Your invoice said $3,000. Your client paid $3,000. You received the INR equivalent of $2,910. The missing $90 went to a conversion markup fee you didn't know about.

This is a common problem for many businesses in India. As the total Indian exports reached $825.3 billion in FY25, more companies are now sending invoices to clients across the world. Getting your invoice and payment process right is the only way to make sure you get paid on time and keep all of your profit.

This guide covers everything from what your international invoice should include to which collection method works best for your business.

International invoice payment: It's the process of collecting or sending payment for an invoice when the buyer and seller are in two countries, often involving currency conversion.

An international invoice payment is a payment made against an invoice when the buyer and seller are in two countries. It typically involves currency conversion, cross-border banking channels, and additional documentation compared to a domestic payment.

For example, a software company in India sends a $5,000 invoice to a client in New York. The client pays using a wire transfer or card payment. The payment travels through one or more banking networks, gets converted from USD to INR, and lands in the company's Indian bank account. The company receives the amount minus any fees and conversion charges.

A delayed payment doesn't just affect your bank balance. It affects your ability to pay suppliers, manage payroll, and plan for growth. When you sell internationally, delays and unexpected costs happen more often than with domestic payments.

Here are the most common reasons:

The total cost of receiving an international payment isn't just the transaction fee. It's the fee plus the conversion markup plus any intermediary deductions plus the cost of waiting.

Tip: Ask your payment provider for a full breakdown of all charges, including the exchange rate they apply. If they can't give you a clear answer, that's a sign to look elsewhere.

Clients have different preferences on how they’ll pay. A corporate buyer in Germany might prefer a bank transfer. A small business in the US might pay by credit card. If you only offer one payment option, you risk losing sales or delaying collection.

Here's how the most common methods compare:

Each method has trade-offs between cost, speed, and convenience. Here's a closer look at the ones that matter most for Indian businesses collecting from global clients.

SWIFT is the oldest and most common channel for large B2B payments. Your client's bank sends the payment through the SWIFT network to your bank in India. It's reliable, but it's also the slowest and most expensive option. SWIFT charges can include a sending fee, intermediary bank fees, and a receiving fee on your end.

For invoices above $5,000, wire transfers are still widely used. For smaller amounts, the fees eat into your margin.

A multi-currency account gives you local bank details in currencies like USD, GBP, and EUR. Your client sends a domestic transfer in their own currency, and you receive it in that currency account. You then convert and settle to INR when the rate works for you.

This is usually cheaper and faster than SWIFT because the payment doesn't cross borders on the client's side. It feels like a local payment to them.

Credit and debit card payments are the fastest way to collect from individual buyers or small businesses. The client pays directly through a checkout page or payment link. Settlement is typically within 1 to 3 business days.

The trade-off is cost. Card processing fees are usually 1.5% to 3.5% per transaction. But for businesses where speed and convenience matter more than saving on fees, cards work well.

Services like Apple Pay and region-specific wallets let clients pay invoices quickly from their phone or browser. They're most useful for smaller invoices and clients who prefer not to enter card or bank details manually.

Fees range from 2% to 4.3% per transaction, which makes wallets expensive for large B2B invoices. But for freelancers or businesses collecting smaller amounts from individual buyers, they're a convenient option that speeds up payment.

Automated clearing house (ACH) transfers are common for US-based clients. They're low-cost and work well for recurring payments. The downside is slower settlement (1 to 3 business days), and they're limited to specific countries.

The right method depends on your invoice size, how often you bill, and where your clients are. Many businesses use two or three methods to cover different client preferences.

Note: Offering your client's preferred payment method can reduce the time between sending an invoice and receiving payment by several days.

A missing detail on your invoice can delay payment by days or even weeks. Your client's bank or payment provider needs specific information to process a cross-border transfer. If anything is unclear, the payment gets held up.

Here's what every invoice for international payment should include:

Purpose code: Some banks require a purpose code for inward remittances. Check with your bank and include it on the invoice if needed.

A well-structured invoice for international payment removes guesswork for your client. It also reduces the chance of your bank asking for additional documents after the money arrives.

Tip: If you use a multi-currency account, include those local account details on your invoice. Your client pays a domestic transfer in their currency, which is faster and cheaper for both sides.

The platform you use to collect payments determines how much you pay in fees, how fast you get your money, and how easy it is for your clients to pay. Picking the wrong one costs you on every transaction.

Here's what to look at:

Don't pick a platform based on one feature alone. The cheapest option isn't always the best if the settlement takes a week. The fastest option isn't always worth it if fees are high.

Note: Test the platform with a small transaction first. Check how the fees compare to what was quoted and how long the settlement actually takes.

Small errors on invoices or poor platform choices lead to real financial losses over time. Here are some of the common mistakes to avoid to ensure smooth international payments:

Most of these mistakes are avoidable with a clear invoicing process and the right payment platform.

Tip: Create an invoice template with all required fields pre-filled. Update only the variable details (amount, description, date) for each new client.

A one-time setup saves hours of manual work on every future invoice. If you're still creating invoices from scratch and adding bank details each time, you're spending time you don't need to. Here’s an easy way to set up and enhance your international payment invoicing process:

1. Pick your primary payment methods: Choose 2 to 3 methods based on where your clients are and how they prefer to pay. For most Indian businesses, a multi-currency account plus card payments covers the majority of clients.

2. Set up your multi-currency accounts: Open accounts in the currencies you bill most often (USD, GBP, and EUR are the most common). Share these local account details on your invoices.

3. Create a standard invoice template: Include every field listed in the invoicing section above. Save it as a template you can reuse.

4. Automate where possible: Use a platform that lets you send payment links, set up recurring billing, and track payment status from one place.

5. Set payment terms clearly: State your payment due date, accepted methods, and any late payment terms on every invoice. Clarity up front prevents disputes later.

6. Keep records organized: Save every invoice, payment confirmation, and FIRC. You'll need these for tax filings and compliance.

Once this process is in place, collecting international payments becomes routine. You spend less time on each invoice and more time on the work that generates revenue.

When your clients are in multiple countries, and each one prefers a different payment method, managing collections gets complicated fast. Every extra step between sending an invoice and receiving payment is a step where money or time is lost.

PayGlocal is built for Indian businesses collecting payments from global clients. It supports 33+ currencies, 180+ countries, and 40+ payment methods from a single platform.

Here's what it gives you:

Every freelancer, exporter, and enterprise collecting from global clients gets the same advantage: faster payments, lower fees, and less time spent on admin.

Getting paid for international work shouldn't take weeks or cost a large portion of your invoice. The right payment method, a clear invoice, and a reliable platform make the difference between chasing payments and receiving them on time.

Start by reviewing your current setup. Check what you're paying in fees, how long the settlement takes, and whether your invoices include every detail your client's bank needs. Fix the gaps you find, and you'll see results on your next payment cycle.

PayGlocal helps Indian businesses collect international payments in 120+ currencies from 180+ countries, with lower fees and faster settlement. Stop losing money on every cross-border invoice. Get started with PayGlocal today.

This is a common problem for many businesses in India. As the total Indian exports reached $825.3 billion in FY25, more companies are now sending invoices to clients across the world. Getting your invoice and payment process right is the only way to make sure you get paid on time and keep all of your profit.

This guide covers everything from what your international invoice should include to which collection method works best for your business.

Key takeaways

International invoice payment: It's the process of collecting or sending payment for an invoice when the buyer and seller are in two countries, often involving currency conversion.

- Payment methods vary in cost and speed: Wire transfers, card payments, local bank transfers, and digital wallets each have different fee structures and settlement times.

- Your invoice needs specific details: Include the currency, payment method, bank details, and any reference codes so your client can pay without back-and-forth.

- Choosing the right platform matters: The platform you use to collect payments affects your costs, speed, and how easy it is for your client to pay.

- PayGlocal makes global payments easy: It offers multi-currency accounts, card payments, and 40+ payment methods to collect from clients in 180+ countries.

What is an international invoice payment?

An international invoice payment is a payment made against an invoice when the buyer and seller are in two countries. It typically involves currency conversion, cross-border banking channels, and additional documentation compared to a domestic payment.

For example, a software company in India sends a $5,000 invoice to a client in New York. The client pays using a wire transfer or card payment. The payment travels through one or more banking networks, gets converted from USD to INR, and lands in the company's Indian bank account. The company receives the amount minus any fees and conversion charges.

Why do international invoice payments get delayed or cost more than expected?

A delayed payment doesn't just affect your bank balance. It affects your ability to pay suppliers, manage payroll, and plan for growth. When you sell internationally, delays and unexpected costs happen more often than with domestic payments.

Here are the most common reasons:

- Currency conversion markups: Banks and payment providers often add a margin on top of the mid-market exchange rate. This markup can be typically 1% to 3.5% or more, and it's rarely shown as a separate line item.

- Intermediary bank fees: Wire transfers using the SWIFT network sometimes pass through one or more intermediary banks. Each one can deduct a fee before the money reaches you.

- Incomplete invoice details: If your invoice doesn't include the right bank details, currency, or reference number, your client's bank may reject or delay the transfer.

- Client's payment method: Some methods are slower than others. A SWIFT transfer can take 1 to 5 business days. A local bank transfer through a multi-currency account can settle in 1 to 3 days.

- Compliance documentation: Cross-border payments sometimes need supporting documents like a purpose code or a foreign inward remittance certificate (FIRC). Missing documents hold up the settlement.

The total cost of receiving an international payment isn't just the transaction fee. It's the fee plus the conversion markup plus any intermediary deductions plus the cost of waiting.

Tip: Ask your payment provider for a full breakdown of all charges, including the exchange rate they apply. If they can't give you a clear answer, that's a sign to look elsewhere.

What are the main methods for international invoice payment?

Clients have different preferences on how they’ll pay. A corporate buyer in Germany might prefer a bank transfer. A small business in the US might pay by credit card. If you only offer one payment option, you risk losing sales or delaying collection.

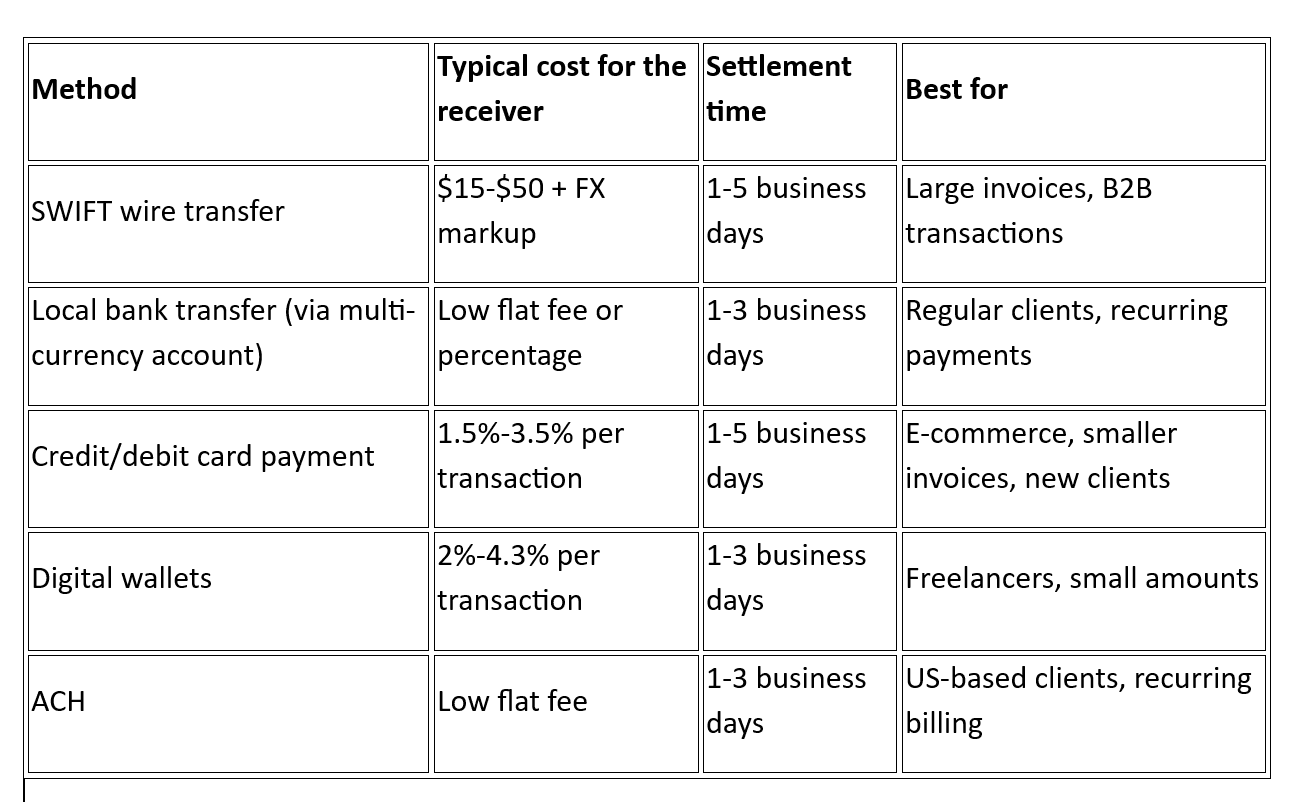

Here's how the most common methods compare:

Each method has trade-offs between cost, speed, and convenience. Here's a closer look at the ones that matter most for Indian businesses collecting from global clients.

1. SWIFT wire transfers

SWIFT is the oldest and most common channel for large B2B payments. Your client's bank sends the payment through the SWIFT network to your bank in India. It's reliable, but it's also the slowest and most expensive option. SWIFT charges can include a sending fee, intermediary bank fees, and a receiving fee on your end.

For invoices above $5,000, wire transfers are still widely used. For smaller amounts, the fees eat into your margin.

2. Local bank transfers via multi-currency accounts

A multi-currency account gives you local bank details in currencies like USD, GBP, and EUR. Your client sends a domestic transfer in their own currency, and you receive it in that currency account. You then convert and settle to INR when the rate works for you.

This is usually cheaper and faster than SWIFT because the payment doesn't cross borders on the client's side. It feels like a local payment to them.

3. Card payments

Credit and debit card payments are the fastest way to collect from individual buyers or small businesses. The client pays directly through a checkout page or payment link. Settlement is typically within 1 to 3 business days.

The trade-off is cost. Card processing fees are usually 1.5% to 3.5% per transaction. But for businesses where speed and convenience matter more than saving on fees, cards work well.

4. Digital wallets

Services like Apple Pay and region-specific wallets let clients pay invoices quickly from their phone or browser. They're most useful for smaller invoices and clients who prefer not to enter card or bank details manually.

Fees range from 2% to 4.3% per transaction, which makes wallets expensive for large B2B invoices. But for freelancers or businesses collecting smaller amounts from individual buyers, they're a convenient option that speeds up payment.

5. ACH

Automated clearing house (ACH) transfers are common for US-based clients. They're low-cost and work well for recurring payments. The downside is slower settlement (1 to 3 business days), and they're limited to specific countries.

The right method depends on your invoice size, how often you bill, and where your clients are. Many businesses use two or three methods to cover different client preferences.

Note: Offering your client's preferred payment method can reduce the time between sending an invoice and receiving payment by several days.

What should an invoice for international payment include?

A missing detail on your invoice can delay payment by days or even weeks. Your client's bank or payment provider needs specific information to process a cross-border transfer. If anything is unclear, the payment gets held up.

Here's what every invoice for international payment should include:

- Your business name and address: Full registered name and address. This needs to match your bank records.

- Client's business name and address: Full details of the buyer, including their country.

- Invoice number and date: A unique number for tracking and a clear issue date.

- Description of goods or services: What you delivered, with enough detail for the client's finance team to approve payment.

- Amount and currency: Clearly state the total amount and the currency you want to be paid in (e.g., USD 5,000). Don't leave the currency ambiguous.

- Payment method and bank details: Include your bank name, account number, SWIFT code, and any routing numbers. If you use a multi-currency account, include those local account details instead.

- Payment due date: Write a specific date instead of vague terms. Your client's finance team processes faster when the deadline is clear.

Purpose code: Some banks require a purpose code for inward remittances. Check with your bank and include it on the invoice if needed.

A well-structured invoice for international payment removes guesswork for your client. It also reduces the chance of your bank asking for additional documents after the money arrives.

Tip: If you use a multi-currency account, include those local account details on your invoice. Your client pays a domestic transfer in their currency, which is faster and cheaper for both sides.

How do you choose the right platform for international invoice payments?

The platform you use to collect payments determines how much you pay in fees, how fast you get your money, and how easy it is for your clients to pay. Picking the wrong one costs you on every transaction.

Here's what to look at:

- Supported currencies and countries: Make sure the platform covers the currencies and countries your clients are in. If you sell to clients in 10 countries but your platform only supports 5, you'll need workarounds for the rest.

- Fee structure: Compare the total cost, not just the transaction fee. Look at currency conversion costs, settlement fees, and any monthly or annual charges.

- Settlement speed: How quickly does the money reach your Indian bank account? Some platforms settle in 1 to 2 days. Others take a week.

- Payment methods offered: Does the platform support cards, bank transfers, and local payment methods? The more options your clients have, the faster they'll pay.

- Compliance support: Does the platform handle documentation like FIRC automatically? Manual compliance work slows everything down.

- Ease of use: Can you send payment links, create invoices, and track payments from one dashboard?

Don't pick a platform based on one feature alone. The cheapest option isn't always the best if the settlement takes a week. The fastest option isn't always worth it if fees are high.

Note: Test the platform with a small transaction first. Check how the fees compare to what was quoted and how long the settlement actually takes.

What mistakes do businesses make with international invoice payments?

Small errors on invoices or poor platform choices lead to real financial losses over time. Here are some of the common mistakes to avoid to ensure smooth international payments:

- Not specifying the invoice currency: If your invoice says "5,000" without a currency symbol or code, your client might pay in their local currency instead of yours. Always write "USD 5,000" or "GBP 3,000" clearly.

- Using only one payment method: Offering only SWIFT transfers forces clients to pay higher fees and wait longer. Add at least one alternative, like a card payment link or local bank transfer option.

- Ignoring FX markups: The exchange rate your provider uses can cost you 1% to 3% on every payment. Compare the rate you receive against the mid-market rate to see the real markup.

- Sending incomplete bank details: A missing SWIFT code or incorrect account number causes the payment to bounce or get stuck. Double-check every detail before sending your invoice.

- Not tracking payments: Without a system to track which invoices are paid, pending, or overdue, you'll spend hours each month chasing clients manually.

- Waiting too long to follow up: If a payment is 3 days past due, send a reminder. Waiting weeks makes it harder to collect and signals that late payment is acceptable.

Most of these mistakes are avoidable with a clear invoicing process and the right payment platform.

Tip: Create an invoice template with all required fields pre-filled. Update only the variable details (amount, description, date) for each new client.

How should you set up your international invoice payment process?

A one-time setup saves hours of manual work on every future invoice. If you're still creating invoices from scratch and adding bank details each time, you're spending time you don't need to. Here’s an easy way to set up and enhance your international payment invoicing process:

1. Pick your primary payment methods: Choose 2 to 3 methods based on where your clients are and how they prefer to pay. For most Indian businesses, a multi-currency account plus card payments covers the majority of clients.

2. Set up your multi-currency accounts: Open accounts in the currencies you bill most often (USD, GBP, and EUR are the most common). Share these local account details on your invoices.

3. Create a standard invoice template: Include every field listed in the invoicing section above. Save it as a template you can reuse.

4. Automate where possible: Use a platform that lets you send payment links, set up recurring billing, and track payment status from one place.

5. Set payment terms clearly: State your payment due date, accepted methods, and any late payment terms on every invoice. Clarity up front prevents disputes later.

6. Keep records organized: Save every invoice, payment confirmation, and FIRC. You'll need these for tax filings and compliance.

Once this process is in place, collecting international payments becomes routine. You spend less time on each invoice and more time on the work that generates revenue.

Accept international invoice payments faster with PayGlocal

When your clients are in multiple countries, and each one prefers a different payment method, managing collections gets complicated fast. Every extra step between sending an invoice and receiving payment is a step where money or time is lost.

PayGlocal is built for Indian businesses collecting payments from global clients. It supports 33+ currencies, 180+ countries, and 40+ payment methods from a single platform.

Here's what it gives you:

- Built-in invoicing: Create professional invoices with your branding, send them directly to clients, and track payment status from the same place you collect funds.

- Automated FIRC: Receive your foreign inward remittance certificate right after settlement, keeping your compliance records up to date without extra effort.

- One platform: Track every invoice, payment, and settlement from a single dashboard, giving you full visibility into your cash flow at any time.

- Global payment methods: Offer 40+ local payment options your clients already trust, which increases the chance they pay quickly.

- Recurring payments: Set up automatic billing for retainer clients or subscription services, and payments arrive on schedule without manual follow-up.

Every freelancer, exporter, and enterprise collecting from global clients gets the same advantage: faster payments, lower fees, and less time spent on admin.

Final thoughts

Getting paid for international work shouldn't take weeks or cost a large portion of your invoice. The right payment method, a clear invoice, and a reliable platform make the difference between chasing payments and receiving them on time.

Start by reviewing your current setup. Check what you're paying in fees, how long the settlement takes, and whether your invoices include every detail your client's bank needs. Fix the gaps you find, and you'll see results on your next payment cycle.

PayGlocal helps Indian businesses collect international payments in 120+ currencies from 180+ countries, with lower fees and faster settlement. Stop losing money on every cross-border invoice. Get started with PayGlocal today.