Your international client pays your invoice within hours, but days later the money still hasn't arrived in your account. Payments are due and salaries need processing, yet your revenue is stuck in the banking system without a clear timeline.

Cross-border payment aggregators fix this by processing international transactions through optimized routes that settle faster. Indian businesses exported $825.25 billion worth of goods and services in 2024-25, with many transactions powered by these platforms handling currency conversion, compliance, and routing.

This guide provides a detailed breakdown of what cross-border payment aggregators are, how they work, and their key benefits for businesses receiving international payments.

A cross-border payment aggregator is an authorized entity facilitating online international transactions between businesses and global customers. Instead of setting up separate bank accounts or connections in every target country, the aggregator provides the infrastructure to collect and settle those payments.

These aggregators act as intermediaries, connecting merchants with international payment networks, handling currency conversion, cross-border processing, and regulatory compliance. They make international payment collection as seamless as domestic payments.

In practice, aggregators support payments for e-commerce goods, SaaS subscriptions, consulting services, and digital products. They eliminate the need to manage complex foreign banking relationships, letting businesses focus on growth while technology handles revenue flow.

Cross-border payment aggregators accelerate payment receipt, improving cash flow. Traditional methods take days or weeks, but these platforms process transactions near real-time.

Key benefits include:

Merchants see fewer failures, faster funds access, and simplified operations.

Any business receiving payments from outside India benefits from these aggregators.

Physical product exporters use aggregators to collect from international buyers. E-commerce stores, fashion brands, handicrafts, and electronics sellers accept global credit cards efficiently. Marketplace sellers on Amazon or eBay streamline collections.

Service providers with global clients rely on aggregators for recurring billing. Software firms, consultants, agencies, and SaaS companies bill worldwide customers reliably. Optimized recurring charges minimize churn from failed payments.

Professionals use aggregators for cost-effective international receipts. Freelancers and consultants avoid slow, expensive bank transfers. Payment links or invoicing integrations provide flexibility.

Tip: Even a few monthly international payments justify an aggregator's time and fee savings over traditional wires.

Cross-border payment aggregators handle the complete payment journey from customer checkout to merchant settlement.

The process starts when an international customer initiates a payment. The aggregator receives the payment request, validates the transaction details, and routes it through the appropriate payment network. This routing happens in real time and considers factors like the customer's location, card type, and transaction currency.

Customers pay via preferred methods—credit/debit cards, local options—with a ₹25 lakh per transaction limit. Processing occurs in the customer's currency for familiarity (USD for US, GBP for UK). Direct connections to card networks and local acquirers boost approvals.

Post-authorization, funds convert to INR or preferred currency at transparent rates. Merchants see exact rates for planning. Settlements occur in 1-3 business days typically, enhancing cash flow.

Transactions undergo checks for regulations, fraud, and sanctions. Onboarding verifies merchants; ongoing monitoring detects anomalies. Records support reporting; enhanced due diligence applies above ₹2.5 lakh for imports.

Tip: Select aggregators offering automated compliance docs to minimize manual work.

Note: Aggregators often include multi-currency accounts, FX management, and compliance—beyond gateways' processing focus.

International card payments fail at higher rates than domestic payments. Cross-border payment aggregators address the specific causes of these failures. Here's how they do it:

The combined effect is significant. Businesses using specialized cross-border payment aggregators achieve higher approval rates on international cards compared to less optimized solutions.

Collecting payments from customers abroad comes with its own set of challenges. Transactions take longer to settle, fees stack up across multiple banks, and cards get declined at higher rates. Cross-border payment aggregators solve these specific problems.

Traditional international payment methods can generally take three to seven business days for settlement. Cross-border payment aggregators reduce this timeline. Many processes settle international payments within one to three business days. Some offer even faster settlement for certain transaction types.

Speed matters for cash flow. Businesses that need quick access to revenue from international sales benefit from faster settlement. This is particularly important for small businesses and startups where cash flow timing affects operations.

International payment processing historically involved multiple intermediary banks, each taking a fee. Cross-border payment aggregators provide transparent pricing. Merchants see a clear percentage rate per transaction with no hidden fees. The total cost is predictable, which helps with financial planning.

Currency conversion costs are shared upfront. Exchange rate markups and conversion fees are shown clearly rather than hidden in the transaction. This transparency helps merchants compare options and know their true costs.

International card transactions fail more frequently than domestic transactions. Different countries have different fraud rules, card network policies, and banking practices.

Cross-border payment aggregators optimize for international approvals. They use the routing and messaging techniques described earlier to maximize the likelihood that international card issuers approve transactions.

International transactions involve multiple regulatory frameworks. Foreign exchange rules, tax reporting, and trade regulations all apply. Cross-border payment aggregators handle all the necessary compliance.

They ensure transactions fulfill the regulatory requirements, maintain required documentation, and provide merchants with compliance reports. This removes a significant operational burden from merchants who would otherwise need to manage these requirements independently.

International payments shouldn't hold your business back. Too many exporters watch sales disappear because of payment failures. Cards get declined. Transactions take days, and compliance feels overwhelming.

PayGlocal is an authorized cross-border payment aggregator that removes these obstacles. The platform is built specifically to help Indian businesses succeed in international commerce. Here's what you get:

PayGlocal handles compliance automatically. You receive the Foreign Inward Remittance Certificate (FIRC) directly in your inbox after settlement. Settlement is also fast, with transactions settling within just a few business days, improving your cash flow compared to traditional international payment methods.

Cross-border payment aggregators turn international payment collection from a problem into a system that works. These authorized entities handle the complexity and help you get more transactions approved.

The right cross-border payment aggregator removes obstacles between you and your global customers. For exporters, SaaS companies, and freelancers receiving international payments, these entities are how you compete globally without the headaches.

Your international payments should work as well as your product. Get started with PayGlocal and stop losing sales to payment failures.

Cross-border payment aggregators fix this by processing international transactions through optimized routes that settle faster. Indian businesses exported $825.25 billion worth of goods and services in 2024-25, with many transactions powered by these platforms handling currency conversion, compliance, and routing.

This guide provides a detailed breakdown of what cross-border payment aggregators are, how they work, and their key benefits for businesses receiving international payments.

Key Takeaways

- Cross-border payment aggregators are authorized entities: They facilitate online international transactions for permissible goods and services, acting as intermediaries between Indian merchants and global customers.

- They differ from regular payment gateways: Aggregators handle multi-currency transactions, international compliance, and currency conversion, while gateways primarily route domestic transactions.

- Approval rates improve significantly: Optimized routing and enhanced messaging to international card networks reduce transaction failures.

- Multiple business types benefit: Goods exporters, service exporters, SaaS companies, and freelancers use aggregators for faster, more reliable payments.

- PayGlocal ensures faster global payments: As an authorized aggregator, PayGlocal boosts approval rates while cutting costs and settlement times.

What is a Cross-Border Payment Aggregator?

A cross-border payment aggregator is an authorized entity facilitating online international transactions between businesses and global customers. Instead of setting up separate bank accounts or connections in every target country, the aggregator provides the infrastructure to collect and settle those payments.

These aggregators act as intermediaries, connecting merchants with international payment networks, handling currency conversion, cross-border processing, and regulatory compliance. They make international payment collection as seamless as domestic payments.

In practice, aggregators support payments for e-commerce goods, SaaS subscriptions, consulting services, and digital products. They eliminate the need to manage complex foreign banking relationships, letting businesses focus on growth while technology handles revenue flow.

What are the benefits of using cross-border payment aggregators?

Cross-border payment aggregators accelerate payment receipt, improving cash flow. Traditional methods take days or weeks, but these platforms process transactions near real-time.

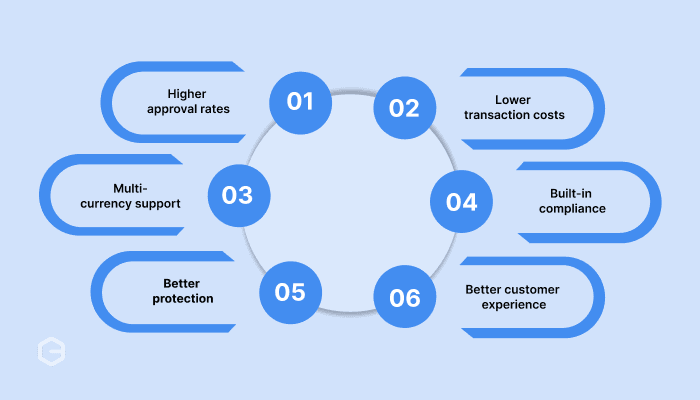

Key benefits include:

- Higher approval rates: Optimized routing and messaging reduce international transaction failures.

- Lower transaction costs: Transparent pricing with no hidden fees and volume discounts.

- Multi-currency support: Accept payments in customers' preferred currencies, boosting conversions.

- Built-in compliance: Handle regulatory checks, due diligence, and monitoring automatically.

- Better protection: Advanced fraud screening reduces chargebacks and fraud risks.

- Improved customer experience: Localized options and familiar currencies reduce checkout abandonment.

Merchants see fewer failures, faster funds access, and simplified operations.

Who Needs a Cross-Border Payment Aggregator?

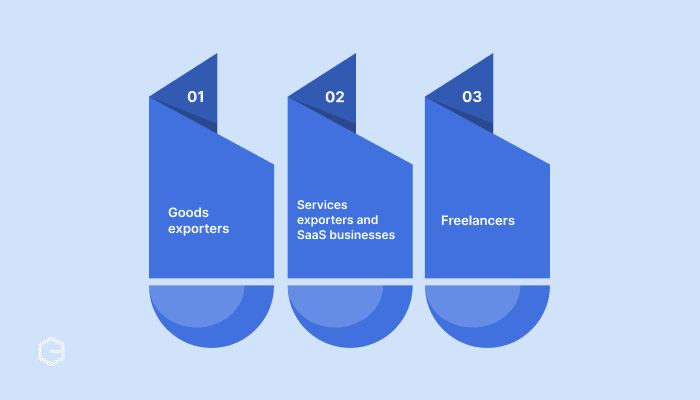

Any business receiving payments from outside India benefits from these aggregators.

1. Goods Exporters

Physical product exporters use aggregators to collect from international buyers. E-commerce stores, fashion brands, handicrafts, and electronics sellers accept global credit cards efficiently. Marketplace sellers on Amazon or eBay streamline collections.

2. Services Exporters and SaaS Businesses

Service providers with global clients rely on aggregators for recurring billing. Software firms, consultants, agencies, and SaaS companies bill worldwide customers reliably. Optimized recurring charges minimize churn from failed payments.

3. Freelancers

Professionals use aggregators for cost-effective international receipts. Freelancers and consultants avoid slow, expensive bank transfers. Payment links or invoicing integrations provide flexibility.

Tip: Even a few monthly international payments justify an aggregator's time and fee savings over traditional wires.

How Cross-Border Payment Aggregators Work?

Cross-border payment aggregators handle the complete payment journey from customer checkout to merchant settlement.

The process starts when an international customer initiates a payment. The aggregator receives the payment request, validates the transaction details, and routes it through the appropriate payment network. This routing happens in real time and considers factors like the customer's location, card type, and transaction currency.

Payment Collection

Customers pay via preferred methods—credit/debit cards, local options—with a ₹25 lakh per transaction limit. Processing occurs in the customer's currency for familiarity (USD for US, GBP for UK). Direct connections to card networks and local acquirers boost approvals.

Currency Conversion and Settlement

Post-authorization, funds convert to INR or preferred currency at transparent rates. Merchants see exact rates for planning. Settlements occur in 1-3 business days typically, enhancing cash flow.

Compliance and Monitoring

Transactions undergo checks for regulations, fraud, and sanctions. Onboarding verifies merchants; ongoing monitoring detects anomalies. Records support reporting; enhanced due diligence applies above ₹2.5 lakh for imports.

Tip: Select aggregators offering automated compliance docs to minimize manual work.

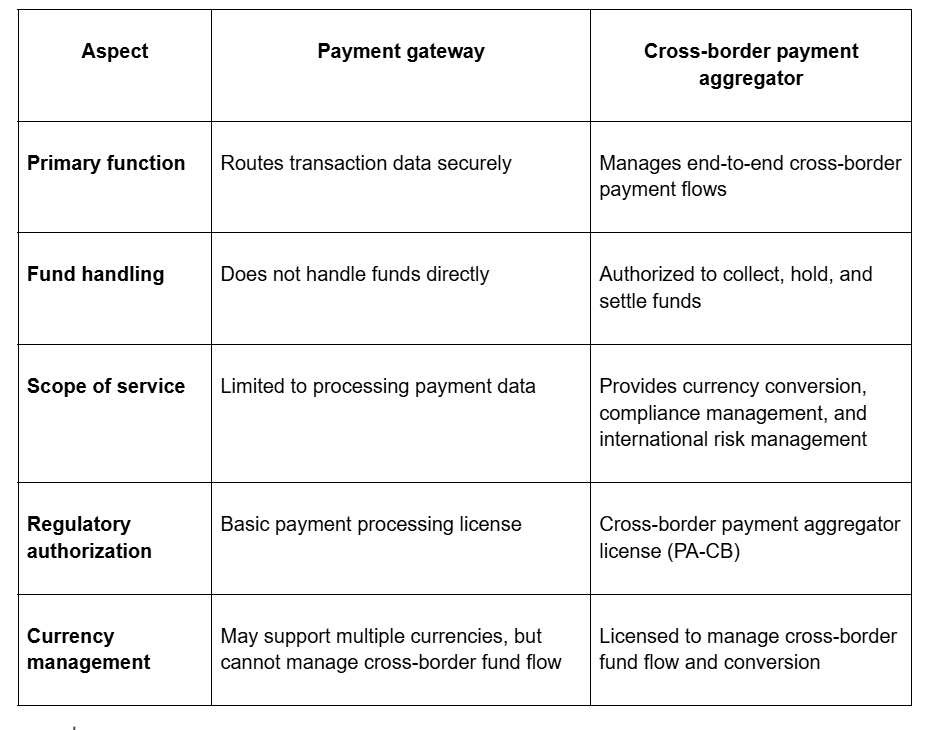

What are the differences between cross-border payment aggregators and payment gateways?

Note: Aggregators often include multi-currency accounts, FX management, and compliance—beyond gateways' processing focus.

How do cross-border payment aggregators improve transaction success rates?

International card payments fail at higher rates than domestic payments. Cross-border payment aggregators address the specific causes of these failures. Here's how they do it:

- Transaction messaging optimization: International card issuers require specific data fields to approve transactions. Cross-border payment aggregators enhance transaction messages with the correct information for each issuing bank and card network.

- Intelligent routing: Not all payment routes deliver the same success rates. Cross-border payment aggregators analyze performance across different routes and direct transactions through the paths most likely to succeed.

- Local acquiring: Processing transactions through local acquiring banks in the customer's country reduces cross-border friction. Card issuers approve transactions that appear local rather than international.

- Balanced fraud screening: Overly aggressive fraud filters block legitimate transactions, while weak filters allow fraud. Cross-border payment aggregators tune their fraud systems to catch actual fraud without creating false positives that hurt approval rates.

- Smart retry logic: When a transaction fails for a temporary reason like a network timeout, intelligent retry systems attempt the transaction again through an alternative route. This recovers transactions that would otherwise be lost.

The combined effect is significant. Businesses using specialized cross-border payment aggregators achieve higher approval rates on international cards compared to less optimized solutions.

What are the common challenges cross-border payment aggregators solve?

Collecting payments from customers abroad comes with its own set of challenges. Transactions take longer to settle, fees stack up across multiple banks, and cards get declined at higher rates. Cross-border payment aggregators solve these specific problems.

Slow international payment processing

Traditional international payment methods can generally take three to seven business days for settlement. Cross-border payment aggregators reduce this timeline. Many processes settle international payments within one to three business days. Some offer even faster settlement for certain transaction types.

Speed matters for cash flow. Businesses that need quick access to revenue from international sales benefit from faster settlement. This is particularly important for small businesses and startups where cash flow timing affects operations.

High transaction fees and hidden charges

International payment processing historically involved multiple intermediary banks, each taking a fee. Cross-border payment aggregators provide transparent pricing. Merchants see a clear percentage rate per transaction with no hidden fees. The total cost is predictable, which helps with financial planning.

Currency conversion costs are shared upfront. Exchange rate markups and conversion fees are shown clearly rather than hidden in the transaction. This transparency helps merchants compare options and know their true costs.

Low approval rates on international cards

International card transactions fail more frequently than domestic transactions. Different countries have different fraud rules, card network policies, and banking practices.

Cross-border payment aggregators optimize for international approvals. They use the routing and messaging techniques described earlier to maximize the likelihood that international card issuers approve transactions.

Complex compliance requirements

International transactions involve multiple regulatory frameworks. Foreign exchange rules, tax reporting, and trade regulations all apply. Cross-border payment aggregators handle all the necessary compliance.

They ensure transactions fulfill the regulatory requirements, maintain required documentation, and provide merchants with compliance reports. This removes a significant operational burden from merchants who would otherwise need to manage these requirements independently.

Switch to PayGlocal for fast and secure cross-border payments

International payments shouldn't hold your business back. Too many exporters watch sales disappear because of payment failures. Cards get declined. Transactions take days, and compliance feels overwhelming.

PayGlocal is an authorized cross-border payment aggregator that removes these obstacles. The platform is built specifically to help Indian businesses succeed in international commerce. Here's what you get:

- Multi-currency accounts: Accept payments in USD, GBP, EUR, CAD, and additional currencies from customers worldwide. Your international customers pay in their preferred currency.

- Recurring payments: Process subscription charges and recurring billing on international cards with network-compliant standing instructions. Reduce involuntary churn from failed renewal payments.

- Advanced risk engine: Every transaction passes through intelligent fraud screening that catches suspicious activity without blocking legitimate customers. Protect your business while maintaining high approval rates.

- Sanction screening: Every transaction gets screened against global sanctions lists automatically. Stay compliant without adding manual checks or slowing down payments.

- One platform management: Control everything from a single dashboard. Set up payments, track transactions, manage settlements, and access reports without jumping between multiple systems.

PayGlocal handles compliance automatically. You receive the Foreign Inward Remittance Certificate (FIRC) directly in your inbox after settlement. Settlement is also fast, with transactions settling within just a few business days, improving your cash flow compared to traditional international payment methods.

Final thoughts

Cross-border payment aggregators turn international payment collection from a problem into a system that works. These authorized entities handle the complexity and help you get more transactions approved.

The right cross-border payment aggregator removes obstacles between you and your global customers. For exporters, SaaS companies, and freelancers receiving international payments, these entities are how you compete globally without the headaches.

Your international payments should work as well as your product. Get started with PayGlocal and stop losing sales to payment failures.