Do international payments take too much of your team's time? Someone creates invoices manually, another person follows up on pending payments, and your finance team spends hours matching received funds to open invoices. This workflow might work for a few payments per month, but it will quickly break down as your business grows.

Cross-border payment automation fixes this by handling everything from invoicing to settlement in one system. Businesses have already started shifting towards automation, with data showing that automated systems are now expected to handle about $1 trillion in commerce spending. This represents half of all e-commerce transactions happening today.

This guide covers in detail what cross-border payment automation is, how it works, what features matter, and how to choose the best platform for your business needs.

Cross-border payment automation is a system that handles international money movement automatically. It takes care of invoicing, FX conversion, compliance checks, payment routing, and reconciliation without manual input at each step.

Instead of creating invoices manually, chasing payments, and reconciling transactions one by one, you set up automated workflows. The platform generates invoices, sends them to clients, accepts payments in multiple currencies, converts funds at transparent rates, and updates your accounting system in real time.

Consider an Indian SaaS firm scaling in the US. Automation means that when a $500 subscription is paid, the system doesn't just move money; it generates the digital FIRC, updates the ledger for the finance team, and ensures the transaction is ready for EDPMS reconciliation without a single manual email to a bank manager.

Automation gives you complete visibility into where each payment stands and reduces processing time from weeks to days.

Automation doesn't just clean up your spreadsheet; it reclaims your working capital. Beyond the speed, the real benefit is the shift from reactive crisis management to proactive scaling. When your payment rails are automated, you stop fighting the system and start using it to your advantage.

Here is how automating cross-border payments changes your bottom line:

Tip: Track your current time spent on payment tasks for one month before implementing automation. This gives you a clear baseline to measure improvement and justify the platform cost to stakeholders.

Cross-border payment automation serves businesses of all sizes doing international commerce. The specific automation features you need depend on your business model, but the core benefits apply across industries.

Here's who benefits most from automation:

The common thing across all these businesses is volume and complexity. Once you're processing more than a handful of international payments per month, manual work becomes expensive and error-prone. Automation scales effortlessly whether you process 10 payments or 10,000.

Not all automation platforms work the same way. Some focus on invoicing, others on compliance, and the best ones handle end-to-end workflows. The features below separate basic tools from complete solutions.

Here are the capabilities you should look for:

The right combination depends on your workflow. For instance, a SaaS business needs strong recurring billing support, while an exporter prioritizes multi-currency accounts and FIRC generation. Pick platforms where features connect into one workflow rather than requiring manual steps between them.

Note: Before choosing a platform, map your current payment workflow step by step. Identify where manual work happens most often and prioritize features that automate those specific bottlenecks.

Cross-border payment automation comes in different models based on how you collect payments and where the integration happens. The type you choose affects your technical requirements, control over customer experience, and operational flexibility.

Here's how the main automation models compare:

Note: Your choice affects more than just technical integration. Consider settlement timing, fees, compliance requirements, and how much control you need over customer experience before selecting a model.

Cross-border payment automation connects your business systems to international banking networks through APIs. These APIs enable direct communication between your invoicing software, payment gateways, and banking partners. Here's how the automated workflow operates:

The key difference of cross-border payment automation from traditional methods is that everything happens in one connected system.

Tip: Choose platforms that offer API testing environments so you can validate the integration with your existing systems before going live with real transactions.

Cross-border payment automation runs on several technology layers working together. You don't need to become a technical expert, but knowing what powers these systems helps you evaluate platforms effectively. Here's the technology foundation that makes automation possible:

Application Programming Interfaces (API) let different software systems connect to each other automatically. When a payment happens, APIs send data between your accounting software, the payment platform, and banking networks. Webhooks push real-time updates to your system the moment a payment status changes.

These are the actual pathways money travels through. Card networks like Visa and Mastercard, SWIFT for international transfers, and real-time payment systems serve as the infrastructure. Good automation platforms connect to multiple networks and choose the best path for each transaction.

Payment platforms run on cloud servers that can handle thousands of transactions simultaneously. This means the system stays available 24/7, scales automatically when transaction volumes spike, and recovers quickly if something fails.

Smart routing technology analyzes each transaction and picks the most efficient path based on cost, speed, and success probability. For example, a USD payment to a US client might route through a local US network instead of SWIFT to save fees and time.

End-to-end encryption protects payment data as it moves between systems. Tokenization replaces sensitive card details with random tokens, so actual card numbers never sit in your database. Multi-factor authentication adds layers of protection to platform access.

These systems screen transactions against sanctions lists, perform KYC checks, and flag suspicious patterns automatically. They run in milliseconds as part of each transaction without slowing down the payment flow.

For instance, when your UK client pays an invoice, the API receives the payment request, the routing algorithm selects the optimal network path, encryption protects the data in transit, the compliance engine screens the transaction, and webhooks notify your accounting system the moment funds settle.

Modern payment platforms keep the complexity behind simple interfaces. You see a dashboard and payment buttons, but advanced technology handles everything behind the scenes to make payments fast, secure, and compliant.

Even with automation, some challenges need attention. Knowing them upfront helps you choose platforms with built-in solutions instead of discovering problems after you've already integrated. Here's what businesses face and how to handle them:

The key is choosing a platform that handles these challenges upfront rather than discovering them after you've already integrated.

Cross-border payment automation continues to evolve rapidly. New technologies and regulatory changes are making international payments faster, cheaper, and more accessible. Here are the trends shaping the industry right now:

Tip: When evaluating platforms, ask about their technology roadmap and how often they add new payment methods or network connections. Platforms that innovate regularly will serve you better as your business grows into new markets.

Choosing the right platform depends on your business model, payment volumes, and growth plans. The wrong choice locks you into expensive contracts or forces workarounds when you scale. Here's what to evaluate:

If you need working capital quickly, look for platforms offering 24-hour settlements. Check if settlement timing varies by currency or payment method. Some platforms settle USD faster than EUR or GBP.

The platform should show exact costs upfront, including transaction fees, FX margins, and any additional charges. Avoid platforms with hidden markup or monthly fees unless your volume justifies the cost. Ask for sample invoices showing real fees on actual transactions.

The platform must connect to your existing accounting software, CRM, or e-commerce system. API quality matters here. Good APIs mean seamless data flow. Poor APIs mean manual workarounds. Request API documentation before committing and check if webhook support exists for real-time updates.

If most clients pay in USD and EUR, you need strong support for those currencies with competitive rates. Multi-currency accounts let you hold funds and reduce conversion frequency. Check if the platform provides local account details in target markets so clients can pay domestically.

For Indian businesses, automatic FIRC generation is essential. The platform should also handle international compliance requirements if you're dealing with regulated industries. Ask how long compliance documentation takes to generate after settlement.

Can customers pay via cards, bank transfers, and local payment methods? More options mean higher success rates and better customer experience. Check which specific payment methods are available in your target markets.

When a payment fails or a client has questions, you need responsive support. Check if the platform offers dedicated account management or just email support. Test response times during the sales process as an indicator of post-sale support quality.

The right platform fits your specific workflow without forcing you to change how you operate.

Manual cross-border payments create bottlenecks that slow down your business. You wait days for settlements, spend hours on reconciliation, and lose money to hidden fees. If you're growing internationally, you need a system built for automation from the ground up.

PayGlocal gives you a complete payment automation platform built for cross-border commerce. You get local accounts in major currencies, automated compliance, and real-time tracking with seamless integration options for your existing systems. Here's what you get:

PayGlocal handles the complexity of cross-border payment automation so you can focus on growing your business. You get transparent pricing, instant notifications, and faster settlements with transparent pricing.

Cross-border payment automation takes the manual work out of international money movement. You get faster settlements, lower costs, and complete visibility into where your money is at all times.

The right platform connects to your existing systems, handles compliance automatically, and gives customers payment options they trust. This means fewer failed transactions, less time spent on reconciliation, and more predictable cash flow for your business.

Automation isn't optional anymore for businesses doing cross-border commerce. Your competitors are already using these systems to move faster and operate more efficiently. The longer you wait, the more manual work adds up and the harder it becomes to catch up.

Ready to collect globally and settle locally without the usual friction? Get started with PayGlocal today and see what automated cross-border payments can do for your business.

Cross-border payment automation fixes this by handling everything from invoicing to settlement in one system. Businesses have already started shifting towards automation, with data showing that automated systems are now expected to handle about $1 trillion in commerce spending. This represents half of all e-commerce transactions happening today.

This guide covers in detail what cross-border payment automation is, how it works, what features matter, and how to choose the best platform for your business needs.

Key Takeaways

- Automated workflows: Cross-border payment automation handles invoicing, FX conversion, compliance, and reconciliation automatically without manual input at each step.

- Multiple automation models: Choose between direct integration for full control, hosted checkout for quick setup, or platform aggregation based on your technical capabilities and business needs.

- Technology foundation: APIs, payment networks, cloud infrastructure, and routing algorithms work together to make payments fast, secure, and compliant behind simple interfaces.

- Platform evaluation: Choose based on settlement speed, fee transparency, integration capabilities, and multi-currency support for your specific business needs.

- Faster global payments advantage: PayGlocal offers multi-currency accounts, API integration, automated compliance, and instant Foreign Inward Remittance Certificate (FIRC) generation for Indian businesses doing global commerce.

What is Cross-Border Payment Automation?

Cross-border payment automation is a system that handles international money movement automatically. It takes care of invoicing, FX conversion, compliance checks, payment routing, and reconciliation without manual input at each step.

Instead of creating invoices manually, chasing payments, and reconciling transactions one by one, you set up automated workflows. The platform generates invoices, sends them to clients, accepts payments in multiple currencies, converts funds at transparent rates, and updates your accounting system in real time.

Consider an Indian SaaS firm scaling in the US. Automation means that when a $500 subscription is paid, the system doesn't just move money; it generates the digital FIRC, updates the ledger for the finance team, and ensures the transaction is ready for EDPMS reconciliation without a single manual email to a bank manager.

Automation gives you complete visibility into where each payment stands and reduces processing time from weeks to days.

What are the Benefits of Automating Cross-Border Payments?

Automation doesn't just clean up your spreadsheet; it reclaims your working capital. Beyond the speed, the real benefit is the shift from reactive crisis management to proactive scaling. When your payment rails are automated, you stop fighting the system and start using it to your advantage.

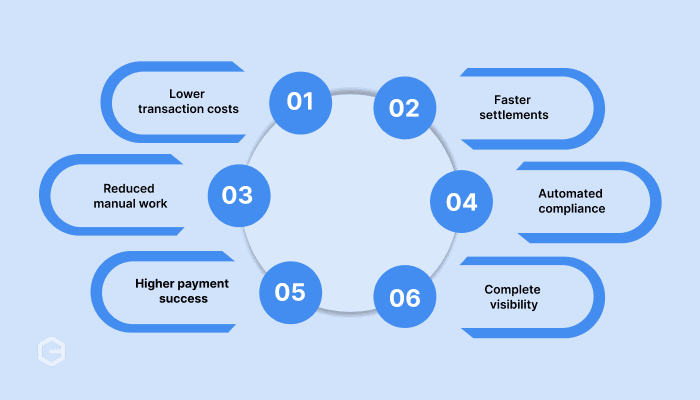

Here is how automating cross-border payments changes your bottom line:

- Lower transaction costs: You avoid hidden fees from correspondent banks because automated platforms use direct banking connections. FX rates are transparent, and you see exactly what you'll receive before confirming any transaction.

- Faster settlements: Instead of waiting weeks for international wire transfers, automated platforms settle funds in just a few days. Some platforms offer same-day settlements for specific currency pairs.

- Reduced manual work: You eliminate manual invoice creation, payment tracking, follow-ups, and reconciliation. Finance teams can focus on growth instead of administrative tasks.

- Automated compliance: The system handles regulations checks, maintains required documentation, and generates audit trails. For Indian exporters, this includes automatic FIRC generation after each settlement.

- Higher payment success: Local payment methods and optimized routing increase approval rates because customers pay through familiar channels, and banks recognize legitimate transactions more easily.

- Complete visibility: Real-time dashboards show exactly where each payment stands. You know when invoices are sent, when payments are received, and when funds will settle.

Tip: Track your current time spent on payment tasks for one month before implementing automation. This gives you a clear baseline to measure improvement and justify the platform cost to stakeholders.

Who Uses Cross-Border Payment Automation?

Cross-border payment automation serves businesses of all sizes doing international commerce. The specific automation features you need depend on your business model, but the core benefits apply across industries.

Here's who benefits most from automation:

- SaaS and subscription businesses: Automate recurring billing, subscription management, and failed payment retries across multiple currencies and time zones.

- E-commerce exporters: Connect your Shopify or WooCommerce store directly to multi-currency checkout, automated reconciliation, and local payment methods.

- Freelancers and agencies: Send professional invoices, collect payments via simple payment links, and track who paid without managing international bank transfers manually.

- B2B service providers: Handle invoice-to-cash workflows, payment reminders, partial payments, and reconciliation across multiple client projects without spreadsheets.

- Manufacturing and goods exporters: Generate invoices, collect payments, and produce required export documents like FIRC automatically for high transaction volumes.

- Travel and hospitality businesses: Process booking payments in real time, handle cancellations and refunds, and confirm bookings instantly without manual verification delays.

- Digital marketplaces: Collect payments from customers and distribute funds to sellers automatically with split payments, escrow holds, and scheduled settlements.

The common thing across all these businesses is volume and complexity. Once you're processing more than a handful of international payments per month, manual work becomes expensive and error-prone. Automation scales effortlessly whether you process 10 payments or 10,000.

What are the Key Features of Payment Automation Platforms?

Not all automation platforms work the same way. Some focus on invoicing, others on compliance, and the best ones handle end-to-end workflows. The features below separate basic tools from complete solutions.

Here are the capabilities you should look for:

- Automated invoicing: The platform pulls customer and transaction data from your system, generates invoices automatically, and sends them to clients. You set the rules once, and invoices go out on schedule without manual intervention.

- Multi-currency support: Accept payments in multiple currencies like USD, GBP, EUR, and CAD. This reduces conversion costs and gives clients familiar payment options.

- API integrations: Direct integration with your accounting software, ERP systems, or e-commerce platforms. This eliminates double entry and enables real-time data sync across all systems.

- Automated compliance: Built-in KYC, sanctions, and other necessary screening that runs automatically on every transaction. The system flags suspicious activity and maintains audit trails for regulators.

- Payment routing: The platform selects the most efficient path for each transaction based on cost, speed, and success probability. This bypasses unnecessary intermediary banks and reduces fees.

- Real-time tracking: Complete visibility into payment status from invoice generation to settlement. You get notifications at each step, and clients can track their payments too.

- Auto-reconciliation: The system matches incoming payments to invoices automatically and updates your accounting records. This reduces reconciliation time from hours to minutes.

The right combination depends on your workflow. For instance, a SaaS business needs strong recurring billing support, while an exporter prioritizes multi-currency accounts and FIRC generation. Pick platforms where features connect into one workflow rather than requiring manual steps between them.

Note: Before choosing a platform, map your current payment workflow step by step. Identify where manual work happens most often and prioritize features that automate those specific bottlenecks.

What are the Different Cross-Border Payment Automation Models?

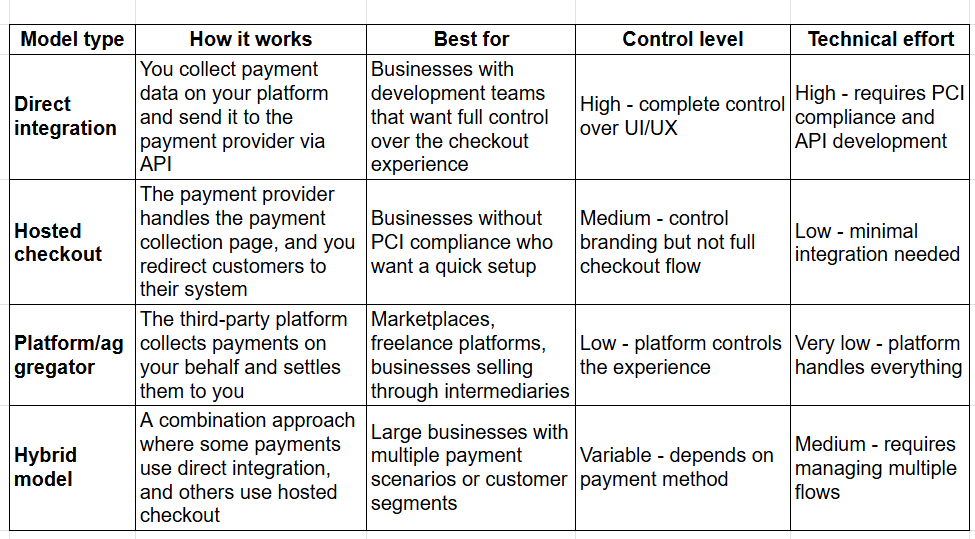

Cross-border payment automation comes in different models based on how you collect payments and where the integration happens. The type you choose affects your technical requirements, control over customer experience, and operational flexibility.

Here's how the main automation models compare:

Note: Your choice affects more than just technical integration. Consider settlement timing, fees, compliance requirements, and how much control you need over customer experience before selecting a model.

How Does Cross-Border Payment Automation Work?

Cross-border payment automation connects your business systems to international banking networks through APIs. These APIs enable direct communication between your invoicing software, payment gateways, and banking partners. Here's how the automated workflow operates:

- Invoice generation: Your accounting software or payment platform creates an invoice automatically using customer and transaction data from your system of record.

- Payment initiation: The system sends the invoice to your client via email or a payment link with multiple payment options.

- Payment collection: Your client pays using their preferred method, such as a credit card, local bank transfer, or digital wallet.

- Automated routing: The platform selects the most efficient payment path based on cost, speed, and success probability.

- Currency conversion: If needed, the system converts currency at transparent rates and applies FX fees upfront.

- Compliance screening: Built-in KYC, regulations, and sanctions checks run automatically on every transaction.

- Settlement: Funds are deposited into your account with automated notifications at each step.

- Reconciliation: The platform matches payments to invoices and updates your accounting records automatically.

The key difference of cross-border payment automation from traditional methods is that everything happens in one connected system.

Tip: Choose platforms that offer API testing environments so you can validate the integration with your existing systems before going live with real transactions.

What Technology Powers Cross-Border Payment Automation?

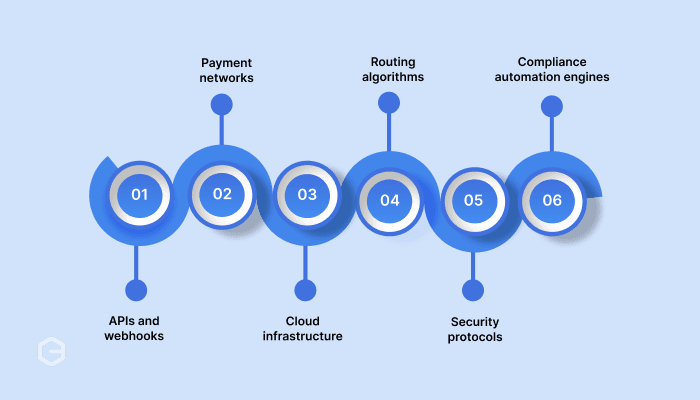

Cross-border payment automation runs on several technology layers working together. You don't need to become a technical expert, but knowing what powers these systems helps you evaluate platforms effectively. Here's the technology foundation that makes automation possible:

APIs and Webhooks

Application Programming Interfaces (API) let different software systems connect to each other automatically. When a payment happens, APIs send data between your accounting software, the payment platform, and banking networks. Webhooks push real-time updates to your system the moment a payment status changes.

Payment Networks

These are the actual pathways money travels through. Card networks like Visa and Mastercard, SWIFT for international transfers, and real-time payment systems serve as the infrastructure. Good automation platforms connect to multiple networks and choose the best path for each transaction.

Cloud Infrastructure

Payment platforms run on cloud servers that can handle thousands of transactions simultaneously. This means the system stays available 24/7, scales automatically when transaction volumes spike, and recovers quickly if something fails.

Routing Algorithms

Smart routing technology analyzes each transaction and picks the most efficient path based on cost, speed, and success probability. For example, a USD payment to a US client might route through a local US network instead of SWIFT to save fees and time.

Security Protocols

End-to-end encryption protects payment data as it moves between systems. Tokenization replaces sensitive card details with random tokens, so actual card numbers never sit in your database. Multi-factor authentication adds layers of protection to platform access.

Compliance Automation Engines

These systems screen transactions against sanctions lists, perform KYC checks, and flag suspicious patterns automatically. They run in milliseconds as part of each transaction without slowing down the payment flow.

For instance, when your UK client pays an invoice, the API receives the payment request, the routing algorithm selects the optimal network path, encryption protects the data in transit, the compliance engine screens the transaction, and webhooks notify your accounting system the moment funds settle.

Modern payment platforms keep the complexity behind simple interfaces. You see a dashboard and payment buttons, but advanced technology handles everything behind the scenes to make payments fast, secure, and compliant.

What are the Common Challenges with Cross-Border Payment Automation?

Even with automation, some challenges need attention. Knowing them upfront helps you choose platforms with built-in solutions instead of discovering problems after you've already integrated. Here's what businesses face and how to handle them:

- Currency volatility and FX risk: Exchange rates can shift between invoice creation and payment, affecting your final settlement amount. Fix this by using forward contracts, accepting payments in the same currency you invoice in, or choosing platforms with FX hedging tools.

- Integration complexity: Not all platforms connect easily with your existing systems, which can delay go-live timelines by weeks. Test integrations with your software before finally committing to it.

- Multi-jurisdiction compliance: Compliance requirements vary by country, and what works for US clients won't work for EU clients. Choose platforms that handle multi-jurisdiction compliance automatically rather than requiring manual checks for each market.

- Payment failures and retry logic: Network issues, insufficient funds, or card declines can stop transactions even with automation. Look for platforms that retry failed payments automatically based on failure reasons and notify you immediately when manual action is needed.

- Settlement timing variations: Not all currencies settle at the same speed, with USD settling in 24 hours while less common currencies take 3-4 days. Ask platforms for currency-specific settlement timelines so you can manage cash flow expectations accurately.

The key is choosing a platform that handles these challenges upfront rather than discovering them after you've already integrated.

What are the Latest Trends in Cross-Border Payment Automation?

Cross-border payment automation continues to evolve rapidly. New technologies and regulatory changes are making international payments faster, cheaper, and more accessible. Here are the trends shaping the industry right now:

- Real-time payment network linkages: Countries are connecting their domestic instant payment systems across borders, enabling instant transfers that bypass traditional correspondent banking completely.

- AI-powered payment routing: Machine learning algorithms analyze thousands of data points to predict which payment path will succeed, increasing approval rates without manual intervention.

- Embedded finance integration: Payment automation is moving directly into business software like accounting systems and CRMs, so you can invoice and collect without leaving your existing workflow.

- Localized payment method expansion: Platforms are adding region-specific options like buy-now-pay-later, digital wallets, and local banking systems to match how customers in each market prefer to pay.

- Open banking adoption: Regulations requiring banks to share customer data are enabling account-to-account transfers that cost less than card payments and settle faster than traditional transfers.

- Transparent FX pricing: Regulatory pressure and competition are forcing platforms to show exact FX rates upfront with real-time displays and rate-lock guarantees becoming standard.

Tip: When evaluating platforms, ask about their technology roadmap and how often they add new payment methods or network connections. Platforms that innovate regularly will serve you better as your business grows into new markets.

How do You Choose the Right Payment Automation Platform?

Choosing the right platform depends on your business model, payment volumes, and growth plans. The wrong choice locks you into expensive contracts or forces workarounds when you scale. Here's what to evaluate:

Settlement Speed and Timing

If you need working capital quickly, look for platforms offering 24-hour settlements. Check if settlement timing varies by currency or payment method. Some platforms settle USD faster than EUR or GBP.

Fee Structure and Transparency

The platform should show exact costs upfront, including transaction fees, FX margins, and any additional charges. Avoid platforms with hidden markup or monthly fees unless your volume justifies the cost. Ask for sample invoices showing real fees on actual transactions.

Integration Capabilities

The platform must connect to your existing accounting software, CRM, or e-commerce system. API quality matters here. Good APIs mean seamless data flow. Poor APIs mean manual workarounds. Request API documentation before committing and check if webhook support exists for real-time updates.

Currency Support and Accounts

If most clients pay in USD and EUR, you need strong support for those currencies with competitive rates. Multi-currency accounts let you hold funds and reduce conversion frequency. Check if the platform provides local account details in target markets so clients can pay domestically.

Compliance and Documentation

For Indian businesses, automatic FIRC generation is essential. The platform should also handle international compliance requirements if you're dealing with regulated industries. Ask how long compliance documentation takes to generate after settlement.

Payment Method Variety

Can customers pay via cards, bank transfers, and local payment methods? More options mean higher success rates and better customer experience. Check which specific payment methods are available in your target markets.

Support Quality and Account Management

When a payment fails or a client has questions, you need responsive support. Check if the platform offers dedicated account management or just email support. Test response times during the sales process as an indicator of post-sale support quality.

The right platform fits your specific workflow without forcing you to change how you operate.

Speed Up Your Global Payment Processes with PayGlocal

Manual cross-border payments create bottlenecks that slow down your business. You wait days for settlements, spend hours on reconciliation, and lose money to hidden fees. If you're growing internationally, you need a system built for automation from the ground up.

PayGlocal gives you a complete payment automation platform built for cross-border commerce. You get local accounts in major currencies, automated compliance, and real-time tracking with seamless integration options for your existing systems. Here's what you get:

- Multi-currency accounts: Collect payments in USD, GBP, EUR, and CAD with local account details. Your clients pay locally, you receive funds faster, and FX costs drop significantly.

- API integration: Connect PayGlocal to your existing systems through comprehensive APIs. Choose from server-to-server integration, e-commerce plugins for Shopify, WooCommerce, or no-code payment links that work without any technical setup.

- Dynamic checkout: Offer customers their preferred payment methods, including cards, bank transfers, and local options. This increases approval rates and reduces payment failures across all markets.

- One platform: Track all payments, view transaction status, download compliance documents, and manage user roles from a single dashboard. No switching between multiple systems or manual report generation.

- Recurring payments: Automate subscription billing and scheduled payments for SaaS businesses. The system handles retry logic, updates your records automatically, and validates card support during registration.

PayGlocal handles the complexity of cross-border payment automation so you can focus on growing your business. You get transparent pricing, instant notifications, and faster settlements with transparent pricing.

Final Thoughts

Cross-border payment automation takes the manual work out of international money movement. You get faster settlements, lower costs, and complete visibility into where your money is at all times.

The right platform connects to your existing systems, handles compliance automatically, and gives customers payment options they trust. This means fewer failed transactions, less time spent on reconciliation, and more predictable cash flow for your business.

Automation isn't optional anymore for businesses doing cross-border commerce. Your competitors are already using these systems to move faster and operate more efficiently. The longer you wait, the more manual work adds up and the harder it becomes to catch up.

Ready to collect globally and settle locally without the usual friction? Get started with PayGlocal today and see what automated cross-border payments can do for your business.