Recent data shows that 53.85 crore loans have been approved in India, showing massive growth in credit access across the country. Numerous financial institutions, banks, and lending partnerships in the country, including the co-lending partnership, are driving this growth.

Co-lending is a partnership model where banks and non-banking financial companies join forces to fund loans together. They share the risk, split the returns, and give borrowers faster access to credit at better rates.

In this guide, we break down in detail what co-lending means, how it actually works, the benefits for everyone involved, and how to choose the right partnership. Let’s get started.

Co-lending is a financial partnership where two or more lending institutions work together to fund loans for borrowers. Usually, this involves a bank partnering with an NBFC or fintech firm. Each lender contributes a specific share of the loan amount, shares the credit risk, and splits the returns based on their contribution.

The typical arrangement splits funds 80-20, with banks providing 80% and NBFCs contributing 20%. This structure lets banks tap into NBFCs' customer networks and local market knowledge, while NBFCs access cheaper capital from banks. Borrowers benefit from lower interest rates compared to NBFC-only loans because the bank's lower cost of funds brings down the overall rate.

For instance, a bank might partner with an NBFC that specializes in small business loans. The NBFC finds qualified borrowers, does initial credit checks, and manages customer relationships. The bank provides most of the capital and helps with final loan approval.

Co-lending follows a structured process that divides responsibilities between partners while keeping the experience simple for borrowers. The workflow balances efficiency with proper risk assessment. Here's how the process works:

For example, if you're getting a business loan for ₹10 lakhs through a co-lending arrangement, the bank might provide ₹8 lakhs and the NBFC ₹2 lakhs. But you receive the full ₹10 lakhs in one disbursement. The NBFC collects your monthly payments and splits them with the bank.

Co-lending arrangements come in different forms based on how partners structure their relationship and responsibilities. Each model serves specific market needs and partnership strengths. Here's a quick comparison:

Let’s take a detailed look at each model:

Partnership model: A bank partners with one or multiple NBFCs to jointly fund loans with shared responsibilities. The NBFC sources borrowers and handles servicing while the bank provides capital and applies credit standards. Both share risk and returns proportionally.

For example, a regional bank might partner with an NBFC specializing in agricultural loans, combining the NBFC's farmer connections with the bank's lower-cost capital.

Single primary lender model: One institution acts as the lead lender, managing the entire loan process from origination to servicing. Other partners contribute capital but take a passive role in operations. The primary lender makes all decisions and handles customer relationships.

This works well when one institution has strong processes and the others primarily want exposure to specific loan segments.

Multiple co-lenders model: One institution originates the loans while multiple other lenders contribute funding. The originator finds borrowers and manages servicing, but several banks or NBFCs provide capital based on their capacity.

For instance, a fintech might source personal loan customers while three different banks fund portions of each loan, spreading risk across multiple balance sheets.

Joint venture model: Partners create a separate legal entity specifically for co-lending operations. This new company handles loan origination, underwriting, and servicing. The parent institutions contribute capital and share profits based on their stake.

This model suits partners planning long-term collaboration with significant volume, as it provides dedicated infrastructure and clear governance.

Syndicated co-lending model: A pool of lenders comes together to fund large loan portfolios rather than individual loans. One institution typically leads the syndication, coordinating the group and managing operations. Each lender commits a specific amount based on their capacity and risk appetite.

This approach works for affordable housing portfolios or small business loan pools where individual loans are small but the total funding need is large.

Co-lending creates advantages for borrowers, banks, NBFCs, and the broader financial system. Here's how different stakeholders benefit:

For borrowers:

For banks:

For NBFCs:

Co-lending applies across multiple loan categories, each serving different borrower needs and market segments. The model works for both secured and unsecured lending. Here's how different loan types use co-lending:

Home loans: Banks and housing finance companies partner to fund residential mortgages. The housing finance company brings property market expertise and customer relationships, while the bank provides capital at competitive rates for faster processing.

Personal loans: Banks team up with consumer-focused NBFCs for quick credit assessment through digital platforms. For instance, an NBFC might assess a salaried professional's eligibility in hours, with the bank funding 80% at lower rates.

Business loans: NBFCs understand local business dynamics and assess cash flow patterns that traditional metrics miss. A textile manufacturer in a small town might get financing where the NBFC evaluates actual business performance and local relationships.

Educational loans: Education-focused NBFCs partner with banks to fund tuition and living expenses for students. The NBFC streamlines documentation and course-specific requirements, while the bank keeps rates affordable for domestic and international studies.

Agricultural loans: NBFCs with rural networks and agricultural expertise source farmers needing crop loans or equipment financing. The bank provides priority sector capital, while the NBFC manages collection cycles aligned with harvest seasons.

Co-lending continues to grow as technology improves and regulatory support strengthens. The model is expanding into new sectors and geographies with innovative partnership structures. Some of the key trends shaping co-lending's future include:

These developments will make co-lending more accessible and efficient. Partnerships will form faster, reach more borrowers, and operate with lower costs as technology handles routine tasks.

Selecting the right partner makes the difference between smooth operations and constant friction. Start by evaluating these factors:

Co-lending brings benefits but also creates operational complexities that partners must manage effectively. Here are the main challenges:

Co-lending partnerships work best when payment collection and fund disbursement flow smoothly across borders and currencies.

If you're managing co-lending arrangements with international partners or serving borrowers who make payments from different countries, you need payment infrastructure that handles multi-currency transactions efficiently. Manual tracking, delayed settlements, and unclear fund status create operational friction that slows down your lending operations.

PayGlocal provides the payment infrastructure co-lending partners need for global operations.

Here's how we help:

PayGlocal helps co-lending partners collect payments faster, track funds clearly, and settle across currencies without the operational headaches. Financial institutions across lending, travel, and global commerce trust us to handle their cross-border payment needs.

Co-lending opens new possibilities for lenders and borrowers by combining the strengths of different financial institutions. Banks get market reach and priority sector coverage. NBFCs access cheaper capital and scale their operations. Borrowers receive faster approvals at lower rates.

The model works best when partners choose each other carefully, integrate their systems well, and maintain clear communication. Knowing how co-lending actually operates helps you evaluate if it fits your lending strategy or borrowing needs.

If you're involved in co-lending arrangements that cross borders or currencies, seamless payment infrastructure becomes critical. Managing fund collection, tracking transactions, and ensuring compliance across multiple jurisdictions shouldn't slow down your lending operations.

Make your co-lending partnerships more efficient with payment solutions built for global operations. Get started with PayGlocal today and focus on growing your lending business while we handle the payment complexity.

Co-lending is a partnership model where banks and non-banking financial companies join forces to fund loans together. They share the risk, split the returns, and give borrowers faster access to credit at better rates.

In this guide, we break down in detail what co-lending means, how it actually works, the benefits for everyone involved, and how to choose the right partnership. Let’s get started.

Key takeaways

- Joint funding model: Co-lending involves two or more lenders partnering to fund loans together, typically a bank and a non-banking financial company (NBFC) sharing both risk and returns.

- Lower borrower costs: Borrowers often get lower interest rates because banks bring cheaper capital to the arrangement.

- Risk distribution: Lenders share credit risk based on their contribution percentage, reducing individual exposure.

- Multiple loan types: Co-lending applies to home loans, personal loans, business financing, educational loans, and agricultural credit.

- Global payment solution: PayGlocal enables co-lending partners to collect payments globally and manage settlements efficiently with multi-currency accounts and transparent tracking.

What is co-lending?

Co-lending is a financial partnership where two or more lending institutions work together to fund loans for borrowers. Usually, this involves a bank partnering with an NBFC or fintech firm. Each lender contributes a specific share of the loan amount, shares the credit risk, and splits the returns based on their contribution.

The typical arrangement splits funds 80-20, with banks providing 80% and NBFCs contributing 20%. This structure lets banks tap into NBFCs' customer networks and local market knowledge, while NBFCs access cheaper capital from banks. Borrowers benefit from lower interest rates compared to NBFC-only loans because the bank's lower cost of funds brings down the overall rate.

For instance, a bank might partner with an NBFC that specializes in small business loans. The NBFC finds qualified borrowers, does initial credit checks, and manages customer relationships. The bank provides most of the capital and helps with final loan approval.

How does co-lending work?

Co-lending follows a structured process that divides responsibilities between partners while keeping the experience simple for borrowers. The workflow balances efficiency with proper risk assessment. Here's how the process works:

- Loan sourcing and initial assessment: The NBFC or fintech partner finds potential borrowers and conducts the first round of credit checks, reviewing income, credit history, and repayment capacity.

- Joint approval: Both lenders review the application together, with the bank applying its credit criteria while the NBFC provides local market insights and customer context.

- Fund disbursement: Each party transfers their agreed share of the loan amount, typically through a common escrow account to ensure clean tracking and transparent fund flow.

- Loan servicing: The NBFC handles ongoing loan management, collecting monthly payments, sending reminders, answering questions, and managing any customer issues.

- Risk and return sharing: Credit risk and returns get divided between lenders in proportion to their original contribution ratio, with losses split the same way if defaults occur.

For example, if you're getting a business loan for ₹10 lakhs through a co-lending arrangement, the bank might provide ₹8 lakhs and the NBFC ₹2 lakhs. But you receive the full ₹10 lakhs in one disbursement. The NBFC collects your monthly payments and splits them with the bank.

What are the types of co-lending models?

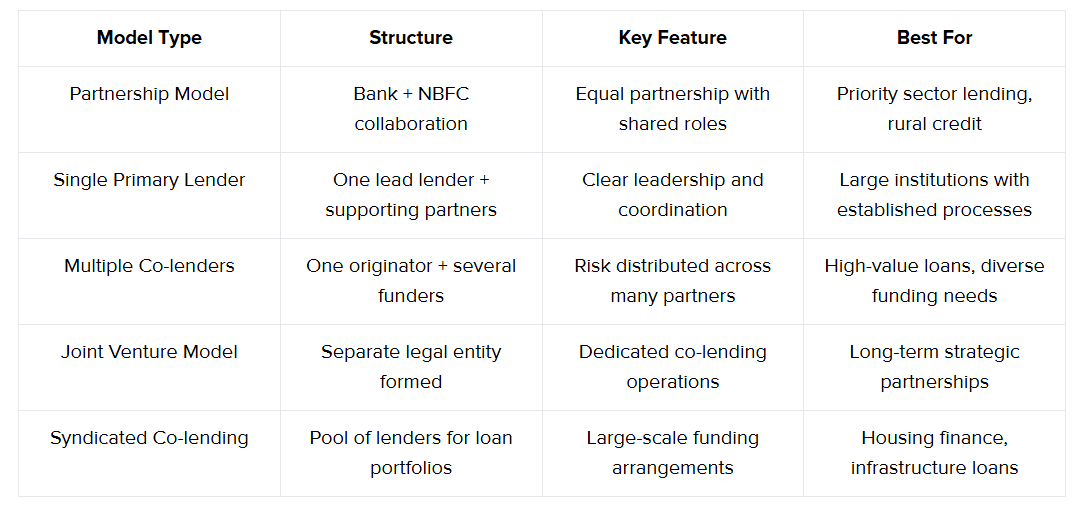

Co-lending arrangements come in different forms based on how partners structure their relationship and responsibilities. Each model serves specific market needs and partnership strengths. Here's a quick comparison:

- Partnership Model: Bank + NBFC collaboration, equal partnership with shared roles, priority sector lending, rural credit.

- Single Primary Lender: One lead lender + supporting partners, clear leadership and coordination, large institutions with established processes.

- Multiple Co-lenders: One originator + several funders, risk distributed across many partners, high-value loans, diverse funding needs.

- Joint Venture Model: Separate legal entity formed, dedicated co-lending operations, long-term strategic partnerships.

- Syndicated Co-lending: Pool of lenders for loan portfolios, large-scale funding arrangements, housing finance, infrastructure loans.

Let’s take a detailed look at each model:

Partnership model: A bank partners with one or multiple NBFCs to jointly fund loans with shared responsibilities. The NBFC sources borrowers and handles servicing while the bank provides capital and applies credit standards. Both share risk and returns proportionally.

For example, a regional bank might partner with an NBFC specializing in agricultural loans, combining the NBFC's farmer connections with the bank's lower-cost capital.

Single primary lender model: One institution acts as the lead lender, managing the entire loan process from origination to servicing. Other partners contribute capital but take a passive role in operations. The primary lender makes all decisions and handles customer relationships.

This works well when one institution has strong processes and the others primarily want exposure to specific loan segments.

Multiple co-lenders model: One institution originates the loans while multiple other lenders contribute funding. The originator finds borrowers and manages servicing, but several banks or NBFCs provide capital based on their capacity.

For instance, a fintech might source personal loan customers while three different banks fund portions of each loan, spreading risk across multiple balance sheets.

Joint venture model: Partners create a separate legal entity specifically for co-lending operations. This new company handles loan origination, underwriting, and servicing. The parent institutions contribute capital and share profits based on their stake.

This model suits partners planning long-term collaboration with significant volume, as it provides dedicated infrastructure and clear governance.

Syndicated co-lending model: A pool of lenders comes together to fund large loan portfolios rather than individual loans. One institution typically leads the syndication, coordinating the group and managing operations. Each lender commits a specific amount based on their capacity and risk appetite.

This approach works for affordable housing portfolios or small business loan pools where individual loans are small but the total funding need is large.

What are the benefits of co-lending?

Co-lending creates advantages for borrowers, banks, NBFCs, and the broader financial system. Here's how different stakeholders benefit:

For borrowers:

- Lower interest rates: Bank participation brings down the overall cost because banks access capital more cheaply than NBFCs. Borrowers pay blended rates that fall between pure bank and pure NBFC pricing.

- Faster approvals: NBFCs handle initial assessment and customer interaction, which typically move faster than traditional bank processes. You get decisions in days instead of weeks.

- Better access to credit: Co-lending extends formal credit to areas and customer segments that banks alone might not serve. Rural borrowers and small businesses gain easier access.

- Simplified experience: You deal with one monthly statement and one servicing partner, even though multiple lenders fund your loan. The complexity stays behind the scenes.

For banks:

- Priority sector targets: Banks must lend specific amounts to priority sectors under regulatory guidelines. Co-lending helps meet these targets by accessing NBFC customer networks in these sectors.

- Market expansion: Partnership with NBFCs opens access to new geographic regions and customer segments without building branch networks or hiring specialized staff.

- Risk distribution: Sharing risk with NBFCs reduces individual exposure on each loan, letting banks diversify their lending portfolio more effectively.

- Technology leverage: Fintech and NBFC partners bring digital platforms and data analytics that banks can benefit from without building everything in-house.

For NBFCs:

- Capital access: Banks provide a stable, lower-cost source of capital compared to what NBFCs can raise independently from markets or depositors.

- Enhanced credibility: Partnering with established banks improves NBFC reputation and helps attract quality borrowers who trust bank involvement.

- Scale growth: Access to bank capital lets NBFCs grow their loan book faster than their own capital base would allow.

- Regulatory alignment: Working alongside banks encourages better compliance practices and governance standards.

What types of loans use co-lending?

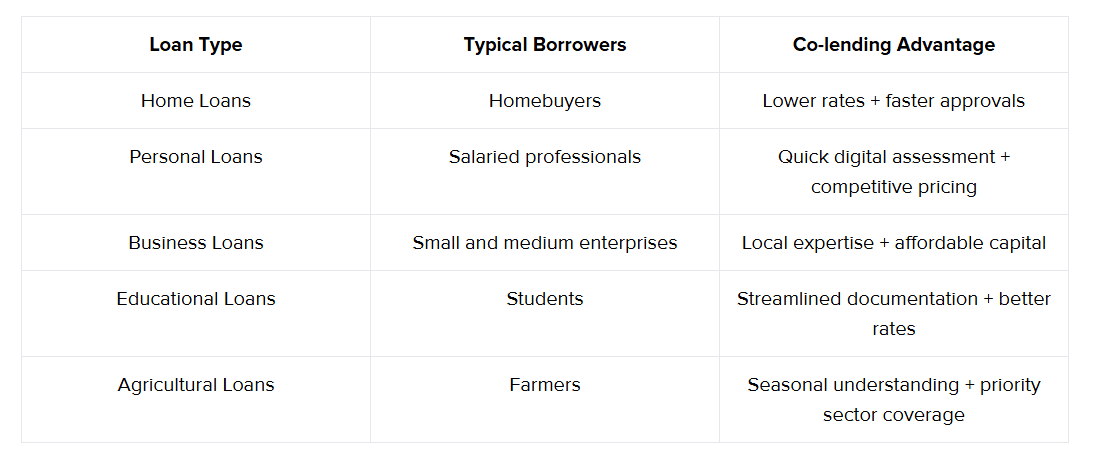

Co-lending applies across multiple loan categories, each serving different borrower needs and market segments. The model works for both secured and unsecured lending. Here's how different loan types use co-lending:

Here's how each category works:

Home loans: Banks and housing finance companies partner to fund residential mortgages. The housing finance company brings property market expertise and customer relationships, while the bank provides capital at competitive rates for faster processing.

Personal loans: Banks team up with consumer-focused NBFCs for quick credit assessment through digital platforms. For instance, an NBFC might assess a salaried professional's eligibility in hours, with the bank funding 80% at lower rates.

Business loans: NBFCs understand local business dynamics and assess cash flow patterns that traditional metrics miss. A textile manufacturer in a small town might get financing where the NBFC evaluates actual business performance and local relationships.

Educational loans: Education-focused NBFCs partner with banks to fund tuition and living expenses for students. The NBFC streamlines documentation and course-specific requirements, while the bank keeps rates affordable for domestic and international studies.

Agricultural loans: NBFCs with rural networks and agricultural expertise source farmers needing crop loans or equipment financing. The bank provides priority sector capital, while the NBFC manages collection cycles aligned with harvest seasons.

What is the future of co-lending?

Co-lending continues to grow as technology improves and regulatory support strengthens. The model is expanding into new sectors and geographies with innovative partnership structures. Some of the key trends shaping co-lending's future include:

- Digital-first partnerships: Fintech companies and digital lenders will drive more co-lending arrangements with faster approvals through AI-powered credit assessment and automated processes.

- Expanded loan categories: Co-lending will move beyond traditional sectors into healthcare financing, education technology, green energy projects, and subscription-based business models.

- Cross-border co-lending: International partnerships between Indian and foreign financial institutions will grow, enabling lending to exporters, students abroad, and global businesses.

- Regulatory evolution: Clearer guidelines and standardized frameworks will reduce compliance complexity and encourage more institutions to participate in co-lending arrangements.

- Technology integration: Better APIs, shared platforms, and blockchain-based systems will make co-lending operations smoother with real-time data sharing and automated settlements.

- Risk management tools: Advanced analytics and machine learning will help partners assess credit risk more accurately, reducing defaults and improving portfolio quality.

- Embedded finance models: Co-lending will integrate into e-commerce platforms, marketplaces, and software applications, offering credit at the point of purchase or service.

These developments will make co-lending more accessible and efficient. Partnerships will form faster, reach more borrowers, and operate with lower costs as technology handles routine tasks.

How do you choose the right co-lending partner?

Selecting the right partner makes the difference between smooth operations and constant friction. Start by evaluating these factors:

- Market alignment: Your partner should serve customer segments and geographic areas that complement your strengths. A bank strong in urban markets might partner with an NBFC focused on rural lending.

- Technology capabilities: Check if the partner has robust digital systems for loan origination, servicing, and reporting. Integration between your systems determines operational efficiency.

- Risk management practices: Review the partner's credit assessment methods, default rates, and recovery processes. You'll share losses, so their risk standards matter as much as yours.

- Regulatory compliance: Ensure your partner maintains good standing with regulators and follows all lending guidelines. Their compliance issues can affect your reputation.

- Operational capacity: Assess if the partner can handle the expected loan volume and has enough staff for customer service, documentation, and dispute resolution.

- Financial stability: Review the partner's capital adequacy, funding sources, and financial health. A struggling partner creates risks even in shared arrangements.

- Cultural fit: Partnership works better when both institutions share similar values around customer treatment, transparency, and business ethics.

What challenges do co-lending arrangements face?

Co-lending brings benefits but also creates operational complexities that partners must manage effectively. Here are the main challenges:

- Coordination overhead: Two institutions must align on every decision, which can slow down approvals and changes that a single lender would make quickly.

- Technology integration: Banks and NBFCs often run different core systems, requiring significant technical work to connect for seamless data flow and reporting.

- Risk assessment conflicts: Partners may use different credit evaluation methods, requiring clear frameworks to resolve when one approves and the other rejects.

- Customer confusion: Borrowers may not understand who handles what, calling the wrong partner for servicing issues that the other manages.

- Regulatory compliance complexity: Different rules apply to banks versus NBFCs, requiring careful legal structuring to ensure the arrangement meets all regulations.

- Payment and settlement tracking: Managing fund flows across multiple currencies and jurisdictions becomes complicated without clear reconciliation systems.

Accept global payments and manage everything in one platform

Co-lending partnerships work best when payment collection and fund disbursement flow smoothly across borders and currencies.

If you're managing co-lending arrangements with international partners or serving borrowers who make payments from different countries, you need payment infrastructure that handles multi-currency transactions efficiently. Manual tracking, delayed settlements, and unclear fund status create operational friction that slows down your lending operations.

PayGlocal provides the payment infrastructure co-lending partners need for global operations.

Here's how we help:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD for seamless international collection.

- Global payment methods: Support 40+ local payment methods so borrowers can pay using their preferred options, increasing collection success rates.

- Instant compliance documentation: Get the FIRC (Foreign Inward Remittance Certificate) right in your inbox after settlement, keeping your regulatory documentation current without manual follow-up.

- Zero fixed costs: Pay only when you transact, with no setup fees, platform charges, or documentation costs affecting your earning margins.

- One platform: Manage all payment operations from a single dashboard with role-based access and detailed reporting.

PayGlocal helps co-lending partners collect payments faster, track funds clearly, and settle across currencies without the operational headaches. Financial institutions across lending, travel, and global commerce trust us to handle their cross-border payment needs.

Final thoughts

Co-lending opens new possibilities for lenders and borrowers by combining the strengths of different financial institutions. Banks get market reach and priority sector coverage. NBFCs access cheaper capital and scale their operations. Borrowers receive faster approvals at lower rates.

The model works best when partners choose each other carefully, integrate their systems well, and maintain clear communication. Knowing how co-lending actually operates helps you evaluate if it fits your lending strategy or borrowing needs.

If you're involved in co-lending arrangements that cross borders or currencies, seamless payment infrastructure becomes critical. Managing fund collection, tracking transactions, and ensuring compliance across multiple jurisdictions shouldn't slow down your lending operations.

Make your co-lending partnerships more efficient with payment solutions built for global operations. Get started with PayGlocal today and focus on growing your lending business while we handle the payment complexity.