With 2.5 billion bank accounts, digital payments have been rapidly growing in India in recent years. In fact, according to the latest data, more than 18,000 crore digital transactions took place in the year 2024-25.

But to ensure smooth transactions, it becomes essential to ensure all your account details are set up correctly. This is especially worth considering when you’re transferring your bank account to a new branch, as it may affect your IFSC code.

In this guide, we break down exactly when IFSC codes change, what steps you need to take, and how to keep your payments flowing smoothly during the change. Let’s get into it.

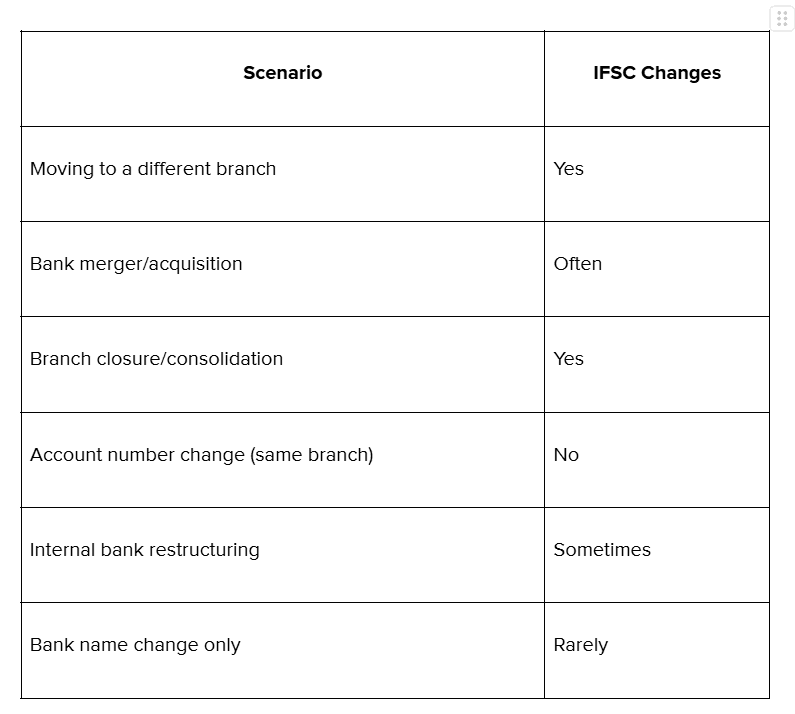

Branch-specific changes: IFSC codes change when you move to a different branch, even if your account number stays the same.

Bank mergers trigger updates: Major restructuring, mergers, or acquisitions often result in new IFSC codes for affected branches.

Account number changes don't affect IFSC: Changing your account number within the same branch keeps your IFSC code unchanged.

Update requirements: You'll need to notify employers, clients, and payment platforms about your new IFSC to avoid transaction failures.

Global payment solution: PayGlocal offers multi-currency accounts that simplify international payment collection without traditional payment complexities.

An IFSC (Indian Financial System Code) is an 11-character alphanumeric identifier that precisely identifies the bank branch to which your money should be sent. The first four characters identify the bank, the fifth is always zero, and the last six digits specify the specific branch location.

For example, in the code HDFC0001234, "HDFC" represents HDFC Bank, "0" is the standard separator, and "001234" identifies the particular branch.

This system ensures that when someone sends you money through NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), or IMPS (Immediate Payment Service), it reaches the correct destination without confusion.

The IFSC code acts like a postal address for your bank account. Just as mail needs the right address to reach you, electronic payments need the correct IFSC to land in your account. When this code changes unexpectedly, payments can fail, bounce back to the sender, or get delayed while banks sort out routing issues.

Your IFSC code changes in specific situations, and knowing these scenarios helps you prepare accordingly.

Let’s take a detailed look at each scenario when IFSC code changes:

Branch transfers: Moving to a different branch is the most common trigger for IFSC changes. Even if you keep the same account number, transferring from one branch to another typically means getting a new IFSC code. For instance, if you relocate and transfer your account to a new city, you'll receive the IFSC code specific to your new branch location.

Bank mergers and acquisitions: These often result in widespread IFSC updates. When banks undergo structural changes, consolidate operations, or rebrand their services, they may issue new IFSC codes to align with their updated systems.

Branch closures or consolidations: These force IFSC changes when your original branch ceases independent operations. If your branch merges with a nearby location or closes permanently, you'll be assigned to a new branch with its corresponding IFSC code.

Internal restructuring: This can also trigger changes, though it's less common. Banks sometimes reorganize their branch networks, update routing systems, or implement new technology platforms that require fresh IFSC assignments.

Banks don't share IFSC changes suddenly. When changes are coming, you'll typically receive advance notification through SMS, email, or physical mail. There’s usually a notice period of a few days, giving you enough time to update your details across all platforms.

IFSC code changing period: During this timeframe, many banks maintain backward compatibility. Your old IFSC code may continue working for several weeks or months while the bank's systems internally route payments to your new branch. This grace period prevents immediate payment failures and gives you breathing room to make necessary updates.

Payment routing adjustments: These happen behind the scenes. Banks often configure their systems to automatically redirect transactions from old IFSC codes to new ones during transition periods. However, this isn't guaranteed indefinitely, and relying on it long-term is risky.

Documentation updates: These become your responsibility. You'll receive new cheque books, passbooks, and account statements reflecting your updated IFSC code. Your existing cheques with the old IFSC may still work temporarily, but you should switch to new ones as soon as possible.

System validations: These may flag your old IFSC as inactive or invalid once the transition period ends. Payment platforms, employer payroll systems, and client payment portals might reject transactions attempted with outdated codes.

The moment you confirm your IFSC change, start updating your details systematically to prevent payment disruptions.

Employer notification: Contact your HR or payroll team immediately with your new IFSC code, account number, and banking details. Most companies need 1-2 pay cycles to implement changes, so early notification prevents salary delays.

Client payment updates: Send professional notifications to everyone who pays you regularly. Include your complete new banking details and specify when the changes take effect. This maintains trust and prevents payment failure conversations.

Platform modifications: Update recurring payment setups across all platforms where you receive money. This includes freelance platforms, e-commerce marketplaces, and subscription-based income sources. Each platform has different update procedures, so allow extra time.

Government department notifications: Inform relevant departments if you receive official payments, refunds, or subsidies. Tax refunds, GST refunds, and other government payments can get delayed if your banking details are outdated.

Investment platform updates: Modify details where you have SIPs (Systematic Investment Plans), mutual fund redemptions, or dividend credits. Brokerages and AMCs (Asset Management Companies) need current banking details to process financial transactions smoothly.

International client communication: Notify overseas clients about banking changes if you receive foreign payments. For exporters and service exporters, accurate banking details are crucial for FIRC compliance and foreign exchange documentation.

Using an incorrect IFSC code doesn't necessarily mean your money disappears into the banking void, but it does create complications you'd rather avoid.

Transaction rejections: These are the most common outcome when banks detect invalid or mismatched IFSC codes. The payment system flags the inconsistency and refuses to process the transaction, usually returning the money to the sender within 1-2 business days.

Delayed processing: This occurs when banks attempt to verify and correct minor IFSC discrepancies. This manual intervention can add 2-3 days to normal transaction times, causing frustration for both sender and receiver.

Same-bank flexibility: This sometimes works in your favor. If the wrong IFSC belongs to the same bank as your account, some internal systems can still route the payment successfully using your account number. However, this varies by bank and shouldn't be relied upon.

Failed international transfers: These are particularly problematic since reversing international payments takes longer and may incur additional fees. Foreign banks have less tolerance for incorrect Indian banking details.

Managing IFSC changes becomes particularly complex when you're dealing with international clients, multiple currencies, and compliance requirements.

For businesses focused on global payment collection, PayGlocal offers specialized global payment solutions. Instead of handling traditional payment complications, you get well-organized international payment capabilities designed for modern global commerce.

Here's how PayGlocal can help you:

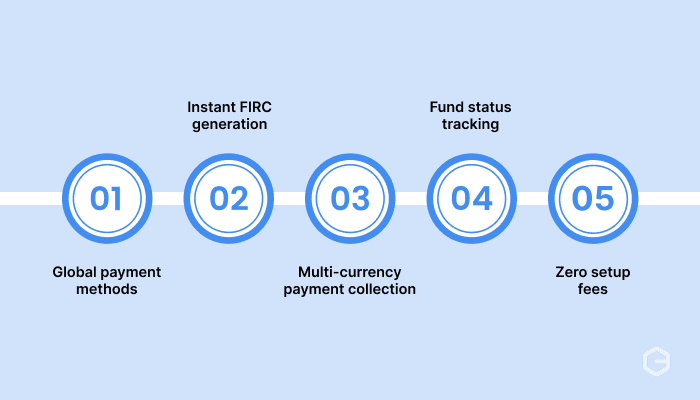

Global payment methods: Accept payments through 40+ international payment options including cards, wallets, and local banking systems from different countries.

Instant FIRC generation: Receive compliance documentation automatically upon settlement, with no manual paperwork or delays caused by banking detail mismatches.

Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries through a single platform, reducing the need to manage multiple Indian bank account details.

Fund status tracking: Monitor payment status in real-time with notifications at every step, removing uncertainty about transaction success or failure.

Zero setup fees: Start collecting international payments immediately without upfront costs or the need to coordinate updates across multiple banks.

Whether you're a freelancer receiving project payments from global clients or an exporter managing multiple international transactions, PayGlocal's infrastructure adapts to your business growth without forcing you to manage banking technicalities.

IFSC codes do change when you transfer your account to a different branch, and being prepared for this change prevents payment disruptions and compliance complications.

It’s essential to act quickly once you receive notification, updating all relevant parties systematically, and maintaining clear communication with everyone who sends you payments.

While traditional banking systems require careful management of these technical details, modern payment solutions like PayGlocal offer an effective payment solution that simplifies international transactions entirely.

Take control of your payment workflows. Whether you're managing a simple payment transfer or scaling international payment processes, the right payment partner makes all the difference. Get started with PayGlocal today.

But to ensure smooth transactions, it becomes essential to ensure all your account details are set up correctly. This is especially worth considering when you’re transferring your bank account to a new branch, as it may affect your IFSC code.

In this guide, we break down exactly when IFSC codes change, what steps you need to take, and how to keep your payments flowing smoothly during the change. Let’s get into it.

Key Takeaways:

Branch-specific changes: IFSC codes change when you move to a different branch, even if your account number stays the same.

Bank mergers trigger updates: Major restructuring, mergers, or acquisitions often result in new IFSC codes for affected branches.

Account number changes don't affect IFSC: Changing your account number within the same branch keeps your IFSC code unchanged.

Update requirements: You'll need to notify employers, clients, and payment platforms about your new IFSC to avoid transaction failures.

Global payment solution: PayGlocal offers multi-currency accounts that simplify international payment collection without traditional payment complexities.

What is an IFSC code and why does it matter?

An IFSC (Indian Financial System Code) is an 11-character alphanumeric identifier that precisely identifies the bank branch to which your money should be sent. The first four characters identify the bank, the fifth is always zero, and the last six digits specify the specific branch location.

For example, in the code HDFC0001234, "HDFC" represents HDFC Bank, "0" is the standard separator, and "001234" identifies the particular branch.

This system ensures that when someone sends you money through NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), or IMPS (Immediate Payment Service), it reaches the correct destination without confusion.

The IFSC code acts like a postal address for your bank account. Just as mail needs the right address to reach you, electronic payments need the correct IFSC to land in your account. When this code changes unexpectedly, payments can fail, bounce back to the sender, or get delayed while banks sort out routing issues.

When does your IFSC code change after an account transfer?

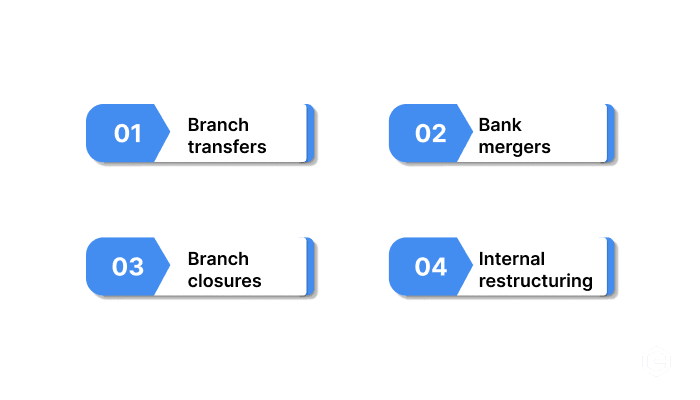

Your IFSC code changes in specific situations, and knowing these scenarios helps you prepare accordingly.

Let’s take a detailed look at each scenario when IFSC code changes:

Branch transfers: Moving to a different branch is the most common trigger for IFSC changes. Even if you keep the same account number, transferring from one branch to another typically means getting a new IFSC code. For instance, if you relocate and transfer your account to a new city, you'll receive the IFSC code specific to your new branch location.

Bank mergers and acquisitions: These often result in widespread IFSC updates. When banks undergo structural changes, consolidate operations, or rebrand their services, they may issue new IFSC codes to align with their updated systems.

Branch closures or consolidations: These force IFSC changes when your original branch ceases independent operations. If your branch merges with a nearby location or closes permanently, you'll be assigned to a new branch with its corresponding IFSC code.

Internal restructuring: This can also trigger changes, though it's less common. Banks sometimes reorganize their branch networks, update routing systems, or implement new technology platforms that require fresh IFSC assignments.

What happens when your IFSC code changes?

Banks don't share IFSC changes suddenly. When changes are coming, you'll typically receive advance notification through SMS, email, or physical mail. There’s usually a notice period of a few days, giving you enough time to update your details across all platforms.

IFSC code changing period: During this timeframe, many banks maintain backward compatibility. Your old IFSC code may continue working for several weeks or months while the bank's systems internally route payments to your new branch. This grace period prevents immediate payment failures and gives you breathing room to make necessary updates.

Payment routing adjustments: These happen behind the scenes. Banks often configure their systems to automatically redirect transactions from old IFSC codes to new ones during transition periods. However, this isn't guaranteed indefinitely, and relying on it long-term is risky.

Documentation updates: These become your responsibility. You'll receive new cheque books, passbooks, and account statements reflecting your updated IFSC code. Your existing cheques with the old IFSC may still work temporarily, but you should switch to new ones as soon as possible.

System validations: These may flag your old IFSC as inactive or invalid once the transition period ends. Payment platforms, employer payroll systems, and client payment portals might reject transactions attempted with outdated codes.

How to update your IFSC code after account transfer?

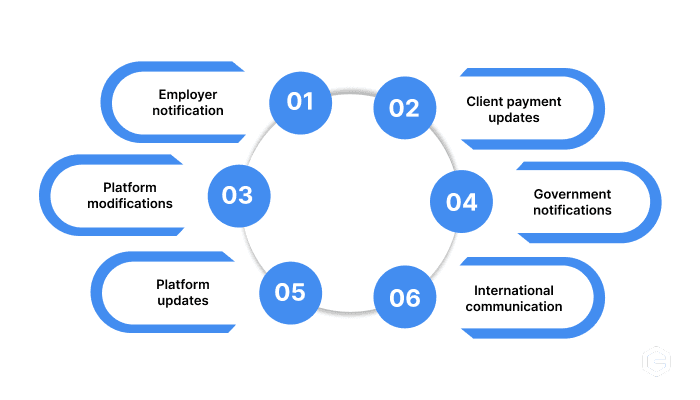

The moment you confirm your IFSC change, start updating your details systematically to prevent payment disruptions.

Employer notification: Contact your HR or payroll team immediately with your new IFSC code, account number, and banking details. Most companies need 1-2 pay cycles to implement changes, so early notification prevents salary delays.

Client payment updates: Send professional notifications to everyone who pays you regularly. Include your complete new banking details and specify when the changes take effect. This maintains trust and prevents payment failure conversations.

Platform modifications: Update recurring payment setups across all platforms where you receive money. This includes freelance platforms, e-commerce marketplaces, and subscription-based income sources. Each platform has different update procedures, so allow extra time.

Government department notifications: Inform relevant departments if you receive official payments, refunds, or subsidies. Tax refunds, GST refunds, and other government payments can get delayed if your banking details are outdated.

Investment platform updates: Modify details where you have SIPs (Systematic Investment Plans), mutual fund redemptions, or dividend credits. Brokerages and AMCs (Asset Management Companies) need current banking details to process financial transactions smoothly.

International client communication: Notify overseas clients about banking changes if you receive foreign payments. For exporters and service exporters, accurate banking details are crucial for FIRC compliance and foreign exchange documentation.

What happens if you use the wrong IFSC code?

Using an incorrect IFSC code doesn't necessarily mean your money disappears into the banking void, but it does create complications you'd rather avoid.

Transaction rejections: These are the most common outcome when banks detect invalid or mismatched IFSC codes. The payment system flags the inconsistency and refuses to process the transaction, usually returning the money to the sender within 1-2 business days.

Delayed processing: This occurs when banks attempt to verify and correct minor IFSC discrepancies. This manual intervention can add 2-3 days to normal transaction times, causing frustration for both sender and receiver.

Same-bank flexibility: This sometimes works in your favor. If the wrong IFSC belongs to the same bank as your account, some internal systems can still route the payment successfully using your account number. However, this varies by bank and shouldn't be relied upon.

Failed international transfers: These are particularly problematic since reversing international payments takes longer and may incur additional fees. Foreign banks have less tolerance for incorrect Indian banking details.

Get paid globally and grow your business with PayGlocal

Managing IFSC changes becomes particularly complex when you're dealing with international clients, multiple currencies, and compliance requirements.

For businesses focused on global payment collection, PayGlocal offers specialized global payment solutions. Instead of handling traditional payment complications, you get well-organized international payment capabilities designed for modern global commerce.

Here's how PayGlocal can help you:

Global payment methods: Accept payments through 40+ international payment options including cards, wallets, and local banking systems from different countries.

Instant FIRC generation: Receive compliance documentation automatically upon settlement, with no manual paperwork or delays caused by banking detail mismatches.

Multi-currency payment collection: Accept payments in 33+ currencies from 180+ countries through a single platform, reducing the need to manage multiple Indian bank account details.

Fund status tracking: Monitor payment status in real-time with notifications at every step, removing uncertainty about transaction success or failure.

Zero setup fees: Start collecting international payments immediately without upfront costs or the need to coordinate updates across multiple banks.

Whether you're a freelancer receiving project payments from global clients or an exporter managing multiple international transactions, PayGlocal's infrastructure adapts to your business growth without forcing you to manage banking technicalities.

Final thoughts

IFSC codes do change when you transfer your account to a different branch, and being prepared for this change prevents payment disruptions and compliance complications.

It’s essential to act quickly once you receive notification, updating all relevant parties systematically, and maintaining clear communication with everyone who sends you payments.

While traditional banking systems require careful management of these technical details, modern payment solutions like PayGlocal offer an effective payment solution that simplifies international transactions entirely.

Take control of your payment workflows. Whether you're managing a simple payment transfer or scaling international payment processes, the right payment partner makes all the difference. Get started with PayGlocal today.