Running a business comes with its own challenges. Some days you're waiting for client payments, other times you need immediate funds for inventory or operations. Businesses are increasingly turning to banking credit facilities to manage their processes.

In fact, according to recent data, in India, the credit disbursement to priority sectors, including agriculture, MSME, and social infrastructure, has grown significantly over the years, from just ₹23 lakh crores in 2019 to ₹42.7 lakh crores in 2024.

Banking solutions like OD (Overdrafts) can solve cash flow challenges. But what exactly does OD mean in banking, and how does it work? Let’s find out!

Key Takeaways:

The full form of OD is Overdraft, a credit facility offered by banks that allows account holders to withdraw money beyond their available account balance. You can think of it as a pre-approved loan that activates automatically when you need it.

When your current account balance drops to zero, an overdraft facility lets you continue making payments up to a predetermined limit. For example, if you have a ₹5 lakh overdraft limit and your account balance is ₹50,000, you can actually access up to ₹5.5 lakh for business operations.

The key advantage is flexibility. You only pay interest on the amount you actually use, not the entire approved limit. This makes overdrafts particularly useful for businesses dealing with seasonal fluctuations or irregular payment cycles.

Banks approve overdraft limits based on your business profile, cash flow patterns, and creditworthiness. Once approved, the facility works seamlessly with your existing current account. Here's how the typical process works:

Banks offer different types of overdraft facilities to match various business needs and risk profiles. Here's how they compare across key factors:

Each type serves different business needs and financial situations.

Secured overdrafts require collateral like fixed deposits, property, or other assets. Banks typically offer higher limits and lower interest rates because the collateral reduces their risk.

For example, if you pledge a ₹10 lakh fixed deposit, banks might approve an overdraft limit of ₹8-9 lakh at competitive interest rates. This type works well for established businesses with substantial assets.

Unsecured overdrafts don't require collateral but depend heavily on your credit score, business cash flow, and banking relationship. Limits are usually lower, and interest rates are higher compared to secured options.

Banks often offer unsecured overdrafts to businesses with consistent monthly turnover and good payment history. Limits typically range from ₹1-50 lakh based on your business profile.

Banks offer salary account holders overdraft facilities based on their monthly income. These are typically smaller limits designed for personal or small business use.

For instance, if your monthly salary is ₹1 lakh, banks might approve an overdraft limit of ₹2-3 lakh. Interest rates are usually competitive since salary accounts indicate stable income.

Specifically designed for business current accounts, these overdrafts consider business cash flow, GST returns, and operational needs. They often come with additional features like sweep-in facilities and flexible renewal terms.

Business overdrafts can handle larger limits and offer customized repayment schedules aligned with your business cycles.

Overdraft facilities offer several advantages that make them popular among businesses managing working capital needs. Some of the key benefits include:

Many business owners wonder whether to choose an overdraft or a personal loan for their funding needs. Both serve different purposes and work differently. Here's how they compare:

The choice depends on your specific business needs and cash flow patterns. Overdrafts work better for businesses with irregular income or seasonal cash flow gaps. You only pay for what you use and can repay anytime without penalties.

Personal loans suit businesses needing a fixed amount for specific purposes like equipment purchase or expansion, where you prefer predictable EMI payments over a set period.

Banks typically charge overdraft interest rates ranging from 12-18% annually for secured facilities and 15-22% for unsecured ones. Rates depend on your credit profile, business relationship with the bank, and market conditions.

Interest is calculated daily on the outstanding overdraft amount. However, banks may charge processing fees (₹1,000-₹10,000), annual maintenance charges, and documentation fees. Some banks also charge penalties for exceeding the approved limit or non-compliance with renewal terms.

While overdraft rates might seem higher than term loans, remember you only pay for what you use. This often makes overdrafts more cost-effective for short-term working capital needs compared to taking unnecessary loans.

Traditional overdraft facilities work well for domestic operations, but they often fall short when you're scaling internationally. Currency conversion delays, high FX charges, and complex compliance requirements can limit your growth potential.

If you're collecting payments from international clients or expanding to global markets, you need a solution like PayGlocal that goes beyond traditional banking limitations.

Here's how PayGlocal improves your payment operations:

Whether you're a freelancer receiving payments from global platforms or an exporter managing international invoices, PayGlocal helps you access funds faster and more efficiently than traditional payment solutions.

The overdraft facility is an essential financial tool for managing short-term cash flow needs and maintaining business operations during payment delays. Knowing how OD works, its types, and cost structure helps you make informed decisions about working capital management.

However, for businesses operating internationally or planning global expansion, traditional banking solutions like overdrafts may not provide the speed, transparency, and cost-effectiveness needed for competitive growth. Modern payment solutions like PayGlocal offer better solutions for international cash flow management with faster processing and lower costs.

The best businesses are already moving beyond traditional payment limitations to access global payments more efficiently. Get started with PayGlocal today and significantly enhance how you collect and manage international payments.

In fact, according to recent data, in India, the credit disbursement to priority sectors, including agriculture, MSME, and social infrastructure, has grown significantly over the years, from just ₹23 lakh crores in 2019 to ₹42.7 lakh crores in 2024.

Banking solutions like OD (Overdrafts) can solve cash flow challenges. But what exactly does OD mean in banking, and how does it work? Let’s find out!

Key Takeaways:

- OD means Overdraft: A flexible credit line that lets you withdraw beyond your account balance up to a pre-approved limit.

- Interest on usage only: You pay interest only on the amount you use, not the entire approved limit.

- Business-friendly features: Includes automatic renewal, flexible repayment, and helps maintain business continuity during cash flow gaps.

- Modern alternatives available: PayGlocal offers advanced payment collection solutions that help businesses reduce dependency on traditional credit facilities through faster international payment processing.

What is OD in banking?

The full form of OD is Overdraft, a credit facility offered by banks that allows account holders to withdraw money beyond their available account balance. You can think of it as a pre-approved loan that activates automatically when you need it.

When your current account balance drops to zero, an overdraft facility lets you continue making payments up to a predetermined limit. For example, if you have a ₹5 lakh overdraft limit and your account balance is ₹50,000, you can actually access up to ₹5.5 lakh for business operations.

The key advantage is flexibility. You only pay interest on the amount you actually use, not the entire approved limit. This makes overdrafts particularly useful for businesses dealing with seasonal fluctuations or irregular payment cycles.

How does an overdraft facility work?

Banks approve overdraft limits based on your business profile, cash flow patterns, and creditworthiness. Once approved, the facility works seamlessly with your existing current account. Here's how the typical process works:

- Account setup: Your bank evaluates your business financials and approves an overdraft limit. This limit can range from ₹1 lakh to higher amounts, depending on your business size and banking relationship.

- Automatic activation: When you make payments that exceed your account balance, the overdraft automatically kicks in to cover the shortfall. No separate loan application needed.

- Interest calculation: Banks charge interest only on the amount you use, calculated daily. For instance, if you use ₹2 lakh from a ₹10 lakh limit for 15 days, you pay interest only on ₹2 lakh for those 15 days.

- Flexible repayment: You can repay the overdraft amount anytime. Once you deposit money, it first goes toward clearing the overdraft balance, reducing your interest burden immediately.

- Renewal process: Most overdraft facilities come with annual renewal terms, though some banks offer automatic renewal based on your account performance.

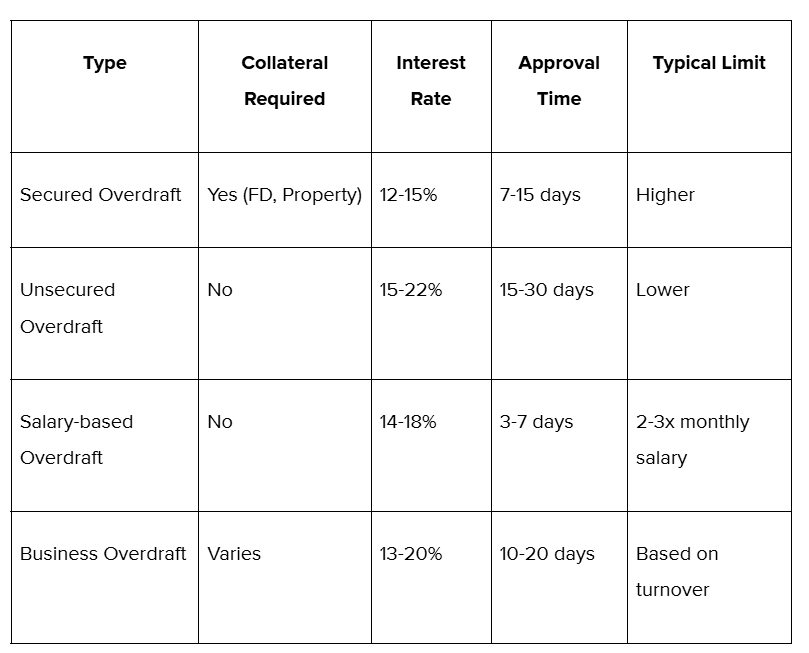

What are the types of overdraft facilities?

Banks offer different types of overdraft facilities to match various business needs and risk profiles. Here's how they compare across key factors:

Each type serves different business needs and financial situations.

1. Secured overdraft

Secured overdrafts require collateral like fixed deposits, property, or other assets. Banks typically offer higher limits and lower interest rates because the collateral reduces their risk.

For example, if you pledge a ₹10 lakh fixed deposit, banks might approve an overdraft limit of ₹8-9 lakh at competitive interest rates. This type works well for established businesses with substantial assets.

2. Unsecured overdraft

Unsecured overdrafts don't require collateral but depend heavily on your credit score, business cash flow, and banking relationship. Limits are usually lower, and interest rates are higher compared to secured options.

Banks often offer unsecured overdrafts to businesses with consistent monthly turnover and good payment history. Limits typically range from ₹1-50 lakh based on your business profile.

3. Salary-based overdraft

Banks offer salary account holders overdraft facilities based on their monthly income. These are typically smaller limits designed for personal or small business use.

For instance, if your monthly salary is ₹1 lakh, banks might approve an overdraft limit of ₹2-3 lakh. Interest rates are usually competitive since salary accounts indicate stable income.

4. Business overdraft

Specifically designed for business current accounts, these overdrafts consider business cash flow, GST returns, and operational needs. They often come with additional features like sweep-in facilities and flexible renewal terms.

Business overdrafts can handle larger limits and offer customized repayment schedules aligned with your business cycles.

What are the benefits of overdraft facilities?

Overdraft facilities offer several advantages that make them popular among businesses managing working capital needs. Some of the key benefits include:

- Immediate access to funds: No lengthy approval process once the facility is set up. Funds are available instantly when your account balance drops below zero.

- Interest only on usage: Unlike term loans, where you pay interest on the entire amount, overdrafts charge interest only on what you actually use.

- Flexible repayment: No fixed EMIs or repayment schedules. You can repay anytime, and interest calculation stops immediately.

- Business continuity: Helps maintain operations during cash flow gaps without disrupting supplier payments or operational expenses.

- Automatic renewal: Most facilities renew annually based on your account performance, ensuring continued access to working capital.

- Multiple withdrawal options: Access funds through cheques, online transfers, or debit cards, making it convenient for various business needs.

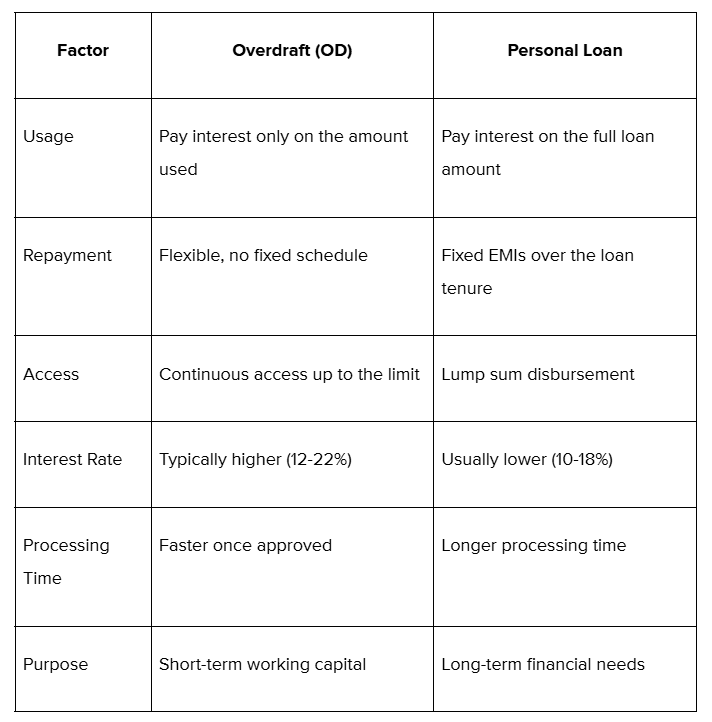

What is the difference between an OD and a personal loan?

Many business owners wonder whether to choose an overdraft or a personal loan for their funding needs. Both serve different purposes and work differently. Here's how they compare:

The choice depends on your specific business needs and cash flow patterns. Overdrafts work better for businesses with irregular income or seasonal cash flow gaps. You only pay for what you use and can repay anytime without penalties.

Personal loans suit businesses needing a fixed amount for specific purposes like equipment purchase or expansion, where you prefer predictable EMI payments over a set period.

What are the overdraft interest rates and charges?

Banks typically charge overdraft interest rates ranging from 12-18% annually for secured facilities and 15-22% for unsecured ones. Rates depend on your credit profile, business relationship with the bank, and market conditions.

Interest is calculated daily on the outstanding overdraft amount. However, banks may charge processing fees (₹1,000-₹10,000), annual maintenance charges, and documentation fees. Some banks also charge penalties for exceeding the approved limit or non-compliance with renewal terms.

While overdraft rates might seem higher than term loans, remember you only pay for what you use. This often makes overdrafts more cost-effective for short-term working capital needs compared to taking unnecessary loans.

Accept faster global payments without complex charges

Traditional overdraft facilities work well for domestic operations, but they often fall short when you're scaling internationally. Currency conversion delays, high FX charges, and complex compliance requirements can limit your growth potential.

If you're collecting payments from international clients or expanding to global markets, you need a solution like PayGlocal that goes beyond traditional banking limitations.

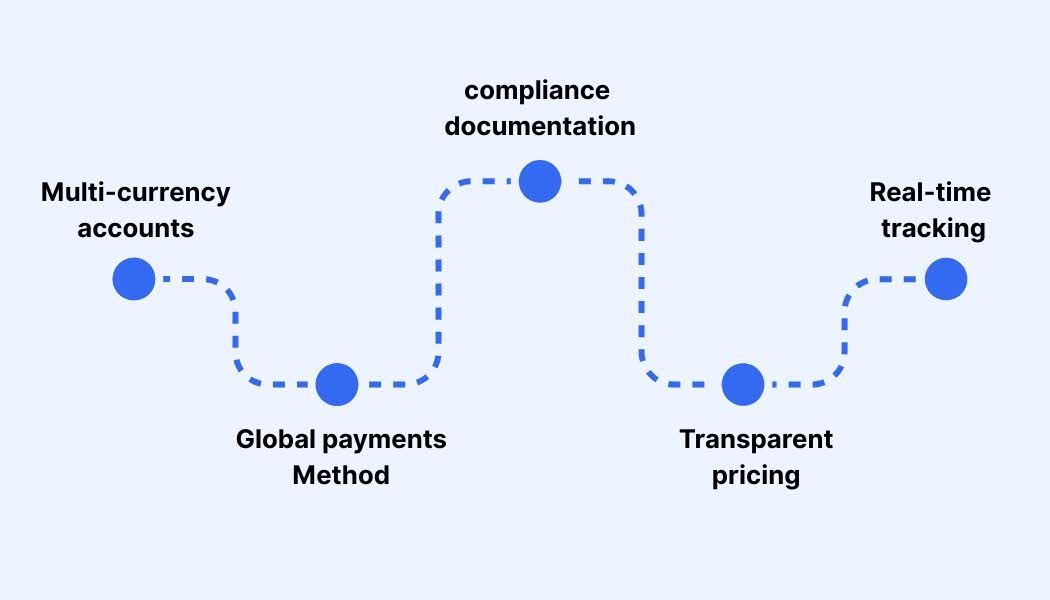

Here's how PayGlocal improves your payment operations:

- Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details, making it easier for your international clients to send payments faster.

- Global payment methods: Accept payments through 40+ international payment methods, reducing dependency on traditional credit facilities for cash flow management.

- Instant compliance documentation: Get instant FIRC generation right after payment settlement, making your export documentation faster without banking delays.

- Transparent pricing: Pay only per transaction with no hidden charges, monthly fees, or complex payment calculations.

- Real-time tracking: Monitor all international payments with instant notifications, helping you plan cash flow better than traditional payment processes.

Whether you're a freelancer receiving payments from global platforms or an exporter managing international invoices, PayGlocal helps you access funds faster and more efficiently than traditional payment solutions.

Final thoughts

The overdraft facility is an essential financial tool for managing short-term cash flow needs and maintaining business operations during payment delays. Knowing how OD works, its types, and cost structure helps you make informed decisions about working capital management.

However, for businesses operating internationally or planning global expansion, traditional banking solutions like overdrafts may not provide the speed, transparency, and cost-effectiveness needed for competitive growth. Modern payment solutions like PayGlocal offer better solutions for international cash flow management with faster processing and lower costs.

The best businesses are already moving beyond traditional payment limitations to access global payments more efficiently. Get started with PayGlocal today and significantly enhance how you collect and manage international payments.