Introduction

Foreign inward remittance plays a critical role in India’s economy, serving as a lifeline for families, students, and investors alike. Whether you’re receiving funds to support family members, cover educational expenses, or invest in the country, understanding the Inward Remittance RBI guidelines set by the Reserve Bank of India is essential for seamless, compliant transactions.

In this guide, we’ll break down the main methods for receiving foreign inward remittances, the specific rules that apply to each, and how to ensure compliance for Inward Remittance RBI Guidelines.

Overview of Foreign Inward Remittance

What is Foreign Inward Remittance?

Inward remittance refers to money sent from a foreign country to India, usually for personal reasons, such as family support, education, or medical expenses. The inflow of these funds is crucial, not just for individual recipients, but for the country’s foreign exchange reserves.

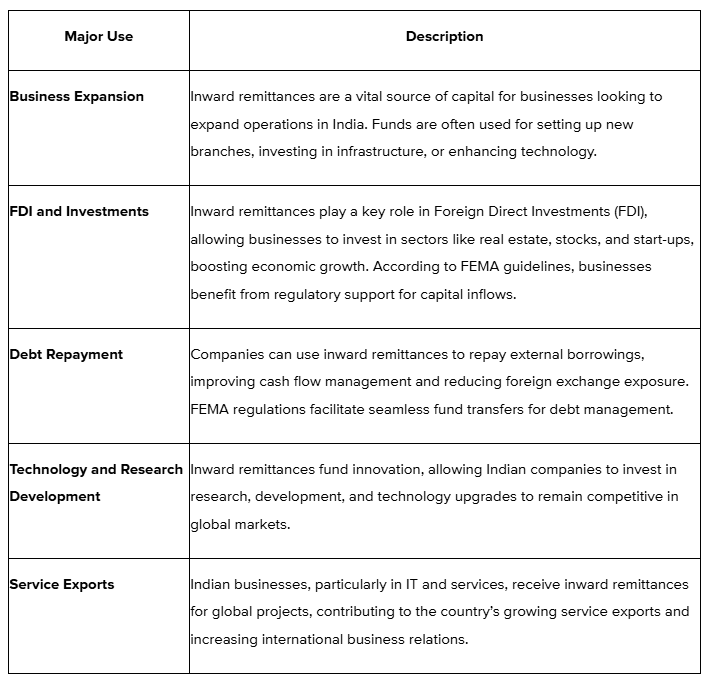

Major Uses of Inward Remittance: A Business Perspective

By leveraging the RBI guidelines, businesses can benefit from the remittances and strengthen their operations, explore new markets, and contribute to India’s economic growth under FEMA guidelines.

Now that we know what Foreign Inward Remittance exactly is, let us look into the various methods for receiving these funds in India:

Methods for Receiving Foreign Inward Remittances

There are several approved methods for receiving funds from abroad, each with its own set of Inward Remittance RBI Guidelines:

1. Rupee Drawing Arrangement (RDA)

The RDA system allows NRIs to send remittances to India via Foreign Exchange Houses approved by the RBI. The funds are received in rupees, making it a convenient option for non-residents who want to support family members or make payments in India without having to manage foreign currency conversions.

2. Money Transfer Service Scheme (MTSS)

MTSS is a system designed for smaller transfers, mainly for personal use. It allows recipients to collect money in cash or have it credited to a bank account, with certain limitations on the amount and frequency of transfers.

3. Foreign Currency Demand Drafts (FCDDs)

Foreign currency demand drafts (FCDDs) are bank drafts issued by a foreign bank, payable in India. Commonly used for purposes like tuition payments or large purchases, FCDDs serve as a foreign currency instrument for transferring funds. They are one of the available methods for foreign inward remittances

Also read: Choosing the Right Payment Gateway: Your guide to a Smooth International Customer Experience.

Having understood the various methods for receiving Foreign Inward Remittances in India, let us now understand more elaborately, what is RDA?

Rupee Drawing Arrangement (RDA)

The Rupee Drawing Arrangement (RDA) is a remittance channel approved by the RBI, allowing overseas non-resident individuals to send money to India through non-resident Exchange Houses.

Types of Permissible Remittances

Under RDA, personal remittances such as family maintenance, savings, and other non-trade transactions are allowed, along with trade-related remittances for businesses.

Limitations and Restrictions

- Personal remittances: No upper limit.

- Trade-related remittances: Capped at Rs. 15 lakh per transaction.

Regulation and Documentation

RDA remittances require proper documentation, including RBI approval and transactions must be routed through designated non-resident Exchange Houses authorized by the RBI.

Now that we learnt what RDA is, let us now delve into what MTSS is:

Money Transfer Service Scheme (MTSS)

The Money Transfer Service Scheme (MTSS) is designed to facilitate small-value, cross-border transfers from abroad to India, primarily for personal use. It allows eligible entities like banks and money transfer agencies to act as intermediaries.

Types of Permissible Remittances

Personal remittances, including family support and personal transfers, fall under MTSS, but trade-related transfers are not allowed.

Limitations and Restrictions

- Each transfer is capped at USD 2,500.

- A maximum of 30 transfers is allowed per beneficiary per year.

Process for Cash and Bank Account Credits

- Cash payments: Up to INR 50,000 can be disbursed as cash.

- Bank credits: Larger amounts are credited directly to the recipient’s bank account.

Also read: Uncovering the Hidden Costs of International Business Transactions.

Now that we have learnt about various Money Transfer Schemes, let us learn various Compliance and Inward Remittance RBI Guidelines:

Compliance and Inward Remittance RBI Guidelines

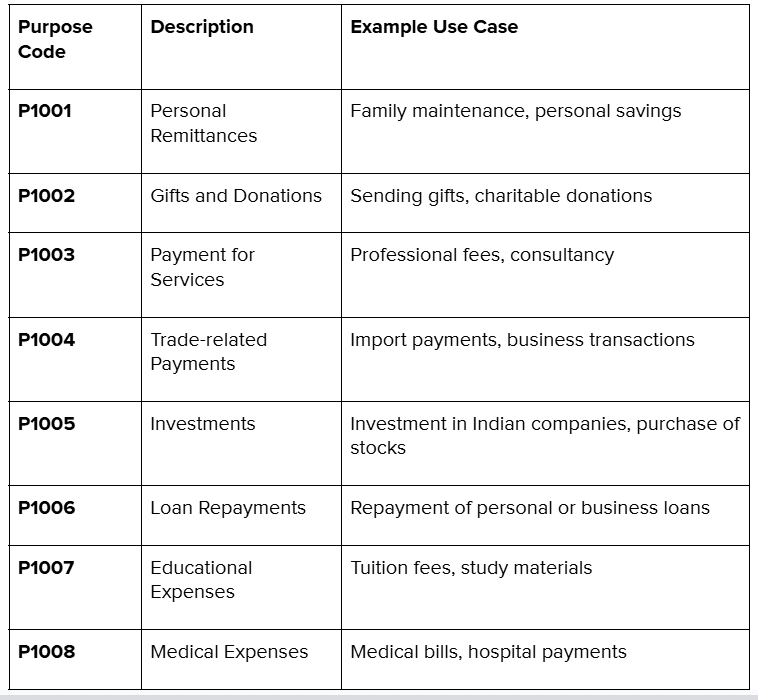

1. Purpose Codes for Transactions

Each remittance must be accompanied by a purpose code that clearly defines the nature of the transaction, ensuring transparency and compliance with RBI norms.

Here are a few examples of purpose codes for inward remittance in a tabular format:

These purpose codes help ensure that inward remittances are categorized correctly, facilitating compliance with RBI regulations and transparency in financial transactions.

2. Disposal Instructions

Clear instructions regarding the disposal or usage of funds must be provided, whether for personal or trade-related purposes.

3. Foreign Inward Remittance Certificate (FIRC)

Recipients of foreign remittances need to obtain an FIRC as proof of funds received from abroad, which is essential for regulatory and tax purposes.

Also read: SOFTEX: A Comprehensive Guide

With a solid understanding of compliance requirements, let's shift our focus to the tax implications of receiving foreign remittances.

Tax Implications of Inward Remittances

1. Non-Taxable Nature of Personal Remittances

Most personal remittances are non-taxable in India. Money sent for family maintenance or personal savings does not attract tax.

2. Specific Taxation Scenarios

Income earned abroad that is transferred to India may be subject to tax. Additionally, large transfers of assets or gifts exceeding a certain threshold may attract gift tax.

Also read: Guide to International Money Transfer for Indian Businesses.

We have covered the Tax Implications according to various Inward Remittances RBI Guidelines, now let us look into the charges that may imply:

Charges for Inward Remittances

1. Variability and Types of Fees

The fees associated with inward remittances can vary depending on the service provider, bank, or method of transfer. Common charges include transaction fees, foreign exchange (FX) conversion charges, and service taxes.

2. Considerations

- Transaction fees: Often based on the amount transferred or the service provider.

- Currency conversion charges: Hidden FX charges can impact the amount received.

- Service tax: Applies to certain remittance services, influencing the overall cost.

By understanding these charges, individuals and businesses can make more informed decisions about selecting the most cost-effective remittance service, ensuring that more of the money reaches its destination.

Conclusion

Understanding inward remittance RBI guidelines is essential for ensuring seamless and compliant cross-border transactions. You can avoid unnecessary delays, penalties, or tax complications by familiarizing yourself with regulations like the RDA and MTSS. Staying informed about these guidelines not only helps you streamline the remittance process but also maximizes the benefits of receiving funds from abroad.

For businesses and individuals, adhering to these guidelines is key to avoiding legal hurdles and ensuring smooth transactions. Whether you're receiving remittances for personal needs or business purposes, following the inward remittance RBI guidelines ensures timely transfers while protecting your financial interests.

Are you compliant with the Inward Remittance RBI Guidelines? Boost your payment success rates with PayGlocal’s advanced fraud protection and risk management systems. Discover our solutions now!