Your customer pulls out their phone, taps it on your payment terminal, and walks away with their purchase confirmed in seconds. That's NFC payment at work.

For businesses accepting payments from customers, offering modern payment methods like NFC can significantly improve the checkout experience. In fact, data shows that the total value of contactless payments will be $18.1 trillion by 2030, highlighting the growing importance of these payment modes.

In this guide, we break down in detail what NFC payments are, how the technology works, why they're secure, and how businesses can accept contactless payments. Let’s get into it.

NFC payment is a contactless payment method that uses Near Field Communication technology to transfer payment information between two devices held close together. The transaction happens when customers tap or hold an NFC-enabled device like a smartphone, smartwatch, or contactless card near a compatible payment terminal.

The technology works through short-range radio waves that communicate within a few centimeters. When customers tap their phone to pay at your checkout, the NFC chip in their device exchanges encrypted payment data with your terminal's NFC reader. This exchange takes less than a second.

For example, when a customer at your store uses Google Pay or Apple Pay, they're using NFC payment. The phone doesn't transmit their actual card number to your terminal. Instead, it sends a one-time encrypted token specific to that transaction. Your terminal receives this token, validates it with the customer's bank, and approves the payment.

NFC payments work both for physical retail transactions and digital checkouts. For physical purchases at your store or showroom, customers tap their device on your terminal. For online purchases through your website, digital wallets using NFC technology can speed up checkout by auto-filling payment details securely.

NFC payment happens through a quick sequence of steps that prioritize both speed and security. The entire process completes in seconds at your checkout.

The process involves five main steps:

For instance, when a customer taps their phone at your checkout counter, the NFC chip activates, generates a token replacing their card number, encrypts the transaction data, waits for their fingerprint confirmation, and completes the authorization within two seconds.

The technology behind contactless NFC transactions ensures the customer's actual payment credentials never leave their device. Your terminal only receives temporary tokens that expire immediately after use.

NFC payment technology works across different devices and scenarios. Each type serves specific use cases while maintaining the same security standards.

Let's look at each type in detail:

For example, when an international customer visits your showroom, they can pay using Google Pay loaded with their home country card. The wallet stores multiple cards, lets them choose which one to use, and keeps a transaction history for their records.

For instance, a business customer's corporate credit card might support contactless payments. At your retail location, they can tap their card on your payment terminal instead of inserting it. Transactions under a certain limit often don't require PIN entry, making checkout even faster.

A customer wearing an Apple Watch can pay for their purchase by tapping their wrist on your terminal. This works even if they left their phone elsewhere, ensuring the transaction still completes.

NFC payments offer practical advantages for both businesses and customers. These benefits highlight why contactless transactions are becoming the global standard.

NFC payment security relies on multiple protective layers working together. The technology prevents fraud at every step, making it more secure than traditional magnetic stripe cards while maintaining the speed customers expect.

Here's how NFC payments protect your business and customers:

The combination of tokenization, encryption, device authentication, limited range, and one-time use makes NFC payments more secure than magnetic stripe cards. Your customers get protection without sacrificing the convenience of fast checkout.

Accepting NFC payments at your business requires compatible hardware and integration with a payment provider. The setup process is straightforward and can be completed quickly.

Here's what you need to start accepting contactless payments:

When selecting terminals, look for devices that support multiple payment types. The terminal should accept contactless cards, mobile wallets like Google Pay and Apple Pay, and wearable devices. This ensures you can serve customers regardless of their preferred payment method.

For businesses accepting international payments, select a provider with global payment infrastructure.

The integration allows transaction data to flow between the terminal and your inventory, accounting, and reporting systems. When a customer taps to pay, the sale automatically updates your records.

Staff should also know that NFC terminals work the same way for cards and mobile wallets. The customer simply taps regardless of payment method.

For instance, if you run an export business with a retail showroom, displaying Apple Pay and Google Pay logos alongside the contactless symbol tells international visitors they can pay using familiar methods from their home countries.

Run test transactions to verify the terminal connects properly, processes payments within seconds, and sends confirmation to both the terminal display and your POS system.

Modern payment technology like NFC creates the fast, frictionless checkout experiences customers expect. But for businesses accepting payments from global customers, offering modern checkout is just one piece of the puzzle.

You also need to accept payments in multiple currencies, provide local payment methods customers trust, manage compliance across borders, and maintain high payment success rates. Doing all this while keeping costs transparent and operations simple requires the right payment partner.

PayGlocal provides a complete payment solution designed for Indian businesses growing globally. Here's how we help:

PayGlocal helps you accept modern payment methods that customers expect while handling the complexity of cross-border commerce. You pay only when you transact with zero setup fees, no platform charges, and transparent pricing.

NFC payment technology has changed how people expect to pay. The tap-and-go experience is now standard in markets worldwide. For businesses, offering contactless payment options means meeting customer expectations and reducing friction at the most critical moment of the buying process.

The security, speed, and convenience of NFC payments benefit both customers and businesses. Customers get faster checkouts and better protection. Businesses see higher success rates and improved customer satisfaction.

If you're doing business with customers across borders, modern payment acceptance goes beyond just NFC. You need a payment stack that handles multiple currencies, offers local payment methods, maintains compliance, and keeps approval rates high.

Get started with PayGlocal today and give your global customers the seamless payment experience they expect.

For businesses accepting payments from customers, offering modern payment methods like NFC can significantly improve the checkout experience. In fact, data shows that the total value of contactless payments will be $18.1 trillion by 2030, highlighting the growing importance of these payment modes.

In this guide, we break down in detail what NFC payments are, how the technology works, why they're secure, and how businesses can accept contactless payments. Let’s get into it.

Key takeaways

- NFC payment: NFC stands for Near Field Communication, a wireless technology that enables contactless payments within a few centimeters of a payment terminal.

- Security through tokenization: NFC transactions use unique tokens instead of actual card numbers, combined with encryption and device authentication for protection.

- Multiple use cases: NFC works for retail purchases, online checkout via digital wallets, recurring payments, and subscription services.

- Business benefits: Accepting NFC payments reduces checkout time, improves payment success rates, and meets modern customer expectations.

- Global payment solution: Payment platforms like PayGlocal provide the infrastructure to accept international payments alongside traditional methods through one unified checkout.

What is NFC payment?

NFC payment is a contactless payment method that uses Near Field Communication technology to transfer payment information between two devices held close together. The transaction happens when customers tap or hold an NFC-enabled device like a smartphone, smartwatch, or contactless card near a compatible payment terminal.

The technology works through short-range radio waves that communicate within a few centimeters. When customers tap their phone to pay at your checkout, the NFC chip in their device exchanges encrypted payment data with your terminal's NFC reader. This exchange takes less than a second.

For example, when a customer at your store uses Google Pay or Apple Pay, they're using NFC payment. The phone doesn't transmit their actual card number to your terminal. Instead, it sends a one-time encrypted token specific to that transaction. Your terminal receives this token, validates it with the customer's bank, and approves the payment.

NFC payments work both for physical retail transactions and digital checkouts. For physical purchases at your store or showroom, customers tap their device on your terminal. For online purchases through your website, digital wallets using NFC technology can speed up checkout by auto-filling payment details securely.

How does NFC payment work?

NFC payment happens through a quick sequence of steps that prioritize both speed and security. The entire process completes in seconds at your checkout.

The process involves five main steps:

- Proximity detection: The customer's NFC-enabled device and your payment terminal must be within 4 centimeters of each other. When they bring their device close, the NFC chips detect each other and establish a connection.

- Token generation: Instead of sending the customer's actual card number, their device creates a unique one-time token for this specific transaction. This token can only be used once and becomes useless if intercepted.

- Data encryption: The token and transaction details get encrypted before transmission. This encryption scrambles the data so only authorized parties can read it.

- Authentication: The customer's device requires authentication through fingerprint, face recognition, or a PIN. This confirms they're authorizing the payment. Your terminal receives the encrypted token and sends it to the customer's bank.

- Authorization and confirmation: The customer's bank validates the token, checks their account balance, approves the transaction, and sends confirmation back to your terminal. Both the customer's device and your terminal screen display payment confirmed.

For instance, when a customer taps their phone at your checkout counter, the NFC chip activates, generates a token replacing their card number, encrypts the transaction data, waits for their fingerprint confirmation, and completes the authorization within two seconds.

The technology behind contactless NFC transactions ensures the customer's actual payment credentials never leave their device. Your terminal only receives temporary tokens that expire immediately after use.

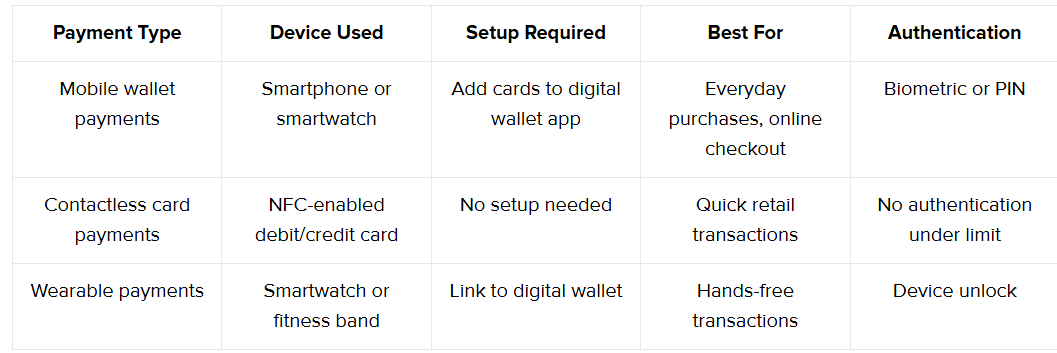

What are the types of NFC payments?

NFC payment technology works across different devices and scenarios. Each type serves specific use cases while maintaining the same security standards.

Let's look at each type in detail:

- Mobile wallet payments: Mobile wallets like Google Pay, Apple Pay, and Samsung Pay use the customer's smartphone NFC chip to make payments. Customers add their cards to the wallet app once, then tap their phone at your contactless terminal to pay.

For example, when an international customer visits your showroom, they can pay using Google Pay loaded with their home country card. The wallet stores multiple cards, lets them choose which one to use, and keeps a transaction history for their records.

- Contactless card payments: Many debit and credit cards now come with built-in NFC chips. These cards have a contactless symbol on them. Customers simply tap the card on your terminal without inserting or swiping.

For instance, a business customer's corporate credit card might support contactless payments. At your retail location, they can tap their card on your payment terminal instead of inserting it. Transactions under a certain limit often don't require PIN entry, making checkout even faster.

- Wearable payments: Smartwatches and fitness bands with NFC chips enable payments without customers pulling out their phone or wallet. Customers link the wearable to their digital wallet and tap it on your terminals.

A customer wearing an Apple Watch can pay for their purchase by tapping their wrist on your terminal. This works even if they left their phone elsewhere, ensuring the transaction still completes.

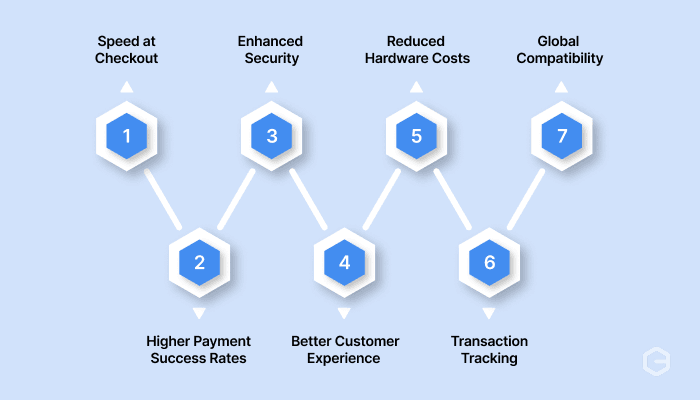

What are the benefits of NFC payment?

NFC payments offer practical advantages for both businesses and customers. These benefits highlight why contactless transactions are becoming the global standard.

- Speed at checkout: NFC transactions are complete in just a few seconds. Customers tap their device and move on. This speed reduces checkout lines and improves the customer experience significantly compared to traditional card insertion or cash handling.

- Higher payment success rates: Contactless payments have fewer failure points than traditional methods. There's no card reader malfunction from worn magnetic strips, no chip insertion errors, and no manual entry mistakes. For businesses, this means more successful transactions and fewer frustrated customers.

- Enhanced security: NFC uses tokenization to replace real card numbers with one-time codes. Even if someone intercepts the data, they get a useless token. Combined with device authentication through fingerprints or face recognition, NFC payments are more secure than magnetic stripe cards.

- Better customer experience: Modern customers expect fast, frictionless payments. Offering NFC payment shows your business keeps pace with customer expectations. This matters especially when serving international customers familiar with tap-to-pay in their home markets.

- Reduced hardware costs: NFC eliminates the need for separate card readers for different payment types. One contactless terminal handles cards, phones, and wearables. This simplifies your payment setup and reduces maintenance.

- Transaction tracking: Digital wallets providing NFC payments automatically record transaction details. For business expenses, this creates an instant digital trail. You can track where money goes without manual record-keeping.

- Global compatibility: NFC payment standards are consistent worldwide. A customer from Europe using Apple Pay can pay at your Indian store the same way they pay at home. This consistency helps businesses serving international customers.

How is the security of NFC payments?

NFC payment security relies on multiple protective layers working together. The technology prevents fraud at every step, making it more secure than traditional magnetic stripe cards while maintaining the speed customers expect.

Here's how NFC payments protect your business and customers:

- Tokenization replaces card data: When customers add cards to digital wallets, the system creates a unique device account number that replaces the real card number. This token is transmitted during payments, so even if transaction data is intercepted, fraudsters only get a useless token.

- Encryption secures transmitted data: All data sent between the customer's device and your payment terminal gets encrypted. This encrypted information looks like random characters to anyone trying to read it without the decryption key.

- Device authentication confirms identity: Customers must unlock their device using fingerprint, face scan, or PIN before the payment process. This prevents unauthorized transactions even if someone steals the device.

- Short-range limits interception: NFC only works within 4 centimeters, making it extremely difficult for fraudsters to position readers close enough to intercept data during active transactions.

- One-time tokens expire immediately: Each transaction generates a fresh token that includes specific transaction details. If somehow captured, the token cannot be reused for another purchase or modified for different amounts.

- Banks monitor for fraud patterns: Payment networks and banks monitor NFC transactions for suspicious activity. Unusual spending triggers alerts just like traditional card payments.

The combination of tokenization, encryption, device authentication, limited range, and one-time use makes NFC payments more secure than magnetic stripe cards. Your customers get protection without sacrificing the convenience of fast checkout.

How to accept NFC payments?

Accepting NFC payments at your business requires compatible hardware and integration with a payment provider. The setup process is straightforward and can be completed quickly.

Here's what you need to start accepting contactless payments:

- Get NFC-enabled payment terminals: Your business needs payment terminals with built-in NFC readers. These terminals display the contactless payment symbol (four curved lines). Most modern payment terminals from providers include NFC capability by default.

When selecting terminals, look for devices that support multiple payment types. The terminal should accept contactless cards, mobile wallets like Google Pay and Apple Pay, and wearable devices. This ensures you can serve customers regardless of their preferred payment method.

- Partner with a payment service provider: Choose a payment provider that supports NFC transactions and offers competitive rates. The provider handles the backend processing, connects to card networks, and manages settlements to your account.

For businesses accepting international payments, select a provider with global payment infrastructure.

- Integrate with your point of sale system: Connect your NFC-enabled terminal to your existing point of sale system. Most modern terminals integrate through simple API connections or plug-and-play solutions.

The integration allows transaction data to flow between the terminal and your inventory, accounting, and reporting systems. When a customer taps to pay, the sale automatically updates your records.

- Train your staff: Brief your team on how contactless payments work. They should know to prompt customers to tap their card or device, confirm the transaction amount is visible before processing, and handle the occasional authentication requirement for larger purchases.

Staff should also know that NFC terminals work the same way for cards and mobile wallets. The customer simply taps regardless of payment method.

- Display contactless payment symbols: Place signs or stickers showing you accept contactless payments. Display the NFC symbol at checkout counters and entrance areas. This signals to customers they can use their preferred tap-to-pay method.

For instance, if you run an export business with a retail showroom, displaying Apple Pay and Google Pay logos alongside the contactless symbol tells international visitors they can pay using familiar methods from their home countries.

- Test the setup: Before going live, test the terminal with different payment methods. Try contactless cards, mobile wallets, and wearable devices to ensure everything processes correctly.

Run test transactions to verify the terminal connects properly, processes payments within seconds, and sends confirmation to both the terminal display and your POS system.

Get paid globally and scale your business with PayGlocal

Modern payment technology like NFC creates the fast, frictionless checkout experiences customers expect. But for businesses accepting payments from global customers, offering modern checkout is just one piece of the puzzle.

You also need to accept payments in multiple currencies, provide local payment methods customers trust, manage compliance across borders, and maintain high payment success rates. Doing all this while keeping costs transparent and operations simple requires the right payment partner.

PayGlocal provides a complete payment solution designed for Indian businesses growing globally. Here's how we help:

- Dynamic checkout: Create seamless checkout flows that accept global cards and local payment methods through one unified interface your customers trust.

- Global payment methods: Offer 40+ local payment methods your international customers prefer, from digital wallets to bank transfers.

- Recurring payments: Handle subscriptions and recurring billing with network-compliant solutions that work across borders.

- Multi-currency accounts: Collect payments in 33+ currencies from 180+ countries with local accounts in USD, GBP, EUR, and CAD.

- One platform: Manage all payment types, view transaction details, download compliance documents, and track fund status from a single dashboard.

PayGlocal helps you accept modern payment methods that customers expect while handling the complexity of cross-border commerce. You pay only when you transact with zero setup fees, no platform charges, and transparent pricing.

Final thoughts

NFC payment technology has changed how people expect to pay. The tap-and-go experience is now standard in markets worldwide. For businesses, offering contactless payment options means meeting customer expectations and reducing friction at the most critical moment of the buying process.

The security, speed, and convenience of NFC payments benefit both customers and businesses. Customers get faster checkouts and better protection. Businesses see higher success rates and improved customer satisfaction.

If you're doing business with customers across borders, modern payment acceptance goes beyond just NFC. You need a payment stack that handles multiple currencies, offers local payment methods, maintains compliance, and keeps approval rates high.

Get started with PayGlocal today and give your global customers the seamless payment experience they expect.