If you’ve worked with international clients, run a business that sells overseas, or received money from family abroad, you’ve likely come across the process already. It’s a common part of how people in India get paid from other countries, whether for work, support, or personal reasons.

The money usually comes through a bank or a trusted platform like PayGlocal, Wise or PayPal and is credited to your Indian bank account in rupees. While the process is fairly straightforward, it helps to know the steps, like sharing the right bank details, knowing what a UTR number is, and how long it typically takes for the money to arrive.

Whether you’re a freelancer, a business owner, or just someone receiving support from family overseas, understanding how foreign inward remittance works can save you time and stress. This guide breaks it down in a simple, clear way—covering the process, common terms, and examples to help you feel confident about receiving money from abroad.

The International Monetary Fund (IMF) defines these remittances as cross-border transfers, often sent by expatriates to their home countries, where they not only sustain families but also catalyze investments across multiple sectors.

When money is wired into a bank located in India from overseas, it's not just a simple transfer – it's a vital boost for the economy. Known as foreign inward remittances, these transactions infuse essential capital that bolsters foreign exchange reserves and fuels the country's economy.

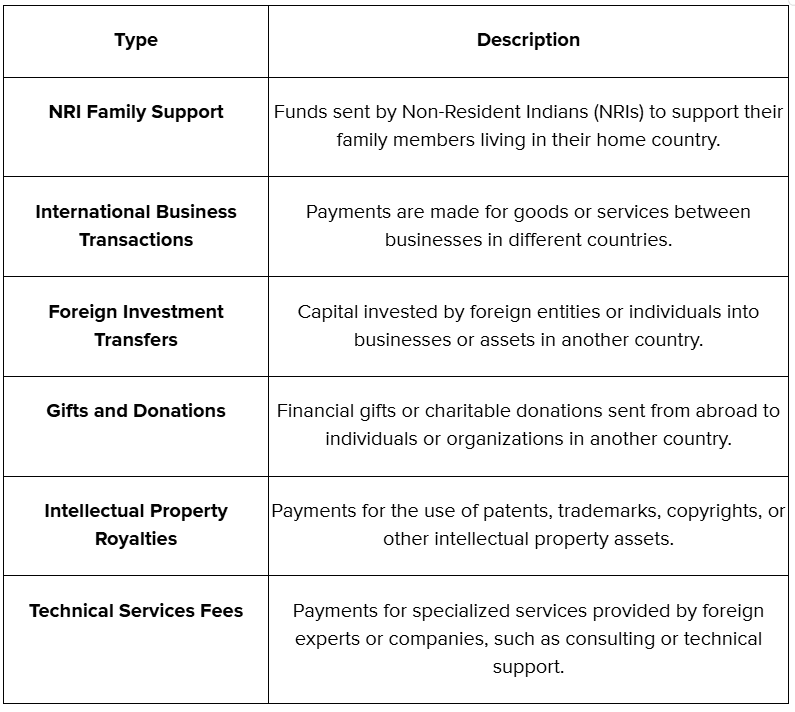

These funds can help with capacity-building and grow your business revenue and financial potential. Whether for personal support, business dealings, or investments, these remittances play a major role in the nation's economic health. Here are a few types of foreign inward remittances:

Examples of Foreign Inward Remittance:

Table depicts various example types of foreign inward remittances.

1. Foreign Exchange Inflows:

Remittances help strengthen India’s foreign exchange reserves, which are essential for international trade and maintaining the value of the rupee.

2. Economic Stability and Growth:

Regular inflows of foreign currency stabilize the economy, reduce the need for borrowing, and support infrastructure development.

3. Improved Living Standards:

For many families, remittances are a lifeline, improving their access to education, healthcare, and basic amenities.

4. Investment and Entrepreneurship:

Remittances often fund small businesses and entrepreneurial ventures, boosting local economies and creating jobs.

Also read: Understanding Nostro and Vostro Accounts

1. Income Tax Regulations:

If the remitted amount is categorized as income, it may be subject to income tax in India. This is particularly relevant for funds received as part of business transactions or compensation for services rendered.

2. Gift Tax Considerations:

When receiving a large sum of money as a gift, gift tax may be applicable based on the relationship between the sender and recipient. Gifts from non-relatives or those surpassing certain thresholds could incur tax obligations. Gifts from relatives are generally exempt from tax, but if the amount exceeds ₹50,000 and is not from a relative, the entire sum becomes taxable.

3. Double Taxation Relief:

Double Taxation Avoidance Agreements (DTAAs) are in place to prevent the same income from being taxed both in India and the country of origin. These agreements ensure that you do not face double taxation on the same income, providing relief under specific circumstances.

4. Tax on Gifts from Non-Close Relatives:

Receiving funds from individuals who are not considered close relatives may have tax implications. The Income Tax Act outlines specific rules regarding gifts from non-relatives, and such remittances could be classified as taxable income.

5. Tax Deducted at Source (TDS):

Certain types of inward remittances may require Tax Deducted at Source (TDS). In these cases, a percentage of the amount is withheld as tax before the funds are credited to your account, ensuring compliance with tax regulations.

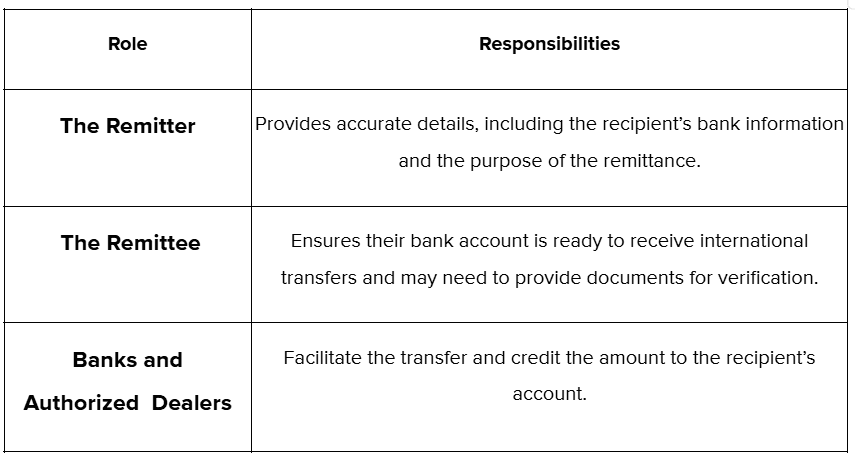

Let us quickly dive into how Foreign Inward Remittance works when put into practice:

The table depicts various roles involved in the process of Inward Remittance

Also read: Why alternate payment methods matter?

This process ensures that international remittances are handled securely and in accordance with regulatory standards. Listed out are the steps involved:

Sender Initiation

The sender initiates the remittance by instructing their bank or financial institution to transfer funds to the recipient. This involves providing the necessary details, such as the recipient's bank account information and the amount to be sent.

Currency Conversion

If the remittance is in a different currency from the recipient's local currency, the funds are converted into the appropriate currency. The conversion rate is determined based on the prevailing exchange rates at the time of the transaction.

Remittance to Authorized Dealer

The funds are transferred to an authorized dealer or intermediary bank that handles international transactions. This institution processes the funds and ensures they comply with both local and international regulations.

Compliance Checks

The remittance undergoes compliance checks to ensure it adheres to regulatory requirements. This includes verifying the source of funds, checking for any suspicious activities, and ensuring the transaction complies with anti-money laundering (AML) and know-your-customer (KYC) regulations.

Inward Remittance Form (IRF)

The recipient's bank or financial institution receives the funds and fills out an Inward Remittance Form (IRF). This form documents the details of the remittance, including the sender's information, the purpose of the transfer, and the amount received.

Credit to Beneficiary's Account

Once all compliance checks are completed and the IRF is processed, the funds are credited to the beneficiary's bank account. The recipient can then access and utilize the funds according to their needs.

A Foreign Inward Remittance Certificate (FIRC) is proof that a remittance has been received. It’s an important document, especially for businesses that need to show that foreign currency payments have been credited.

1. Contents of a FIRC:

An FIRC includes details like:

Sender and receiver information

2. How to Obtain a FIRC:

This procedure may vary slightly between banks. However, the general steps are as follows:

Also read: FIRC- Everything you need to know

It is important to know, there are several ways to send inward remittances. Let’s explore!

The most common method, where funds are transferred directly from one bank to another.

Services like Wise and PayPal offer quick and affordable international transfers.

These are bank drafts issued in a foreign currency and can be deposited in Indian banks.

Also read: SWIFT - The network powering international money transfer

Now we know that foreign inward remittances are more than just financial translation. Let's wrap things up!

Foreign inward remittance is like the master key that keeps families thriving, businesses booming, and economies growing. You'll ensure your remittances are smooth and secure by mastering the process, guidelines, and tax implications. Sticking to the rules is crucial for seamless transactions, whether you're the sender or the receiver. Keep these tips handy, and you'll be all set to handle any remittance adventures that come your way!

While PayGlocal doesn’t handle foreign inward remittance services directly, we can assist you in managing your business finances efficiently. Sign up today to discover our solutions.

The money usually comes through a bank or a trusted platform like PayGlocal, Wise or PayPal and is credited to your Indian bank account in rupees. While the process is fairly straightforward, it helps to know the steps, like sharing the right bank details, knowing what a UTR number is, and how long it typically takes for the money to arrive.

Whether you’re a freelancer, a business owner, or just someone receiving support from family overseas, understanding how foreign inward remittance works can save you time and stress. This guide breaks it down in a simple, clear way—covering the process, common terms, and examples to help you feel confident about receiving money from abroad.

What is Foreign Inward Remittance?

The International Monetary Fund (IMF) defines these remittances as cross-border transfers, often sent by expatriates to their home countries, where they not only sustain families but also catalyze investments across multiple sectors.

When money is wired into a bank located in India from overseas, it's not just a simple transfer – it's a vital boost for the economy. Known as foreign inward remittances, these transactions infuse essential capital that bolsters foreign exchange reserves and fuels the country's economy.

These funds can help with capacity-building and grow your business revenue and financial potential. Whether for personal support, business dealings, or investments, these remittances play a major role in the nation's economic health. Here are a few types of foreign inward remittances:

Examples of Foreign Inward Remittance:

Table depicts various example types of foreign inward remittances.

Economic and Social Impact of Foreign Inward Remittance

1. Foreign Exchange Inflows:

Remittances help strengthen India’s foreign exchange reserves, which are essential for international trade and maintaining the value of the rupee.

2. Economic Stability and Growth:

Regular inflows of foreign currency stabilize the economy, reduce the need for borrowing, and support infrastructure development.

3. Improved Living Standards:

For many families, remittances are a lifeline, improving their access to education, healthcare, and basic amenities.

4. Investment and Entrepreneurship:

Remittances often fund small businesses and entrepreneurial ventures, boosting local economies and creating jobs.

Also read: Understanding Nostro and Vostro Accounts

Tax Implications for Foreign Inward Remittance

1. Income Tax Regulations:

If the remitted amount is categorized as income, it may be subject to income tax in India. This is particularly relevant for funds received as part of business transactions or compensation for services rendered.

2. Gift Tax Considerations:

When receiving a large sum of money as a gift, gift tax may be applicable based on the relationship between the sender and recipient. Gifts from non-relatives or those surpassing certain thresholds could incur tax obligations. Gifts from relatives are generally exempt from tax, but if the amount exceeds ₹50,000 and is not from a relative, the entire sum becomes taxable.

3. Double Taxation Relief:

Double Taxation Avoidance Agreements (DTAAs) are in place to prevent the same income from being taxed both in India and the country of origin. These agreements ensure that you do not face double taxation on the same income, providing relief under specific circumstances.

4. Tax on Gifts from Non-Close Relatives:

Receiving funds from individuals who are not considered close relatives may have tax implications. The Income Tax Act outlines specific rules regarding gifts from non-relatives, and such remittances could be classified as taxable income.

5. Tax Deducted at Source (TDS):

Certain types of inward remittances may require Tax Deducted at Source (TDS). In these cases, a percentage of the amount is withheld as tax before the funds are credited to your account, ensuring compliance with tax regulations.

Let us quickly dive into how Foreign Inward Remittance works when put into practice:

Key Players in Foreign Inward Remittance

The table depicts various roles involved in the process of Inward Remittance

Also read: Why alternate payment methods matter?

This process ensures that international remittances are handled securely and in accordance with regulatory standards. Listed out are the steps involved:

Process Flow of Foreign Inward Remittance

Sender Initiation

The sender initiates the remittance by instructing their bank or financial institution to transfer funds to the recipient. This involves providing the necessary details, such as the recipient's bank account information and the amount to be sent.

Currency Conversion

If the remittance is in a different currency from the recipient's local currency, the funds are converted into the appropriate currency. The conversion rate is determined based on the prevailing exchange rates at the time of the transaction.

Remittance to Authorized Dealer

The funds are transferred to an authorized dealer or intermediary bank that handles international transactions. This institution processes the funds and ensures they comply with both local and international regulations.

Compliance Checks

The remittance undergoes compliance checks to ensure it adheres to regulatory requirements. This includes verifying the source of funds, checking for any suspicious activities, and ensuring the transaction complies with anti-money laundering (AML) and know-your-customer (KYC) regulations.

Inward Remittance Form (IRF)

The recipient's bank or financial institution receives the funds and fills out an Inward Remittance Form (IRF). This form documents the details of the remittance, including the sender's information, the purpose of the transfer, and the amount received.

Credit to Beneficiary's Account

Once all compliance checks are completed and the IRF is processed, the funds are credited to the beneficiary's bank account. The recipient can then access and utilize the funds according to their needs.

A Foreign Inward Remittance Certificate (FIRC) is proof that a remittance has been received. It’s an important document, especially for businesses that need to show that foreign currency payments have been credited.

Foreign Inward Remittance Certificate (FIRC)

1. Contents of a FIRC:

An FIRC includes details like:

Sender and receiver information

- Remittance date and amount

- Bank details

- Purpose of remittance

- Exchange rate used

2. How to Obtain a FIRC:

This procedure may vary slightly between banks. However, the general steps are as follows:

- Requesting a Foreign Inward Remittance Certificate (FIRC) from the bank after receiving the remittance.

- Providing the required details of the transaction.

- Paying a nominal fee, if applicable.

Also read: FIRC- Everything you need to know

It is important to know, there are several ways to send inward remittances. Let’s explore!

Methods of Sending Inward Remittances

- International Bank Transfers:

The most common method, where funds are transferred directly from one bank to another.

- Online Money Transfer Providers:

Services like Wise and PayPal offer quick and affordable international transfers.

- Foreign Currency Demand Drafts (FCDDs):

These are bank drafts issued in a foreign currency and can be deposited in Indian banks.

Also read: SWIFT - The network powering international money transfer

Now we know that foreign inward remittances are more than just financial translation. Let's wrap things up!

Conclusion

Foreign inward remittance is like the master key that keeps families thriving, businesses booming, and economies growing. You'll ensure your remittances are smooth and secure by mastering the process, guidelines, and tax implications. Sticking to the rules is crucial for seamless transactions, whether you're the sender or the receiver. Keep these tips handy, and you'll be all set to handle any remittance adventures that come your way!

While PayGlocal doesn’t handle foreign inward remittance services directly, we can assist you in managing your business finances efficiently. Sign up today to discover our solutions.