Global payments in India have been growing significantly in recent years. In fact, 49% of global real-time payment transactions occurred in India.

Whether you're a freelancer receiving payments from international clients or an enterprise managing complex multi-currency operations, knowing how global transactions work can significantly impact your business efficiency.

In this guide, we break down everything you need to know about global transactions, from basic concepts to choosing the right platform that can help you enhance your international payment processes.

A global transaction is a distributed payment process that spans multiple systems, currencies, or geographic locations while ensuring all parts complete successfully as a single unit.

When you process an international payment, you're essentially coordinating between different banks, payment processors, and regulatory systems across borders.

For example, when an Indian software company receives payment from a US client, the transaction involves currency conversion, compliance checks, SWIFT messaging, and settlement across different banking systems.

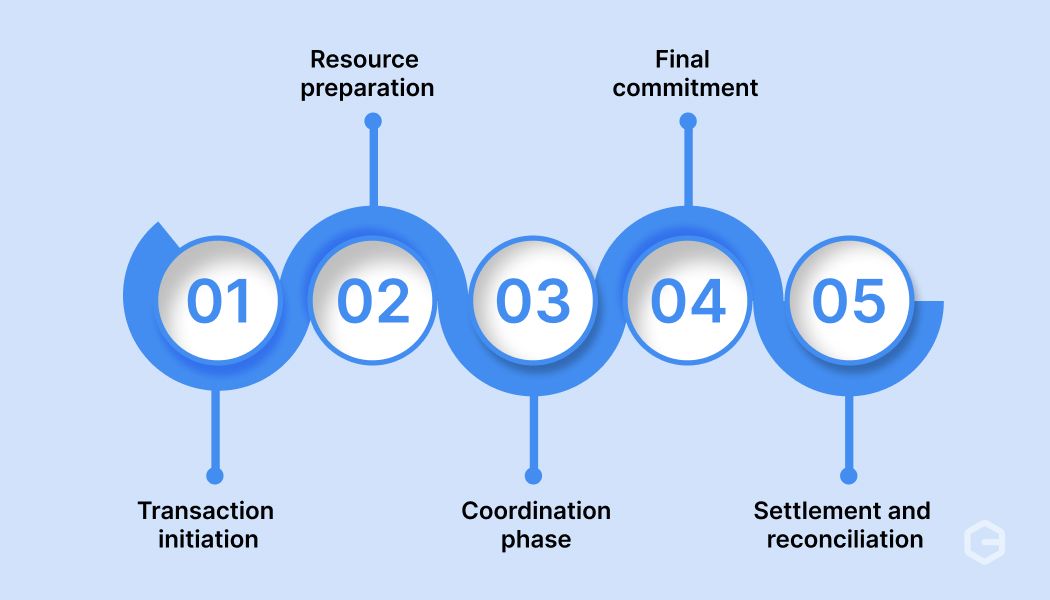

The process starts when a customer initiates an international payment through your checkout system. Your payment system creates a unique Global Transaction Identifier (GTRID) and propagates this information to all participating systems, which include your payment gateway, acquiring bank, card networks, and the customer's issuing bank.

Here's how the coordination happens:

1.Transaction initiation: Your payment system receives the international payment request and validates basic information like currency, amount, and customer details.

2. Resource preparation: Each participating system (banks, payment processors, compliance systems) receives a preparation request and validates its ability to process its portion of the transaction.

3. Coordination phase: The transaction manager collects responses from all systems. If any system cannot complete its part, the entire transaction is marked for rollback.

4. Final commitment: When all systems confirm readiness, the transaction manager sends commit instructions, making all changes permanent across all participating systems.

5. Settlement and reconciliation: Funds move between accounts, compliance documents are generated automatically, and all systems update their records simultaneously.

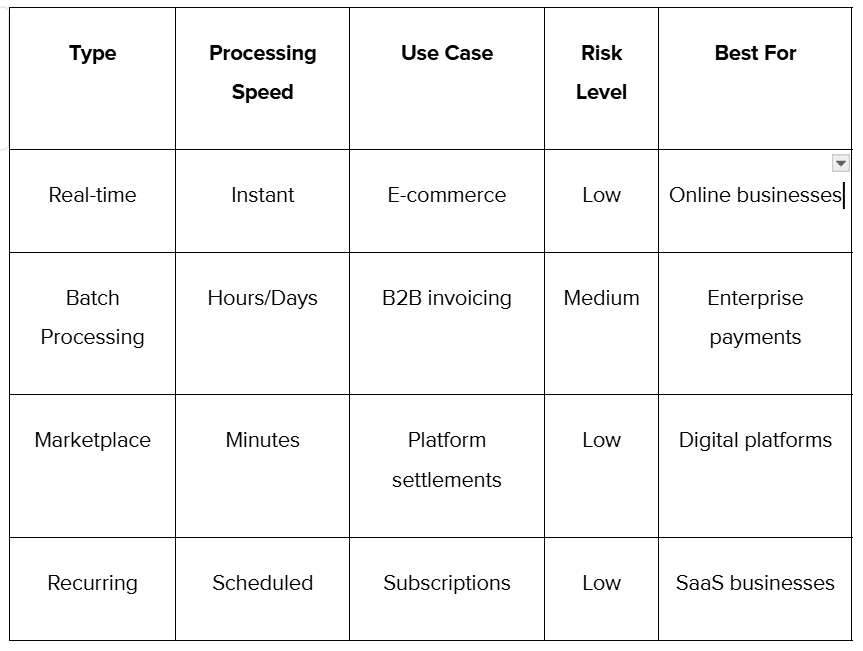

Different business scenarios require different approaches to global transaction processing. Here's how the main types compare across key factors:

Each type serves specific business needs and operational requirements. Let’s look at them in detail:

The real-time global transactions process immediately when customers make payments on your website or app. For instance, when someone buys a software product from an Indian company using a US credit card, the payment is authorized and settled within seconds across multiple banking systems.

Real-time transactions work best for e-commerce, digital services, and any business where immediate payment confirmation matters for customer experience.

The batch global transactions process multiple payments together at scheduled intervals, typically used for B2B invoicing or marketplace settlements. For example, a freelance platform might batch process all contractor payments at the end of each week.

Batch processing reduces transaction costs and works well when immediate settlement isn't critical for business operations.

These handle complex multi-party settlements where funds are split between multiple recipients. For instance, when someone books a hotel through your travel platform, the payment is split between your commission, the hotel payment, and applicable taxes across different areas.

These handle subscription payments, installments, or any scheduled international payment transfers. SaaS companies use these for monthly subscription billing across different countries and currencies.

Global transactions offer several advantages for businesses operating internationally. Some of the key benefits include:

Traditional international payment methods have several problems that global transaction systems address effectively.

To select the right platform for your international payment it’s essential to evaluate several key factors that impact both cost and operational efficiency. Some of those key factors include:

Handling global transactions shouldn't mean juggling multiple vendors, currencies, and compliance requirements. For growing businesses, the complexity of international payments can quickly become a bottleneck to expansion.

PayGlocal simplifies global transaction processing by providing a unified platform that handles everything from payment collection to compliance documentation. Whether you're a freelancer receiving payments from international clients or an enterprise managing complex multi-currency operations, the platform adapts to your specific needs.

Here's how PayGlocal addresses common global transaction challenges:

PayGlocal's global transaction infrastructure ensures high success rates while reducing the operational complexity typically associated with international payment processing. This lets you focus on growing your business instead of managing payment logistics.

Global transactions have become essential for any business operating across borders, providing the reliability and consistency needed for international commerce. For businesses ready to scale internationally, choosing the right global transaction platform can significantly impact both operational efficiency and customer experience.

The best solutions combine high success rates with simplified integration and automatic compliance handling. PayGlocal helps businesses collect payments from anywhere while settling locally with complete transparency and compliance.

Ready to simplify your international payment processing? Get started with PayGlocal today and experience the difference a purpose-built global payment platform can make for your business growth.

Whether you're a freelancer receiving payments from international clients or an enterprise managing complex multi-currency operations, knowing how global transactions work can significantly impact your business efficiency.

In this guide, we break down everything you need to know about global transactions, from basic concepts to choosing the right platform that can help you enhance your international payment processes.

Key Takeaways:

- Complete payment process: Global transactions ensure all parts of a cross-border payment either complete successfully or roll back entirely, maintaining data integrity.

- Multi-system coordination: These transactions span multiple resource managers and payment systems across different countries and currencies.

- Enhanced reliability: Proper global transaction management reduces payment failures and improves cash flow for international businesses.

- Seamless processing: PayGlocal offers global transaction processing with a high success rate across 180+ countries for reliable international payments.

What is a global transaction?

A global transaction is a distributed payment process that spans multiple systems, currencies, or geographic locations while ensuring all parts complete successfully as a single unit.

When you process an international payment, you're essentially coordinating between different banks, payment processors, and regulatory systems across borders.

For example, when an Indian software company receives payment from a US client, the transaction involves currency conversion, compliance checks, SWIFT messaging, and settlement across different banking systems.

The process starts when a customer initiates an international payment through your checkout system. Your payment system creates a unique Global Transaction Identifier (GTRID) and propagates this information to all participating systems, which include your payment gateway, acquiring bank, card networks, and the customer's issuing bank.

Here's how the coordination happens:

1.Transaction initiation: Your payment system receives the international payment request and validates basic information like currency, amount, and customer details.

2. Resource preparation: Each participating system (banks, payment processors, compliance systems) receives a preparation request and validates its ability to process its portion of the transaction.

3. Coordination phase: The transaction manager collects responses from all systems. If any system cannot complete its part, the entire transaction is marked for rollback.

4. Final commitment: When all systems confirm readiness, the transaction manager sends commit instructions, making all changes permanent across all participating systems.

5. Settlement and reconciliation: Funds move between accounts, compliance documents are generated automatically, and all systems update their records simultaneously.

What are the types of global transactions?

Different business scenarios require different approaches to global transaction processing. Here's how the main types compare across key factors:

Each type serves specific business needs and operational requirements. Let’s look at them in detail:

1. Real-time global transactions

The real-time global transactions process immediately when customers make payments on your website or app. For instance, when someone buys a software product from an Indian company using a US credit card, the payment is authorized and settled within seconds across multiple banking systems.

Real-time transactions work best for e-commerce, digital services, and any business where immediate payment confirmation matters for customer experience.

2. Batch global transactions

The batch global transactions process multiple payments together at scheduled intervals, typically used for B2B invoicing or marketplace settlements. For example, a freelance platform might batch process all contractor payments at the end of each week.

Batch processing reduces transaction costs and works well when immediate settlement isn't critical for business operations.

3. Marketplace global transactions

These handle complex multi-party settlements where funds are split between multiple recipients. For instance, when someone books a hotel through your travel platform, the payment is split between your commission, the hotel payment, and applicable taxes across different areas.

4. Recurring global transactions

These handle subscription payments, installments, or any scheduled international payment transfers. SaaS companies use these for monthly subscription billing across different countries and currencies.

What are the benefits of global transactions?

- Data consistency: All payment-related updates happen simultaneously across different systems, preventing discrepancies in your financial records or customer accounts.

- Reduced payment failures: The complete nature of global payment means partial payments can't occur, preventing scenarios where money gets stuck between systems during cross-border transfers.

- Automated compliance: Global transaction systems automatically generate required documentation like FIRC certificates, tax reports, and regulatory filings across different jurisdictions.

- Multi-currency efficiency: Handle payments in customers' local currencies while settling in your preferred currency, improving conversion rates and customer experience.

- Audit trail clarity: Complete transaction logs across all participating systems make financial audits and dispute resolution much simpler for international operations.

- Scalability across markets: Add new countries and payment methods without rebuilding your core transaction infrastructure.

Global transactions offer several advantages for businesses operating internationally. Some of the key benefits include:

What challenges do global transactions solve?

Traditional international payment methods have several problems that global transaction systems address effectively.

- Cross-border complexity: Managing payments across different banking systems, regulations, and currencies traditionally required multiple vendors and manual reconciliation. Global transaction platforms consolidate this complexity into single, coordinated operations.

- Payment failure risks: With traditional methods, payments could fail at various stages, like after debiting the customer but before crediting your account, creating reconciliation nightmares. Global transactions prevent partial payment scenarios entirely.

- Compliance burden: Different countries require different documentation and reporting. Global transaction systems automatically generate compliance documents like FIRC certificates, tax reports, and audit trails as part of the transaction process.

- Currency conversion inefficiencies: Traditional methods often involve multiple currency conversions with poor exchange rates. Modern global transaction systems optimize currency routing and provide transparent, competitive rates.

- Settlement delays: International payments traditionally took days or weeks to settle. Global transaction systems provide faster settlement with real-time status tracking throughout the process.

- Lack of visibility: Traditional international payments offered minimal tracking once initiated. Global transaction platforms provide end-to-end visibility with real-time status updates and detailed reporting.

How to choose the right global transaction solution?

To select the right platform for your international payment it’s essential to evaluate several key factors that impact both cost and operational efficiency. Some of those key factors include:

- Transaction volume assessment: Start by evaluating your monthly payment volume and geographic reach. High-volume businesses need platforms offering volume discounts and diverse payment methods across multiple markets.

- Integration requirements: Consider your technical capabilities and timeline. Some platforms require extensive development work, while others offer plug-and-play solutions that work with existing e-commerce platforms or accounting systems.

- Compliance capabilities: For Indian businesses, automatic FIRC generation, GST compliance, and export documentation can save significant time and reduce regulatory risks compared to manual processes.

- Currency and settlement options: Look for platforms that let you collect payments in customers' local currencies while settling in INR, USD, or other preferred currencies with competitive exchange rates.

- Success rate metrics: Payment failures directly impact revenue, so choose platforms with proven track records of high authorization rates across different markets and payment methods.

- Total cost analysis: Review all costs, including setup fees, transaction charges, currency conversion costs, and hidden fees that might impact your margins as you scale internationally.

Manage all of your international payments in one platform

Handling global transactions shouldn't mean juggling multiple vendors, currencies, and compliance requirements. For growing businesses, the complexity of international payments can quickly become a bottleneck to expansion.

PayGlocal simplifies global transaction processing by providing a unified platform that handles everything from payment collection to compliance documentation. Whether you're a freelancer receiving payments from international clients or an enterprise managing complex multi-currency operations, the platform adapts to your specific needs.

Here's how PayGlocal addresses common global transaction challenges:

- Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries while settling in your preferred currency with transparent, competitive rates.

- Global payment methods: Offer 40+ global payment methods, including cards, digital wallets, and local banking options that customers trust in their regions.

- Instant compliance: Automatic FIRC generation and compliance documentation reduce manual paperwork and regulatory risks for export businesses.

- One platform management: Handle all your international payments, tracking, and settlements from a single dashboard instead of managing multiple vendor relationships.

- Dynamic checkout: Provide localized payment experiences that increase conversion rates by showing familiar payment options and currencies to each customer.

PayGlocal's global transaction infrastructure ensures high success rates while reducing the operational complexity typically associated with international payment processing. This lets you focus on growing your business instead of managing payment logistics.

Final thoughts

Global transactions have become essential for any business operating across borders, providing the reliability and consistency needed for international commerce. For businesses ready to scale internationally, choosing the right global transaction platform can significantly impact both operational efficiency and customer experience.

The best solutions combine high success rates with simplified integration and automatic compliance handling. PayGlocal helps businesses collect payments from anywhere while settling locally with complete transparency and compliance.

Ready to simplify your international payment processing? Get started with PayGlocal today and experience the difference a purpose-built global payment platform can make for your business growth.