You shipped the product, delivered the service, and sent the invoice. Now you're waiting for the money to actually arrive. For businesses selling globally, that wait can stretch into days or even weeks if they don’t have the right international payment systems in place.

According to recent data, the global payments industry accounts for $2.5 trillion in revenue from around 3.6 trillion transactions. That's a massive volume of money moving across borders, and every delay or failure in that flow costs real revenue.

This post breaks down the key advantages of international payment systems. You'll learn how they work and how to pick the right one for your business.

An international payment system moves money between buyers and sellers across countries. It handles currency conversion, routes the payment through the right channels, and settles the funds into your account. The goal is to make cross-border payments work as smoothly as domestic ones.

For instance, an online store in India sells products to a buyer in Germany. The buyer pays in euros through the store's checkout. The international payment system converts the euros, processes the transaction through the right network, and deposits Indian rupees into the seller's account, all within a day or two.

Without that system, the seller would need to rely on a SWIFT transfer that could take three to five business days and cost significantly more in fees.

These systems are used by exporters, freelancers, SaaS companies, travel businesses, and anyone in India who collects money from customers or clients abroad.

Tip: If you collect payments from more than one country, you likely need an international payment system, not just a bank account that accepts foreign wire transfers.

When a payment crosses borders, it passes through several steps before reaching your account. A delayed or failed payment usually means one of these steps didn't go as planned.

Here's what happens in a typical international transaction.

1. Payment initiation: The buyer enters their payment details at checkout, choosing a card, digital wallet, or local bank transfer.

2. Authentication: The system verifies the buyer's identity and checks for fraud signals before the payment moves forward.

3. Routing: The payment is sent through the most efficient network based on the buyer's location, currency, and payment method.

4. Currency conversion: The system converts the buyer's currency into your preferred settlement currency at the current exchange rate.

5. Authorization: The buyer's bank or payment provider approves or declines the transaction based on available funds and risk checks.

6. Settlement: The converted funds are deposited into your bank account, typically within one to three business days.

Each step is handled automatically by the payment system. The fewer manual steps involved, the faster and more reliable the process becomes.

Tip: Look for a system that handles routing and conversion in one step. Fewer handoffs between banks and processors usually result in lower fees and fewer failures.

A slow, expensive, or unreliable payment setup costs you more than fees. It costs you customers, time, and the ability to grow into new markets. Here are the key benefits of international payment systems that matter most for businesses in India selling globally:

Traditional bank-to-bank transfers across borders often take three to five business days. Modern international payment systems reduce that to same-day or next-day settlement in many cases.

For an exporter waiting on a large payment to release a new shipment, that difference is significant. Faster access to funds keeps your business moving without relying on credit to cover the wait.

Cross-border payments through traditional banks often involve intermediary fees, markup on currency conversion, and receiving charges.

International payment systems reduce these by routing payments directly and offering competitive exchange rates. Over hundreds of transactions a month, even a small reduction per transaction adds up to a meaningful amount. Your hidden costs drop, and your margins improve.

Credit cards aren't the default payment method everywhere. In the Netherlands, for instance, buyers prefer iDEAL. In Germany, many use SOFORT.

A good international payment system lets you offer local payment methods that match what your buyers already trust. This directly improves your checkout completion rate because buyers don't abandon a purchase when they see a familiar option.

Showing prices in a buyer's local currency builds trust and reduces confusion at checkout. International payment systems handle this automatically. They accept payments in the buyer's currency and settle in yours, typically INR for Indian businesses.

You don't need to manage separate accounts for each currency or calculate conversion rates yourself. The system does it, and your multi-currency accounts keep everything organized.

A failed transaction doesn't just mean a retry. It often means a lost customer. International payment systems improve approval rates by sending the right data to issuing banks, using local acquiring networks, and applying smart routing.

When the buyer's bank sees a familiar transaction format, it's more likely to approve the payment. For businesses with high transaction volumes, even a five-percent improvement in approvals has a direct impact on revenue.

Cross-border transactions carry a higher fraud risk than domestic ones. International payment systems include fraud screening that checks device data, location, transaction history, and card behavior before approving a payment.

This protects you from chargebacks and fraudulent orders without blocking genuine buyers. The screening happens in real time, so it doesn't slow down the checkout experience.

Selling internationally comes with documentation requirements, including certificates and tax records for every inward remittance. Modern payment systems generate these automatically.

For Indian businesses, getting a foreign inward remittance certificate (FIRC) after every settlement saves hours of manual follow-up with banks. Everything is tracked, recorded, and available from a dashboard.

Adding a new country to your sales map shouldn't require a new banking relationship or payment integration. International payment systems are built to cover many countries and currencies from a single setup.

When you're ready to sell in Australia, the Middle East, or Southeast Asia, your payment infrastructure is already there. Scaling becomes a business decision, not a technical one.

The benefits of international payment systems go beyond any single feature. Together, they create a payment experience that works for your buyers and keeps your business running efficiently.

Note: The biggest advantage isn't any one benefit. It's having all of them work together in a single system, so you don't need to patch five tools into one workflow.

You might assume these systems are only for large companies. In reality, any business in India that collects money from abroad can benefit. The value depends on your business model and where your buyers are. Here are the business types that gain the most advantage from international payment systems:

Tip: If international payments make up more than 20% of your monthly revenue, a dedicated system will likely pay for itself through lower fees and higher approval rates alone.

If your domestic payments work fine, you might wonder why international payments need a separate system at all. The difference comes down to what happens behind the scenes when money crosses a border. Here's a side-by-side comparison:

A domestic payment setup can't handle international sales well. Currency conversion alone adds a layer of cost and complexity that domestic transactions don't have.

For Indian businesses selling globally, the key point to note is that international payments require purpose-built infrastructure. Trying to force domestic tools into a global workflow leads to higher fees, slower settlement, and more failed transactions.

Tip: If you're currently accepting international payments through a domestic gateway, compare your approval rates and fees against a dedicated cross-border payment platform. The difference is often significant.

Picking a payment system based only on price is a common mistake. The cheapest option often has hidden limitations that cost more in the long run. Here's what to evaluate before you commit:

Don't finalize based on a features list alone. Ask for a demo or test environment and run a few transactions to see the actual experience.

Even after choosing a good system, businesses often make errors that reduce its value. These mistakes are avoidable once you know what to watch for.

Most of these mistakes come from a set-it-and-forget-it approach. Your payment system needs regular attention, just like any other part of your business.

Tip: Review your payment success rates and decline reasons at least once a month. Small adjustments to fraud filters or payment method offerings can recover lost revenue.

Knowing the advantages is good. But putting the right system in place is what actually brings results. Here's a simple process to get started:

1. Identify your buyer locations: List the top five to ten countries where your customers or clients are based. This determines the currencies and payment methods you need.

2. Audit your current setup: Look at your existing payment flow. Note the fees, settlement time, approval rates, and any recurring issues like failed transactions or delayed FIRCs.

3. Shortlist providers: Based on the criteria in the "how to choose" section above, narrow your options to two or three platforms that fit your business type and scale.

4. Run a test: Most providers offer a test setup where you can simulate transactions. Use it to check the checkout experience, response time, and reporting dashboard.

5. Go live with a small volume: Start with a portion of your traffic to compare performance against your current setup. Track approval rates, fees, and settlement time.

6. Scale gradually: Once you're confident in the results, move your full transaction volume to the new system. Add local payment methods for your highest-traffic markets first.

Getting started doesn't require a full migration on day one. A phased approach lets you compare results and make informed adjustments.

International payments shouldn't be the reason you lose a sale. Yet for many businesses selling globally, failed transactions, high fees, and limited payment options have become common. It doesn’t have to be that way when you pick the right payment platform.

PayGlocal is built for Indian businesses that collect payments from global customers. Here's what you get:

PayGlocal gives Indian businesses a complete payment setup that covers cards, local methods, compliance, and fraud protection in one place. You pay only when you transact, with no setup fees or monthly charges.

The advantages of international payment systems directly affect how fast you get paid, how much you keep, and how many global buyers complete their purchase. For Indian businesses selling across borders, the right system is a core part of your growth.

Start by reviewing your current payment setup. Look at your fees, settlement times, and approval rates. If any of those numbers are costing you revenue, it's time to make a change.

Every week you wait to fix a broken payment flow, you're leaving money with customers who wanted to pay you. Get started with PayGlocal today.

1. Can freelancers in India use international payment systems?

Yes, freelancers can use these systems to collect payments from global clients. They work well for project-based billing, retainer payments, and marketplace payouts from freelancing platforms.

2. Do international payment systems support recurring billing?

Yes, many platforms support recurring billing on international cards. This is useful for subscription businesses, SaaS companies, and service providers who bill clients on a monthly or annual cycle.

3. What's the difference between a payment gateway and a payment system?

A payment gateway is the technology that captures and transmits payment data at checkout. An international payment system is broader and includes routing, currency conversion, fraud screening, and settlement.

4. Are international payment systems safe to use?

Yes, reputable systems use encryption, tokenization, and real-time fraud screening to protect both merchants and buyers. Look for providers that hold recognized security certifications.

5. Do these systems work with e-commerce platforms like Shopify?

Yes, most international payment systems offer plug-ins or built-in integrations for popular platforms like Shopify, WooCommerce, and Magento. Setup typically takes a few hours to a few days, depending on the system.

According to recent data, the global payments industry accounts for $2.5 trillion in revenue from around 3.6 trillion transactions. That's a massive volume of money moving across borders, and every delay or failure in that flow costs real revenue.

This post breaks down the key advantages of international payment systems. You'll learn how they work and how to pick the right one for your business.

Key takeaways

- Faster payments: International payment systems move funds in hours or minutes instead of days, keeping your cash flow healthy.

- Lower costs: Modern systems reduce conversion fees and remove unnecessary middlemen from the transaction chain.

- Global buyer experience: Letting customers pay in their own currency and preferred method increases trust and conversion.

- PayGlocal for businesses: PayGlocal offers 40+ payment methods, 33+ currencies, and coverage in 180+ countries, purpose-built for Indian businesses selling globally.

- Choosing the right platform matters: The right system depends on your business type, customer locations, and transaction volume, not just price.

What are international payment systems?

An international payment system moves money between buyers and sellers across countries. It handles currency conversion, routes the payment through the right channels, and settles the funds into your account. The goal is to make cross-border payments work as smoothly as domestic ones.

For instance, an online store in India sells products to a buyer in Germany. The buyer pays in euros through the store's checkout. The international payment system converts the euros, processes the transaction through the right network, and deposits Indian rupees into the seller's account, all within a day or two.

Without that system, the seller would need to rely on a SWIFT transfer that could take three to five business days and cost significantly more in fees.

These systems are used by exporters, freelancers, SaaS companies, travel businesses, and anyone in India who collects money from customers or clients abroad.

Tip: If you collect payments from more than one country, you likely need an international payment system, not just a bank account that accepts foreign wire transfers.

How do international payment systems work?

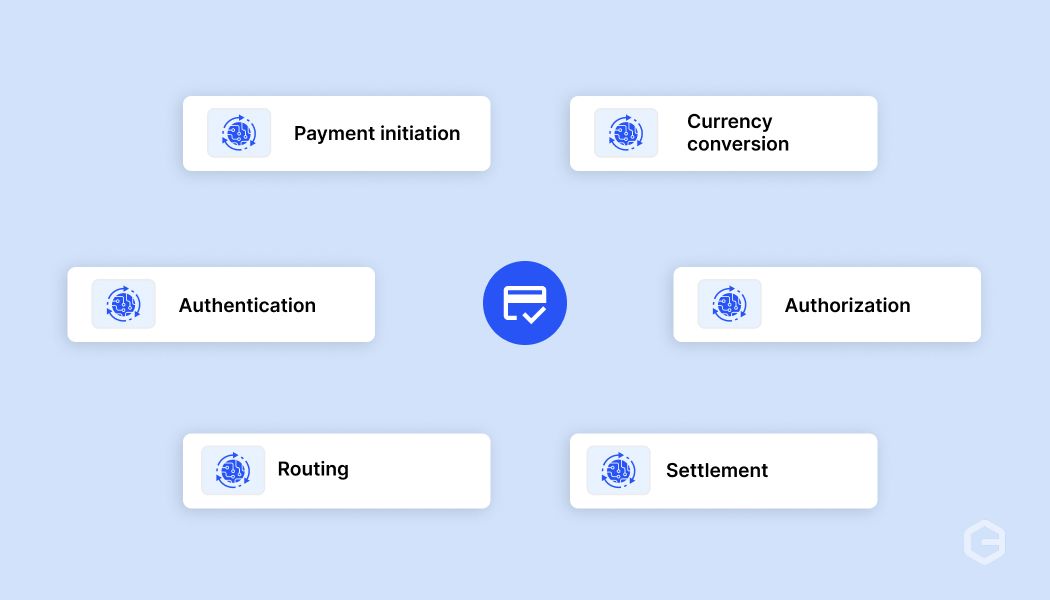

When a payment crosses borders, it passes through several steps before reaching your account. A delayed or failed payment usually means one of these steps didn't go as planned.

Here's what happens in a typical international transaction.

1. Payment initiation: The buyer enters their payment details at checkout, choosing a card, digital wallet, or local bank transfer.

2. Authentication: The system verifies the buyer's identity and checks for fraud signals before the payment moves forward.

3. Routing: The payment is sent through the most efficient network based on the buyer's location, currency, and payment method.

4. Currency conversion: The system converts the buyer's currency into your preferred settlement currency at the current exchange rate.

5. Authorization: The buyer's bank or payment provider approves or declines the transaction based on available funds and risk checks.

6. Settlement: The converted funds are deposited into your bank account, typically within one to three business days.

Each step is handled automatically by the payment system. The fewer manual steps involved, the faster and more reliable the process becomes.

Tip: Look for a system that handles routing and conversion in one step. Fewer handoffs between banks and processors usually result in lower fees and fewer failures.

What are the key advantages of international payment systems?

A slow, expensive, or unreliable payment setup costs you more than fees. It costs you customers, time, and the ability to grow into new markets. Here are the key benefits of international payment systems that matter most for businesses in India selling globally:

1. Faster access to your money

Traditional bank-to-bank transfers across borders often take three to five business days. Modern international payment systems reduce that to same-day or next-day settlement in many cases.

For an exporter waiting on a large payment to release a new shipment, that difference is significant. Faster access to funds keeps your business moving without relying on credit to cover the wait.

2. Lower fees on every transaction

Cross-border payments through traditional banks often involve intermediary fees, markup on currency conversion, and receiving charges.

International payment systems reduce these by routing payments directly and offering competitive exchange rates. Over hundreds of transactions a month, even a small reduction per transaction adds up to a meaningful amount. Your hidden costs drop, and your margins improve.

3. Support for local payment methods your buyers prefer

Credit cards aren't the default payment method everywhere. In the Netherlands, for instance, buyers prefer iDEAL. In Germany, many use SOFORT.

A good international payment system lets you offer local payment methods that match what your buyers already trust. This directly improves your checkout completion rate because buyers don't abandon a purchase when they see a familiar option.

4. Multi-currency support without manual conversion

Showing prices in a buyer's local currency builds trust and reduces confusion at checkout. International payment systems handle this automatically. They accept payments in the buyer's currency and settle in yours, typically INR for Indian businesses.

You don't need to manage separate accounts for each currency or calculate conversion rates yourself. The system does it, and your multi-currency accounts keep everything organized.

5. Higher payment approval rates

A failed transaction doesn't just mean a retry. It often means a lost customer. International payment systems improve approval rates by sending the right data to issuing banks, using local acquiring networks, and applying smart routing.

When the buyer's bank sees a familiar transaction format, it's more likely to approve the payment. For businesses with high transaction volumes, even a five-percent improvement in approvals has a direct impact on revenue.

6. Built-in fraud protection

Cross-border transactions carry a higher fraud risk than domestic ones. International payment systems include fraud screening that checks device data, location, transaction history, and card behavior before approving a payment.

This protects you from chargebacks and fraudulent orders without blocking genuine buyers. The screening happens in real time, so it doesn't slow down the checkout experience.

7. Easier compliance and documentation

Selling internationally comes with documentation requirements, including certificates and tax records for every inward remittance. Modern payment systems generate these automatically.

For Indian businesses, getting a foreign inward remittance certificate (FIRC) after every settlement saves hours of manual follow-up with banks. Everything is tracked, recorded, and available from a dashboard.

8. Ability to scale into new markets

Adding a new country to your sales map shouldn't require a new banking relationship or payment integration. International payment systems are built to cover many countries and currencies from a single setup.

When you're ready to sell in Australia, the Middle East, or Southeast Asia, your payment infrastructure is already there. Scaling becomes a business decision, not a technical one.

The benefits of international payment systems go beyond any single feature. Together, they create a payment experience that works for your buyers and keeps your business running efficiently.

Note: The biggest advantage isn't any one benefit. It's having all of them work together in a single system, so you don't need to patch five tools into one workflow.

What businesses benefit most from international payment systems?

You might assume these systems are only for large companies. In reality, any business in India that collects money from abroad can benefit. The value depends on your business model and where your buyers are. Here are the business types that gain the most advantage from international payment systems:

- Goods exporters: If you ship products to buyers in other countries, you need fast settlement and automatic export documentation like FIRCs. Delays in payment slow down your next shipment and tie up working capital.

- Service exporters and SaaS companies: IT firms, consulting businesses, and SaaS platforms bill international clients regularly. An international payment system lets you send invoices and collect in the client's currency without manual conversion or bank follow-ups.

- Freelancers: Independent professionals working with global clients often lose money on conversion fees and wait days for bank transfers. A dedicated payment system reduces both the cost and the wait.

- Travel and hospitality: Hotels, tour operators, and travel agencies collect payments from travelers worldwide. These buyers expect to pay in their own currency using a familiar method. If the checkout doesn't support that, the booking goes to someone who does.

- E-commerce and D2C brands: Online stores selling to international buyers need high approval rates, local payment methods, and a checkout that works across countries. Every failed transaction at checkout is a lost sale.

Tip: If international payments make up more than 20% of your monthly revenue, a dedicated system will likely pay for itself through lower fees and higher approval rates alone.

How are international payment systems different from domestic ones?

If your domestic payments work fine, you might wonder why international payments need a separate system at all. The difference comes down to what happens behind the scenes when money crosses a border. Here's a side-by-side comparison:

A domestic payment setup can't handle international sales well. Currency conversion alone adds a layer of cost and complexity that domestic transactions don't have.

For Indian businesses selling globally, the key point to note is that international payments require purpose-built infrastructure. Trying to force domestic tools into a global workflow leads to higher fees, slower settlement, and more failed transactions.

Tip: If you're currently accepting international payments through a domestic gateway, compare your approval rates and fees against a dedicated cross-border payment platform. The difference is often significant.

How do you choose the right international payment system?

Picking a payment system based only on price is a common mistake. The cheapest option often has hidden limitations that cost more in the long run. Here's what to evaluate before you commit:

- Country and currency coverage: Confirm the system supports the specific countries and currencies where your buyers are located. A system that covers 180+ countries gives you room to expand later.

- Payment methods supported: Check whether the system offers local payment methods for your key markets, not just cards. Your checkout needs to match your buyers' preferences.

- Settlement speed and currency: Find out how quickly funds reach your bank account and in which currency. For Indian businesses, settlement in INR with a clear forex rate matters.

- Approval rate track record: Ask about the system's payment success rate (PSR). A difference of five to ten percent in approvals can significantly affect your monthly revenue.

- Fraud screening: Look for built-in fraud detection that screens transactions in real time. You need protection that doesn't block genuine buyers.

- Compliance documentation: For Indian exporters, automatic FIRC generation after settlement is a must-have. This saves time and keeps your records clean.

- Pricing transparency: Look for clear pricing with no setup fees, no monthly charges, and no hidden markups on currency conversion. Pay-per-transaction models work best for growing businesses.

Don't finalize based on a features list alone. Ask for a demo or test environment and run a few transactions to see the actual experience.

What mistakes do businesses make with international payment systems?

Even after choosing a good system, businesses often make errors that reduce its value. These mistakes are avoidable once you know what to watch for.

- Using one payment method for all markets: Offering only credit cards in a market where buyers prefer bank transfers or digital wallets leads to abandoned checkouts.

- Ignoring currency display at checkout: Showing prices only in INR or USD when your buyer is in Europe or Southeast Asia creates hesitation. Buyers want to see their local currency before they pay.

- Not tracking approval rates: If you don't measure how many transactions succeed on the first attempt, you won't know how much revenue you're losing to declines.

- Overlooking fraud settings: Some businesses set fraud filters too aggressively, blocking legitimate buyers. Others leave them too loose and deal with chargebacks later. Both cost money.

- Skipping reconciliation: Without regular reconciliation between your payment system dashboard and your bank statements, discrepancies pile up. A proper reconciliation process catches issues early.

- Delaying compliance documentation: Waiting weeks to collect FIRCs or remittance certificates from your bank creates audit headaches. A system that generates these automatically removes the delay entirely.

Most of these mistakes come from a set-it-and-forget-it approach. Your payment system needs regular attention, just like any other part of your business.

Tip: Review your payment success rates and decline reasons at least once a month. Small adjustments to fraud filters or payment method offerings can recover lost revenue.

How do you get started with an international payment system?

Knowing the advantages is good. But putting the right system in place is what actually brings results. Here's a simple process to get started:

1. Identify your buyer locations: List the top five to ten countries where your customers or clients are based. This determines the currencies and payment methods you need.

2. Audit your current setup: Look at your existing payment flow. Note the fees, settlement time, approval rates, and any recurring issues like failed transactions or delayed FIRCs.

3. Shortlist providers: Based on the criteria in the "how to choose" section above, narrow your options to two or three platforms that fit your business type and scale.

4. Run a test: Most providers offer a test setup where you can simulate transactions. Use it to check the checkout experience, response time, and reporting dashboard.

5. Go live with a small volume: Start with a portion of your traffic to compare performance against your current setup. Track approval rates, fees, and settlement time.

6. Scale gradually: Once you're confident in the results, move your full transaction volume to the new system. Add local payment methods for your highest-traffic markets first.

Getting started doesn't require a full migration on day one. A phased approach lets you compare results and make informed adjustments.

Accept international payments easily in multiple currencies with PayGlocal

International payments shouldn't be the reason you lose a sale. Yet for many businesses selling globally, failed transactions, high fees, and limited payment options have become common. It doesn’t have to be that way when you pick the right payment platform.

PayGlocal is built for Indian businesses that collect payments from global customers. Here's what you get:

- Card payments: Your international card transactions get approved more often because of improved messaging to global issuing banks, putting more completed sales in your account.

- Global payment methods: Buyers in 180+ countries can pay using 40+ local options they already trust, which means fewer people leave your checkout without paying.

- Multi-currency accounts: Collect payments in 33+ currencies and get your FIRC delivered straight to your inbox after settlement, removing the wait and paperwork.

- Recurring payments: Set up automatic billing for subscriptions or repeat services on international cards, creating predictable revenue without manual follow-ups.

- One platform: Manage all your international payments, reports, and settlements from a single dashboard, saving your finance team hours every week.

PayGlocal gives Indian businesses a complete payment setup that covers cards, local methods, compliance, and fraud protection in one place. You pay only when you transact, with no setup fees or monthly charges.

Final thoughts

The advantages of international payment systems directly affect how fast you get paid, how much you keep, and how many global buyers complete their purchase. For Indian businesses selling across borders, the right system is a core part of your growth.

Start by reviewing your current payment setup. Look at your fees, settlement times, and approval rates. If any of those numbers are costing you revenue, it's time to make a change.

Every week you wait to fix a broken payment flow, you're leaving money with customers who wanted to pay you. Get started with PayGlocal today.

FAQs

1. Can freelancers in India use international payment systems?

Yes, freelancers can use these systems to collect payments from global clients. They work well for project-based billing, retainer payments, and marketplace payouts from freelancing platforms.

2. Do international payment systems support recurring billing?

Yes, many platforms support recurring billing on international cards. This is useful for subscription businesses, SaaS companies, and service providers who bill clients on a monthly or annual cycle.

3. What's the difference between a payment gateway and a payment system?

A payment gateway is the technology that captures and transmits payment data at checkout. An international payment system is broader and includes routing, currency conversion, fraud screening, and settlement.

4. Are international payment systems safe to use?

Yes, reputable systems use encryption, tokenization, and real-time fraud screening to protect both merchants and buyers. Look for providers that hold recognized security certifications.

5. Do these systems work with e-commerce platforms like Shopify?

Yes, most international payment systems offer plug-ins or built-in integrations for popular platforms like Shopify, WooCommerce, and Magento. Setup typically takes a few hours to a few days, depending on the system.