GST collections reached a record ₹22.08 lakh crore( in 2024-25, growing 9.4% year-on-year. This indicates that an

increasing number of businesses are ensuring proper tax compliance and filing their returns on time.

Filing ITC refers to the process of submitting various GST forms that allow businesses to claim, transfer, or declare input tax credit. Whether you're a newly registered business claiming opening credit or managing job work transactions, knowing the correct filing procedure can save you from penalties and ensure smooth cash flow.

In this guide, we cover everything you need to know about filing ITC forms, from eligibility requirements to step-by-step procedures, so you can handle your GST compliance effectively.

Key Takeaways:

Filing ITC means submitting specific GST forms to claim, transfer, or declare input tax credit with the tax authorities. The GST system includes several ITC forms designed for different business scenarios and compliance requirements.

Input Tax Credit allows businesses to offset the tax paid on purchases against the tax liability on sales. However, certain situations require filing dedicated ITC forms beyond regular GST returns. For example, when you register for GST and have existing stock, you need to file ITC-01 to claim credit on that inventory.

ITC filing follows a structured process that varies by form type but generally involves data preparation, online submission, and verification steps. The process requires careful attention to documentation and timeline requirements.

Here's how the general ITC filing process works:

Let’s take a detailed look at each of the ITC forms:

ITC-01 allows newly registered taxpayers to claim input tax credit on goods held in stock before registration. You can file this form if you applied for registration within 30 days of becoming liable or took voluntary registration.

The form requires detailed information about each invoice, including supplier GSTIN, invoice numbers, dates, and tax amounts. You must provide descriptions of inputs, quantities, and the ITC amount claimed for central tax, state tax, integrated tax, and cess.

For example, if you registered for GST in March and had raw materials worth ₹2 lakh in stock with ₹36,000 GST paid, you can claim this ₹36,000 as opening credit through ITC-01. This helps reduce your initial tax burden and improves cash flow during the early stages of GST compliance.

ITC-02A enables the transfer of unutilized input tax credit between different registrations of the same business entity within the same state.

This applies when you have multiple places of business in a state with separate GST registrations. The transferor entity files this form within 30 days of obtaining new registration, and the transferee entity then accepts or rejects the transfer request. Once accepted, the credit moves from one electronic credit ledger to another.

For instance, if your Delhi head office has excess credit of ₹5 lakh and your Delhi warehouse needs ₹3 lakh for tax payment, you can transfer the required amount using ITC-02A to optimize credit utilization across locations.

ITC-03 is used to pay back input tax credit when businesses switch to the composition scheme or when their supplies become exempt from GST. The form requires detailed information about goods for which credit was previously claimed.

For example, if you switch to the composition scheme and previously claimed ₹1 lakh credit on stock worth ₹10 lakh, you must pay back this ₹1 lakh through ITC-03 along with details of all relevant invoices and goods.

ITC-04 tracks goods sent to job workers for processing through quarterly or half-yearly submissions, depending on your business turnover.

For instance, if you send ₹50,000 worth of components to a job worker in April, receive finished goods worth ₹75,000 in June, and sell some directly from the job worker's premises, all these movements must be reported in ITC-04 to maintain your credit claims and comply with job work regulations.

Different businesses have varying ITC filing requirements based on their registration status, business activities, and specific circumstances. The following businesses typically need to file ITC forms:

ITC filing allows businesses to claim credit on various types of purchases made for business purposes.

Here's what you can typically claim through ITC forms:

The GST regulations clearly define which purchases qualify for input tax credit and which don't. This helps businesses plan procurement and credit claiming strategies effectively. Here's a quick overview of what you can and cannot claim as ITC:

Proper ITC filing provides significant financial and operational advantages for businesses. These benefits directly impact cash flow, compliance status, and overall business efficiency.

Some of the key advantages include:

Filing ITC forms requires specific procedures for each form type. While the basic portal navigation remains similar, each form has unique requirements and data entry steps that businesses must complete correctly.

Here's how to file different ITC forms properly:

ITC-01 helps newly registered businesses claim credit on existing stock when they start GST compliance. The process involves entering detailed invoice information and verifying eligibility criteria.

Follow these steps to file ITC-01 successfully:

1. Portal access: Login to the GST portal with your credentials, navigate to Services > Returns > ITC Forms, and click "PREPARE ONLINE" on the ITC-01 tile.

2. Section selection: Choose Section 18(1)(a) for businesses that applied for registration within 30 days of becoming liable, as this is the most common scenario.

3. Invoice entry: Input supplier GSTIN, invoice number, invoice date, goods type, description of inputs, unit quantity code, quantity, and invoice value for each transaction.

4. Tax details: Enter ITC claimed amounts separately for CGST, SGST/UTGST, IGST, and cess, ensuring the total doesn't exceed the invoice value.

5. Multiple entries: Click "ADD" after each invoice entry, then "SAVE" to store all information before proceeding to the next invoice.

6. Preview and submit: Use "PREVIEW" to review your complete form, verify all details are correct, then click "SUBMIT" to freeze the data permanently.

7. Professional certification: Upload CA or Cost Accountant certificate if claiming more than ₹2 lakh, including firm details, professional name, and membership number.

8. Final filing: Complete the declaration, select an authorized signatory, and file using DSC or EVC verification to generate your ARN.

ITC-02A allows businesses with multiple locations to move unutilized credit between different registrations. This process involves both the transferor and the transferee entities taking specific actions.

Complete these steps for successful credit transfer:

1. Transfer initiation: Login as the transferor entity, access the ITC-02A form, and click "TRANSFER ITC" to start the process.

2. Transferee details: Enter the GSTIN of the transferee entity, which auto-populates their legal name and trade name for verification.

3. Credit specification: Review available credit balances, then enter specific amounts to transfer for CGST, SGST, IGST, and cess as needed.

4. Transfer submission: Save the transfer details, preview the form, complete declarations, and file using DSC or EVC verification.

5. Acceptance process: The transferee entity receives notification, logs into their account, and views pending transfer requests under "TAKE ACTION".

6. Decision making: Transferee reviews transfer amounts and either accepts or rejects the request based on their credit requirements.

7. Final confirmation: Complete the acceptance/rejection process with proper authorization and verification to finalize the transfer.

ITC-03 requires businesses to pay back previously claimed credit when switching to the composition scheme or when supplies become exempt. The form has two sections for different scenarios.

Here's how to file ITC-03 correctly:

1. Portal navigation: Access the GST portal, go to ITC Forms, and select "PREPARE ONLINE" for ITC-03.

2. Section choice: Select Section 18(4)(a) for composition scheme transition or Section 18(4)(b) for exempt supply situations.

3. Nil return option: Choose "File Nil GST ITC-03" if you have no credit to reverse, complete declarations, and submit directly.

4. Invoice details: For regular filing, enter supplier information, invoice numbers, dates, and goods details in the "Goods Details With Invoices" section.

5. Bulk entry: Use "Goods Details Without Invoices" for summary entries when specific invoice details aren't available for all items.

6. CA certification: Upload professional certification if required, including CA/Cost Accountant details and certificate in JPEG format.

7. Payment calculation: Review ITC payable amounts, utilize available cash and credit balances, and create challans for additional payments if needed.

8. Payment processing: Complete payment through the electronic cash ledger or create new challans for insufficient balance situations.

9. Final submission: File the return with proper authorization after making all required payments and completing verification.

ITC-04 maintains records of goods sent to job workers and helps track credit eligibility on materials used in job work arrangements. The form requires detailed challan and movement information.

Complete these steps for proper ITC-04 filing:

1. Form access: Log in to the GST portal, select the appropriate financial year and return period, then click "PREPARE ONLINE" for ITC-04.

2. Job worker classification: Identify whether your job workers are registered or unregistered, as this affects the information required for each entry.

3. Goods dispatched: Complete Table 4 with details of inputs and capital goods sent to job workers, including challan numbers, dates, and item descriptions.

4. Goods received: Fill Table 5A for items received back from the same job worker who originally received them, including any losses or wastages.

5. Inter-worker transfers: Use Table 5B for goods received from different job workers than those who originally received the materials.

6. Direct supplies: Complete Table 5C for goods supplied directly from job worker premises to customers, maintaining proper invoice records.

7. Documentation: Ensure all entries match physical challans, maintain transport documents, and keep job work agreements for reference.

8. Review and submit: Preview all tables, verify challan details match actual movements, and file with proper authorization and verification.

Making errors during ITC filing that lead to rejections, delays, or compliance issues. Avoiding these frequent filing errors can save time and prevent compliance problems:

Proper documentation forms the foundation of successful ITC filing. Missing or incorrect documents can lead to rejections, penalties, or delayed processing.

Essential documents vary by form type but generally include tax invoices, delivery challans, proof of tax payment, and business registration documents.

Primary documentation requirements includes:

Apart from the main documents, you will also need supporting documents, including bank statements showing payments to suppliers, transport documents for goods movement, and correspondence with job workers to support your filing.

Maintain digital copies of all documents, as the GST portal may require uploads during verification. For businesses with international transactions, ensure FIRC and other compliance documents are readily available. This documentation becomes particularly important when dealing with export-import activities requiring additional scrutiny.

Managing international payments while handling compliance documentation can be challenging for growing businesses. Traditional payment methods often involve multiple platforms, unclear fee structures, and delayed documentation that complicates tax filing procedures.

PayGlocal provides a unified solution that makes global payment collection simple while supporting your business growth needs. Here's what PayGlocal offers for your business:

Whether you're collecting payments from international clients or managing complex business transactions, PayGlocal significantly enhances your payment management processes.

Filing ITC forms doesn't have to be complex when you know the requirements and follow systematic approaches. Whether claiming opening credit through ITC-01, managing job work with ITC-04, or transferring credit via ITC-02A, proper documentation and timely filing protect your business interests.

For businesses operating internationally, having reliable payment collection systems becomes essential for maintaining proper documentation and cash flow. PayGlocal offers solutions that simplify global payment operations while providing the documentation businesses need for compliance and financial management.

Most successful businesses already use integrated payment solutions to handle their international transactions efficiently. Ready to join them and simplify your global payment collection processes? Get started with PayGlocal today.

increasing number of businesses are ensuring proper tax compliance and filing their returns on time.

Filing ITC refers to the process of submitting various GST forms that allow businesses to claim, transfer, or declare input tax credit. Whether you're a newly registered business claiming opening credit or managing job work transactions, knowing the correct filing procedure can save you from penalties and ensure smooth cash flow.

In this guide, we cover everything you need to know about filing ITC forms, from eligibility requirements to step-by-step procedures, so you can handle your GST compliance effectively.

Key Takeaways:

- ITC-01 filing: Required within specific timeframes for newly registered businesses to claim opening credit on existing stock.

- Job work compliance: ITC-04 must be filed quarterly or half-yearly, depending on turnover, to track goods sent for job work.

- Transfer procedures: ITC-02A enables credit transfer between multiple business locations under the same registration.

- Global payment collection: PayGlocal helps businesses collect international payments efficiently while maintaining proper documentation for GST filing.

What does an ITC filing in GST mean?

Filing ITC means submitting specific GST forms to claim, transfer, or declare input tax credit with the tax authorities. The GST system includes several ITC forms designed for different business scenarios and compliance requirements.

Input Tax Credit allows businesses to offset the tax paid on purchases against the tax liability on sales. However, certain situations require filing dedicated ITC forms beyond regular GST returns. For example, when you register for GST and have existing stock, you need to file ITC-01 to claim credit on that inventory.

How does ITC filing work in GST?

ITC filing follows a structured process that varies by form type but generally involves data preparation, online submission, and verification steps. The process requires careful attention to documentation and timeline requirements.

Here's how the general ITC filing process works:

- Data preparation: Collect all relevant invoices, challans, and supporting documents required for your specific ITC form type.

- Portal access: Log in to the GST portal using your credentials and navigate to the appropriate ITC form section.

- Information entry: Input supplier details, transaction information, tax amounts, and other required data fields accurately.

- Verification: Review entered data, preview the form, and ensure all information matches your source documents.

- Submission: Submit the form using a digital signature or electronic verification code after completing declaration requirements.

- Confirmation: Receive acknowledgment receipt number (ARN) and monitor processing status through the portal.

What are the different types of ITC forms you can file?

Let’s take a detailed look at each of the ITC forms:

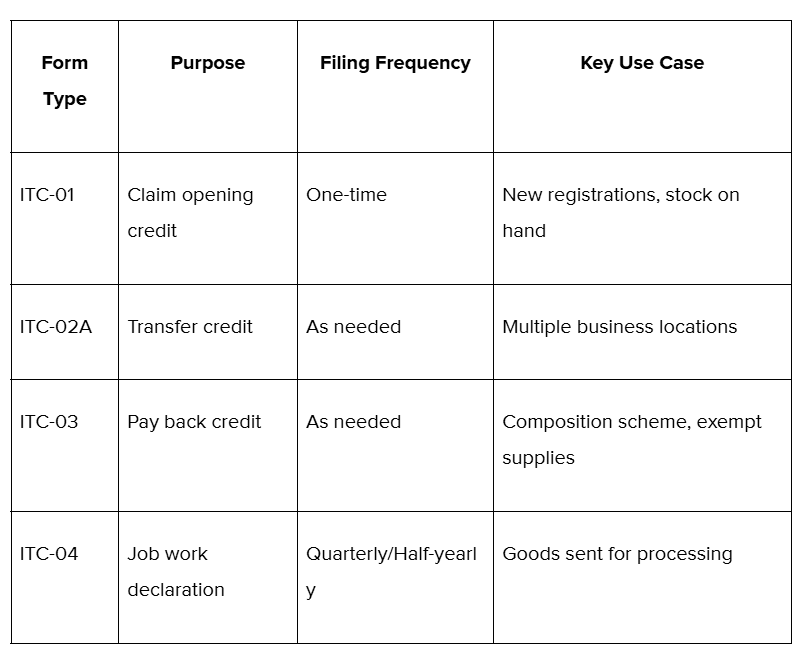

1. ITC-01: Opening credit claim

ITC-01 allows newly registered taxpayers to claim input tax credit on goods held in stock before registration. You can file this form if you applied for registration within 30 days of becoming liable or took voluntary registration.

The form requires detailed information about each invoice, including supplier GSTIN, invoice numbers, dates, and tax amounts. You must provide descriptions of inputs, quantities, and the ITC amount claimed for central tax, state tax, integrated tax, and cess.

For example, if you registered for GST in March and had raw materials worth ₹2 lakh in stock with ₹36,000 GST paid, you can claim this ₹36,000 as opening credit through ITC-01. This helps reduce your initial tax burden and improves cash flow during the early stages of GST compliance.

2. ITC-02A: Credit transfer between locations

ITC-02A enables the transfer of unutilized input tax credit between different registrations of the same business entity within the same state.

This applies when you have multiple places of business in a state with separate GST registrations. The transferor entity files this form within 30 days of obtaining new registration, and the transferee entity then accepts or rejects the transfer request. Once accepted, the credit moves from one electronic credit ledger to another.

For instance, if your Delhi head office has excess credit of ₹5 lakh and your Delhi warehouse needs ₹3 lakh for tax payment, you can transfer the required amount using ITC-02A to optimize credit utilization across locations.

3. ITC-03: Credit reversal for scheme changes

ITC-03 is used to pay back input tax credit when businesses switch to the composition scheme or when their supplies become exempt from GST. The form requires detailed information about goods for which credit was previously claimed.

For example, if you switch to the composition scheme and previously claimed ₹1 lakh credit on stock worth ₹10 lakh, you must pay back this ₹1 lakh through ITC-03 along with details of all relevant invoices and goods.

4. ITC-04: Job work compliance

ITC-04 tracks goods sent to job workers for processing through quarterly or half-yearly submissions, depending on your business turnover.

For instance, if you send ₹50,000 worth of components to a job worker in April, receive finished goods worth ₹75,000 in June, and sell some directly from the job worker's premises, all these movements must be reported in ITC-04 to maintain your credit claims and comply with job work regulations.

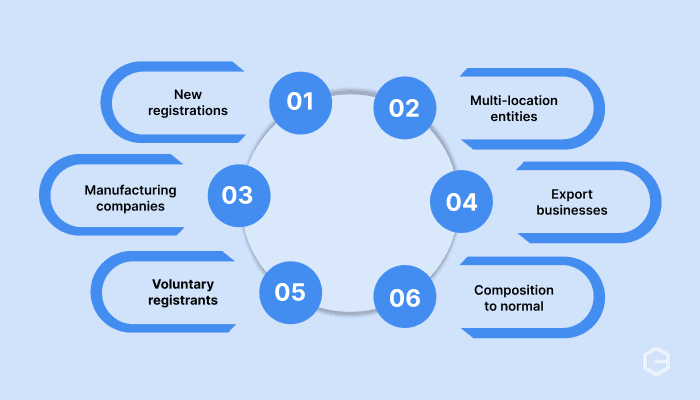

Who needs to file ITC forms?

Different businesses have varying ITC filing requirements based on their registration status, business activities, and specific circumstances. The following businesses typically need to file ITC forms:

- New registrations: Businesses registering for GST who have existing stock and want to claim opening credit.

- Multi-location entities: Companies with separate registrations in the same state need ITC-02A for credit transfers.

- Manufacturing companies: Manufacturers sending goods to job workers must file ITC-04 to track movement and credit claims.

- Export businesses: Exporters often need ITC-03 for refund claims when they have excess input credit.

- Voluntary registrants: Businesses taking voluntary GST registration can claim opening credit through ITC-01.

- Composition to normal: Entities switching from the composition scheme to normal taxation need ITC-01 for stock credit.

What can you claim through an ITC filing?

ITC filing allows businesses to claim credit on various types of purchases made for business purposes.

Here's what you can typically claim through ITC forms:

- Input goods: Raw materials, components, and other goods used in manufacturing or business operations.

- Input services: Professional services, transportation, rent, and other services used for business purposes.

- Capital goods: Plant, machinery, equipment, and other capital assets used in business operations.

- Opening stock: Goods held in inventory at the time of GST registration or scheme changes.

- Job work inputs: Materials sent to job workers for processing, subject to compliance requirements.

- Fuel and power: Electricity, fuel, and power used in manufacturing processes or business operations.

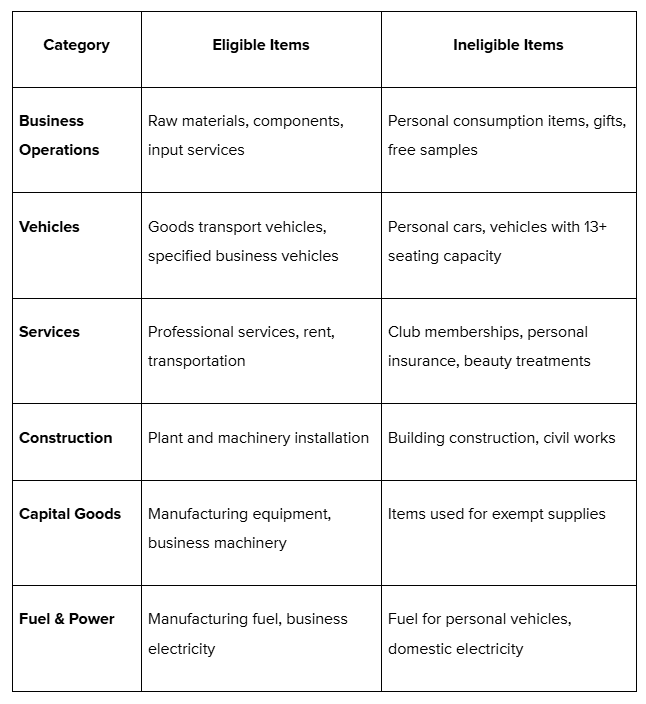

What are the eligible and ineligible items for ITC?

The GST regulations clearly define which purchases qualify for input tax credit and which don't. This helps businesses plan procurement and credit claiming strategies effectively. Here's a quick overview of what you can and cannot claim as ITC:

What are the benefits of filing ITC correctly?

Proper ITC filing provides significant financial and operational advantages for businesses. These benefits directly impact cash flow, compliance status, and overall business efficiency.

Some of the key advantages include:

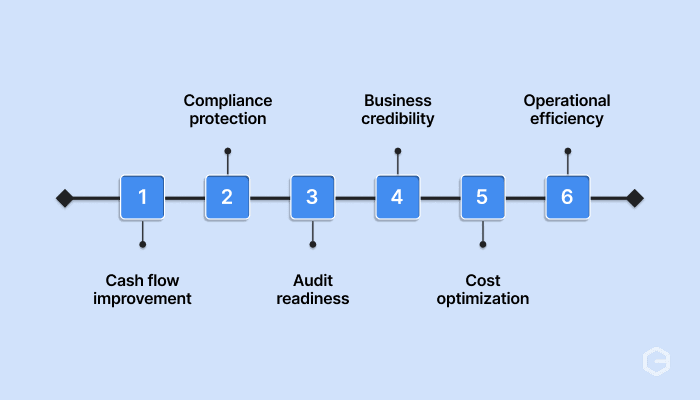

- Cash flow improvement: Reduces actual tax burden by offsetting input tax against output tax liability.

- Compliance protection: Ensures adherence to GST regulations and avoids penalties or legal issues.

- Audit readiness: Maintains proper documentation trail for tax authority reviews and assessments.

- Business credibility: Demonstrates professional tax management to suppliers, customers, and financial institutions.

- Cost optimization: Maximizes legitimate tax savings through proper credit utilization and planning.

- Operational efficiency: Creates systematic processes for purchase documentation and tax management.

How to file different ITC forms?

Filing ITC forms requires specific procedures for each form type. While the basic portal navigation remains similar, each form has unique requirements and data entry steps that businesses must complete correctly.

Here's how to file different ITC forms properly:

Steps for filing the ITC-01 form for opening a credit

ITC-01 helps newly registered businesses claim credit on existing stock when they start GST compliance. The process involves entering detailed invoice information and verifying eligibility criteria.

Follow these steps to file ITC-01 successfully:

1. Portal access: Login to the GST portal with your credentials, navigate to Services > Returns > ITC Forms, and click "PREPARE ONLINE" on the ITC-01 tile.

2. Section selection: Choose Section 18(1)(a) for businesses that applied for registration within 30 days of becoming liable, as this is the most common scenario.

3. Invoice entry: Input supplier GSTIN, invoice number, invoice date, goods type, description of inputs, unit quantity code, quantity, and invoice value for each transaction.

4. Tax details: Enter ITC claimed amounts separately for CGST, SGST/UTGST, IGST, and cess, ensuring the total doesn't exceed the invoice value.

5. Multiple entries: Click "ADD" after each invoice entry, then "SAVE" to store all information before proceeding to the next invoice.

6. Preview and submit: Use "PREVIEW" to review your complete form, verify all details are correct, then click "SUBMIT" to freeze the data permanently.

7. Professional certification: Upload CA or Cost Accountant certificate if claiming more than ₹2 lakh, including firm details, professional name, and membership number.

8. Final filing: Complete the declaration, select an authorized signatory, and file using DSC or EVC verification to generate your ARN.

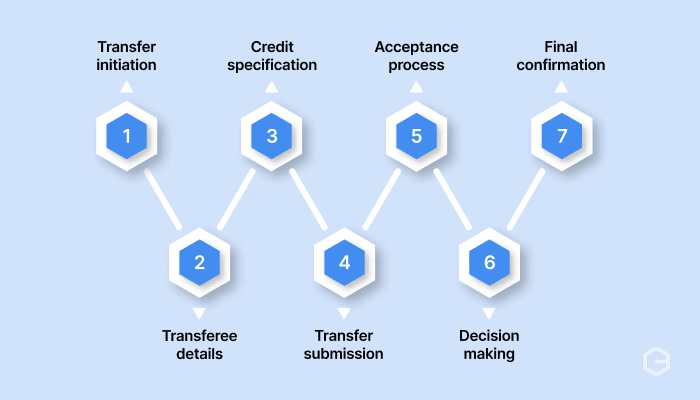

Steps for filing the ITC-02A form for credit transfers

ITC-02A allows businesses with multiple locations to move unutilized credit between different registrations. This process involves both the transferor and the transferee entities taking specific actions.

Complete these steps for successful credit transfer:

1. Transfer initiation: Login as the transferor entity, access the ITC-02A form, and click "TRANSFER ITC" to start the process.

2. Transferee details: Enter the GSTIN of the transferee entity, which auto-populates their legal name and trade name for verification.

3. Credit specification: Review available credit balances, then enter specific amounts to transfer for CGST, SGST, IGST, and cess as needed.

4. Transfer submission: Save the transfer details, preview the form, complete declarations, and file using DSC or EVC verification.

5. Acceptance process: The transferee entity receives notification, logs into their account, and views pending transfer requests under "TAKE ACTION".

6. Decision making: Transferee reviews transfer amounts and either accepts or rejects the request based on their credit requirements.

7. Final confirmation: Complete the acceptance/rejection process with proper authorization and verification to finalize the transfer.

Steps for filing the ITC-03 form for credit reversal

ITC-03 requires businesses to pay back previously claimed credit when switching to the composition scheme or when supplies become exempt. The form has two sections for different scenarios.

Here's how to file ITC-03 correctly:

1. Portal navigation: Access the GST portal, go to ITC Forms, and select "PREPARE ONLINE" for ITC-03.

2. Section choice: Select Section 18(4)(a) for composition scheme transition or Section 18(4)(b) for exempt supply situations.

3. Nil return option: Choose "File Nil GST ITC-03" if you have no credit to reverse, complete declarations, and submit directly.

4. Invoice details: For regular filing, enter supplier information, invoice numbers, dates, and goods details in the "Goods Details With Invoices" section.

5. Bulk entry: Use "Goods Details Without Invoices" for summary entries when specific invoice details aren't available for all items.

6. CA certification: Upload professional certification if required, including CA/Cost Accountant details and certificate in JPEG format.

7. Payment calculation: Review ITC payable amounts, utilize available cash and credit balances, and create challans for additional payments if needed.

8. Payment processing: Complete payment through the electronic cash ledger or create new challans for insufficient balance situations.

9. Final submission: File the return with proper authorization after making all required payments and completing verification.

Steps for filing the ITC-04 form for job work

ITC-04 maintains records of goods sent to job workers and helps track credit eligibility on materials used in job work arrangements. The form requires detailed challan and movement information.

Complete these steps for proper ITC-04 filing:

1. Form access: Log in to the GST portal, select the appropriate financial year and return period, then click "PREPARE ONLINE" for ITC-04.

2. Job worker classification: Identify whether your job workers are registered or unregistered, as this affects the information required for each entry.

3. Goods dispatched: Complete Table 4 with details of inputs and capital goods sent to job workers, including challan numbers, dates, and item descriptions.

4. Goods received: Fill Table 5A for items received back from the same job worker who originally received them, including any losses or wastages.

5. Inter-worker transfers: Use Table 5B for goods received from different job workers than those who originally received the materials.

6. Direct supplies: Complete Table 5C for goods supplied directly from job worker premises to customers, maintaining proper invoice records.

7. Documentation: Ensure all entries match physical challans, maintain transport documents, and keep job work agreements for reference.

8. Review and submit: Preview all tables, verify challan details match actual movements, and file with proper authorization and verification.

What are some common filing mistakes to avoid?

Making errors during ITC filing that lead to rejections, delays, or compliance issues. Avoiding these frequent filing errors can save time and prevent compliance problems:

- Incorrect GSTIN entries: Double-check supplier GSTIN numbers match exactly with their registrations and filings.

- Mismatched dates: Ensure invoice dates, challan dates, and reporting periods align correctly across all entries.

- Wrong classifications: Use correct HSN codes, tax rates, and goods/services categories as per GST classification rules.

- Incomplete documentation: Maintain complete records, including invoices, proof of payment, delivery documents, and supporting papers.

- Timeline violations: File forms within prescribed deadlines to avoid losing credit claims or facing penalties.

- Calculation errors: Verify tax amounts, credit claims, and numerical entries match source documents accurately.

- Missing signatures: Complete digital signing or EVC verification properly to ensure successful form submission.

What documents do you need for filing ITC forms?

Proper documentation forms the foundation of successful ITC filing. Missing or incorrect documents can lead to rejections, penalties, or delayed processing.

Essential documents vary by form type but generally include tax invoices, delivery challans, proof of tax payment, and business registration documents.

Primary documentation requirements includes:

- Tax invoices: Original invoices from suppliers showing GSTIN, tax amounts, and transaction details.

- Delivery challans: For ITC-04, challans showing goods movement to and from job workers.

- Payment proof: Evidence that tax has been paid by the supplier to the government.

- Stock registers: Detailed records of inventory with quantities, values, and tax components.

- Professional certificates: CA/CPA certification for claims exceeding ₹2 lakh in ITC-01.

Apart from the main documents, you will also need supporting documents, including bank statements showing payments to suppliers, transport documents for goods movement, and correspondence with job workers to support your filing.

Maintain digital copies of all documents, as the GST portal may require uploads during verification. For businesses with international transactions, ensure FIRC and other compliance documents are readily available. This documentation becomes particularly important when dealing with export-import activities requiring additional scrutiny.

Get paid globally with instant compliance documentation

Managing international payments while handling compliance documentation can be challenging for growing businesses. Traditional payment methods often involve multiple platforms, unclear fee structures, and delayed documentation that complicates tax filing procedures.

PayGlocal provides a unified solution that makes global payment collection simple while supporting your business growth needs. Here's what PayGlocal offers for your business:

- Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD for faster settlement and better exchange rates.

- One platform management: Handle all payment operations from one dashboard with real-time tracking, removing the need to switch between multiple systems.

- Transparent pricing: Pay only when you transact with no setup fees, platform charges, or hidden costs. This helps you predict expenses and manage cash flow better.

- Instant FIRC generation after fund settlement: Get an immediate FIRC (Foreign Inward Remittance Certificate), keeping your export documentation organized for GST and regulatory compliance.

- Global payment methods: Offer 40+ payment options, including cards, bank transfers, and local payment methods that let customers pay using their preferred options.

Whether you're collecting payments from international clients or managing complex business transactions, PayGlocal significantly enhances your payment management processes.

Final thoughts

Filing ITC forms doesn't have to be complex when you know the requirements and follow systematic approaches. Whether claiming opening credit through ITC-01, managing job work with ITC-04, or transferring credit via ITC-02A, proper documentation and timely filing protect your business interests.

For businesses operating internationally, having reliable payment collection systems becomes essential for maintaining proper documentation and cash flow. PayGlocal offers solutions that simplify global payment operations while providing the documentation businesses need for compliance and financial management.

Most successful businesses already use integrated payment solutions to handle their international transactions efficiently. Ready to join them and simplify your global payment collection processes? Get started with PayGlocal today.