India's economy is growing at record speed. Data shows India's actual GDP expanded by 6.5% in 2024-25, with this growth pace expected to continue through 2025-26. This economic growth indicates more businesses are scaling operations and accepting digital payments from customers worldwide.

Every time a customer pays with a card or digital payment method, your business pays a fee. But these fees, called MDR charges, can quickly add up and impact your profit margins.

In this guide, we’re going to do a detailed breakdown of MDR charges, from basic calculations to their different types. By the end, you’ll have a complete idea of how they work and impact your business. Let’s get into it.

MDR charges, or Merchant Discount Rate charges, are fees that businesses pay to accept digital payments like credit cards, debit cards, and other electronic payment methods. It is essentially the cost of providing convenience to your customers.

When you accept a ₹1,000 payment via credit card with a 2% MDR, you pay ₹20 in fees and receive ₹980. This fee covers the complex infrastructure needed to process payments securely, from encryption to settlement.

The fee gets split between three main parties. The payment gateway that handles technology infrastructure, the customer's bank that manages risk and verification, and the card network, like Visa or Mastercard, that handles routing and standards. Each party provides essential services that enable digital payments, which is why the fee exists.

MDR charges operate on a percentage-based model that activates every time a customer makes a digital payment. The process starts when your customer initiates a payment and ends when funds reach your account.

For example, if a customer pays ₹5,000 using a credit card with 2.5% MDR, you pay ₹125 in fees and receive ₹4,875 in your account.

Each payment method has its own MDR structure because banks and processors face different costs and risks when handling various transaction types. Knowing these rate differences helps you choose the right payment mix for your business.

Here's how various payment types affect your costs:

Let’s break down each type and what drives their costs:

Several factors determine your actual MDR rates, and knowing these helps you negotiate better deals and choose optimal payment solutions.

For instance, an e-commerce business with ₹25 lakh monthly volume, ₹2,500 average transaction size, and 60% debit card usage can negotiate MDR rates 0.5-1% lower than standard rates.

Calculating MDR charges helps you budget accurately and learn the true cost of each payment method. The basic formula is straightforward, but real-world applications can be more complex.

Basic MDR calculation:

MDR Amount = Transaction Value × MDR Rate

Example calculations:

For a ₹10,000 credit card payment with 2.5% MDR:

MDR Amount = ₹10,000 × 2.5% = ₹250

Net Amount Received = ₹10,000 - ₹250 = ₹9,750

Blended rate calculation:

If you accept multiple payment methods, calculate your effective blended MDR:

Total volume: ₹10,00,000

Total fees: ₹16,100

Blended MDR: 1.61%

Some payment processors charge setup fees, annual maintenance charges, or per-transaction fees on top of MDR percentages. Factor these into your total cost calculations.

Traditional payment solutions often surprise businesses with hidden fees, complex rate structures, and unclear pricing models. You need a payment partner that puts transparency first and helps you optimize costs rather than maximize them.

Modern businesses require payment solutions that scale globally while maintaining clear, predictable costs. That’s where PayGlocal comes in, helping you effectively manage your payment processes:

With PayGlocal, you get transparent pricing, no setup fees, and no hidden charges. You pay only when you transact, with rates that make sense for your business scale.

MDR charges are an unavoidable part of accepting digital payments, but they don't have to be unpredictable or excessive. Smart businesses treat payment processing costs as an investment in customer convenience and revenue growth rather than just an expense.

The key is choosing payment partners who offer transparent pricing, competitive rates, and the features you need to scale globally. Hidden fees and complex rate structures can quickly erode your margins, especially as transaction volumes grow.

Don't let payment processing costs affect your profits while competitors optimize theirs. Every day you delay optimizing payment costs is revenue left on the table. Get started with PayGlocal today and see exactly what you'll pay before you commit.

Every time a customer pays with a card or digital payment method, your business pays a fee. But these fees, called MDR charges, can quickly add up and impact your profit margins.

In this guide, we’re going to do a detailed breakdown of MDR charges, from basic calculations to their different types. By the end, you’ll have a complete idea of how they work and impact your business. Let’s get into it.

Key takeaways

- MDR definition: MDR charges are fees merchants pay to accept digital payments, typically ranging from 1% to 3% of transaction value.

- Cost breakdown: MDR fees are split between payment processors, banks, and card networks to cover transaction processing costs.

- Payment method variation: Credit cards generally have higher MDR rates than debit cards, while UPI transactions currently have no MDR for most users.

- Calculation factors: MDR rates depend on card type, business category, transaction volume, and risk assessment.

- Global payment solutions: PayGlocal offers clear pricing with no hidden fees, helping businesses optimize their payment acceptance costs.

What are MDR charges?

MDR charges, or Merchant Discount Rate charges, are fees that businesses pay to accept digital payments like credit cards, debit cards, and other electronic payment methods. It is essentially the cost of providing convenience to your customers.

When you accept a ₹1,000 payment via credit card with a 2% MDR, you pay ₹20 in fees and receive ₹980. This fee covers the complex infrastructure needed to process payments securely, from encryption to settlement.

The fee gets split between three main parties. The payment gateway that handles technology infrastructure, the customer's bank that manages risk and verification, and the card network, like Visa or Mastercard, that handles routing and standards. Each party provides essential services that enable digital payments, which is why the fee exists.

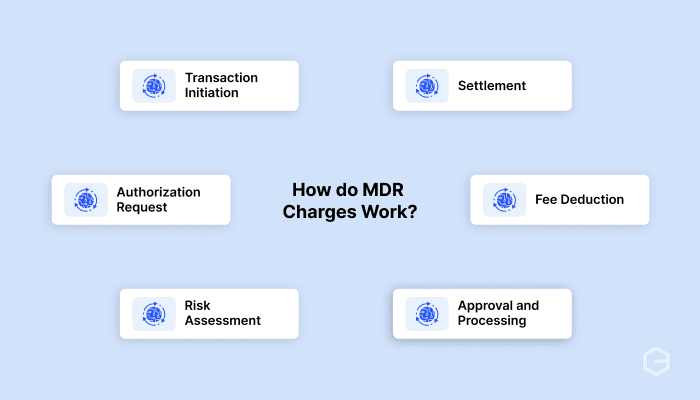

How do MDR charges work?

MDR charges operate on a percentage-based model that activates every time a customer makes a digital payment. The process starts when your customer initiates a payment and ends when funds reach your account.

- Transaction initiation: Customer enters payment details on your checkout page or swipes their card at your store.

- Authorization request: The payment processor sends transaction details to the customer's bank for approval.

- Risk assessment: Multiple systems check for fraud, available funds, and transaction validity in real-time.

- Approval and processing: Once approved, the transaction moves through the payment network for settlement.

- Fee deduction: MDR charges are automatically deducted from the transaction amount before funds reach your account.

- Settlement: You receive the net amount (transaction value minus MDR) typically within 1-2 business days.

For example, if a customer pays ₹5,000 using a credit card with 2.5% MDR, you pay ₹125 in fees and receive ₹4,875 in your account.

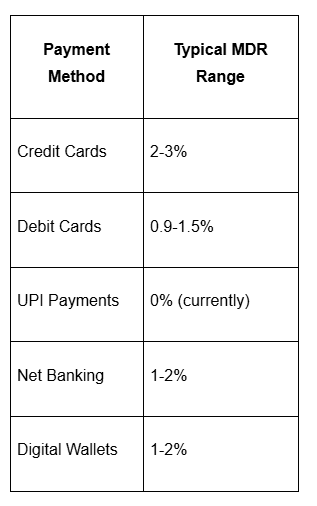

What are the types of MDR charges?

Each payment method has its own MDR structure because banks and processors face different costs and risks when handling various transaction types. Knowing these rate differences helps you choose the right payment mix for your business.

Here's how various payment types affect your costs:

Let’s break down each type and what drives their costs:

- Credit card MDR charges: Highest rates (2-3%) due to credit facilities and reward programs, with international cards having additional currency conversion fees.

- Debit card MDR charges: Lower rates (0.9-1.5%) since money is directly deducted from customer accounts, with RuPay offering the most competitive rates.

- UPI payment MDR charges: Currently free for bank account transactions, though UPI credit card payments can incur charges.

- Net banking MDR charges: Moderate rates (1-2%) with longer processing times, but direct bank-to-bank transfers.

- Digital wallet MDR charges: Variable rates (1-2%) depending on funding source, with wallet balance payments typically cheaper than linked card payments.

What factors affect MDR rates?

Several factors determine your actual MDR rates, and knowing these helps you negotiate better deals and choose optimal payment solutions.

- Business category and risk profile: Low-risk businesses like utilities or education typically get lower MDR rates compared to high-risk categories like gaming or travel. Payment processors assess your industry's chargeback rates and fraud risk.

- Transaction volume: Higher monthly processing volumes often qualify for reduced MDR rates. A business processing ₹10 lakh monthly can get better rates than one processing ₹1 lakh.

- Average transaction size: Larger average transactions usually get lower percentage rates since fixed processing costs get spread over bigger amounts. A ₹50,000 transaction can have lower MDR than multiple ₹5,000 transactions.

- Payment method mix: Your overall payment mix affects pricing. If most customers use debit cards or UPI, your blended MDR will be lower than if they primarily use credit cards.

- Settlement timeline: Faster settlement (next day vs. 3-5 days) can come with slightly higher MDR rates, but improves cash flow significantly.

- Geographic reach: Domestic-only businesses typically get better rates than those accepting international payments, which involve currency conversion and higher processing complexity.

For instance, an e-commerce business with ₹25 lakh monthly volume, ₹2,500 average transaction size, and 60% debit card usage can negotiate MDR rates 0.5-1% lower than standard rates.

How to calculate MDR charges?

Calculating MDR charges helps you budget accurately and learn the true cost of each payment method. The basic formula is straightforward, but real-world applications can be more complex.

Basic MDR calculation:

MDR Amount = Transaction Value × MDR Rate

Example calculations:

For a ₹10,000 credit card payment with 2.5% MDR:

MDR Amount = ₹10,000 × 2.5% = ₹250

Net Amount Received = ₹10,000 - ₹250 = ₹9,750

Blended rate calculation:

If you accept multiple payment methods, calculate your effective blended MDR:

- Monthly credit card payments: ₹5,00,000 at 2.5% = ₹12,500 fees

- Monthly debit card payments: ₹3,00,000 at 1.2% = ₹3,600 fees

- Monthly UPI payments: ₹2,00,000 at 0% = ₹0 fees

Total volume: ₹10,00,000

Total fees: ₹16,100

Blended MDR: 1.61%

Some payment processors charge setup fees, annual maintenance charges, or per-transaction fees on top of MDR percentages. Factor these into your total cost calculations.

Manage payment costs effectively with PayGlocal

Traditional payment solutions often surprise businesses with hidden fees, complex rate structures, and unclear pricing models. You need a payment partner that puts transparency first and helps you optimize costs rather than maximize them.

Modern businesses require payment solutions that scale globally while maintaining clear, predictable costs. That’s where PayGlocal comes in, helping you effectively manage your payment processes:

- Multi-currency accounts: Accept payments in 33+ currencies with transparent rates and automatic FIRC generation for compliance.

- Card payments: Competitive MDR rates on international credit and debit cards with industry-leading approval rates.

- Global payment methods: Access 40+ local payment methods worldwide with clear, upfront pricing.

- Dynamic checkout: Optimized checkout flows that boost conversion rates, maximizing revenue per transaction.

- Recurring payments: Automated subscription billing with transparent per-transaction costs.

- One platform: Unified dashboard for all payment methods, reducing operational complexity and hidden costs.

With PayGlocal, you get transparent pricing, no setup fees, and no hidden charges. You pay only when you transact, with rates that make sense for your business scale.

Final thoughts

MDR charges are an unavoidable part of accepting digital payments, but they don't have to be unpredictable or excessive. Smart businesses treat payment processing costs as an investment in customer convenience and revenue growth rather than just an expense.

The key is choosing payment partners who offer transparent pricing, competitive rates, and the features you need to scale globally. Hidden fees and complex rate structures can quickly erode your margins, especially as transaction volumes grow.

Don't let payment processing costs affect your profits while competitors optimize theirs. Every day you delay optimizing payment costs is revenue left on the table. Get started with PayGlocal today and see exactly what you'll pay before you commit.