Managing fund transfers can be challenging, especially when dealing with transaction limits, processing delays, and unexpected fees. If you’ve ever faced confusion about how NEFT works, its charges, or whether it suits your financial needs, you’re not alone.**

This blog breaks down the key features, transfer limits, and associated costs of NEFT, helping you make financial decisions for seamless and hassle-free transactions.

NEFT stands for National Electronic Funds Transfer. It is an electronic system that facilitates the transfer of funds between bank accounts.

NEFT operates on a deferred net settlement (DNS) system, processing transactions in batches and settling them at half-hourly (30 minutes) intervals. It is also important to note here that NEFT transactions cannot be used for international transfers. It is intended for sending money between banks within India.

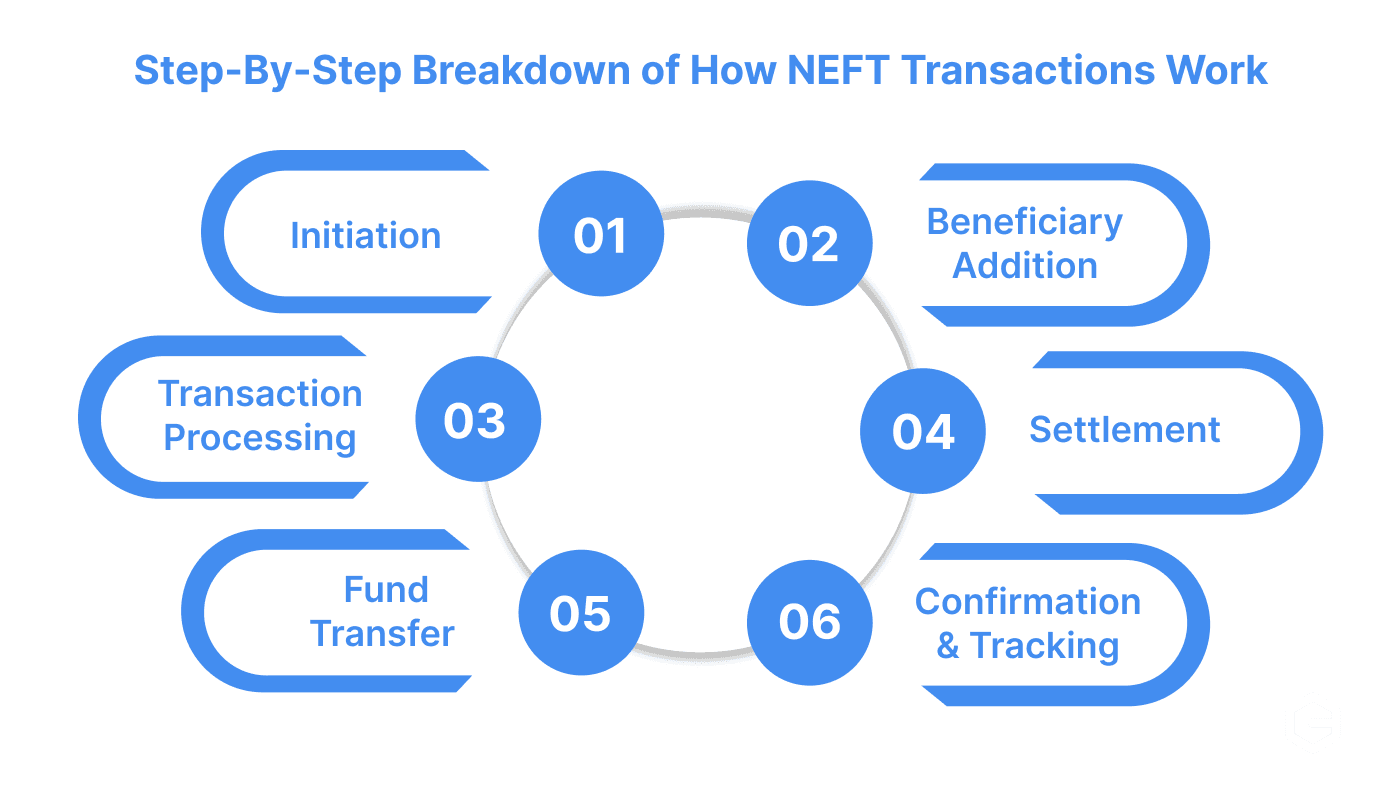

Here’s a step-by-step breakdown of how NEFT transactions work:

The sender begins the process by providing essential details, including the beneficiary's account number, bank branch, and the amount to be transferred.

The sender must add the beneficiary’s account details (account number and branch). This step is only needed once for future transfers.

Once initiated, the sender’s bank sends the transaction details to the NEFT clearing center, where transactions from different banks are grouped into batches for processing.

NEFT transactions are processed in hourly batches throughout the day. The clearing center (RBI) processes these batches and sends them to the respective banks for settlement.

After the settlement, the beneficiary’s bank credits the funds to their account. This happens either the same day or the next working day, depending on the timing of the transaction.

Both the sender and the beneficiary receive confirmation from their banks once the transfer is complete. The sender can also track the status through net banking.

NEFT ensures secure domestic transfers, but is limited when it comes to international transactions. For exporters, freelancers, and businesses handling cross-border payments, PayGlocal provides fast and secure international transactions with multi-currency support.

While NEFT assures you that your money is transferred securely, you must keep the necessary details in hand before proceeding with the transaction to avoid errors and ensure the funds reach the beneficiary smoothly.

Quick Read: Difference Between NEFT and RTGS: A Simple Guide

To complete a successful NEFT transfer, you will need the following information about the beneficiary.

Having the correct details for an NEFT transaction will ensure an accurate transfer. Let’s take a look at the limits and timings, as it helps you manage the transfer process smoothly.

NEFT offers flexible transfer options, with varying limits depending on the time of day and security protocols. Here are more details.

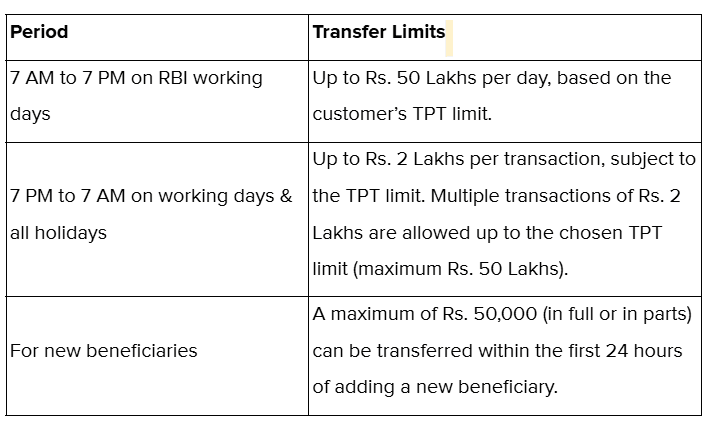

The Reserve Bank of India does not set any specific limits on NEFT fund transfers. However, individual banks may impose their limits, which could vary depending on the bank’s policies and the timing of the transfer for security reasons.

Here is an example of the limit set by HDFC Bank

NEFT services for online transfers are available 24/7 throughout the year, allowing you to make transactions at any time via net banking or mobile banking.

For offline NEFT transfers, however, the timings depend on the operating hours of the bank branch.

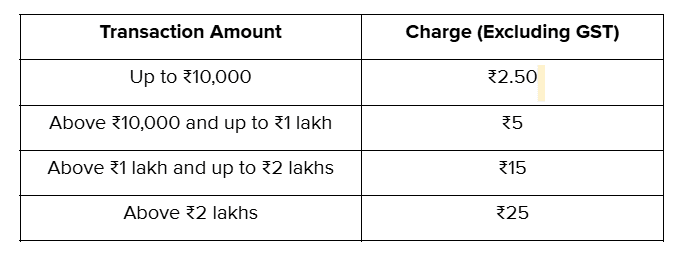

There are no charges for NEFT transactions for the receiving bank. Furthermore, starting January 2020, most banks will no longer charge savings account holders for online NEFT transfers. However, the sending bank may charge its customers for outward transactions with the following maximum fees.

NEFT charges for different banks:

NEFT transactions generally offer cost-effective transfer options. Moving ahead to provide a clearer overview, let's summarize the key features we’ve discussed above in bite-sized points for better understanding.

NEFT offers a reliable and secure way to transfer funds across India. Here are some of the features that make it a convenient choice for both individuals and businesses.

While NEFT offers numerous features, it also has certain limitations that users should consider before making transactions.

Let us understand the drawbacks of NEFT payments which will further help you in choosing the right payment method based on specific needs.

To overcome these challenges, PayGlocal offers a comprehensive international payment platform with the following features:

By using PayGlocal's advanced payment solutions, businesses and freelancers can improve their payment processes, ensuring speed, reliability, and global reach beyond the constraints of traditional systems like NEFT.

Although the NEFT transactions are pretty simple to operate but, you need to exercise extreme caution. Here are some tips for a smooth and secure transfer.

These best practices help streamline your NEFT transactions while maintaining security and accuracy.

NEFT provides a secure and flexible way to transfer funds, offering round-the-clock accessibility for seamless transactions. Its flexibility and round-the-clock availability make it a convenient choice for individuals and businesses alike. Whether for personal transactions or business payments, NEFT simplifies financial operations with its structured process and widespread accessibility.

However, for businesses looking to expand globally and accept cross-border payments with ease, solutions like PayGlocal offer advanced payment processing with higher success rates and robust security.

Understanding NEFT alongside modern payment solutions helps in making informed financial decisions and optimizing transactions. Get Started Today!

This blog breaks down the key features, transfer limits, and associated costs of NEFT, helping you make financial decisions for seamless and hassle-free transactions.

What is NEFT?

NEFT stands for National Electronic Funds Transfer. It is an electronic system that facilitates the transfer of funds between bank accounts.

How Does NEFT Work?

NEFT operates on a deferred net settlement (DNS) system, processing transactions in batches and settling them at half-hourly (30 minutes) intervals. It is also important to note here that NEFT transactions cannot be used for international transfers. It is intended for sending money between banks within India.

Here’s a step-by-step breakdown of how NEFT transactions work:

- Step 1: Initiation

The sender begins the process by providing essential details, including the beneficiary's account number, bank branch, and the amount to be transferred.

- Step 2: Beneficiary Addition

The sender must add the beneficiary’s account details (account number and branch). This step is only needed once for future transfers.

- Step 3: Transaction Processing

Once initiated, the sender’s bank sends the transaction details to the NEFT clearing center, where transactions from different banks are grouped into batches for processing.

- Step 4: Settlement

NEFT transactions are processed in hourly batches throughout the day. The clearing center (RBI) processes these batches and sends them to the respective banks for settlement.

- Step 5: Fund Transfer

After the settlement, the beneficiary’s bank credits the funds to their account. This happens either the same day or the next working day, depending on the timing of the transaction.

- Step 6: Confirmation and Tracking

Both the sender and the beneficiary receive confirmation from their banks once the transfer is complete. The sender can also track the status through net banking.

- Sender: The person who initiates the transfer.

- Beneficiary: The person who receives the funds.

NEFT ensures secure domestic transfers, but is limited when it comes to international transactions. For exporters, freelancers, and businesses handling cross-border payments, PayGlocal provides fast and secure international transactions with multi-currency support.

While NEFT assures you that your money is transferred securely, you must keep the necessary details in hand before proceeding with the transaction to avoid errors and ensure the funds reach the beneficiary smoothly.

Quick Read: Difference Between NEFT and RTGS: A Simple Guide

What are the Details Required for NEFT Transactions?

To complete a successful NEFT transfer, you will need the following information about the beneficiary.

- Beneficiary’s Name

- Bank Account Number

- IFSC Code of the beneficiary’s branch (found on your cheque book or through online banking)

- Bank Name and Branch Location

- Transfer Amount (the exact amount you wish to transfer)

- Sender’s Account Details

- Sender and Beneficiary Legal Entity Identifier (LEI) is required in business or corporate transfers.

Having the correct details for an NEFT transaction will ensure an accurate transfer. Let’s take a look at the limits and timings, as it helps you manage the transfer process smoothly.

Limits and Timings of NEFT in India

NEFT offers flexible transfer options, with varying limits depending on the time of day and security protocols. Here are more details.

NEFT Limit in India

The Reserve Bank of India does not set any specific limits on NEFT fund transfers. However, individual banks may impose their limits, which could vary depending on the bank’s policies and the timing of the transfer for security reasons.

Here is an example of the limit set by HDFC Bank

NEFT Timings in India

NEFT services for online transfers are available 24/7 throughout the year, allowing you to make transactions at any time via net banking or mobile banking.

For offline NEFT transfers, however, the timings depend on the operating hours of the bank branch.

NEFT Charges in India

There are no charges for NEFT transactions for the receiving bank. Furthermore, starting January 2020, most banks will no longer charge savings account holders for online NEFT transfers. However, the sending bank may charge its customers for outward transactions with the following maximum fees.

NEFT charges for different banks:

- State Bank of India (SBI): Rs. 2 to Rs. 20 based on the transaction amount.

- HDFC Bank: Rs. 2.5 to Rs. 25 for NEFT transactions.

- ICICI Bank: Rs. 2.5 to Rs. 25, similar to HDFC Bank.

NEFT transactions generally offer cost-effective transfer options. Moving ahead to provide a clearer overview, let's summarize the key features we’ve discussed above in bite-sized points for better understanding.

Key Features of NEFT Transaction

NEFT offers a reliable and secure way to transfer funds across India. Here are some of the features that make it a convenient choice for both individuals and businesses.

- No Minimum Transfer Limit: NEFT allows you to transfer even small amounts, making it suitable for both small and large transactions.

- 24/7 Availability: NEFT is accessible around the clock, including weekends and holidays, ensuring you can transfer funds at any time.

- Nationwide Coverage: You can send money to any bank account within India that is NEFT-enabled.

- Batch Processing: NEFT transactions are processed in batches, typically every 30 minutes, which helps streamline the transfer process.

- Security: NEFT transactions are regulated by the Reserve Bank of India (RBI), ensuring secure and reliable transactions.

- Online and Offline Options: You can initiate NEFT transfers via Internet banking, mobile apps, or directly at a bank branch.

While NEFT offers numerous features, it also has certain limitations that users should consider before making transactions.

Disadvantages of NEFT Payments

Let us understand the drawbacks of NEFT payments which will further help you in choosing the right payment method based on specific needs.

- Transaction Delays: NEFT transactions are processed in half-hourly batches, which can lead to delays, especially for time-sensitive transfers.

- Bank Participation Requirement: Both the sender and recipient must have accounts with NEFT-enabled banks; transactions cannot be completed if either bank is not part of the NEFT network.

- Lack of Immediate Confirmation: Unlike IMPS or UPI, NEFT does not provide instant transaction status updates, requiring users to wait for confirmation.

How Does PayGlocal Address These Limitations?

To overcome these challenges, PayGlocal offers a comprehensive international payment platform with the following features:

- Instant Transactions: PayGlocal facilitates real-time payments and dynamic checkout for viewing and managing payments from a single place.

- Global Bank Integration: With support for payments in 33 currencies across 180+ countries, PayGlocal enables transactions regardless of the banks' participation in traditional systems like NEFT.

- Samruddhi-X Security Protocol: An advanced tool that ensures compliance and safeguards each transaction, providing extra security in cross-border payments.

By using PayGlocal's advanced payment solutions, businesses and freelancers can improve their payment processes, ensuring speed, reliability, and global reach beyond the constraints of traditional systems like NEFT.

Tips for Effective NEFT Use

Although the NEFT transactions are pretty simple to operate but, you need to exercise extreme caution. Here are some tips for a smooth and secure transfer.

- Verify beneficiary details (name, account number, IFSC) to avoid errors.

- Add beneficiaries in advance to save time if required by your bank.

- Schedule NEFT for future payments if your bank allows it.

- Be aware of transaction limits set by your bank.

- NEFT runs 24/7 but processes in batches—transfer during banking hours for faster processing.

- Check transaction fees in advance to avoid unexpected charges.

- Keep transaction receipts as proof for future reference.

- Use only official banking websites or apps to prevent fraud.

- Avoid transfers to unknown individuals or companies.

- Report errors immediately to your bank for quick resolution.

These best practices help streamline your NEFT transactions while maintaining security and accuracy.

Conclusion

NEFT provides a secure and flexible way to transfer funds, offering round-the-clock accessibility for seamless transactions. Its flexibility and round-the-clock availability make it a convenient choice for individuals and businesses alike. Whether for personal transactions or business payments, NEFT simplifies financial operations with its structured process and widespread accessibility.

However, for businesses looking to expand globally and accept cross-border payments with ease, solutions like PayGlocal offer advanced payment processing with higher success rates and robust security.

Understanding NEFT alongside modern payment solutions helps in making informed financial decisions and optimizing transactions. Get Started Today!