With eCommerce fraud costing merchants 3% of annual revenue ($48 billion globally), a merchant account is essential for secure, scalable operations. These accounts enable businesses to accept diverse payment methods, enhance security with PCI compliance and fraud detection tools, and improve cash flow through faster settlements.

In this blog, we’ll explore the benefits of merchant accounts, from multi-channel payment acceptance to actionable fraud prevention strategies, while detailing how to apply, navigate different account types, and optimize payment processes for long-term growth.

A merchant is any business or individual selling goods or services and accepting payments. Merchants can be small businesses, online stores, or exporters.

A merchant account is a special bank account that enables businesses to receive and process payments via debit/credit cards or electronic payment systems. Thus, it is an intermediary between customer payments and the business bank account.

For example, in an export business scenario, you are the "merchant" if you run an online clothing store exporting goods internationally. You need a merchant account with a payment service provider to accept customer payments abroad. This account lets you securely process payments in multiple currencies and transfer funds from the customer's bank to your business account.

Also Read: Merchant Onboarding Policy @PayGlocal

Different types of merchant accounts exist to cater to the varied needs of businesses, from small online shops to large enterprises. These accounts are designed to handle different payment methods, transaction volumes, and industry-specific risks.

1. Retail Merchant Accounts: This account is ideal if you own a retail store with one or more physical locations. It has low setup fees and is suitable for businesses that require in-person payment processing capabilities. Retail accounts handle both credit and debit card transactions, enabling fast and secure credit card processing. They integrate with various POS systems for stores, restaurants, and salons.

2. eCommerce Merchant Accounts: An Internet merchant account is the right choice if you sell products or services online without a physical store location. Customers can enter their credit/debit card information into the system via encrypted payment gateways rather than giving out card details over the phone or via mail. These accounts also offer features like recurring billing for subscription-based services.

3. Mobile Merchant Accounts: These are perfect for businesses that need the flexibility to accept payments on the go. These accounts help process payments via mobile devices, card readers, or contactless payment systems, whether at trade shows, flea markets, or pop-up stores.

4. High-Risk Merchant Accounts: High-risk merchants, such as those in online gambling or pharmaceuticals, face stricter approval processes and higher transaction fees for merchant accounts. While they still offer standard features like credit card processing and payment gateway integration, they include added security measures like tokenization and encryption due to the higher risk.

5. International Merchant Account: This type of account is for businesses that operate globally and need to accept payments in multiple currencies. It is ideal for exporters who must process cross-border transactions. It allows businesses to securely accept payments via credit/debit cards, checks, mobile payments, and UPI, as per each consumer country.

Explore: Understanding International Transaction Fees: How Businesses Can Thrive Globally?

A merchant account allows businesses to accept various payment methods, improving cash flow and customer convenience. Let’s explore below for more details on how merchant accounts can benefit your business.

1. Increase in Sales: Card payments surpass cash purchases, with ₹10.80 crore of card transactions in December 2024. However, businesses that cannot process card payments risk losing sales opportunities. The shift towards a cashless economy and the surge in e-commerce underscore the importance of accepting card payments and the merchant accounts' role in facilitating domestic and international card transactions.

2. Accepting multiple payments: Customers opt for digital transactions via wallet or cards rather than relying on physical cash. A merchant account with integrated payment solutions helps businesses to accept payments online through UPI, net banking, or debit/credit cards.

3. Secure Payment Processing: Payment gateways serve as a vital link, seamlessly integrating online card processing into your business operations to minimize fraud risks and theft. This ensures a secure checkout experience, such as PCI DSS compliance, which protects you and your customers from data breaches and safeguards transactions.

4. Enhance cash flow: Credit and debit card transactions allow instant authorizations and funding within 1-2 business days. In contrast, relying solely on invoicing and check payments can extend the process to 30 days, factoring in mailing time and check processing delays.

5. Data-Driven Decision Making: Merchant accounts offer reporting tools and analytics that help businesses track sales, monitor trends, and manage financial data. With access to the GCC dashboard, merchants can get detailed reports, including transaction insights and top-selling products, and make informed decisions.

When a customer makes a payment, their information is securely transmitted to the payment processor for verification. The processor checks with the card network for sufficient funds that match the provided details. Once approved, funds are transferred to the merchant account, and necessary fees are deducted.

1. Customer Initiates Payment: The process begins when a customer decides to make a purchase and initiates a payment using a credit or debit card.

2. Payment Information Submission: The customer's payment details are entered into the merchant's point-of-sale (POS) system or online payment gateway.

3. Authorization Request: The merchant's system sends the payment information to the payment processor, which forwards it to the card network (e.g., Visa, MasterCard).

4. Issuer Bank Verification: The card network routes the transaction to the customer's issuing bank to verify the availability of funds and check for potential fraud.

5. Authorization Response: The issuing bank approves or declines the transaction and sends an authorization code back through the network to the merchant's system.

6. Transaction Completion: If approved, the merchant completes the sale, and the customer receives a receipt or confirmation of the transaction.

7. Batching Transactions: At the end of the business day, the merchant batches all approved transactions and submits them to the payment processor for settlement.

8. Settlement Process: The payment processor forwards the transaction details to the card networks, which then communicate with the issuing banks to transfer funds.

9. Funds Transfer: The issuing bank transfers the funds to the acquiring (merchant's) bank, minus any applicable fees.

10. Deposit to Merchant Account: The acquiring bank deposits the funds into the merchant's account, completing the payment cycle.

After these steps, the merchant account handles the final processing, ensuring the funds are accurately deposited into the business’s bank account. Any discrepancies or issues are flagged for review, and all transaction records are maintained for accounting and reporting purposes.

Explore: Understanding Payment Transaction Processing and Types

Understanding eligibility to apply for a merchant account is essential to ensure smooth approval and compliance. It helps align with regulatory standards and manage financial transactions efficiently.

Below are the essential documents required to set up a merchant account. Each category ensures that your business meets legal, financial, and compliance standards for payment processing.

After gathering your business license, financial statements, and other required documentation, you should submit these details to the chosen payment processor.

Obtaining a merchant account is the first step in enabling your business to accept credit and debit card payments. While the process involves extensive paperwork, payment processors offer a more streamlined process, allowing quick approval.

Step 1: Obtain a Business License

Depending on your industry and local regulations, you may need a business license before applying for a merchant account. An active license demonstrates compliance with local laws, aiding the approval process.

Step 2: Establish a Business Bank Account Acquirers and processors typically require a dedicated business bank account. This account is the final destination for cleared funds from your merchant account and facilitates debits for fees like processing and chargebacks.

Step 3: Assess Your Business Needs

Different business types and structures may require separate merchant accounts based on how transactions are conducted. Determine if you need accounts for e-commerce, in-person sales, international transactions, or high-risk payments.

Step 4: Gather Required Documentation

Acquirers and processors need comprehensive business information for underwriting. To support your application, collect necessary documents such as a business background, financial statements, and risk management procedures.

Step 5: Research Merchant Account Providers and Submit Application

Identify merchant account providers specializing in your transaction types or industry. Choose a provider that meets your business's volume and size requirements. Then, apply with the chosen merchant account provider. Some providers may charge an application fee.

Step 6: Await Approval

The underwriting process varies but typically takes a few days. During this period, be prepared to provide additional information or implement risk management measures if requested.

Step 7: Review and Sign the Merchant Service Agreement

Upon approval, carefully review the merchant service agreement. Before signing, negotiate terms and understand fees, payment structures, and chargeback policies.

Step 8: Activate Your Merchant Account

Once the agreement is signed and any setup fees are paid, your merchant account will be activated to process payments.

This structured approach ensures that businesses are well-prepared to navigate the merchant account application process effectively.

Once you've successfully applied for and obtained a merchant account, the fees can impact your overall payment processing costs associated with the merchant account.

When you have a merchant account, the primary costs you’ll face are the ongoing payment processing fees charged per transaction. These fees can differ depending on the provider.

Apart from transaction fees, merchant account providers may charge additional fees, including:

Setup Fee: A one-time charge for establishing your merchant account.

Monthly Minimum Fee: Some providers require you to meet a minimum monthly payment processing amount. If your transactions fall short, you’ll be billed for the difference.

Annual Fee: Certain providers charge a yearly fee to maintain your merchant account.

Batch Fee: Transactions are often grouped in a "batch" and submitted for processing. A batch fee covers this process.

Chargeback Fee: If a customer disputes a charge, resulting in a reversal, you may incur a chargeback fee.

Early Termination Fee: If you close your account before the end of the agreed-upon term, you may be charged a fee for early cancellation.

These fees can vary, so reviewing the terms and understanding the costs involved when choosing a merchant account provider is essential.

Establishing a merchant account is a pivotal step for businesses aiming to accept credit and debit card payments. It streamlines operations, enhances payment flexibility, and ensures robust security for both merchants and customers. However, to truly capitalize on the global market, especially for Indian businesses, partnering with a specialized payment solutions provider is essential.

PayGlocal stands out as a premier choice for cross-border payments. Tailored to meet the unique challenges of international transactions, PayGlocal offers:

Multi-Currency Accounts: Accept payments in over 33 currencies from over 180 countries, reducing conversion costs and settlement delays.

Transparent Pricing: Enjoy zero setup, maintenance, or hidden charges, with transparent and competitive transaction fees.

High Approval Rates: Benefit from an intelligent orchestration engine that enhances transaction success, even with international cards.

Comprehensive Support: Access 24/7 customer service, dedicated account managers, and real-time transaction tracking.

By choosing PayGlocal, businesses can easily navigate the complexities of cross-border payments. Get Started Today!

In this blog, we’ll explore the benefits of merchant accounts, from multi-channel payment acceptance to actionable fraud prevention strategies, while detailing how to apply, navigate different account types, and optimize payment processes for long-term growth.

Who is a Merchant and What is a Merchant Account?

A merchant is any business or individual selling goods or services and accepting payments. Merchants can be small businesses, online stores, or exporters.

A merchant account is a special bank account that enables businesses to receive and process payments via debit/credit cards or electronic payment systems. Thus, it is an intermediary between customer payments and the business bank account.

For example, in an export business scenario, you are the "merchant" if you run an online clothing store exporting goods internationally. You need a merchant account with a payment service provider to accept customer payments abroad. This account lets you securely process payments in multiple currencies and transfer funds from the customer's bank to your business account.

Also Read: Merchant Onboarding Policy @PayGlocal

Types of Merchant Accounts

Different types of merchant accounts exist to cater to the varied needs of businesses, from small online shops to large enterprises. These accounts are designed to handle different payment methods, transaction volumes, and industry-specific risks.

1. Retail Merchant Accounts: This account is ideal if you own a retail store with one or more physical locations. It has low setup fees and is suitable for businesses that require in-person payment processing capabilities. Retail accounts handle both credit and debit card transactions, enabling fast and secure credit card processing. They integrate with various POS systems for stores, restaurants, and salons.

2. eCommerce Merchant Accounts: An Internet merchant account is the right choice if you sell products or services online without a physical store location. Customers can enter their credit/debit card information into the system via encrypted payment gateways rather than giving out card details over the phone or via mail. These accounts also offer features like recurring billing for subscription-based services.

3. Mobile Merchant Accounts: These are perfect for businesses that need the flexibility to accept payments on the go. These accounts help process payments via mobile devices, card readers, or contactless payment systems, whether at trade shows, flea markets, or pop-up stores.

4. High-Risk Merchant Accounts: High-risk merchants, such as those in online gambling or pharmaceuticals, face stricter approval processes and higher transaction fees for merchant accounts. While they still offer standard features like credit card processing and payment gateway integration, they include added security measures like tokenization and encryption due to the higher risk.

5. International Merchant Account: This type of account is for businesses that operate globally and need to accept payments in multiple currencies. It is ideal for exporters who must process cross-border transactions. It allows businesses to securely accept payments via credit/debit cards, checks, mobile payments, and UPI, as per each consumer country.

Explore: Understanding International Transaction Fees: How Businesses Can Thrive Globally?

What are the Benefits of Holding a Merchant Account?

A merchant account allows businesses to accept various payment methods, improving cash flow and customer convenience. Let’s explore below for more details on how merchant accounts can benefit your business.

1. Increase in Sales: Card payments surpass cash purchases, with ₹10.80 crore of card transactions in December 2024. However, businesses that cannot process card payments risk losing sales opportunities. The shift towards a cashless economy and the surge in e-commerce underscore the importance of accepting card payments and the merchant accounts' role in facilitating domestic and international card transactions.

2. Accepting multiple payments: Customers opt for digital transactions via wallet or cards rather than relying on physical cash. A merchant account with integrated payment solutions helps businesses to accept payments online through UPI, net banking, or debit/credit cards.

3. Secure Payment Processing: Payment gateways serve as a vital link, seamlessly integrating online card processing into your business operations to minimize fraud risks and theft. This ensures a secure checkout experience, such as PCI DSS compliance, which protects you and your customers from data breaches and safeguards transactions.

4. Enhance cash flow: Credit and debit card transactions allow instant authorizations and funding within 1-2 business days. In contrast, relying solely on invoicing and check payments can extend the process to 30 days, factoring in mailing time and check processing delays.

5. Data-Driven Decision Making: Merchant accounts offer reporting tools and analytics that help businesses track sales, monitor trends, and manage financial data. With access to the GCC dashboard, merchants can get detailed reports, including transaction insights and top-selling products, and make informed decisions.

How Does a Merchant Account Work?

When a customer makes a payment, their information is securely transmitted to the payment processor for verification. The processor checks with the card network for sufficient funds that match the provided details. Once approved, funds are transferred to the merchant account, and necessary fees are deducted.

1. Customer Initiates Payment: The process begins when a customer decides to make a purchase and initiates a payment using a credit or debit card.

2. Payment Information Submission: The customer's payment details are entered into the merchant's point-of-sale (POS) system or online payment gateway.

3. Authorization Request: The merchant's system sends the payment information to the payment processor, which forwards it to the card network (e.g., Visa, MasterCard).

4. Issuer Bank Verification: The card network routes the transaction to the customer's issuing bank to verify the availability of funds and check for potential fraud.

5. Authorization Response: The issuing bank approves or declines the transaction and sends an authorization code back through the network to the merchant's system.

6. Transaction Completion: If approved, the merchant completes the sale, and the customer receives a receipt or confirmation of the transaction.

7. Batching Transactions: At the end of the business day, the merchant batches all approved transactions and submits them to the payment processor for settlement.

8. Settlement Process: The payment processor forwards the transaction details to the card networks, which then communicate with the issuing banks to transfer funds.

9. Funds Transfer: The issuing bank transfers the funds to the acquiring (merchant's) bank, minus any applicable fees.

10. Deposit to Merchant Account: The acquiring bank deposits the funds into the merchant's account, completing the payment cycle.

After these steps, the merchant account handles the final processing, ensuring the funds are accurately deposited into the business’s bank account. Any discrepancies or issues are flagged for review, and all transaction records are maintained for accounting and reporting purposes.

Explore: Understanding Payment Transaction Processing and Types

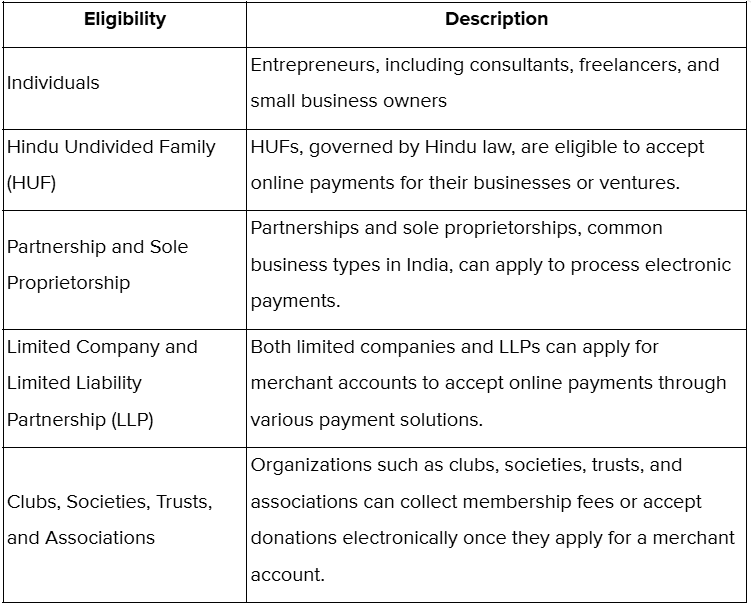

Who is Eligible to Apply for a Merchant Account?

Understanding eligibility to apply for a merchant account is essential to ensure smooth approval and compliance. It helps align with regulatory standards and manage financial transactions efficiently.

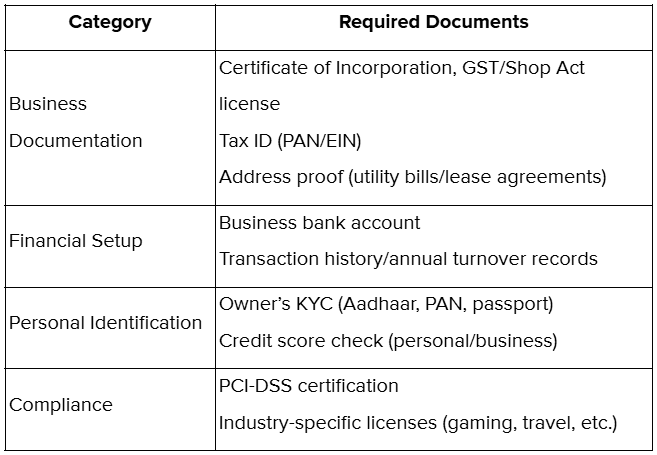

Document Required to Open a Merchant Account

Below are the essential documents required to set up a merchant account. Each category ensures that your business meets legal, financial, and compliance standards for payment processing.

After gathering your business license, financial statements, and other required documentation, you should submit these details to the chosen payment processor.

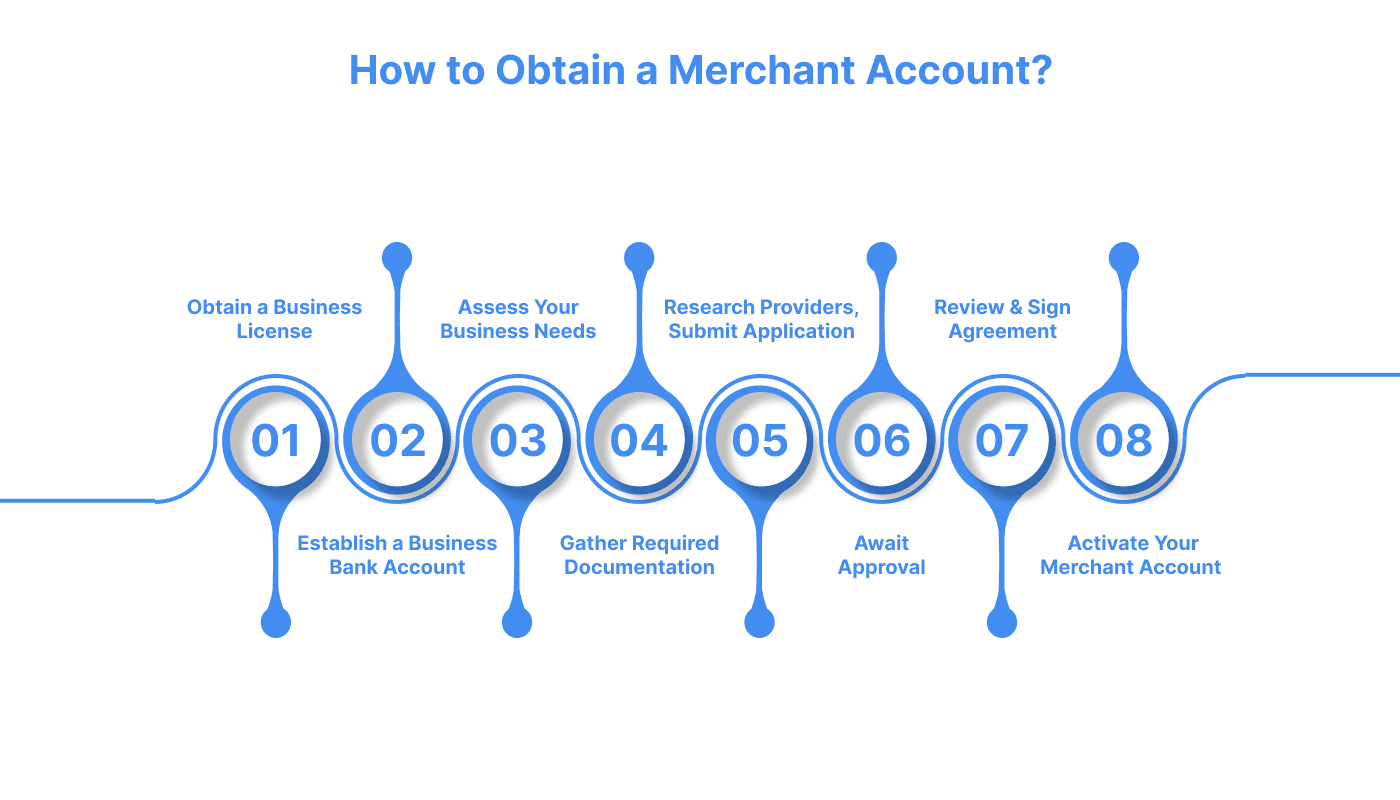

How to Obtain a Merchant Account?

Obtaining a merchant account is the first step in enabling your business to accept credit and debit card payments. While the process involves extensive paperwork, payment processors offer a more streamlined process, allowing quick approval.

Step 1: Obtain a Business License

Depending on your industry and local regulations, you may need a business license before applying for a merchant account. An active license demonstrates compliance with local laws, aiding the approval process.

Step 2: Establish a Business Bank Account Acquirers and processors typically require a dedicated business bank account. This account is the final destination for cleared funds from your merchant account and facilitates debits for fees like processing and chargebacks.

Step 3: Assess Your Business Needs

Different business types and structures may require separate merchant accounts based on how transactions are conducted. Determine if you need accounts for e-commerce, in-person sales, international transactions, or high-risk payments.

Step 4: Gather Required Documentation

Acquirers and processors need comprehensive business information for underwriting. To support your application, collect necessary documents such as a business background, financial statements, and risk management procedures.

Step 5: Research Merchant Account Providers and Submit Application

Identify merchant account providers specializing in your transaction types or industry. Choose a provider that meets your business's volume and size requirements. Then, apply with the chosen merchant account provider. Some providers may charge an application fee.

Step 6: Await Approval

The underwriting process varies but typically takes a few days. During this period, be prepared to provide additional information or implement risk management measures if requested.

Step 7: Review and Sign the Merchant Service Agreement

Upon approval, carefully review the merchant service agreement. Before signing, negotiate terms and understand fees, payment structures, and chargeback policies.

Step 8: Activate Your Merchant Account

Once the agreement is signed and any setup fees are paid, your merchant account will be activated to process payments.

This structured approach ensures that businesses are well-prepared to navigate the merchant account application process effectively.

Once you've successfully applied for and obtained a merchant account, the fees can impact your overall payment processing costs associated with the merchant account.

What are the Fees Associated with Merchant Accounts?

When you have a merchant account, the primary costs you’ll face are the ongoing payment processing fees charged per transaction. These fees can differ depending on the provider.

Apart from transaction fees, merchant account providers may charge additional fees, including:

Setup Fee: A one-time charge for establishing your merchant account.

Monthly Minimum Fee: Some providers require you to meet a minimum monthly payment processing amount. If your transactions fall short, you’ll be billed for the difference.

Annual Fee: Certain providers charge a yearly fee to maintain your merchant account.

Batch Fee: Transactions are often grouped in a "batch" and submitted for processing. A batch fee covers this process.

Chargeback Fee: If a customer disputes a charge, resulting in a reversal, you may incur a chargeback fee.

Early Termination Fee: If you close your account before the end of the agreed-upon term, you may be charged a fee for early cancellation.

These fees can vary, so reviewing the terms and understanding the costs involved when choosing a merchant account provider is essential.

Conclusion

Establishing a merchant account is a pivotal step for businesses aiming to accept credit and debit card payments. It streamlines operations, enhances payment flexibility, and ensures robust security for both merchants and customers. However, to truly capitalize on the global market, especially for Indian businesses, partnering with a specialized payment solutions provider is essential.

PayGlocal stands out as a premier choice for cross-border payments. Tailored to meet the unique challenges of international transactions, PayGlocal offers:

Multi-Currency Accounts: Accept payments in over 33 currencies from over 180 countries, reducing conversion costs and settlement delays.

Transparent Pricing: Enjoy zero setup, maintenance, or hidden charges, with transparent and competitive transaction fees.

High Approval Rates: Benefit from an intelligent orchestration engine that enhances transaction success, even with international cards.

Comprehensive Support: Access 24/7 customer service, dedicated account managers, and real-time transaction tracking.

By choosing PayGlocal, businesses can easily navigate the complexities of cross-border payments. Get Started Today!