If you're managing global payments, you're already aware of the central role cross-border transactions play in scaling your business. Whether you’re an exporter dealing with overseas clients, a fintech platform offering global services, or a CFO overseeing international receivables, cross-border payments have become a strategic priority.

In 2024, the global cross-border payments market was valued at $198.6 million and is expected to reach $351.6 million by 2032. India is leading with record-breaking remittances of $135.4 billion in FY 2024–25, a 14% increase from the previous year.

As someone leading payment, compliance, or technology infrastructure, you need a cross-border payments solution that can reduce FX slippage, increase success rates, comply with ever-evolving regulations, and integrate cleanly with your existing systems. This blog helps you do exactly that.

Cross-border payments are financial transactions where the sender and recipient are located in different countries.

For example, when an Indian software company receives payment from a client in the United States, the transaction flows from a US bank account in dollars to an Indian bank account in rupees.

The key thing about cross-border payments is the geographic separation between payer and payee, which creates additional complexity compared to domestic transfers.

Cross-border payments involve several intermediaries and verification stages. Here's how international payments move from sender to recipient:

When sending or receiving money across countries, the method you choose affects cost, speed, compliance, and the overall customer experience. Businesses today have access to a range of cross-border payment solutions, each with its unique use cases, risks, and benefits.

Choosing the right mix depends on transaction size, frequency, destination, and the level of control you need over currency and compliance. Here's a look at the most common options available today.

Cross-border payments play an important role in how most transactions occur. Here are some of the common uses of cross-border payments:

Sending money across borders requires careful handling. Mistakes or oversights in even one step can result in delays, additional fees, or failed transactions. That’s why having a clear process in place is crucial.

Here are the key steps to sending cross-border payments effectively:

1. Select the Right Payment Method: Start by choosing the most suitable payment method for your transaction. Wire transfers are commonly used for large-value payments, while card payments or digital wallets may be more suitable for smaller or recurring transactions.

2. Check the Exchange Rate: Exchange rates fluctuate frequently. Before you process a payment, check the live rate and understand any markup your provider may charge.

3. Use a Trusted Global Payment Platform: Instead of handling international transfers manually, partner with a trusted cross-border payment provider.

4. Enter Accurate Recipient Details: Ensure you have the recipient’s full name, account number, bank details (including the SWIFT/BIC code), and currency preference. Errors here are one of the most common reasons for delayed or failed international transactions.

5. Review and Verify the Payment: Double-check all payment details, including the amount, currency, and recipient information. Some platforms also allow you to pre-validate card support to avoid decline.

6. Authorize and Send: Once everything is confirmed, authorize the transaction. Depending on the method used, the processing time may vary from a few seconds to several days.

7. Monitor and Track the Transaction: After sending, track the status using your provider’s dashboard. Real-time updates help ensure the payment reaches the recipient as expected.

Despite technological advances, international payments still encounter several persistent obstacles that affect businesses daily.

Selecting an international payment provider requires careful evaluation of multiple factors that directly impact your business operations.

Start by assessing your transaction patterns, such as frequency, amounts, currencies, and destination countries. For instance, a freelancer receiving occasional payments has different needs than an e-commerce business processing hundreds of international orders monthly.

Managing international payments doesn't have to drain your resources or complicate your operations. Without the right payment solution, businesses often struggle with expensive payment transfers, delayed settlements, and complex compliance requirements that slow down growth.

Whether you're scaling your business globally or expanding in new markets, PayGlocal provides the infrastructure you need to collect payments globally while settling locally in INR.

Cross-border payments are essential infrastructure for any business operating internationally. While traditional banking methods continue to serve basic needs, modern payment platforms offer significant advantages in cost, speed, and user experience.

The key to success is choosing a solution that matches your specific business requirements. Consider your transaction patterns, growth plans, and operational needs when evaluating providers. PayGlocal offers a complete, all-in-one platform to manage your global transactions.

Ready to enhance your international payment collection processes and focus on growing your business? Get started with PayGlocal today.

In 2024, the global cross-border payments market was valued at $198.6 million and is expected to reach $351.6 million by 2032. India is leading with record-breaking remittances of $135.4 billion in FY 2024–25, a 14% increase from the previous year.

As someone leading payment, compliance, or technology infrastructure, you need a cross-border payments solution that can reduce FX slippage, increase success rates, comply with ever-evolving regulations, and integrate cleanly with your existing systems. This blog helps you do exactly that.

Key Takeaways:

- Cross-border payments: Essential for Indian exporters, D2C brands, and tech-led businesses looking to scale globally, but they come with cost, compliance, and conversion challenges.

- Common methods: Common cross-border payment methods include wire transfers, card payments, ACH, digital wallets, and online payment platforms.

- Key uses: It ranges from international trade and freelancing to education, remittances, and global e-commerce, each requiring tailored payment infrastructure.

- Global payment platform: PayGlocal provides multi-currency accounts and global payment methods to simplify international transactions for businesses.

What are cross-border payments?

Cross-border payments are financial transactions where the sender and recipient are located in different countries.

For example, when an Indian software company receives payment from a client in the United States, the transaction flows from a US bank account in dollars to an Indian bank account in rupees.

The key thing about cross-border payments is the geographic separation between payer and payee, which creates additional complexity compared to domestic transfers.

How do cross-border payments work?

Cross-border payments involve several intermediaries and verification stages. Here's how international payments move from sender to recipient:

- Payment initiation: The sender starts the transfer through their bank or payment provider by providing the recipient's details, transfer amount, and purpose of payment.

- Authentication and compliance checks: The sending institution verifies that the transaction meets regulatory requirements and screens for sanctions or fraud indicators.

- Routing through correspondent networks: The payment travels through SWIFT or other messaging networks that connect banks globally, often passing through multiple intermediary institutions.

- Currency conversion: Exchange rates are applied at various points in the process, with each intermediary potentially adding its own margin to the conversion.

- Final settlement: The receiving bank credits the recipient's account after completing its own verification and compliance procedures.

- Confirmation and reporting: Both parties receive confirmation of the completed transfer, with documentation provided for compliance and accounting purposes.

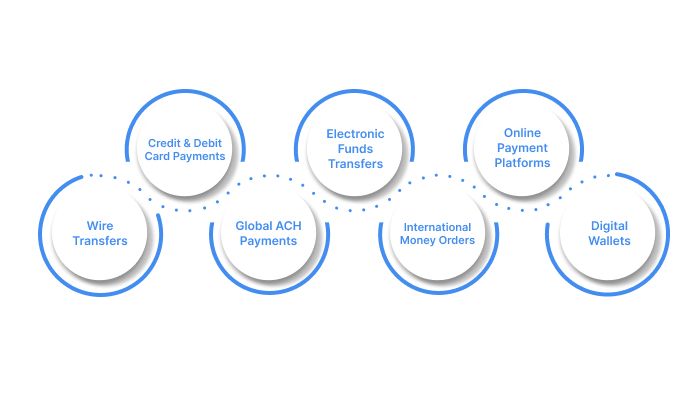

What are the different cross-border payment solutions?

When sending or receiving money across countries, the method you choose affects cost, speed, compliance, and the overall customer experience. Businesses today have access to a range of cross-border payment solutions, each with its unique use cases, risks, and benefits.

Choosing the right mix depends on transaction size, frequency, destination, and the level of control you need over currency and compliance. Here's a look at the most common options available today.

- Wire Transfers: This method is widely used for large-value transfers. Wire transfers rely on the SWIFT network to send money between banks. While secure, they’re often slow (2–5 days) and come with multiple hidden fees.

- Credit and Debit Card Payments: Global card networks, such as Visa, MasterCard, and RuPay, enable you to accept international payments quickly.

- Global ACH Payments: Global ACH (Automated Clearing House) transfers enable low-cost, batch-processed transactions across international borders. They're ideal for payroll, vendor payments, or mass disbursements. Processing times may vary by country.

- Electronic Funds Transfers (EFTs): Used for direct account-to-account transfers, EFTs are better suited for recurring billing or payroll. They’re cost-effective but still depend on regional infrastructure that may delay processing.

- International Money Orders: This cross-border payment method is used occasionally for low-value payments, though not ideal for growing digital businesses.

- Online Payment Platforms: Solutions like PayGlocal, PayPal, Wise, and Stripe facilitate quick cross-border payments, particularly for freelancers and small businesses.

- Digital Wallets: Platforms like Apple Pay, Google Pay, and Alipay offer wallet-based payments that can be linked to a card or bank account. Useful in consumer-driven cross-border transactions, especially e-commerce.

What are the uses of cross-border payments?

Cross-border payments play an important role in how most transactions occur. Here are some of the common uses of cross-border payments:

- International Trade: Exporters and importers rely on cross-border payments to settle invoices, receive payments for goods, and manage logistics-related costs.

- Global Freelancing and Remote Work: Freelancers and remote teams often get paid in foreign currencies. Cross-border payment solutions are crucial for ensuring timely payouts, particularly for Indian developers, consultants, and service providers working with clients overseas.

- Travel and Tourism: Hotels, travel agents, and tour operators accept payments from global customers and often use cross-border payment solutions to ensure smooth transactions.

- Remittances: Migrant workers send billions of dollars home every year. In India, this accounts for a major share of inward foreign exchange. These P2P payments are among the most frequent use cases globally.

- Investments: Whether it’s funding a startup overseas, buying stocks, or investing in global real estate, cross-border payments enable capital to move freely across regions.

- E-commerce Sales and Marketplaces: D2C brands and marketplaces that accept international orders require cross-border payment systems that support global cards, local wallets, and dynamic currency conversion to deliver a better customer experience.

- Education and Cross-Border Tuition Payments: Students and parents making tuition fee payments to international institutions, or businesses collecting course fees globally, rely on low-fee and timely cross-border transfers.

How to send cross-border payments?

Sending money across borders requires careful handling. Mistakes or oversights in even one step can result in delays, additional fees, or failed transactions. That’s why having a clear process in place is crucial.

Here are the key steps to sending cross-border payments effectively:

1. Select the Right Payment Method: Start by choosing the most suitable payment method for your transaction. Wire transfers are commonly used for large-value payments, while card payments or digital wallets may be more suitable for smaller or recurring transactions.

2. Check the Exchange Rate: Exchange rates fluctuate frequently. Before you process a payment, check the live rate and understand any markup your provider may charge.

3. Use a Trusted Global Payment Platform: Instead of handling international transfers manually, partner with a trusted cross-border payment provider.

4. Enter Accurate Recipient Details: Ensure you have the recipient’s full name, account number, bank details (including the SWIFT/BIC code), and currency preference. Errors here are one of the most common reasons for delayed or failed international transactions.

5. Review and Verify the Payment: Double-check all payment details, including the amount, currency, and recipient information. Some platforms also allow you to pre-validate card support to avoid decline.

6. Authorize and Send: Once everything is confirmed, authorize the transaction. Depending on the method used, the processing time may vary from a few seconds to several days.

7. Monitor and Track the Transaction: After sending, track the status using your provider’s dashboard. Real-time updates help ensure the payment reaches the recipient as expected.

What are the challenges of cross-border payments?

Despite technological advances, international payments still encounter several persistent obstacles that affect businesses daily.

- High costs: Traditional banks charge high combined fees and unfavorable exchange rates. These expenses can significantly impact profit margins, especially for businesses with frequent international transactions.

- Slow processing times: Creates cash flow challenges and customer satisfaction issues. When payments take 3-5 business days to clear, businesses struggle to maintain smooth operations, and customers become frustrated with delayed service delivery.

- Limited transparency: Makes it difficult to track payment status or resolve issues quickly. Many traditional systems provide minimal visibility into where payments are in the processing pipeline, creating uncertainty for both senders and recipients.

- Complex compliance requirements: Businesses have to handle different regulations, documentation requirements, and reporting obligations in each country they operate.

- Currency volatility: Introduces financial risk, especially for businesses that don't manage their foreign exchange exposure. Exchange rate fluctuations between transaction initiation and settlement can significantly impact received amounts.

- Access limitations: Prevent some businesses from using optimal payment methods due to geographic restrictions or banking relationship requirements.

How to choose the right cross-border payment solution?

Selecting an international payment provider requires careful evaluation of multiple factors that directly impact your business operations.

Start by assessing your transaction patterns, such as frequency, amounts, currencies, and destination countries. For instance, a freelancer receiving occasional payments has different needs than an e-commerce business processing hundreds of international orders monthly.

- Compare total costs: Calculate the true cost, including exchange rate margins, intermediary fees, and any monthly or setup charges. Request quotes for your typical transaction scenarios to make accurate comparisons.

- Evaluate processing speeds: If you need same-day settlement for cash flow reasons, prioritize providers offering faster processing even if fees are slightly higher.

- Check global coverage: Make sure the solution supports all countries and currencies relevant to your business. Some providers excel in specific regions but have limited coverage elsewhere.

- Integration: Review integration options to understand how easily the solution connects with your existing accounting, invoicing, or e-commerce systems. Seamless integration saves time and reduces manual work.

- Compliance support: Check compliance support to verify the provider handles regulatory requirements in your operating area. This includes tax documentation, reporting, and ongoing compliance monitoring.

- Customer support: Test customer support quality and availability, especially if you operate across multiple time zones. Responsive support becomes crucial when payment issues arise.

Collect cross-border payments faster with PayGlocal

Managing international payments doesn't have to drain your resources or complicate your operations. Without the right payment solution, businesses often struggle with expensive payment transfers, delayed settlements, and complex compliance requirements that slow down growth.

- PayGlocal removes these friction points with a platform designed specifically for businesses that need reliable, cost-effective cross-border payment solutions.

- Multi-currency accounts in USD, GBP, EUR, CAD: Look local to your international clients and reduce currency conversion costs with dedicated accounts in major currencies.

- 40+ global payment methods: Accept payments through local payment methods your customers trust across 180+ countries.

- Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) automatically upon settlement, removing paperwork delays and regulatory concerns.

- Zero setup fees: Start accepting international payments immediately without upfront costs. You only pay when you do the transaction

- One platform management: Handle all your international payment needs through a single dashboard, reducing complexity and administrative overhead.

Whether you're scaling your business globally or expanding in new markets, PayGlocal provides the infrastructure you need to collect payments globally while settling locally in INR.

Final thoughts

Cross-border payments are essential infrastructure for any business operating internationally. While traditional banking methods continue to serve basic needs, modern payment platforms offer significant advantages in cost, speed, and user experience.

The key to success is choosing a solution that matches your specific business requirements. Consider your transaction patterns, growth plans, and operational needs when evaluating providers. PayGlocal offers a complete, all-in-one platform to manage your global transactions.

Ready to enhance your international payment collection processes and focus on growing your business? Get started with PayGlocal today.