Your global business growth depends on getting paid efficiently by international customers. Research shows the worldwide cross-border payments industry will grow from $206.5 billion in 2024 to $414.6 billion by 2034, proving how rapidly global transactions are expanding.

Whether you're a freelancer collecting payments from overseas clients or an exporter expanding into new markets, your payment system directly affects your cash flow and growth potential. High fees, slow settlements, and failed transfers don’t need to be part of global business.

This guide breaks down how international business payments work, the types of global payment methods available, and how to choose the best option for your business.

International business payments are fund transfers across borders for business-related transactions. These payments help businesses collect money from global customers, pay overseas suppliers, and receive earnings from international platforms.

Cross-border payments work differently from domestic transfers. Local payments move money within one country using familiar banks and regulations. Whereas, international payments cross multiple banking systems and follow different country rules. Currency conversion happens during the process, which adds costs and processing time.

Domestic payments typically settle within hours using local banking networks. International transfers take longer because money moves through correspondent banks in different countries. Each bank verifies the transaction and applies local compliance checks.

Here's how the international payment process typically works:

Businesses across various sectors rely on international payments for different purposes:

* Travel and hospitality platforms: Handle bookings and cancellations across different currencies, process insurance claims, and manage complex multi-party payment flows.

International business payments use different payment instruments depending on the transaction size, the relationship between parties, and security requirements.

Each payment type offers specific advantages for different business situations.

Wire transfers move money directly between banks using the SWIFT network. For example, a pharmaceutical exporter in India receives wire transfers from distributors in Europe for bulk medicine orders. Similarly, software companies use wire transfers for large project payments from enterprise clients.

These transfers provide high security and work for any amount. Banks generate detailed transaction records that help with accounting and compliance. SWIFT charges can be significant but predictable for budgeting purposes.

International checks work like domestic checks but require currency conversion and international clearing. For example, a freelance consultant might receive an international check from a small business client who prefers traditional payment methods.

Banks generally take 2-4 weeks to clear international checks due to verification processes. This method works better for established business relationships where payment timing isn't urgent.

Forex transfers focus specifically on currency conversion efficiency. For instance, an import business uses forex transfers to pay suppliers in another country, converting INR to USD at competitive rates.

Specialized forex providers often offer better exchange rates than traditional banks. These transfers work well for regular international transactions where currency rates significantly impact costs.

Tired of losing money on poor exchange rates? PayGlocal offers competitive FX rates with transparent pricing. Get started with zero setup fees.

Letters of credit provide payment guarantees for trade transactions. For example, a machinery exporter uses letters of credit when shipping equipment to new international buyers. This arrangement ensures the buyer's bank guarantees payment once shipping documents prove delivery.

This instrument reduces risk for both exporters and importers. Trade finance banks handle the documentation and verification process, making it suitable for high-value transactions with unknown partners.

Documentary collections require buyers to pay or accept payment terms before receiving shipping documents. For example, an agricultural exporter uses documentary collections when selling rice to overseas distributors.

Banks handle document exchange but don't guarantee payment like letters of credit. This option costs less than letters of credit while providing some security through document control.

Modern EFT systems allow faster international transfers through digital networks. For instance, a SaaS company receives EFT payments from global customers through automated subscription billing.

EFT transfers typically process faster than traditional wire transfers and offer better tracking. International money transfer options continue expanding with new EFT technologies.

Struggling with slow payment processing and poor tracking? PayGlocal provides real-time payment tracking and faster settlements. Get started today.

Different platforms and systems process international payments with varying costs, speeds, and features.

Here’s how the top methods of international business payments compare:

Choosing the right method depends on your business size, transaction volume, and customer preferences.

Banks use the SWIFT network to process wire transfers and other international transactions. They offer maximum security and work with any transaction amount. However, banks charge high fees and take 3-5 business days for processing.

Banks provide detailed transaction records and handle complex compliance requirements. SWIFT charges include both fixed fees and percentage-based costs that can add up quickly.

Best for: Large B2B transactions, established businesses with high-value transfers, and companies that prioritize security over speed.

Online platforms offer user-friendly interfaces and quick setup processes. PayPal works well for freelancers receiving payments from freelance platforms like Upwork. Wise provides competitive exchange rates for regular international transfers.

These platforms charge percentage-based fees (typically 3-5%) and may have limited customer support for business accounts. Currency conversion often includes hidden markups.

Best for: Freelancers, small businesses, and companies with occasional international transactions under $10,000.

Payment gateways specialize in processing card transactions and online payments. They offer developer-friendly APIs and handle multiple payment methods. However, many gateways don't provide proper FIRA documentation for Indian businesses.

Choosing the right payment gateway requires evaluating compliance features, approval rates, and customer support quality.

Best for: E-commerce stores, SaaS companies, and businesses that primarily collect card payments from global customers.

Virtual accounts provide local bank details in major currencies like USD, GBP, and EUR. Customers can pay using familiar local banking methods, which improves approval rates and reduces transaction costs.

Modern fintech solutions offer better exchange rates, automatic compliance documentation, and real-time tracking. Multi-currency accounts simplify international payment collection for growing businesses.

Best for: SMBs, exporters, and businesses that want cost-effective solutions with automated compliance and a better customer experience.

Start by analyzing who's paying you and from where. B2B clients might prefer bank transfers, while consumers favor cards and digital wallets. Geographic location affects payment preferences significantly.

Here are some of the top factors to consider while choosing the right method for international business payments:

Traditional payment solutions create unnecessary friction and costs for growing businesses. You shouldn't have to choose between speed, cost, and compliance when collecting international payments.

PayGlocal handles these challenges by providing a complete international payment solution designed specifically for Indian businesses. Here's how we make global payments work for you:

Whether you're billing clients across continents or scaling your export business, PayGlocal helps you get paid faster without the friction.

International business payments don't have to be complex or costly. With the right solution, you can expand globally without worrying about failed transactions, hidden fees, or compliance delays.

Whether you're a solopreneur working with global clients or a scaling business entering new markets, your payments should move as fast as your ambitions. The key is choosing a payment partner that supports your specific needs and growth goals.

Make your global collections smarter with PayGlocal. Ready to scale globally? Get started now.

Whether you're a freelancer collecting payments from overseas clients or an exporter expanding into new markets, your payment system directly affects your cash flow and growth potential. High fees, slow settlements, and failed transfers don’t need to be part of global business.

This guide breaks down how international business payments work, the types of global payment methods available, and how to choose the best option for your business.

Key Takeaways

- Payment fundamentals: International business payments are cross-border fund transfers that require different methods, costs, and compliance steps compared to domestic payments.

- Available methods: SWIFT transfers, online platforms, payment gateways, and virtual accounts each differ in cost, speed, and convenience.

- Smart solutions: Modern fintech platforms and virtual accounts offer lower fees and faster processing than traditional banks.

- PayGlocal advantage: PayGlocal provides comprehensive international payment solutions with zero setup costs, automatic compliance, and real-time tracking for Indian businesses.

- What Are International Business Payments?

International business payments are fund transfers across borders for business-related transactions. These payments help businesses collect money from global customers, pay overseas suppliers, and receive earnings from international platforms.

Cross-border payments work differently from domestic transfers. Local payments move money within one country using familiar banks and regulations. Whereas, international payments cross multiple banking systems and follow different country rules. Currency conversion happens during the process, which adds costs and processing time.

Domestic payments typically settle within hours using local banking networks. International transfers take longer because money moves through correspondent banks in different countries. Each bank verifies the transaction and applies local compliance checks.

How Do International Payments Work?

Here's how the international payment process typically works:

- Payment initiation: The sender (customer or business) provides payment details, including recipient information, amount, currency, and purpose code to their bank or payment platform.

- Compliance verification: Banks verify the sender's identity, check sanctions lists, and ensure the transaction meets anti-money laundering rules in both countries.

- Currency conversion: When currencies differ, the sending bank or payment processor converts money at current exchange rates, often adding markup fees.

- Correspondent banking: Money moves through correspondent banks that connect the sender's country and the recipient's country, with each bank charging processing fees.

- Regulatory clearance: Both sending and receiving countries apply their compliance rules, which may include export documentation strategy requirements and FIRA documentation.

- Final settlement: The recipient's bank receives the funds and credits the account, then provides transaction confirmation and necessary compliance documentation.

Common Uses for International Business Payments

Businesses across various sectors rely on international payments for different purposes:

- Freelancers & service providers: Collect payments from global clients, receive platform payouts from freelance marketplaces, and handle project-based billing across multiple currencies.

- Export businesses: Receive payments from overseas buyers for goods and services, manage supplier payments for raw materials, and handle goods exporter documentation requirements.

- E-commerce companies: Process customer payments from multiple countries, handle refunds and disputes, and manage marketplace settlements for platforms like Amazon Global.

- SaaS and technology companies: Collect subscription payments from global users, process one-time purchases, and manage recurring payment cycles for different market segments.

* Travel and hospitality platforms: Handle bookings and cancellations across different currencies, process insurance claims, and manage complex multi-party payment flows.

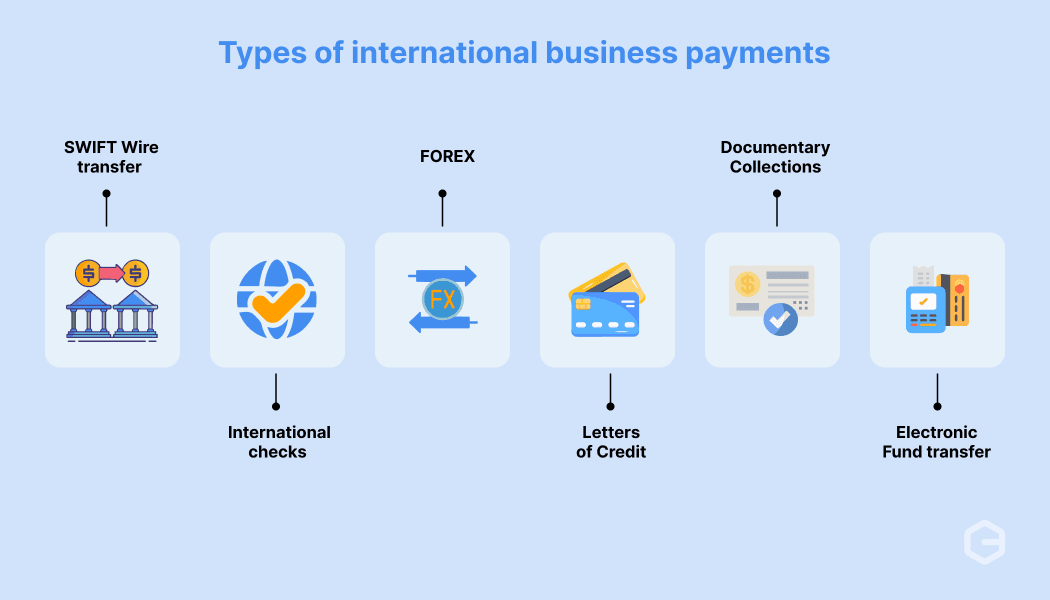

Types of International Business Payments

International business payments use different payment instruments depending on the transaction size, the relationship between parties, and security requirements.

Each payment type offers specific advantages for different business situations.

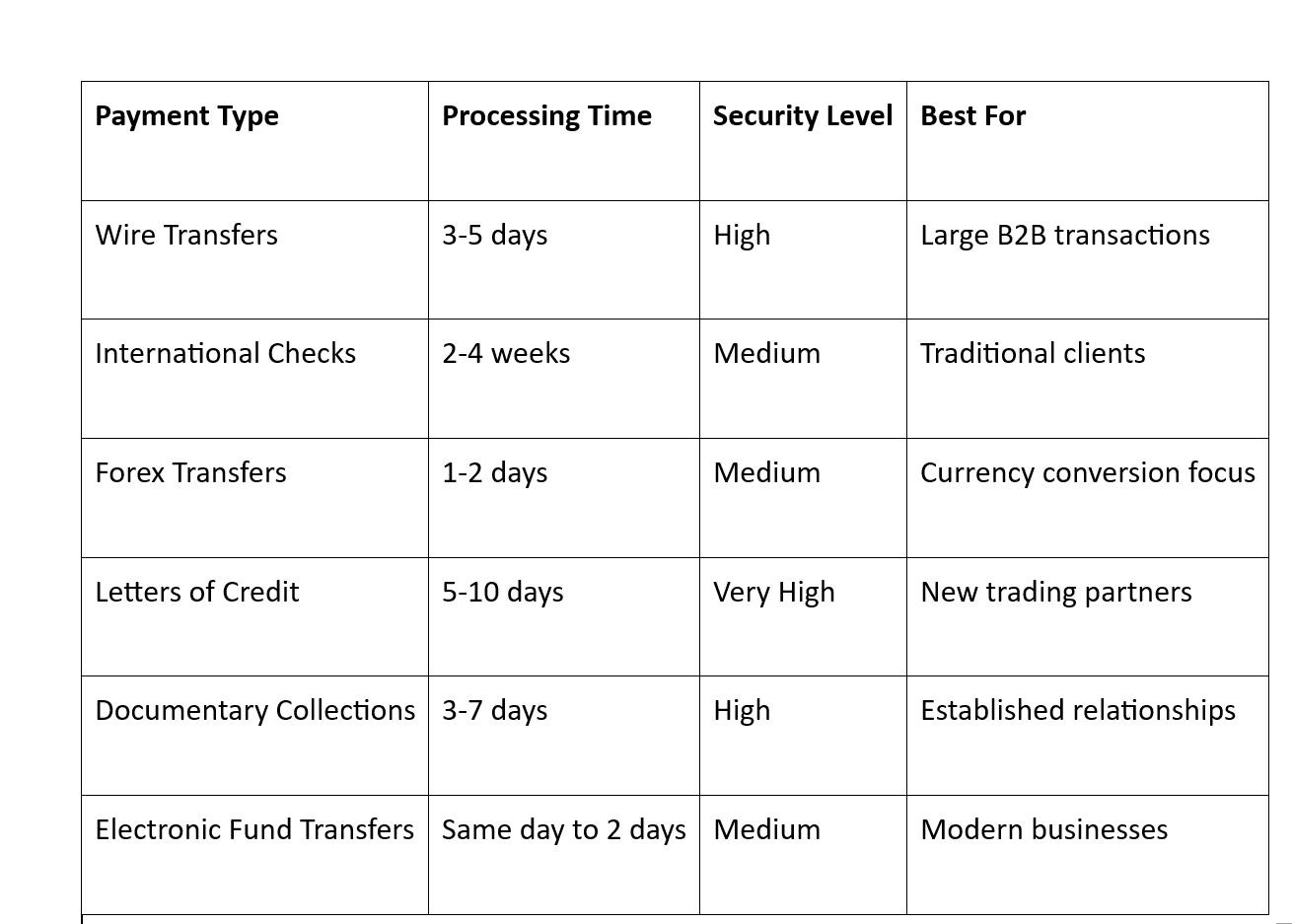

1. Wire Transfers (SWIFT)

Wire transfers move money directly between banks using the SWIFT network. For example, a pharmaceutical exporter in India receives wire transfers from distributors in Europe for bulk medicine orders. Similarly, software companies use wire transfers for large project payments from enterprise clients.

These transfers provide high security and work for any amount. Banks generate detailed transaction records that help with accounting and compliance. SWIFT charges can be significant but predictable for budgeting purposes.

2. International Checks

International checks work like domestic checks but require currency conversion and international clearing. For example, a freelance consultant might receive an international check from a small business client who prefers traditional payment methods.

Banks generally take 2-4 weeks to clear international checks due to verification processes. This method works better for established business relationships where payment timing isn't urgent.

3. Foreign Exchange (Forex) Transfers

Forex transfers focus specifically on currency conversion efficiency. For instance, an import business uses forex transfers to pay suppliers in another country, converting INR to USD at competitive rates.

Specialized forex providers often offer better exchange rates than traditional banks. These transfers work well for regular international transactions where currency rates significantly impact costs.

Tired of losing money on poor exchange rates? PayGlocal offers competitive FX rates with transparent pricing. Get started with zero setup fees.

4. Letters of Credit

Letters of credit provide payment guarantees for trade transactions. For example, a machinery exporter uses letters of credit when shipping equipment to new international buyers. This arrangement ensures the buyer's bank guarantees payment once shipping documents prove delivery.

This instrument reduces risk for both exporters and importers. Trade finance banks handle the documentation and verification process, making it suitable for high-value transactions with unknown partners.

5. Documentary Collections

Documentary collections require buyers to pay or accept payment terms before receiving shipping documents. For example, an agricultural exporter uses documentary collections when selling rice to overseas distributors.

Banks handle document exchange but don't guarantee payment like letters of credit. This option costs less than letters of credit while providing some security through document control.

6. Electronic Fund Transfers (EFT)

Modern EFT systems allow faster international transfers through digital networks. For instance, a SaaS company receives EFT payments from global customers through automated subscription billing.

EFT transfers typically process faster than traditional wire transfers and offer better tracking. International money transfer options continue expanding with new EFT technologies.

Struggling with slow payment processing and poor tracking? PayGlocal provides real-time payment tracking and faster settlements. Get started today.

Payment methods and systems for international business

Different platforms and systems process international payments with varying costs, speeds, and features.

Here’s how the top methods of international business payments compare:

Choosing the right method depends on your business size, transaction volume, and customer preferences.

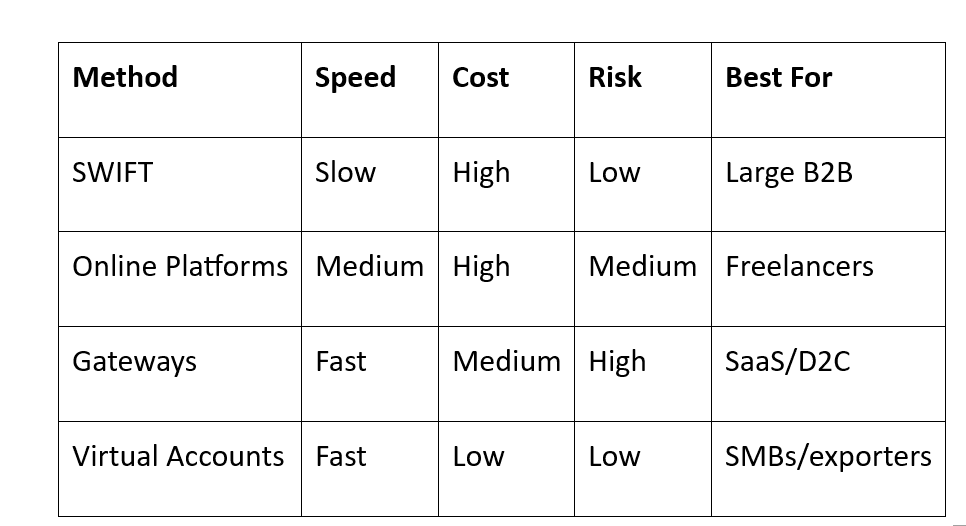

1. Traditional Banks (SWIFT Network)

Banks use the SWIFT network to process wire transfers and other international transactions. They offer maximum security and work with any transaction amount. However, banks charge high fees and take 3-5 business days for processing.

Banks provide detailed transaction records and handle complex compliance requirements. SWIFT charges include both fixed fees and percentage-based costs that can add up quickly.

Best for: Large B2B transactions, established businesses with high-value transfers, and companies that prioritize security over speed.

2. Online Payment Platforms (PayPal, Wise)

Online platforms offer user-friendly interfaces and quick setup processes. PayPal works well for freelancers receiving payments from freelance platforms like Upwork. Wise provides competitive exchange rates for regular international transfers.

These platforms charge percentage-based fees (typically 3-5%) and may have limited customer support for business accounts. Currency conversion often includes hidden markups.

Best for: Freelancers, small businesses, and companies with occasional international transactions under $10,000.

3. Payment Gateways (Stripe, Razorpay)

Payment gateways specialize in processing card transactions and online payments. They offer developer-friendly APIs and handle multiple payment methods. However, many gateways don't provide proper FIRA documentation for Indian businesses.

Choosing the right payment gateway requires evaluating compliance features, approval rates, and customer support quality.

Best for: E-commerce stores, SaaS companies, and businesses that primarily collect card payments from global customers.

4. Virtual Accounts & Fintech Solutions

Virtual accounts provide local bank details in major currencies like USD, GBP, and EUR. Customers can pay using familiar local banking methods, which improves approval rates and reduces transaction costs.

Modern fintech solutions offer better exchange rates, automatic compliance documentation, and real-time tracking. Multi-currency accounts simplify international payment collection for growing businesses.

Best for: SMBs, exporters, and businesses that want cost-effective solutions with automated compliance and a better customer experience.

How to choose the right payment method for your business?

Start by analyzing who's paying you and from where. B2B clients might prefer bank transfers, while consumers favor cards and digital wallets. Geographic location affects payment preferences significantly.

Here are some of the top factors to consider while choosing the right method for international business payments:

- Transaction volume and frequency: High-volume businesses benefit more from lower percentage fees, even with setup costs. Occasional transactions might work better with simple, fee-per-transaction models.

- Customer experience requirements: Consumers typically prefer local currency pricing when making purchase decisions, making payment localization important for international business.

- Compliance and documentation needs: Proper export documentation strategy becomes crucial for businesses handling significant international volumes.

- Settlement preferences: Some businesses need instant access to funds, while others can wait for better exchange rates.

Increase your global reach with a faster payment solution

Traditional payment solutions create unnecessary friction and costs for growing businesses. You shouldn't have to choose between speed, cost, and compliance when collecting international payments.

PayGlocal handles these challenges by providing a complete international payment solution designed specifically for Indian businesses. Here's how we make global payments work for you:

- Multi-currency collection: Accept payments in 33+ currencies, including USD, GBP, EUR, and CAD, with multi-currency accounts that improve approval rates and customer experience.

- Zero setup costs: No fixed fees, platform charges, or documentation costs; you only pay when you successfully collect payments from customers.

- Automatic compliance: Receive FIRC documentation instantly upon settlement, removing manual paperwork and ensuring proper regulatory compliance.

- High success rates: Dynamic checkout technology and intelligent routing maximize approval rates for international card transactions.

- Multiple payment methods: Support cards, bank transfers, alternate payment methods, payment links, and recurring payments from one integrated platform.

Whether you're billing clients across continents or scaling your export business, PayGlocal helps you get paid faster without the friction.

Final Thoughts

International business payments don't have to be complex or costly. With the right solution, you can expand globally without worrying about failed transactions, hidden fees, or compliance delays.

Whether you're a solopreneur working with global clients or a scaling business entering new markets, your payments should move as fast as your ambitions. The key is choosing a payment partner that supports your specific needs and growth goals.

Make your global collections smarter with PayGlocal. Ready to scale globally? Get started now.