As of January 2025, India boasts over 28 lakh registered private companies, of which approximately 65% are actively operating. Limited Liability Companies (LLCs) are increasingly popular for their combination of liability protection and operational flexibility. This trend reflects the growing number of entrepreneurs who want to protect their assets while scaling their businesses.

In this blog, we'll explore the benefits of LLCs, the legal requirements for establishing them, and other essential considerations every entrepreneur should know when choosing this business structure.

A Limited Liability Company (LLC) is a business structure that protects its owners from personal liabilities and financial losses. Unlike traditional partnerships or sole proprietorships, where individuals can be personally responsible for business debts, the LLC structure ensures that the company holds the liability, not the individual partners or shareholders.

LLCs also offer flexibility in managing and taxing the business, making them a popular choice for many small business owners and entrepreneurs.

Example: Let’s say you start a company called “Sharma Exports” and set it up as an LLC. Unfortunately, the company faces a lawsuit due to a supplier issue, and you owe a large sum of money.

When deciding on an LLC structure, it is essential to know the different types that may suit your business needs.

This business entity is registered under the Companies Act of 2013, where the shares are privately held and cannot be publicly traded. A private limited company requires a minimum of two shareholders for incorporation and can have up to 50 shareholders.

A public limited company is also formed under the Companies Act 2013, but its shares can be publicly traded on stock exchanges or offered through an Initial Public Offering (IPO). It requires at least seven shareholders at the time of incorporation and allows for wider public investment.

Did you know Google is a Limited Liability Company (LLC), operating under the legal name Google LLC? It's a subsidiary of Alphabet Inc., a provider of search and advertising services on the Internet.

Many businesses, including those of professionals such as doctors and lawyers, form LLCs to take advantage of their liability protection and flexibility. Unlike corporations, LLCs protect personal liability without the burdensome paperwork, red tape, or formalities.

An LLP offers limited liability, where the protection can be compromised if members personally guarantee debts or fail to operate the LLP as a distinct entity, exposing their assets.

LLCs offer several benefits, but they also come with some drawbacks. For example, an LLC may be required to dissolve according to state law in case of a member's death or insolvency.

Both partners must have certain documents to register as a Limited Liability Company (LLC) in India. Below is a detailed list of the required documents:

Draft the Articles of Association (AoA): The AoA outlines the internal rules and regulations governing the company's management, including directors' powers, voting rights, and meeting procedures.

After furnishing the necessary documents for opening an LLC, the Registrar of Companies (ROC) reviews the submission and, upon approval, issues the incorporation certificate. Once the certificate is obtained, the formation of the LLC officially begins.

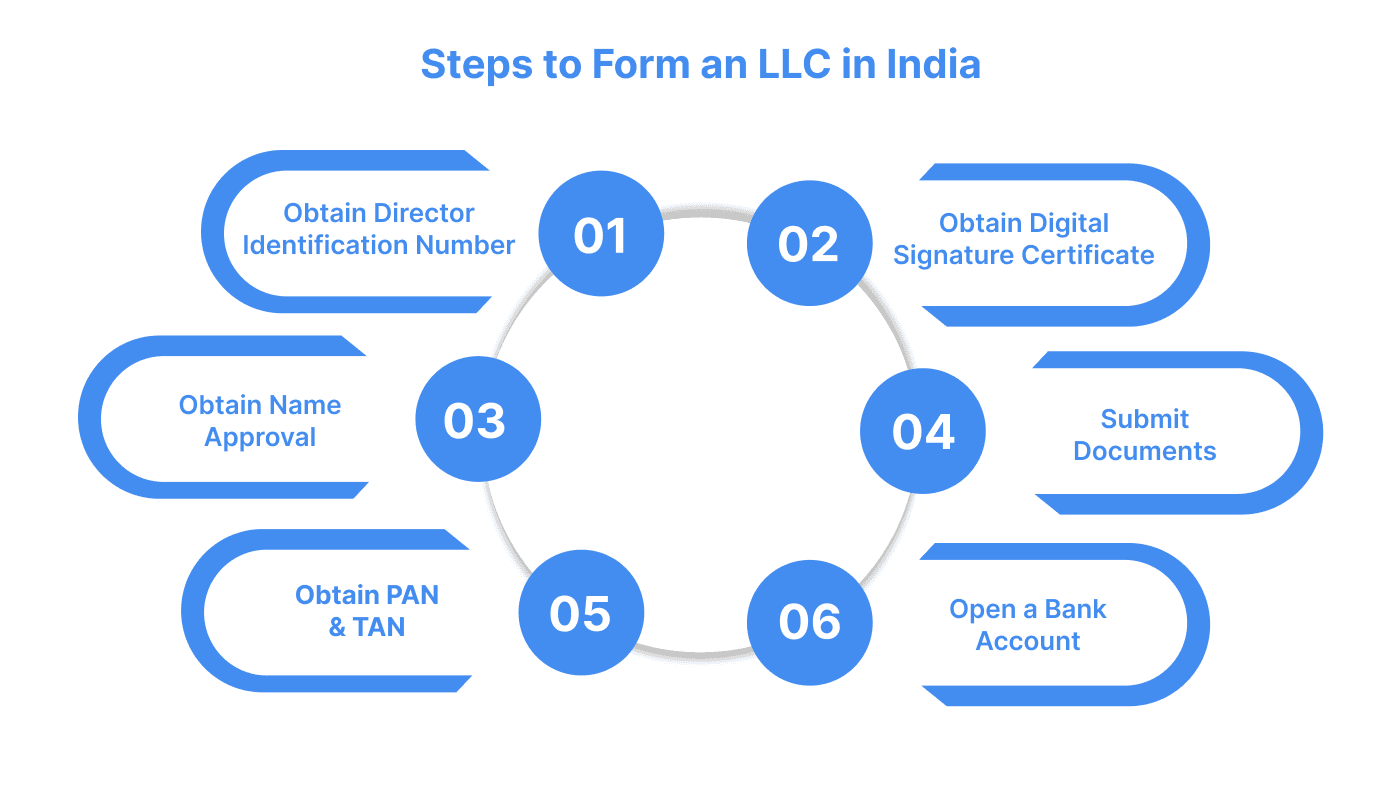

Here are the key steps to follow when forming an LLC in India in 2025.

1. Obtain Director Identification Number (DIN): The company director must acquire a DIN, which can be obtained in person or through a special process if the director is not physically present in India.

2. Obtain a Digital Signature Certificate (DSC): The company director must submit a digital signature for use on the company’s official documents.

3. Obtain Name Approval: The company name must be unique, and an application for name approval is submitted to the Registrar of Companies.

4. Submit Documents: After setting up a bank account and gathering the necessary documents, the incorporation certificate is obtained by submitting them to the Registrar of Companies (ROC).

5. Obtain PAN and TAN: Apply for a Permanent Account Number (PAN) and Tax Deduction Account Number (TAN) from the Income Tax Department for tax-related purposes.

6. Open a Bank Account: Set up a corporate bank account in the name of the LLC to manage business transactions and operations.

Knowing the tax obligations will help ensure compliance and effective financial management as your business begins to operate.

The primary purpose of an LLC as a business structure is to shield the owners' assets from debt collection and lawsuits targeting the company. Also, LLCs offer certain tax benefits, making them popular, particularly for small business owners.

Limited Liability Companies (LLCs) are treated as pass-through entities for tax purposes. This means that the LLC itself does not pay federal income taxes. Instead, after the LLC covers its expenses and debts, the remaining profits or losses are passed directly to the members (owners).

Each member then reports their share of these profits or losses on their personal income tax returns, regardless of whether the income was distributed.

This pass-through ensures that business income is taxed only once at the individual level and is not subject to double taxation at the corporate and individual levels. Owners of pass-through entities may also qualify for a qualified business income (QBI) deduction of up to 20%.

LLCs provide a balanced structure offering liability protection and tax advantages, making them ideal for small to medium-sized businesses. An LLC’s flexible structure and limited liability protection provide a perfect foundation for entrepreneurs, but managing payments, especially with global transactions, can be complex.

That’s where Payglocal comes in. It offers cross-border payment solutions designed to streamline transactions and make managing your LLC’s finances effortless.

Here are some reasons why Payglocal is an excellent choice for LLC partners:

Opting for Payglocal can enable smooth, secure, and efficient payment management. Get Started Today!

In this blog, we'll explore the benefits of LLCs, the legal requirements for establishing them, and other essential considerations every entrepreneur should know when choosing this business structure.

What is a Limited Liability Company (LLC)?

A Limited Liability Company (LLC) is a business structure that protects its owners from personal liabilities and financial losses. Unlike traditional partnerships or sole proprietorships, where individuals can be personally responsible for business debts, the LLC structure ensures that the company holds the liability, not the individual partners or shareholders.

LLCs also offer flexibility in managing and taxing the business, making them a popular choice for many small business owners and entrepreneurs.

Example: Let’s say you start a company called “Sharma Exports” and set it up as an LLC. Unfortunately, the company faces a lawsuit due to a supplier issue, and you owe a large sum of money.

- Without an LLC: If Sharma Exports were a sole proprietorship or partnership, your assets could be at risk, and you could be forced to sell your home or car to pay off the company’s debts.

- With an LLC: Since your company is set up as an LLC, only the business assets, such as inventory and cash, are at risk. Your personal property, home, savings, and car remain protected from lawsuits or business debts.

Types of Limited Liability Company (LLC)

When deciding on an LLC structure, it is essential to know the different types that may suit your business needs.

1. Private Limited Company

This business entity is registered under the Companies Act of 2013, where the shares are privately held and cannot be publicly traded. A private limited company requires a minimum of two shareholders for incorporation and can have up to 50 shareholders.

2. Public Limited Company

A public limited company is also formed under the Companies Act 2013, but its shares can be publicly traded on stock exchanges or offered through an Initial Public Offering (IPO). It requires at least seven shareholders at the time of incorporation and allows for wider public investment.

Did you know Google is a Limited Liability Company (LLC), operating under the legal name Google LLC? It's a subsidiary of Alphabet Inc., a provider of search and advertising services on the Internet.

What are the Benefits of Forming an LLC?

Many businesses, including those of professionals such as doctors and lawyers, form LLCs to take advantage of their liability protection and flexibility. Unlike corporations, LLCs protect personal liability without the burdensome paperwork, red tape, or formalities.

- Separate Legal Identity: An LLC in India is a separate legal entity, distinct from its owners. It can own property, make contracts, and be involved in legal actions in its name, protecting members from personal liability.

- Limited Liability: An LLC's owners (members) are not personally liable for the company's debts. Their risk is limited to their investment in the business, ensuring personal assets are protected.

- Perpetual Existence: An LLC continues to operate even if members change, retire, or pass away, providing business continuity without interruption.

- Flexible Management Structure: LLCs offer flexibility in management, where control can rest with the members or designated managers, providing adaptability for businesses of all sizes.

- Free Transferability of Financial Interests: Membership interests can be transferred freely, subject to the LLC’s operating agreement. This gives flexibility in ownership transfer while protecting against unauthorized management changes.

- Pass-Through Taxation: LLCs benefit from pass-through taxation, meaning the company doesn’t pay taxes. Instead, profits and losses are passed through to the owners’ tax returns, simplifying the tax process.

What are the Limitations of an LLC?

An LLP offers limited liability, where the protection can be compromised if members personally guarantee debts or fail to operate the LLP as a distinct entity, exposing their assets.

- Penalty for Non-Compliance: Although LLPs have minimal compliance requirements, failure to meet deadlines can result in heavy fines. Even if the LLP has no activities in a year, it must file annual returns with the Ministry of Corporate Affairs (MCA), and non-compliance can lead to fines.

- Winding Up and Dissolution: An LLP can be dissolved if the number of partners falls below two for six months or if it is unable to pay its debts. If key conditions are not met, this could potentially lead to closure.

- Difficulty in Raising Capital: Unlike corporations, LLPs don't have equity or shareholders. This limits their ability to raise funds from angel investors or venture capitalists, who prefer investing in companies with shareholding structures. Thus, LLPS find it challenging to secure external capital.

LLCs offer several benefits, but they also come with some drawbacks. For example, an LLC may be required to dissolve according to state law in case of a member's death or insolvency.

Documents Required to Open an LLC in India

Both partners must have certain documents to register as a Limited Liability Company (LLC) in India. Below is a detailed list of the required documents:

- PAN Card/ID Proof: All partners must provide their PAN card as a primary identification document during registration.

- Residence Proof: Partners must submit a document as proof of their residence. This can be one of the following:

- Voter’s ID

- Passport

- Driver’s License

- Utility Bills (not older than 2 months)

- Aadhaar Card

- Photograph: A recent passport-size photograph of the partner (preferably on a white background).

- Passport (For Foreign Nationals/NRIs): Foreign nationals and NRIs seeking to become partners must submit their passports, which must be notarized or apostilled by the relevant authorities in their country.

- Proof of Registered Office Address: Documentation proving the registered office address must be submitted within 30 days of incorporation. A rental agreement and a No-Objection Certificate (NOC) from the landlord are required if the office is on rent.

- Digital Signature Certificate (DSC): One of the designated partners must obtain a digital signature certificate, as all documents and applications will require digital signatures.

- Memorandum of Association (MoA): This document defines the company's name, registered office, objectives, member liabilities, and share capital.

Draft the Articles of Association (AoA): The AoA outlines the internal rules and regulations governing the company's management, including directors' powers, voting rights, and meeting procedures.

After furnishing the necessary documents for opening an LLC, the Registrar of Companies (ROC) reviews the submission and, upon approval, issues the incorporation certificate. Once the certificate is obtained, the formation of the LLC officially begins.

Steps to Form an LLC in India

Here are the key steps to follow when forming an LLC in India in 2025.

1. Obtain Director Identification Number (DIN): The company director must acquire a DIN, which can be obtained in person or through a special process if the director is not physically present in India.

2. Obtain a Digital Signature Certificate (DSC): The company director must submit a digital signature for use on the company’s official documents.

3. Obtain Name Approval: The company name must be unique, and an application for name approval is submitted to the Registrar of Companies.

4. Submit Documents: After setting up a bank account and gathering the necessary documents, the incorporation certificate is obtained by submitting them to the Registrar of Companies (ROC).

5. Obtain PAN and TAN: Apply for a Permanent Account Number (PAN) and Tax Deduction Account Number (TAN) from the Income Tax Department for tax-related purposes.

6. Open a Bank Account: Set up a corporate bank account in the name of the LLC to manage business transactions and operations.

Knowing the tax obligations will help ensure compliance and effective financial management as your business begins to operate.

Taxation of LLCs: How Does it Work?

The primary purpose of an LLC as a business structure is to shield the owners' assets from debt collection and lawsuits targeting the company. Also, LLCs offer certain tax benefits, making them popular, particularly for small business owners.

Limited Liability Companies (LLCs) are treated as pass-through entities for tax purposes. This means that the LLC itself does not pay federal income taxes. Instead, after the LLC covers its expenses and debts, the remaining profits or losses are passed directly to the members (owners).

Each member then reports their share of these profits or losses on their personal income tax returns, regardless of whether the income was distributed.

This pass-through ensures that business income is taxed only once at the individual level and is not subject to double taxation at the corporate and individual levels. Owners of pass-through entities may also qualify for a qualified business income (QBI) deduction of up to 20%.

Conclusion

LLCs provide a balanced structure offering liability protection and tax advantages, making them ideal for small to medium-sized businesses. An LLC’s flexible structure and limited liability protection provide a perfect foundation for entrepreneurs, but managing payments, especially with global transactions, can be complex.

That’s where Payglocal comes in. It offers cross-border payment solutions designed to streamline transactions and make managing your LLC’s finances effortless.

Here are some reasons why Payglocal is an excellent choice for LLC partners:

- Multi-Currency Support: With Payglocal, LLCs can accept payments in multiple currencies, providing a seamless experience for international customers.

- Easy Integration: Payglocal integrates smoothly with e-commerce platforms and business systems, simplifying the setup for LLCs.

- Real-Time Analytics: Payglocal offers insightful, real-time financial reports to help LLCs monitor their cash flow, track invoices, and optimize business operations.

- Secure Transactions: Payglocal ensures top-tier security for all transactions, giving LLCs and their customers peace of mind with end-to-end encryption.

Opting for Payglocal can enable smooth, secure, and efficient payment management. Get Started Today!