You sent the invoice two weeks ago. Your international client already paid, but the money still hasn't reached your bank account. Between slow bank transfers, unclear fees, and multiple banks in between, collecting from global customers often feels harder than earning the revenue.

Borderless payments solve this problem by moving money across countries without the usual banking delays. With Indian exports reaching $825.25 billion and a 6.05% year-over-year growth rate, more businesses are now selling globally. To stay competitive in global markets and ensure better cash flow, it’s essential to choose faster global payment solutions.

This guide breaks down how borderless payments work, their benefits, and how to choose the right provider for your business.

Borderless payments are international transactions that move money between countries without the delays, high fees, or technical friction that traditional banking systems create. Instead of routing funds through multiple banks over several days, borderless payment platforms handle everything through a single connection.

For example, if you run a SaaS company in India and your customer in Germany pays in euros, a borderless payment system processes that payment, handles the currency conversion, and settles the amount in Indian rupees to your bank account. Your customer pays in a currency they trust. You get paid in yours.

Accepting international payments through traditional channels works, but it comes with trade-offs. Slow settlements, declined transactions, and unclear fees eat into your revenue and your time.

Here’s what borderless payments improve for businesses selling globally.

Note: Stop obsessing over transaction fees. The real hidden tax is the revenue lost to declined payments. If your provider isn't optimizing approval rates, you're leaving money on the table.

The process looks simple from the outside, but several things happen behind the scenes in every transaction. Each step is designed to make the payment feel local to the customer while moving funds across borders.

Here is what happens when a global customer pays you through a borderless payment platform.

1. Payment initiation: Your customer enters their payment details on your checkout page. The platform detects their location and shows relevant payment options like cards, wallets, or bank transfers.

2. Currency handling: The platform identifies the customer's currency and your settlement currency. It calculates the exchange rate and shows the final amount to your customer before they confirm.

3. Payment routing: The system routes the transaction through the most efficient path. This could mean using a local acquiring bank in the customer's country or a direct card network connection.

4. Authorization and fraud check: The payment goes through real-time fraud screening and is sent to the customer's bank for authorization. Smart messaging helps increase the chances of approval.

5. Settlement: Once approved, the platform converts the funds and settles them into your Indian bank account based on the agreed timeline.

6. Documentation: Compliance documents like Foreign Inward Remittance Certificate (FIRC) are generated and delivered to you automatically, so your records stay complete without manual effort.

Tip: Look for providers that show you the status of each payment at every stage. Real-time tracking saves hours of follow-up with banks and customers.

The type of network a provider uses affects how fast your payments settle, what fees you pay, and which payment methods your customers can use. Here’s how the main network types compare.

Most modern providers combine two or more of these networks. For instance, a platform might process card payments through Visa while also connecting to local bank networks in Southeast Asia for wallet-based payments. The result is broader coverage and higher success rates across regions.

Borderless payments are not just faster than traditional bank wires. They use a different technology stack to move money, detect fraud, and connect with local banking systems across the world.

Here’s a quick look at the core technologies and what each one does.

Each of these works together to create a payment experience that feels local to the customer and global for the business.

Countries like the UK (Faster Payments), the EU (SEPA Instant), and India (UPI) have built real-time payment systems. Borderless platforms connect to these networks, so funds move in real time instead of days. For instance, a customer in the UK paying through their bank can complete the transfer instantly, and the platform begins the settlement right away.

Modern borderless payment providers run on cloud infrastructure. This means you connect once through an API or plugin and get access to payment processing across dozens of countries. For example, a Shopify store can integrate a payment gateway and start accepting payments from the US, UK, and Europe without building separate connections for each.

Every international transaction carries some fraud risk. AI-based systems analyze patterns like device type, location, transaction history, and card behavior to flag suspicious payments before they go through. This protects you from chargebacks while making sure genuine customers are not blocked.

Credit cards are popular in the US and UK, but customers in other regions prefer bank transfers, digital wallets, or buy-now-pay-later options. Borderless platforms integrate these local methods so your checkout page shows the right options based on where the customer is. For example, offering iDEAL for Dutch customers or Bancontact for Belgian buyers increases completion rates.

Tip: A provider that supports multiple local payment methods gives you much better coverage than one that only processes card payments.

Your choice of the borderless payment provider depends on where your customers are, what you sell, and how you want to manage payments day-to-day. Here’s what to evaluate before you pick a provider.

Check how many currencies the provider supports for payment collection. If your customers are spread across the US, Europe, the Middle East, and Southeast Asia, you need a platform that handles all those currencies without requiring separate setups for each region.

This is the percentage of transactions that get approved on the first attempt. A difference of even five to ten percent in success rates directly affects your revenue. Ask providers for their average success rates on international card payments, and look for platforms that use smart routing and enhanced messaging to issuers.

Good fraud protection blocks bad transactions without rejecting real customers. Look for providers that use real-time screening with AI, not just basic rule-based filters. The best systems learn from transaction patterns and adjust automatically.

Compare the total cost, not just the headline percentage. Some providers charge low transaction fees but add markups on currency conversion, monthly platform fees, or documentation charges. The clearest pricing models charge a single rate per transaction with no hidden extras.

Check if the provider offers API documentation, e-commerce plugins (Shopify, WooCommerce), and no-code options like payment links. The faster you can go live, the sooner you start collecting payments.

Tip: Request a test transaction before committing. It is the fastest way to see how the checkout looks, how fast settlement happens, and how reporting works.

Borderless payments solve many transaction problems. But there are still a few common issues that can quietly cost you money or create operational challenges if you do not catch them early. Here are some of the essential things to check before you commit to a platform.

The right provider handles these areas well from day one. If you have to work around any of these issues after going live, switching later costs more time and effort than choosing carefully now.

Failed transactions, slow settlements, and manual compliance paperwork cost Indian businesses real money every day. If you are selling globally, your payment system should work as hard as your sales team does.

PayGlocal is built for Indian businesses that collect payments from global customers. It brings together payment acceptance, fraud protection, and compliance into one platform.

Here is what PayGlocal offers.

Get your money where it belongs. PayGlocal simplifies the global-to-local journey, handling the complexity of 180+ countries so you can focus on growth. No more manual FIRC chasing; just payments that work.

Borderless payments are how modern global businesses collect money. They give your customers a smooth checkout experience, give you faster access to your funds, and remove the manual work around compliance and reconciliation.

The technology is ready, and the platforms exist, too. What matters now is picking a provider that matches your business needs and going live. Every month without a proper borderless payment setup is revenue left on the table.

Get started with PayGlocal today and start accepting global payments with higher approval rates, clear pricing, and better security.

Borderless payments solve this problem by moving money across countries without the usual banking delays. With Indian exports reaching $825.25 billion and a 6.05% year-over-year growth rate, more businesses are now selling globally. To stay competitive in global markets and ensure better cash flow, it’s essential to choose faster global payment solutions.

This guide breaks down how borderless payments work, their benefits, and how to choose the right provider for your business.

Key takeaways

- Borderless payments: Your customers pay in their local currency, and you receive the funds in yours, without manual steps in between.

- Multi-currency payments, one platform: PayGlocal lets Indian businesses collect payments from 180+ countries through 33+ currencies.

- Approval rates drive revenue: The right provider routes payments through the best path for each transaction, which directly increases successful checkouts.

- Fit matters more than features: Your business type, customer geography, and payment volume should drive the decision.

- Compliance can be automatic: The best platforms generate Foreign Inward Remittance Certificate (FIRC) and other required documents without manual paperwork.

What are borderless payments?

Borderless payments are international transactions that move money between countries without the delays, high fees, or technical friction that traditional banking systems create. Instead of routing funds through multiple banks over several days, borderless payment platforms handle everything through a single connection.

For example, if you run a SaaS company in India and your customer in Germany pays in euros, a borderless payment system processes that payment, handles the currency conversion, and settles the amount in Indian rupees to your bank account. Your customer pays in a currency they trust. You get paid in yours.

What are the benefits of borderless payments for your business?

Accepting international payments through traditional channels works, but it comes with trade-offs. Slow settlements, declined transactions, and unclear fees eat into your revenue and your time.

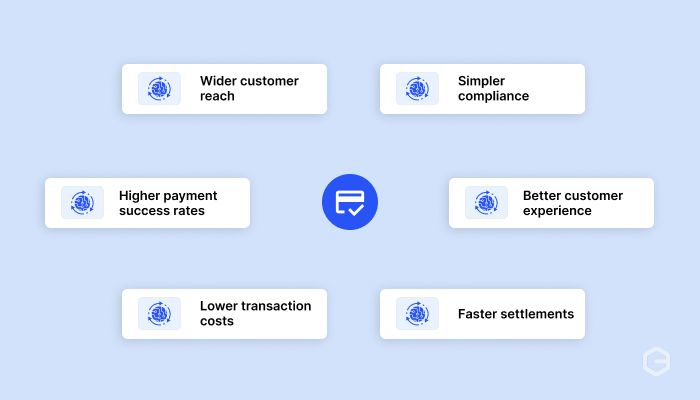

Here’s what borderless payments improve for businesses selling globally.

- Wider customer reach: You can accept payments from customers in 180+ countries using their preferred payment method, whether that is a credit card, bank transfer, or local wallet.

- Higher payment success rates: Smart routing and enhanced transaction messaging reduce declines. More approved payments mean more revenue from the same traffic.

- Lower transaction costs: Borderless platforms cut out intermediary banks and their fees. You pay one clear rate instead of stacking transaction fees from multiple parties.

- Faster settlements: Instead of waiting five to ten business days for a wire transfer, most platforms settle within one to two business days.

- Better customer experience: When your checkout shows local currencies and familiar payment methods, customers trust the process and complete the purchase.

- Simpler compliance: Automatic generation of FIRC and settlement reports means less paperwork and fewer errors in your financial records.

Note: Stop obsessing over transaction fees. The real hidden tax is the revenue lost to declined payments. If your provider isn't optimizing approval rates, you're leaving money on the table.

How do borderless payments work?

The process looks simple from the outside, but several things happen behind the scenes in every transaction. Each step is designed to make the payment feel local to the customer while moving funds across borders.

Here is what happens when a global customer pays you through a borderless payment platform.

1. Payment initiation: Your customer enters their payment details on your checkout page. The platform detects their location and shows relevant payment options like cards, wallets, or bank transfers.

2. Currency handling: The platform identifies the customer's currency and your settlement currency. It calculates the exchange rate and shows the final amount to your customer before they confirm.

3. Payment routing: The system routes the transaction through the most efficient path. This could mean using a local acquiring bank in the customer's country or a direct card network connection.

4. Authorization and fraud check: The payment goes through real-time fraud screening and is sent to the customer's bank for authorization. Smart messaging helps increase the chances of approval.

5. Settlement: Once approved, the platform converts the funds and settles them into your Indian bank account based on the agreed timeline.

6. Documentation: Compliance documents like Foreign Inward Remittance Certificate (FIRC) are generated and delivered to you automatically, so your records stay complete without manual effort.

Tip: Look for providers that show you the status of each payment at every stage. Real-time tracking saves hours of follow-up with banks and customers.

What are the different types of borderless payment networks?

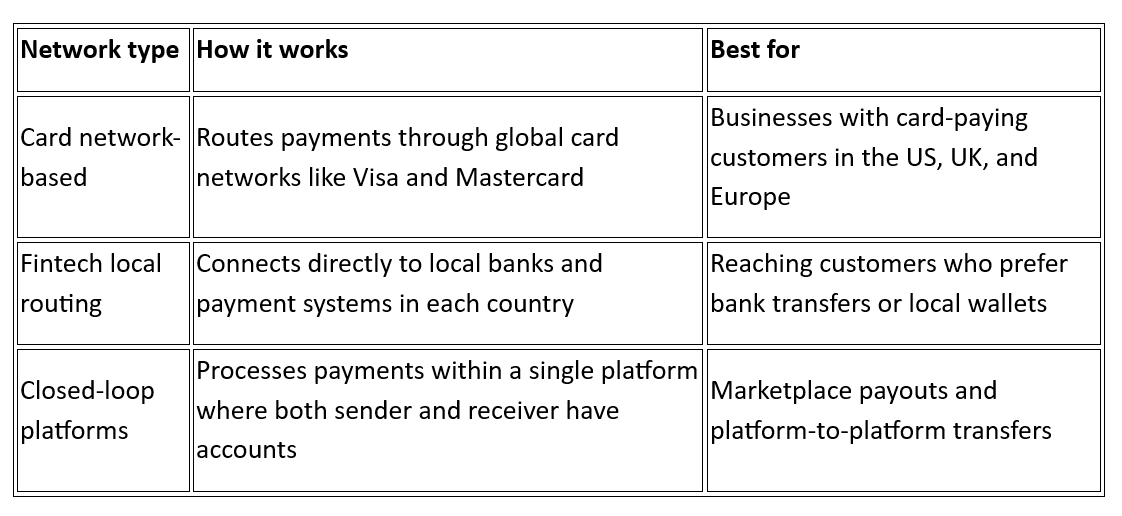

The type of network a provider uses affects how fast your payments settle, what fees you pay, and which payment methods your customers can use. Here’s how the main network types compare.

Most modern providers combine two or more of these networks. For instance, a platform might process card payments through Visa while also connecting to local bank networks in Southeast Asia for wallet-based payments. The result is broader coverage and higher success rates across regions.

What technologies power borderless payments?

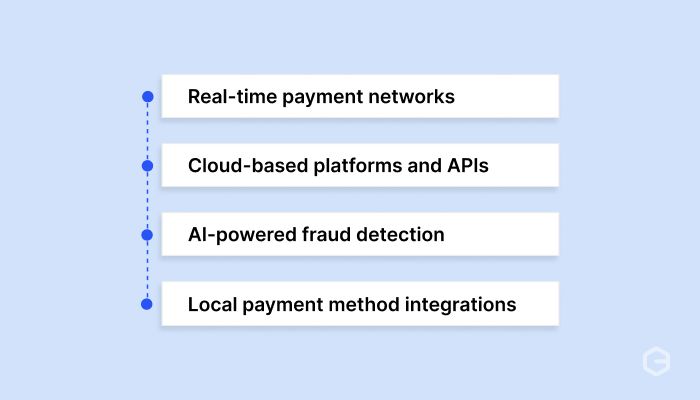

Borderless payments are not just faster than traditional bank wires. They use a different technology stack to move money, detect fraud, and connect with local banking systems across the world.

Here’s a quick look at the core technologies and what each one does.

Each of these works together to create a payment experience that feels local to the customer and global for the business.

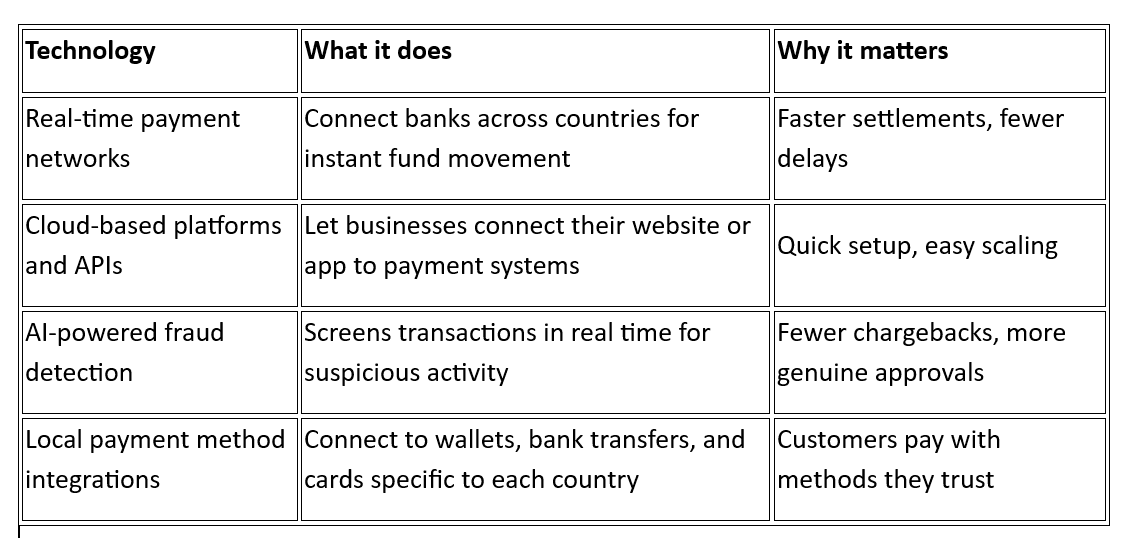

1. Real-time payment networks

Countries like the UK (Faster Payments), the EU (SEPA Instant), and India (UPI) have built real-time payment systems. Borderless platforms connect to these networks, so funds move in real time instead of days. For instance, a customer in the UK paying through their bank can complete the transfer instantly, and the platform begins the settlement right away.

2. Cloud-based payment platforms and APIs

Modern borderless payment providers run on cloud infrastructure. This means you connect once through an API or plugin and get access to payment processing across dozens of countries. For example, a Shopify store can integrate a payment gateway and start accepting payments from the US, UK, and Europe without building separate connections for each.

3. AI-powered fraud detection

Every international transaction carries some fraud risk. AI-based systems analyze patterns like device type, location, transaction history, and card behavior to flag suspicious payments before they go through. This protects you from chargebacks while making sure genuine customers are not blocked.

4. Local payment method integrations

Credit cards are popular in the US and UK, but customers in other regions prefer bank transfers, digital wallets, or buy-now-pay-later options. Borderless platforms integrate these local methods so your checkout page shows the right options based on where the customer is. For example, offering iDEAL for Dutch customers or Bancontact for Belgian buyers increases completion rates.

Tip: A provider that supports multiple local payment methods gives you much better coverage than one that only processes card payments.

How to choose the right borderless payment provider?

Your choice of the borderless payment provider depends on where your customers are, what you sell, and how you want to manage payments day-to-day. Here’s what to evaluate before you pick a provider.

1. Multi-currency acceptance

Check how many currencies the provider supports for payment collection. If your customers are spread across the US, Europe, the Middle East, and Southeast Asia, you need a platform that handles all those currencies without requiring separate setups for each region.

2. Payment success rates

This is the percentage of transactions that get approved on the first attempt. A difference of even five to ten percent in success rates directly affects your revenue. Ask providers for their average success rates on international card payments, and look for platforms that use smart routing and enhanced messaging to issuers.

3. Fraud and risk management

Good fraud protection blocks bad transactions without rejecting real customers. Look for providers that use real-time screening with AI, not just basic rule-based filters. The best systems learn from transaction patterns and adjust automatically.

4. Pricing and fee transparency

Compare the total cost, not just the headline percentage. Some providers charge low transaction fees but add markups on currency conversion, monthly platform fees, or documentation charges. The clearest pricing models charge a single rate per transaction with no hidden extras.

5. Integration and ease of setup

Check if the provider offers API documentation, e-commerce plugins (Shopify, WooCommerce), and no-code options like payment links. The faster you can go live, the sooner you start collecting payments.

Tip: Request a test transaction before committing. It is the fastest way to see how the checkout looks, how fast settlement happens, and how reporting works.

What should you watch out for with borderless payments?

Borderless payments solve many transaction problems. But there are still a few common issues that can quietly cost you money or create operational challenges if you do not catch them early. Here are some of the essential things to check before you commit to a platform.

- Hidden currency conversion markups: Some providers advertise low transaction fees but add a separate markup on the exchange rate, which increases your actual cost per payment.

- Low payment approval rates: If a provider does not use smart routing or enhanced messaging to card issuers, your customers will see more declined transactions at checkout.

- Slow or unclear settlement timelines: Ask specifically when funds reach your bank account. Vague promises of settling within a few days can mean anything from two days to two weeks.

- No automatic compliance documents: If you have to request FIRC or settlement reports manually, it adds hours of admin work every month and increases the risk of errors in your records.

- Limited integration options: A provider with only API-based setup does not work for every team. Check if they also support plugins for your e-commerce platform or no-code options like payment links.

The right provider handles these areas well from day one. If you have to work around any of these issues after going live, switching later costs more time and effort than choosing carefully now.

Accept borderless payments with better approval rates and security

Failed transactions, slow settlements, and manual compliance paperwork cost Indian businesses real money every day. If you are selling globally, your payment system should work as hard as your sales team does.

PayGlocal is built for Indian businesses that collect payments from global customers. It brings together payment acceptance, fraud protection, and compliance into one platform.

Here is what PayGlocal offers.

- Multi-currency accounts: Collect funds in 33+ currencies from 180+ countries, with local accounts in USD, GBP, EUR, and CAD.

- Dynamic checkout: A customizable checkout flow that adapts to each customer's location, showing the right currency and payment options to increase conversions.

- Card payments: Accept all major international credit and debit cards with a payment orchestration engine that routes transactions for the highest possible approval rates.

- Sanction screening: Screen transactions against 300+ global sanction lists in real time, so your business stays compliant without slowing down payments.

- Advanced fraud protection: Every transaction passes through an advanced risk engine that blocks suspicious activity while letting genuine customers pay without friction.

Get your money where it belongs. PayGlocal simplifies the global-to-local journey, handling the complexity of 180+ countries so you can focus on growth. No more manual FIRC chasing; just payments that work.

Final thoughts

Borderless payments are how modern global businesses collect money. They give your customers a smooth checkout experience, give you faster access to your funds, and remove the manual work around compliance and reconciliation.

The technology is ready, and the platforms exist, too. What matters now is picking a provider that matches your business needs and going live. Every month without a proper borderless payment setup is revenue left on the table.

Get started with PayGlocal today and start accepting global payments with higher approval rates, clear pricing, and better security.