If you're visiting India without a local bank account, you might be wondering how to pay for things when almost everyone uses UPI. Data shows that UPI now consists of 85% of all digital transactions in India and nearly 50% of all global real-time digital payments are UPI-based. In fact, nearly 460 million people and 65 million merchants use UPI across the country.

But the good news is that you don't need an Indian bank account or phone number anymore. International UPI apps now let foreign visitors and NRIs make digital payments across India using their international mobile numbers.

In this guide, we walk you through what international UPI apps are, which ones work best, and what you need to get started. By the end, you'll know exactly which app fits your needs and how to start paying like a local. Let’s get started.

An international UPI app is a payment application that allows you to use UPI (Unified Payments Interface) in India even if you don't have an Indian bank account or local mobile number. These apps are designed specifically for NRIs, foreign tourists, and international students visiting or living in India.

Regular UPI apps like Google Pay, PhonePe, and Paytm require an Indian bank account and Indian mobile number. International UPI apps remove this barrier. They work through a wallet system where you load money in Indian Rupees and then scan QR codes to pay at millions of merchants across India.

The National Payments Corporation of India (NPCI) created the UPI One World framework to enable this.

Apps under this framework let you sign up with an international mobile number, complete identity verification, load funds, and start making payments just like Indian users do. For instance, if you're a tourist from the UK visiting India for two weeks, you can download Cheq or Mony, add money from your

British debit card, and pay for everything from street food to hotel bills using UPI.

International UPI apps connect your international identity to India's UPI payment network through a wallet-based system. The process involves registering with your foreign mobile number, verifying your identity, loading funds in INR, and then making payments just like Indian users do.

Here's how each step works from signup to your first payment:

Download and register: You download a UPI One World partner app like Cheq, Mony, or NamasPay from your app store and sign up using your international mobile number instead of an Indian one.

Complete KYC verification: The app requires you to verify your identity using your passport and visa, either through video KYC from anywhere or by visiting a partner location in India with your physical documents.

Load your wallet: You add Indian Rupees to your digital wallet using your international credit card, debit card, or forex card, and the app converts your currency to INR and credits your balance within minutes.

Scan and pay: When making a purchase, you open the app, select scan and pay, point your camera at the merchant's UPI QR code, enter the payment amount, and authenticate with your UPI PIN.

Get instant confirmation: The merchant receives payment immediately, you see the transaction confirmed on your screen, and your wallet balance updates automatically with a detailed transaction record.

For example, if you're an NRI visiting family in Delhi and want to pay for groceries, you scan the store's QR code, authenticate the payment, and the payment goes through in seconds. The shopkeeper gets a confirmation, and your wallet balance updates.

You get three main ways to access UPI payments in India as a foreigner or NRI. Each option serves different situations depending on whether you have an Indian bank account, how long you're staying, and what level of setup you're willing to do.

Here's a quick comparison of the different types of international UPI payments:

Here's what you need to know about each type.

UPI One World apps like Cheq, Mony, NamasPay, and IDFC First are wallet-based payment apps designed for foreign nationals and NRIs without Indian bank accounts. You sign up with your international number, load money into a digital wallet in INR, and use that balance to pay merchants.

These apps work best for tourists, business travelers, and students visiting India for short to medium periods. For instance, if you're a German tourist spending three weeks traveling across Rajasthan, you can load Rs 50,000 into your Cheq wallet and use it to pay for hotels, restaurants, transport, and shopping throughout your trip.

The main advantage is that you don't need any Indian banking relationship. The downside is that you must load money in advance, and some apps charge fees for wallet loading or currency conversion.

If you're an NRI with an existing Indian bank account (like an NRE or NRO account), you can link your international mobile number directly to UPI apps like BHIM, iMobile Pay from ICICI, or AU Small Finance Bank. This lets you make UPI payments that debit directly from your Indian bank account.

This option works best for NRIs who maintain financial ties with India, visit frequently, or need to make regular payments in India. For example, if you're an NRI in the US with an ICICI NRE account, you can link your US mobile number to iMobile Pay and transfer rent to your property manager in Mumbai via UPI without needing to carry cash or wait for international transfers.

The key benefit is that you're using your own bank funds directly, not a prepaid wallet. You also avoid wallet loading fees. The requirement is that you must already have an Indian bank account and go through your bank's process to register your international number.

Google Pay offers UPI International in select countries, allowing users to make UPI payments while traveling. However, this feature typically still requires linking to an Indian bank account and may not be available in all countries.

This works for users who already use Google Pay in India and want to continue using the same app when traveling. Availability and functionality vary by country and merchant, so it's less reliable than dedicated UPI One World apps for first-time visitors.

International UPI apps solves many challenges for visitors and NRIs in India. Here's what makes them valuable.

No need for cash: You don't have to carry large amounts of cash or worry about finding ATMs. Digital payments work at street vendors, restaurants, shops, and even for online purchases.

Wide acceptance: UPI is accepted at most merchants across India. From auto rickshaws to luxury hotels, you can pay digitally almost anywhere.

Lower fees than forex cards: Compared to forex card transaction fees or dynamic currency conversion charges on international cards, UPI One World apps often offer more transparent and lower fees.

Instant transactions: Payments happen in real time. No waiting for authorization or settlement. The merchant gets paid immediately, and you get instant confirmation.

Track your spending: Apps provide detailed transaction history. You can see exactly where your money goes, making it easier to manage your budget during your stay.

Safer than cash: If you lose your phone, your wallet is protected by PIN and biometric authentication. Losing cash means it's gone forever.

Several apps now support international UPI payments, each with different features, setup processes, and fee structures. Choosing the right app depends on whether you're a tourist, NRI, or someone with an existing Indian bank account.

Here are the main international UPI apps and what makes each one different:

Cheq UPI: Focuses specifically on NRIs and foreign nationals with video KYC for remote verification, supports multiple international cards for wallet loading, and provides detailed transaction tracking for tourists and short-term visitors who want quick setup.

Mony: Offers similar wallet-based features to Cheq with international mobile number registration, emphasizes user-friendly interfaces and fast KYC processing, and works well for users who prioritize ease of use.

NamasPay: Suitable for foreign tourists and NRIs with emphasis on security and compliance, includes detailed KYC processes and transaction monitoring, and suits users who prioritize security and want clear documentation of all transactions.

IDFC First Bank: Provides UPI One World services through its banking app with the backing of an established bank, offers better customer support for complex issues, and works best for users who prefer working with a traditional bank rather than a fintech startup.

BHIM (for NRIs with Indian accounts): The government-backed UPI app that lets NRIs link their international numbers if they already have an Indian bank account, ideal for NRIs who already have Indian banking relationships.

iMobile Pay (ICICI Bank): Allows NRIs to link international numbers to their NRE or NRO accounts with strong support for NRI customers and additional banking services alongside UPI payments.

Getting set up with an international UPI app requires specific documents and meeting certain conditions. Having everything ready before you start makes the process much faster and helps you avoid delays when you want to make your first payment.

Here's exactly what you need to prepare:

Valid passport: Your passport serves as your primary identity document and must have at least six months of validity remaining with all details clearly visible when you photograph or scan it.

Valid visa for India: You need a tourist visa, business visa, student visa, or employment visa that shows you're legally in India or planning to visit, which apps verify during KYC.

International mobile number: Your foreign mobile number must be active and capable of receiving SMS or calls in India for verification codes throughout setup and transaction authentication.

International payment card: You need a credit card, debit card, or forex card that supports international transactions and has sufficient balance or limit to load your wallet with INR.

Proof of address: Some apps require proof of address in your home country such as a utility bill, bank statement, or government-issued address proof, so check your chosen app's specific requirements.

Smartphone with internet: You need a phone with data connectivity through hotel WiFi, an international roaming plan, or a local Indian SIM card to use the app.

Indian bank account details (for NRIs): If you're linking an existing Indian bank account, you need your account details, registered mobile number, and your bank's permission to register your international number for UPI.

Knowing how international UPI apps stack up against other payment options helps you make the right choice for handling money in India. Each method has different costs, acceptance levels, and convenience factors that matter when you're traveling or living in the country.

Here's how international UPI apps compare to your other payment options:

International credit cards: Work at many merchants but not everywhere, especially small vendors and street shops that only accept UPI, and charge foreign transaction fees plus dynamic currency conversion charges on every purchase.

Forex cards: Let you load foreign currency in advance with better exchange rates than on-the-spot conversions, but still charge transaction fees, don't work at all merchants, and can't scan UPI QR codes which are now the dominant payment method.

ATM cash withdrawals: Work anywhere cash is accepted but come with high fees per withdrawal plus percentage fees from your home bank, have daily withdrawal limits, and require you to carry cash which increases theft risk.

Carrying cash: Works everywhere but is risky and inconvenient for large amounts, requires finding exchange services that offer worse rates than digital methods, and provides no transaction tracking or proof of payment.

International UPI apps: Offer the widest acceptance, charge lower overall fees than cards or forex options, provide instant payments with full tracking, and work just like local payment apps. The only main tradeoff being upfront setup time and the need to load your wallet in advance.

International UPI apps solve payment problems for individuals visiting India. But if you're a business collecting payments from international customers, you face different challenges like managing multiple currencies, ensuring compliance, and tracking cross-border transactions.

PayGlocal gives you an all-in-one platform to collect payments from global customers while staying compliant and reducing costs.

Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries and collect locally in USD, GBP, EUR, and CAD.

Global payment methods: Offer your international customers their preferred local payment options with 40+ payment methods supported.

One platform: Set up, view, manage, and settle all your payments from a single dashboard with complete transparency and control.

Card payments: Process international credit and debit card payments with industry-leading approval rates and seamless checkout experiences.

Zero fixed costs: Pay only when you transact with no setup fees, no platform fees, and no documentation charges.

Whether you're an exporter, SaaS company, or travel business, PayGlocal helps you collect payments faster and grow globally.

International UPI apps remove the biggest barrier foreign visitors and NRIs face when making digital payments in India. You can now pay like a local without needing an Indian bank account or mobile number.

The setup process takes a few days, but once you're approved and loaded, you get access to India's massive digital payment network. You can pay at millions of merchants, track every transaction, and avoid the hassles and fees of cash or international cards.

Choose the app that matches your needs. Tourists and short-term visitors do well with UPI One World wallet apps like Cheq or Mony. NRIs with existing Indian bank accounts should link their international numbers through their banks for direct account access.

If you're building a business that accepts international payments or serves global customers, you need more than consumer payment apps. You need a full payment infrastructure that handles multiple currencies, ensures compliance, and gives you complete control. PayGlocal makes that possible. Ready to accept payments from customers worldwide? Get started with PayGlocal today.

But the good news is that you don't need an Indian bank account or phone number anymore. International UPI apps now let foreign visitors and NRIs make digital payments across India using their international mobile numbers.

In this guide, we walk you through what international UPI apps are, which ones work best, and what you need to get started. By the end, you'll know exactly which app fits your needs and how to start paying like a local. Let’s get started.

Key takeaways

- No Indian bank account needed: International UPI apps let you make digital payments in India using your foreign mobile number and without an Indian bank account.

- UPI One World wallet apps: Apps like Cheq, Mony, and NamasPay allow tourists and NRIs to load wallets with INR and pay at UPI-accepting merchants across India.

- KYC verification required: Setting up requires completing KYC verification with your passport and visa, either physically or remotely, depending on the app you choose.

- Direct bank linking for NRIs: NRIs with Indian bank accounts can link their international numbers to apps like BHIM or iMobile Pay for direct bank-linked UPI payments.

- Business payment solutions available: Businesses accepting international payments can use solutions like PayGlocal to collect from global customers seamlessly while managing compliance and tracking.

What is an international UPI app?

An international UPI app is a payment application that allows you to use UPI (Unified Payments Interface) in India even if you don't have an Indian bank account or local mobile number. These apps are designed specifically for NRIs, foreign tourists, and international students visiting or living in India.

Regular UPI apps like Google Pay, PhonePe, and Paytm require an Indian bank account and Indian mobile number. International UPI apps remove this barrier. They work through a wallet system where you load money in Indian Rupees and then scan QR codes to pay at millions of merchants across India.

The National Payments Corporation of India (NPCI) created the UPI One World framework to enable this.

Apps under this framework let you sign up with an international mobile number, complete identity verification, load funds, and start making payments just like Indian users do. For instance, if you're a tourist from the UK visiting India for two weeks, you can download Cheq or Mony, add money from your

British debit card, and pay for everything from street food to hotel bills using UPI.

How does an international UPI app work?

International UPI apps connect your international identity to India's UPI payment network through a wallet-based system. The process involves registering with your foreign mobile number, verifying your identity, loading funds in INR, and then making payments just like Indian users do.

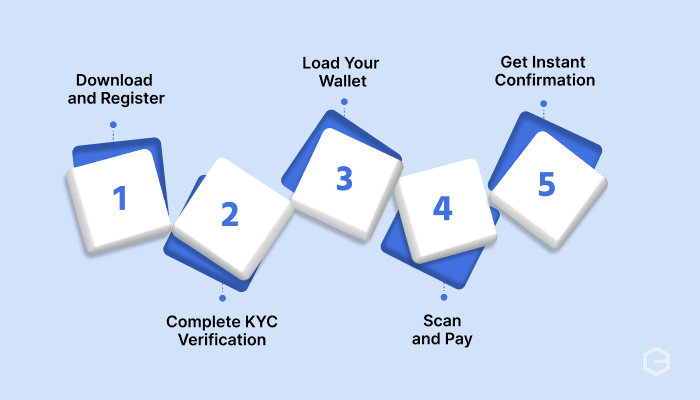

Here's how each step works from signup to your first payment:

Download and register: You download a UPI One World partner app like Cheq, Mony, or NamasPay from your app store and sign up using your international mobile number instead of an Indian one.

Complete KYC verification: The app requires you to verify your identity using your passport and visa, either through video KYC from anywhere or by visiting a partner location in India with your physical documents.

Load your wallet: You add Indian Rupees to your digital wallet using your international credit card, debit card, or forex card, and the app converts your currency to INR and credits your balance within minutes.

Scan and pay: When making a purchase, you open the app, select scan and pay, point your camera at the merchant's UPI QR code, enter the payment amount, and authenticate with your UPI PIN.

Get instant confirmation: The merchant receives payment immediately, you see the transaction confirmed on your screen, and your wallet balance updates automatically with a detailed transaction record.

For example, if you're an NRI visiting family in Delhi and want to pay for groceries, you scan the store's QR code, authenticate the payment, and the payment goes through in seconds. The shopkeeper gets a confirmation, and your wallet balance updates.

What are the types of international UPI solutions?

You get three main ways to access UPI payments in India as a foreigner or NRI. Each option serves different situations depending on whether you have an Indian bank account, how long you're staying, and what level of setup you're willing to do.

Here's a quick comparison of the different types of international UPI payments:

Here's what you need to know about each type.

UPI One World wallet apps

UPI One World apps like Cheq, Mony, NamasPay, and IDFC First are wallet-based payment apps designed for foreign nationals and NRIs without Indian bank accounts. You sign up with your international number, load money into a digital wallet in INR, and use that balance to pay merchants.

These apps work best for tourists, business travelers, and students visiting India for short to medium periods. For instance, if you're a German tourist spending three weeks traveling across Rajasthan, you can load Rs 50,000 into your Cheq wallet and use it to pay for hotels, restaurants, transport, and shopping throughout your trip.

The main advantage is that you don't need any Indian banking relationship. The downside is that you must load money in advance, and some apps charge fees for wallet loading or currency conversion.

Bank-linked UPI for NRIs

If you're an NRI with an existing Indian bank account (like an NRE or NRO account), you can link your international mobile number directly to UPI apps like BHIM, iMobile Pay from ICICI, or AU Small Finance Bank. This lets you make UPI payments that debit directly from your Indian bank account.

This option works best for NRIs who maintain financial ties with India, visit frequently, or need to make regular payments in India. For example, if you're an NRI in the US with an ICICI NRE account, you can link your US mobile number to iMobile Pay and transfer rent to your property manager in Mumbai via UPI without needing to carry cash or wait for international transfers.

The key benefit is that you're using your own bank funds directly, not a prepaid wallet. You also avoid wallet loading fees. The requirement is that you must already have an Indian bank account and go through your bank's process to register your international number.

International UPI on Google Pay

Google Pay offers UPI International in select countries, allowing users to make UPI payments while traveling. However, this feature typically still requires linking to an Indian bank account and may not be available in all countries.

This works for users who already use Google Pay in India and want to continue using the same app when traveling. Availability and functionality vary by country and merchant, so it's less reliable than dedicated UPI One World apps for first-time visitors.

What are the benefits of using an international UPI app?

International UPI apps solves many challenges for visitors and NRIs in India. Here's what makes them valuable.

No need for cash: You don't have to carry large amounts of cash or worry about finding ATMs. Digital payments work at street vendors, restaurants, shops, and even for online purchases.

Wide acceptance: UPI is accepted at most merchants across India. From auto rickshaws to luxury hotels, you can pay digitally almost anywhere.

Lower fees than forex cards: Compared to forex card transaction fees or dynamic currency conversion charges on international cards, UPI One World apps often offer more transparent and lower fees.

Instant transactions: Payments happen in real time. No waiting for authorization or settlement. The merchant gets paid immediately, and you get instant confirmation.

Track your spending: Apps provide detailed transaction history. You can see exactly where your money goes, making it easier to manage your budget during your stay.

Safer than cash: If you lose your phone, your wallet is protected by PIN and biometric authentication. Losing cash means it's gone forever.

Which international UPI apps are available?

Several apps now support international UPI payments, each with different features, setup processes, and fee structures. Choosing the right app depends on whether you're a tourist, NRI, or someone with an existing Indian bank account.

Here are the main international UPI apps and what makes each one different:

Cheq UPI: Focuses specifically on NRIs and foreign nationals with video KYC for remote verification, supports multiple international cards for wallet loading, and provides detailed transaction tracking for tourists and short-term visitors who want quick setup.

Mony: Offers similar wallet-based features to Cheq with international mobile number registration, emphasizes user-friendly interfaces and fast KYC processing, and works well for users who prioritize ease of use.

NamasPay: Suitable for foreign tourists and NRIs with emphasis on security and compliance, includes detailed KYC processes and transaction monitoring, and suits users who prioritize security and want clear documentation of all transactions.

IDFC First Bank: Provides UPI One World services through its banking app with the backing of an established bank, offers better customer support for complex issues, and works best for users who prefer working with a traditional bank rather than a fintech startup.

BHIM (for NRIs with Indian accounts): The government-backed UPI app that lets NRIs link their international numbers if they already have an Indian bank account, ideal for NRIs who already have Indian banking relationships.

iMobile Pay (ICICI Bank): Allows NRIs to link international numbers to their NRE or NRO accounts with strong support for NRI customers and additional banking services alongside UPI payments.

What documents and requirements do you need?

Getting set up with an international UPI app requires specific documents and meeting certain conditions. Having everything ready before you start makes the process much faster and helps you avoid delays when you want to make your first payment.

Here's exactly what you need to prepare:

Valid passport: Your passport serves as your primary identity document and must have at least six months of validity remaining with all details clearly visible when you photograph or scan it.

Valid visa for India: You need a tourist visa, business visa, student visa, or employment visa that shows you're legally in India or planning to visit, which apps verify during KYC.

International mobile number: Your foreign mobile number must be active and capable of receiving SMS or calls in India for verification codes throughout setup and transaction authentication.

International payment card: You need a credit card, debit card, or forex card that supports international transactions and has sufficient balance or limit to load your wallet with INR.

Proof of address: Some apps require proof of address in your home country such as a utility bill, bank statement, or government-issued address proof, so check your chosen app's specific requirements.

Smartphone with internet: You need a phone with data connectivity through hotel WiFi, an international roaming plan, or a local Indian SIM card to use the app.

Indian bank account details (for NRIs): If you're linking an existing Indian bank account, you need your account details, registered mobile number, and your bank's permission to register your international number for UPI.

How do international UPI apps compare to other payment methods?

Knowing how international UPI apps stack up against other payment options helps you make the right choice for handling money in India. Each method has different costs, acceptance levels, and convenience factors that matter when you're traveling or living in the country.

Here's how international UPI apps compare to your other payment options:

International credit cards: Work at many merchants but not everywhere, especially small vendors and street shops that only accept UPI, and charge foreign transaction fees plus dynamic currency conversion charges on every purchase.

Forex cards: Let you load foreign currency in advance with better exchange rates than on-the-spot conversions, but still charge transaction fees, don't work at all merchants, and can't scan UPI QR codes which are now the dominant payment method.

ATM cash withdrawals: Work anywhere cash is accepted but come with high fees per withdrawal plus percentage fees from your home bank, have daily withdrawal limits, and require you to carry cash which increases theft risk.

Carrying cash: Works everywhere but is risky and inconvenient for large amounts, requires finding exchange services that offer worse rates than digital methods, and provides no transaction tracking or proof of payment.

International UPI apps: Offer the widest acceptance, charge lower overall fees than cards or forex options, provide instant payments with full tracking, and work just like local payment apps. The only main tradeoff being upfront setup time and the need to load your wallet in advance.

Manage all global payments easily from one platform

International UPI apps solve payment problems for individuals visiting India. But if you're a business collecting payments from international customers, you face different challenges like managing multiple currencies, ensuring compliance, and tracking cross-border transactions.

PayGlocal gives you an all-in-one platform to collect payments from global customers while staying compliant and reducing costs.

Multi-currency accounts: Accept payments in 33+ currencies from 180+ countries and collect locally in USD, GBP, EUR, and CAD.

Global payment methods: Offer your international customers their preferred local payment options with 40+ payment methods supported.

One platform: Set up, view, manage, and settle all your payments from a single dashboard with complete transparency and control.

Card payments: Process international credit and debit card payments with industry-leading approval rates and seamless checkout experiences.

Zero fixed costs: Pay only when you transact with no setup fees, no platform fees, and no documentation charges.

Whether you're an exporter, SaaS company, or travel business, PayGlocal helps you collect payments faster and grow globally.

Final thoughts

International UPI apps remove the biggest barrier foreign visitors and NRIs face when making digital payments in India. You can now pay like a local without needing an Indian bank account or mobile number.

The setup process takes a few days, but once you're approved and loaded, you get access to India's massive digital payment network. You can pay at millions of merchants, track every transaction, and avoid the hassles and fees of cash or international cards.

Choose the app that matches your needs. Tourists and short-term visitors do well with UPI One World wallet apps like Cheq or Mony. NRIs with existing Indian bank accounts should link their international numbers through their banks for direct account access.

If you're building a business that accepts international payments or serves global customers, you need more than consumer payment apps. You need a full payment infrastructure that handles multiple currencies, ensures compliance, and gives you complete control. PayGlocal makes that possible. Ready to accept payments from customers worldwide? Get started with PayGlocal today.