can be challenging in areas with poor network coverage. Businesses can address this with backup connectivity options like mobile hotspots or offline-capable payment terminals that store transactions until connection is restored.

What is the future of electronic payment systems?

Electronic payment technology continues to advance rapidly, with new innovations reshaping how businesses and consumers handle transactions. The payment industry is moving toward more integrated, smart, and user-friendly solutions that adapt to changing consumer behaviors and business needs:

- Internet of Things (IoT) payments: Connected devices like smart refrigerators, cars, and wearables will initiate payments automatically when supplies run low or services are needed. This creates seamless payment experiences without human intervention.

- Artificial intelligence integration: AI-powered systems will predict payment preferences, detect fraud in real-time, and optimize transaction routing for better success rates. Machine learning algorithms will continuously improve payment processing efficiency.

- Central Bank Digital Currencies (CBDCs): Government-issued digital currencies will provide new payment options that combine the stability of traditional money with the convenience of digital transactions. These systems will offer faster settlement and reduced costs.

- Voice and conversational payments: Smart assistants and voice interfaces will enable payment commands through natural language, making transactions as simple as speaking a request. This technology will particularly benefit accessibility and hands-free scenarios.

How to choose the right electronic payment system?

Selecting an appropriate payment system requires evaluating business needs, customer preferences, and growth plans to ensure a suitable solution. The right choice balances functionality, cost, and ease of implementation.

- Assess your business requirements: Start by analyzing current payment patterns, customer locations, and transaction types. Businesses serving international customers need multi-currency support and global payment methods.

- Evaluate integration capabilities: Choose systems that integrate smoothly with existing accounting software, e-commerce platforms, and business management tools. Seamless integration reduces manual data entry and improves accuracy across business operations.

- Consider scalability and features: Select solutions that grow with your business. Features like recurring billing, subscription management, mobile optimization, and advanced reporting become valuable as operations expand.

*- Review security and compliance: Ensure chosen providers maintain appropriate security certifications, offer fraud protection, and handle compliance requirements. This protects both business and customer data while reducing liability risks.

- Compare pricing structures: Different providers offer various pricing models, including flat fees, percentage-based charges, or hybrid approaches. Calculate total costs based on your expected transaction volume and average amounts.

- Test customer experience: The payment process directly affects conversion rates and customer satisfaction. Test checkout flows on different devices and with various payment methods to ensure a smooth user experience.

Start collecting payments globally with PayGlocal

Traditional payment systems work for local transactions, but they create barriers when businesses expand internationally. Managing multiple currencies, handling different banking systems, and ensuring payment acceptance across diverse markets requires specialized solutions.'=

PayGlocal removes these complexities by providing a complete international payment platform designed specifically for businesses targeting global markets.

Here’s how PayGlocal supports your international payment processes:

- Multi-currency collection: Accept payments in 33+ currencies and settle in your preferred currency, reducing conversion hassles for both you and your customers.

- Global payment methods: Offer 40+ local payment options, including cards, bank transfers, and regional preferences to maximize acceptance rates worldwide.

- Manage everything from one platform: Track all international transactions, view real-time payment status, and access detailed reports from a single dashboard without juggling multiple payment interfaces.

- Recurring payment solutions: Set up automated billing for subscriptions, installments, or retainer fees with international customers. This works best for SaaS companies or service providers with ongoing client relationships.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically upon settlement, ensuring seamless compliance with export regulations and tax requirements without manual paperwork.

PayGlocal provides businesses with a complete payment infrastructure needed for scaling globally with a fast, reliable, and secure payment solution.

Final thoughts

Electronic payment systems have evolved from convenience features to business necessities. Some of the main benefits of electronic payment systems include faster processing, lower costs, enhanced security, and global reach, directly impacting business growth and customer satisfaction.

Smart businesses use electronic payments strategically, choosing solutions that match their current needs while supporting future expansion. PayGlocal offers all the tools and solutions you need to manage your international payment processes.

Ready to enhance your payment processes and expand globally? Get started with PayGlocal today.