You delivered the project three weeks ago. Your client confirmed they sent the payment. But your bank account shows nothing. You call your bank. They mention a compliance hold, but can't tell you when it will clear or if it will clear at all.

International payments bring risks that domestic payments don't. Data shows that nearly 79% of businesses face payment fraud attempts on international transactions. One bad payment can freeze your funds or lead to compliance reviews, costing you time and money.

If you're doing business across borders, you need to know how to manage payment risk. This includes protecting your revenue, ensuring payments flow smoothly, and avoiding common issues that cause payment delays or failures. Here's what you need to know to get paid reliably.

International payment risk management is how you identify and reduce the risks that come with accepting payments from customers in other countries. While domestic payments in India are predictable and instant, global transactions move through intermediary banks, volatile exchange rates, and manual compliance checks.

Every step in this chain introduces a point of failure. A payment might be held because a compliance algorithm misread your client's address, or a transaction might be "short-settled" because an intermediary bank took an unexpected cut. Worse, you could face a chargeback months after you've already spent the revenue.

For an Indian SaaS or export business, risk management is the active process of ensuring your transactions are coded correctly, screened for fraud before they hit the network, and protected from the volatility of exchange rate shifts. It's about making sure the money your client sent actually becomes the money you can spend.

Risk management isn't a single check; it's a series of invisible filters that every transaction must pass through before it reaches your balance. These filters act as your frontline defense, stopping high-risk activity before it can trigger a bank hold or a compliance audit.

Here is how that defensive chain works:

For an Indian business, this means a £5,000 payment from London doesn't just show up. It arrives cleaned of fraud risk, verified for compliance, and backed by the documentation you need for your auditors.

Each stage in the global payment process can go wrong in different ways. Currency values change while payments are in transit, fraud filters block legitimate customers, and compliance rules vary by country. Knowing these risks helps you prevent them effectively.

The value of currencies changes constantly. If you invoice a customer in USD and they pay two weeks later, the exchange rate might have moved. For instance, what was worth ₹83,000 at invoicing could be ₹81,500 by settlement. You delivered the full service, but you earn less.

Cross-border transactions get declined more often than domestic ones. A customer's bank in the US or UK might flag a legitimate payment to India simply because it looks unusual for their card profile. High decline rates don't just lose you one sale; they damage your reputation with the client.

Every international payment needs to be screened against sanction lists. If your payment involves a blocked entity or passes through a restricted country, it can be frozen or rejected. Missing compliance documentation, like FIRC, can also create issues during audits.

International transactions are more attractive to fraudsters. Stolen cards, fake identities, and friendly fraud (where a customer disputes a legitimate charge) all happen more frequently across borders. Chargebacks not only reverse the payment but often come with penalties.

Some countries have currency controls, unstable banking systems, or situations that make it hard to move money. A payment might be approved, but still get stuck due to local restrictions you have no control over.

With traditional banking routes, you often don't know where your payment is. It leaves the customer's account, passes through intermediaries, and eventually reaches you, but you have no real-time visibility. This makes cash flow planning difficult.

Even when a payment is approved, it can take days or weeks to settle. Funds might sit in intermediary banks or clearing systems, delaying access to your money.

International payments often come with hidden fees. Intermediary bank charges, exchange rate markups, and processing fees can reduce what you actually receive. Without transparency, you don't know the true cost until after settlement.

Note: These risks don't operate separately. A payment can face multiple issues at once. For example, a transaction might pass fraud checks but still get delayed due to compliance screening, and then settle at a worse exchange rate than expected. The cumulative effect creates cash flow uncertainty and makes it harder to scale internationally with confidence.

Risk management isn't just about security; it's about liquidity. For a growing Indian exporter or SaaS founder, it is the difference between scaling with cash in hand and being held hostage by a "payment pending" status for three weeks.

Here's how tightening your risk controls can unlock operational speed for your business:

The cost of ignoring risk management isn't just a fee; it's the lost time spent in back-and-forth emails with support desks and bank managers trying to locate "stuck" funds.

Managing risk isn't about avoiding global trade; it's about using tools that turn a fragmented cross-border process into a predictable one. For an Indian business, this means moving away from "hope-based" banking and adopting an active defense:

Not all payment methods carry the same risk. Cash in advance is the safest for you, but the least convenient for customers. Open account terms (invoicing with payment due later) are convenient but risky if the customer doesn't pay. Cards and payment gateways sit in between, offering balance and speed.

For exporters and service providers, accepting international cards through a reliable payment platform reduces risk while keeping the process smooth for customers. You get faster settlements, built-in fraud checks, and fewer manual steps.

Fraud is higher in cross-border payments. A good payment platform screens transactions in real time, flags suspicious patterns, and blocks high-risk payments before they reach you. This protects you from chargebacks and reduces the chance of dealing with fraudulent transactions.

For instance, advanced fraud engines analyze device data, card history, and location signals to identify threats without blocking legitimate customers.

Currency fluctuations are hard to predict. If you're invoicing in a foreign currency, the value can shift between the invoice and the payment. Platforms that offer transparent, locked-in exchange rates at the time of transaction remove this uncertainty. You know exactly what you'll receive.

Some providers also let you collect payments in local currencies (USD, GBP, EUR, CAD) and settle in INR, reducing exposure to rate changes during the settlement window.

Manual compliance checks slow down payments and increase the risk of errors. Platforms that automatically screen transactions against global sanction lists (OFAC, UNSC, EU, HM Treasury) ensure you're not dealing with blocked entities. Automatic FIRC generation also keeps you compliant without manual paperwork.

This is particularly important if you're dealing with customers in multiple countries, where regulations vary.

Not knowing where your money is creates cash flow uncertainty. Payment platforms with real-time tracking show you exactly where funds are at every stage, from customer payment to your account settlement. You get alerts when payments are received, processed, and cleared.

This visibility helps you plan cash flow, follow up on delays, and give customers accurate information when they ask about payment status.

Payment failures happen when transactions aren't formatted correctly for international issuers, when fraud filters are too aggressive, or when the wrong processing route is used. Platforms with intelligent payment orchestration automatically optimize how transactions are routed, formatted, and messaged to increase approval rates.

Higher approval rates mean fewer lost sales and less time spent troubleshooting failed payments.

Tip: Choose a payment provider that offers transparent fees, real-time tracking, and automatic compliance. This removes most of the manual risk management work and protects your revenue.

Most payment failures aren't bad luck; they are the result of systemic blind spots. If you are relying on legacy banking processes or manual checks, you are actively increasing your exposure to fraud, settlement delays, and margin erosion.

To secure your cash flow, you have to eliminate these high-risk habits:

You can't run a global business if you're spending half your day playing detective with your own bank. Eliminating these foundational errors turns your payment setup from a liability into a competitive advantage.

Each payment platform handles the international payment risk in different ways. The right choice depends on what problems you need to solve and how you operate. Here's what to look for:

Tip: Start with your biggest challenge. If payments fail often, prioritize approval rates. If compliance takes too much time, prioritize automation. If you don't know where your money is, prioritize tracking.

International payment risk doesn't have to slow you down or take up your margins. The right payment platform removes these international risks automatically while giving you full visibility and control.

If you're accepting payments from customers in the US, UK, UAE, Canada, or anywhere else, you need a solution built for cross-border complexity. That's where PayGlocal comes in. Here's how the platform can help you:

PayGlocal helps businesses reduce payment failures, speed up settlements, and stay compliant across borders without the manual work.

Managing payment risk in international trade is how you protect your revenue and keep your business running smoothly. Currency fluctuations, payment failures, compliance gaps, and fraud all create exposure you don't face with domestic payments.

The good news is that you don't have to manage these risks manually. Modern payment platforms like PayGlocal handle fraud detection, compliance screening, currency management, and real-time tracking automatically. You get higher approval rates, faster settlements, and full visibility into where your money is.

Your competitors are already using advanced tools to collect payments reliably and scale internationally. If you're growing across borders, you need a reliable payment infrastructure that matches your business. Stop chasing payments and start collecting them with confidence.

Get started with PayGlocal today to secure your international payment processes.

International payments bring risks that domestic payments don't. Data shows that nearly 79% of businesses face payment fraud attempts on international transactions. One bad payment can freeze your funds or lead to compliance reviews, costing you time and money.

If you're doing business across borders, you need to know how to manage payment risk. This includes protecting your revenue, ensuring payments flow smoothly, and avoiding common issues that cause payment delays or failures. Here's what you need to know to get paid reliably.

Key Takeaways

- Currency risk: Exchange rate fluctuations can reduce your actual earnings even when the customer pays in full.

- Payment failures: International transactions face higher decline rates due to fraud checks, compliance filters, and issuer limitations.

- Compliance exposure: Missing documentation or sanction screening can delay payments or trigger penalties.

- Fraud and chargeback risk: Cross-border transactions are more vulnerable to fraudulent activity and disputed charges.

- Reliable payment platform: PayGlocal helps in handling common international payment risks with advanced fraud protection, automatic compliance, and higher approval rates for international payments.

What is International Payment Risk Management?

International payment risk management is how you identify and reduce the risks that come with accepting payments from customers in other countries. While domestic payments in India are predictable and instant, global transactions move through intermediary banks, volatile exchange rates, and manual compliance checks.

Every step in this chain introduces a point of failure. A payment might be held because a compliance algorithm misread your client's address, or a transaction might be "short-settled" because an intermediary bank took an unexpected cut. Worse, you could face a chargeback months after you've already spent the revenue.

For an Indian SaaS or export business, risk management is the active process of ensuring your transactions are coded correctly, screened for fraud before they hit the network, and protected from the volatility of exchange rate shifts. It's about making sure the money your client sent actually becomes the money you can spend.

How Does International Payment Risk Management Work?

Risk management isn't a single check; it's a series of invisible filters that every transaction must pass through before it reaches your balance. These filters act as your frontline defense, stopping high-risk activity before it can trigger a bank hold or a compliance audit.

Here is how that defensive chain works:

- Real-time Fraud Screening: The moment your customer clicks "pay," the system analyzes device fingerprints, location data, and card history. It's looking for the subtle patterns of stolen credentials or "card testing" that a human eye would miss.

- Sanction & Regulatory Guardrails: Every transaction is instantly cross-referenced against global sanction lists. This ensures you aren't unknowingly accepting funds from restricted entities, a mistake that could get your own accounts flagged.

- Intelligent Network Routing: The system selects the processing path most likely to succeed based on the client's country and card type. This reduces "false positives" where a legitimate bank might decline a transaction simply because it looks "unusual" for a cross-border payment.

- Settlement & Compliance Automation: Once approved, funds move through the payment network. You receive a settlement in your account, along with compliance documentation like the Foreign Inward Remittance Certificate (FIRC).

For an Indian business, this means a £5,000 payment from London doesn't just show up. It arrives cleaned of fraud risk, verified for compliance, and backed by the documentation you need for your auditors.

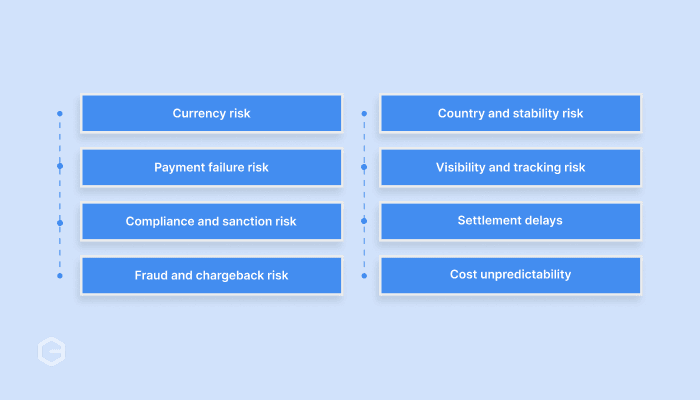

What are the main risks in international payments?

Each stage in the global payment process can go wrong in different ways. Currency values change while payments are in transit, fraud filters block legitimate customers, and compliance rules vary by country. Knowing these risks helps you prevent them effectively.

Currency Risk

The value of currencies changes constantly. If you invoice a customer in USD and they pay two weeks later, the exchange rate might have moved. For instance, what was worth ₹83,000 at invoicing could be ₹81,500 by settlement. You delivered the full service, but you earn less.

Payment Failure Risk

Cross-border transactions get declined more often than domestic ones. A customer's bank in the US or UK might flag a legitimate payment to India simply because it looks unusual for their card profile. High decline rates don't just lose you one sale; they damage your reputation with the client.

Compliance and Sanction Risk

Every international payment needs to be screened against sanction lists. If your payment involves a blocked entity or passes through a restricted country, it can be frozen or rejected. Missing compliance documentation, like FIRC, can also create issues during audits.

Fraud and Chargeback Risk

International transactions are more attractive to fraudsters. Stolen cards, fake identities, and friendly fraud (where a customer disputes a legitimate charge) all happen more frequently across borders. Chargebacks not only reverse the payment but often come with penalties.

Country and Stability Risk

Some countries have currency controls, unstable banking systems, or situations that make it hard to move money. A payment might be approved, but still get stuck due to local restrictions you have no control over.

Visibility and Tracking Risk

With traditional banking routes, you often don't know where your payment is. It leaves the customer's account, passes through intermediaries, and eventually reaches you, but you have no real-time visibility. This makes cash flow planning difficult.

Settlement Delays

Even when a payment is approved, it can take days or weeks to settle. Funds might sit in intermediary banks or clearing systems, delaying access to your money.

Cost Unpredictability

International payments often come with hidden fees. Intermediary bank charges, exchange rate markups, and processing fees can reduce what you actually receive. Without transparency, you don't know the true cost until after settlement.

Note: These risks don't operate separately. A payment can face multiple issues at once. For example, a transaction might pass fraud checks but still get delayed due to compliance screening, and then settle at a worse exchange rate than expected. The cumulative effect creates cash flow uncertainty and makes it harder to scale internationally with confidence.

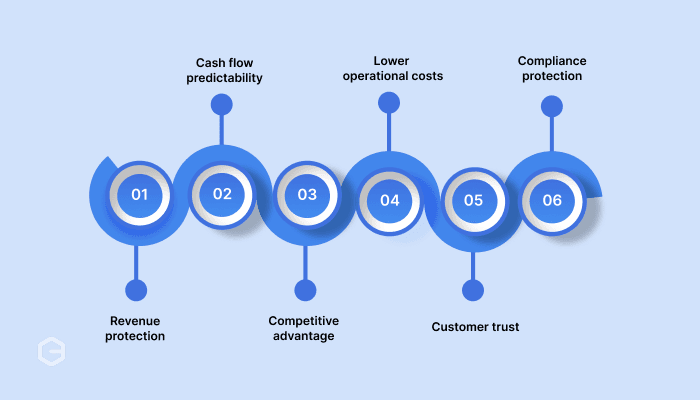

Why International Payment Risk Management Matters for Your Business?

Risk management isn't just about security; it's about liquidity. For a growing Indian exporter or SaaS founder, it is the difference between scaling with cash in hand and being held hostage by a "payment pending" status for three weeks.

Here's how tightening your risk controls can unlock operational speed for your business:

- Revenue protection: Fewer failed payments mean more money in your account. Higher approval rates directly increase your earnings.

- Cash flow predictability: When you know payments will clear on time, you can plan expenses, pay suppliers, and run payroll without gaps.

- Competitive advantage: Customers prefer businesses where checkout works smoothly. If your payment system fails less often than competitors, you win more deals.

- Lower operational costs: Automatic compliance and fraud detection remove manual work. Your team spends less time chasing payments or fixing issues.

- Customer trust: When payments process cleanly without declines or delays, customers come back. Failed transactions damage relationships.

- Compliance protection: Automatic sanction screening and documentation keep you out of legal trouble and make audits easier.

The cost of ignoring risk management isn't just a fee; it's the lost time spent in back-and-forth emails with support desks and bank managers trying to locate "stuck" funds.

How to Manage Risk in International Payments

Managing risk isn't about avoiding global trade; it's about using tools that turn a fragmented cross-border process into a predictable one. For an Indian business, this means moving away from "hope-based" banking and adopting an active defense:

Pick Secure Payment Methods

Not all payment methods carry the same risk. Cash in advance is the safest for you, but the least convenient for customers. Open account terms (invoicing with payment due later) are convenient but risky if the customer doesn't pay. Cards and payment gateways sit in between, offering balance and speed.

For exporters and service providers, accepting international cards through a reliable payment platform reduces risk while keeping the process smooth for customers. You get faster settlements, built-in fraud checks, and fewer manual steps.

Use Platforms with Built-in Fraud Detection

Fraud is higher in cross-border payments. A good payment platform screens transactions in real time, flags suspicious patterns, and blocks high-risk payments before they reach you. This protects you from chargebacks and reduces the chance of dealing with fraudulent transactions.

For instance, advanced fraud engines analyze device data, card history, and location signals to identify threats without blocking legitimate customers.

Lock in Exchange Rates Where Possible

Currency fluctuations are hard to predict. If you're invoicing in a foreign currency, the value can shift between the invoice and the payment. Platforms that offer transparent, locked-in exchange rates at the time of transaction remove this uncertainty. You know exactly what you'll receive.

Some providers also let you collect payments in local currencies (USD, GBP, EUR, CAD) and settle in INR, reducing exposure to rate changes during the settlement window.

Automate Compliance and Sanction Screening

Manual compliance checks slow down payments and increase the risk of errors. Platforms that automatically screen transactions against global sanction lists (OFAC, UNSC, EU, HM Treasury) ensure you're not dealing with blocked entities. Automatic FIRC generation also keeps you compliant without manual paperwork.

This is particularly important if you're dealing with customers in multiple countries, where regulations vary.

Track Payments in Real Time

Not knowing where your money is creates cash flow uncertainty. Payment platforms with real-time tracking show you exactly where funds are at every stage, from customer payment to your account settlement. You get alerts when payments are received, processed, and cleared.

This visibility helps you plan cash flow, follow up on delays, and give customers accurate information when they ask about payment status.

Reduce Payment Failures with Smart Routing

Payment failures happen when transactions aren't formatted correctly for international issuers, when fraud filters are too aggressive, or when the wrong processing route is used. Platforms with intelligent payment orchestration automatically optimize how transactions are routed, formatted, and messaged to increase approval rates.

Higher approval rates mean fewer lost sales and less time spent troubleshooting failed payments.

Tip: Choose a payment provider that offers transparent fees, real-time tracking, and automatic compliance. This removes most of the manual risk management work and protects your revenue.

What are the common mistakes that increase international payment risk?

Most payment failures aren't bad luck; they are the result of systemic blind spots. If you are relying on legacy banking processes or manual checks, you are actively increasing your exposure to fraud, settlement delays, and margin erosion.

To secure your cash flow, you have to eliminate these high-risk habits:

- Using only traditional banking: Bank transfers are slow and give you no visibility. You don't know where payments are or when they'll arrive. Modern platforms show you real-time status.

- Ignoring fraud screening: Waiting until after a chargeback to think about fraud is expensive. Built-in fraud detection blocks bad transactions before they cost you money.

- Accepting high decline rates: If a high percentage of your international payments fail, that's not normal. Better routing and transaction formatting can significantly increase approval rates.

- Manual compliance work: Requesting FIRC documents from your bank or checking sanction lists manually wastes time and creates errors. Automation handles this instantly.

- No cost transparency: Hidden fees and exchange rate markups reduce what you actually receive. You should know the full cost before accepting a payment.

You can't run a global business if you're spending half your day playing detective with your own bank. Eliminating these foundational errors turns your payment setup from a liability into a competitive advantage.

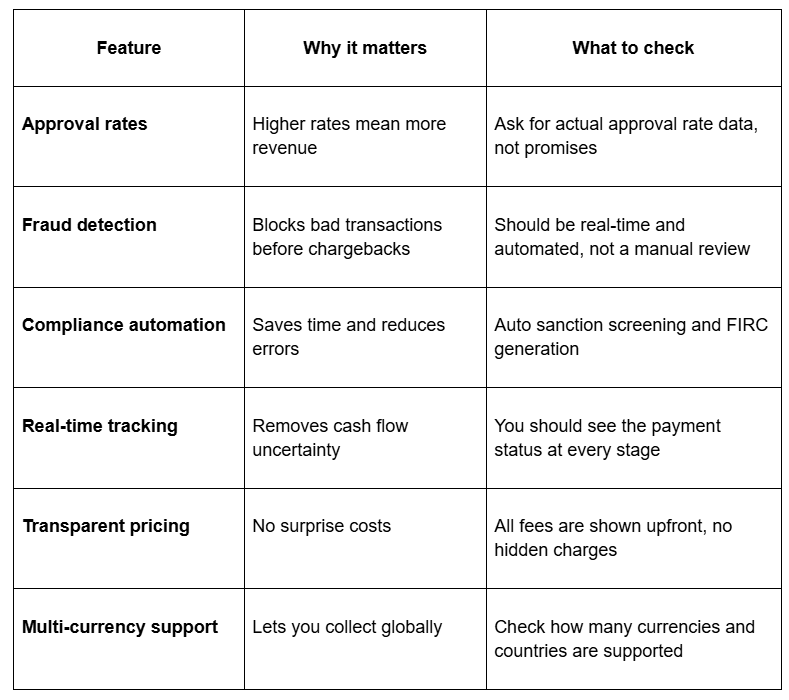

How to Choose the Right Payment Risk Management Solution?

Each payment platform handles the international payment risk in different ways. The right choice depends on what problems you need to solve and how you operate. Here's what to look for:

Tip: Start with your biggest challenge. If payments fail often, prioritize approval rates. If compliance takes too much time, prioritize automation. If you don't know where your money is, prioritize tracking.

Secure Your International Transactions with PayGlocal

International payment risk doesn't have to slow you down or take up your margins. The right payment platform removes these international risks automatically while giving you full visibility and control.

If you're accepting payments from customers in the US, UK, UAE, Canada, or anywhere else, you need a solution built for cross-border complexity. That's where PayGlocal comes in. Here's how the platform can help you:

- Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries, with local accounts in USD, GBP, EUR, and CAD.

- Advanced fraud protection: Built-in fraud detection analyzes device data, card history, and location signals to block suspicious transactions while approving legitimate payments.

- Recurring payments: Execute subscriptions and recurring billing on international cards with network-compliant solutions for predictable revenue.

- Sanction screening: Automatic screening against global sanction lists with zero-knowledge-proof technology to protect your business.

- Easy compliance documentation: Get FIRC directly after settlement, with no manual paperwork or delays.

PayGlocal helps businesses reduce payment failures, speed up settlements, and stay compliant across borders without the manual work.

Final Thoughts

Managing payment risk in international trade is how you protect your revenue and keep your business running smoothly. Currency fluctuations, payment failures, compliance gaps, and fraud all create exposure you don't face with domestic payments.

The good news is that you don't have to manage these risks manually. Modern payment platforms like PayGlocal handle fraud detection, compliance screening, currency management, and real-time tracking automatically. You get higher approval rates, faster settlements, and full visibility into where your money is.

Your competitors are already using advanced tools to collect payments reliably and scale internationally. If you're growing across borders, you need a reliable payment infrastructure that matches your business. Stop chasing payments and start collecting them with confidence.

Get started with PayGlocal today to secure your international payment processes.