Digital payments have been growing rapidly in India, with 18,000 crore transactions happening just in 2024-25. In fact, there are around 1 billion debit cards in India, and 85% of all digital payments are UPI-based.**

But with this varied payment acceptance, it also becomes important to have the right platform that can effectively handle different payment methods. That’s where payment aggregators come in, becoming the preferred solution for businesses that want to accept multiple payment methods without all the complexity.

Find out how payment aggregators work, their benefits, and tips to choose the right one for your business.

Key Takeaways:

* Payment collection simplified: Payment aggregators collect and process payments from multiple sources through a single platform.

* Multiple benefits: Benefits include faster onboarding, multiple payment methods, and improved cash flow.

* Main payment aggregators types: There are two main types of payment aggregators, the bank aggregator, which offers lower fees for high volumes, and the third-party aggregator, which provides faster setup and better features.

* Global payment solution: PayGlocal provides global payment collection with multi-currency accounts and instant compliance documentation.

A payment aggregator is a third-party service provider that enables businesses to accept payments from customers through multiple payment methods using a single platform. Instead of setting up individual relationships with different banks and payment processors, businesses can use one aggregator to handle everything.

Payment aggregators work as intermediaries that collect payments from various sources, including credit cards, debit cards, UPI, net banking, and digital wallets, and then process and settle these funds to your business account.

Payment aggregators follow a straightforward process that happens within seconds of a customer initiating the payment. Here’s how they work:

Different aggregator types serve specific business needs and transaction requirements. Here's how the main types compare:

Both types handle the same core function but differ in their approach and target customers.

These are aggregation services provided directly by banks like HDFC, ICICI, or SBI. They use their existing banking infrastructure to offer payment processing services.

Best for: Established businesses with high transaction volumes who want direct bank relationships and potentially lower transaction costs after meeting volume thresholds.

Examples: HDFC PayZapp, ICICI Merchant Services

Independent companies that specialize in payment processing and offer more advanced features and integrations than bank aggregators.

Best for: Startups, SMBs, and businesses needing quick setup, advanced features, and better customer support.

Examples: PayGlocal, Razorpay, PayU

Payment aggregators solve multiple business challenges while improving your payment acceptance capabilities.

* Quick onboarding: Set up payment acceptance within days instead of the months required for direct bank relationships.

* Multiple payment options: Accept credit cards, debit cards, UPI, net banking, and wallets through a single integration.

* Reduced compliance burden: Aggregators handle PCI DSS (Payment Card Industry Data Security Standard) compliance and security requirements, reducing your regulatory overhead.

* Better cash flow: Faster settlements compared to traditional payment processing can improve your working capital.

* Detailed analytics: Real-time dashboards and transaction reports help you track performance and identify trends.

* Technical support: Dedicated support teams help resolve payment issues quickly, ensuring smooth operations.

* Sub-merchant accounts: Avoid the complexity and documentation required for individual merchant accounts with banks.

Payment aggregators and payment gateways serve different functions in the payment ecosystem. Here's how they compare:

The main difference lies in their scope of service. Payment gateways act as secure channels that transmit payment information between customers, merchants, and banks.

Payment aggregators provide a complete payment solution by combining gateway functionality with fund collection and settlement services. They maintain relationships with multiple banks and payment networks, allowing businesses to access these services without individual agreements.

For most businesses, a payment aggregator is the best choice because it handles both data transmission and fund settlement through a single service. This reduces complexity and speeds up the setup process significantly.

Selecting the right aggregator impacts your customer experience, costs, and operational efficiency. Here’s how to choose the right payment aggregator:

* Transaction fees: Compare percentage fees and fixed charges. Look for transparent pricing without hidden costs.

* Payment methods supported: Ensure they support the payment methods your customers prefer, such as UPI, cards, wallets, and BNPL (Buy Now Pay Later) options.

* Settlement timeframes: Check how quickly funds are transferred to your account. Daily settlements are better for cash flow.

* Geographic coverage: If you serve international customers, choose aggregators with global capabilities and multi-currency support.

* Integration complexity: Evaluate how easily their APIs (Application Programming Interfaces) integrate with your existing systems and e-commerce platforms.

* Customer support quality: Test their support responsiveness during onboarding - you'll need reliable help when issues arise.

* Compliance and security: Verify they're PCI DSS compliant and follow local regulations.

Most payment aggregators work well for domestic transactions, but international payments require specialized capabilities that traditional aggregators often lack.

If you're collecting payments from international clients or customers, you need more than basic aggregation. You need a global payment infrastructure that handles multiple currencies, compliance requirements, and different payment preferences across various markets. That’s where PayGlocal comes in. Here’s how PayGlocal can help you:

* Multi-currency accounts: Accept payments in USD, GBP, EUR, CAD and 33+ other currencies without currency conversion hassles.

* Global payment methods: Support 40+ local payment methods preferred by customers worldwide, increasing your acceptance rates.

* Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) documents automatically upon settlement, removing manual paperwork for export compliance.

* Transparent pricing: No hidden fees, setup costs, or annual charges. Pay only when you transact.

* One platform management: Handle all your international payments, settlements, and reporting from a single dashboard.

Whether you're a freelancer receiving payments from global clients or a SaaS company scaling internationally, PayGlocal simplifies international payments while ensuring compliance and competitive rates.

Payment aggregators have changed how businesses accept payments by removing the complexity of multiple banking relationships and providing unified payment acceptance. They're particularly valuable for startups and businesses that need quick setup and multiple payment options.

For businesses with international transactions, solutions like PayGlocal become essential for handling multi-currency payments and compliance requirements while maintaining fast and secure payment processing.

Companies that choose the right payment infrastructure early save time and money while providing better customer experiences. Get started with PayGlocal today and join several businesses already collecting payments from 180+ countries with zero setup fees.

But with this varied payment acceptance, it also becomes important to have the right platform that can effectively handle different payment methods. That’s where payment aggregators come in, becoming the preferred solution for businesses that want to accept multiple payment methods without all the complexity.

Find out how payment aggregators work, their benefits, and tips to choose the right one for your business.

Key Takeaways:

* Payment collection simplified: Payment aggregators collect and process payments from multiple sources through a single platform.

* Multiple benefits: Benefits include faster onboarding, multiple payment methods, and improved cash flow.

* Main payment aggregators types: There are two main types of payment aggregators, the bank aggregator, which offers lower fees for high volumes, and the third-party aggregator, which provides faster setup and better features.

* Global payment solution: PayGlocal provides global payment collection with multi-currency accounts and instant compliance documentation.

What is a payment aggregator?

A payment aggregator is a third-party service provider that enables businesses to accept payments from customers through multiple payment methods using a single platform. Instead of setting up individual relationships with different banks and payment processors, businesses can use one aggregator to handle everything.

Payment aggregators work as intermediaries that collect payments from various sources, including credit cards, debit cards, UPI, net banking, and digital wallets, and then process and settle these funds to your business account.

How do payment aggregators work?

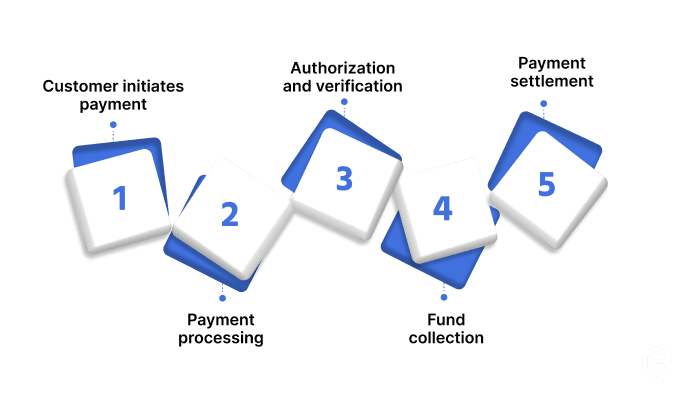

Payment aggregators follow a straightforward process that happens within seconds of a customer initiating the payment. Here’s how they work:

- Customer initiates payment: When someone makes a purchase, they're redirected to the aggregator's payment page, where they can choose from available payment methods.

- Payment processing: The aggregator securely captures payment details and routes the transaction to the appropriate payment network (Visa, Mastercard, UPI, etc.).

- Authorization and verification: Banks and payment networks verify the transaction details and either approve or decline the payment based on available funds and security checks.

- Fund collection: Once approved, the aggregator collects funds from the customer's bank or payment source.

- Payment settlement: The aggregator consolidates funds from multiple transactions and transfers the net amount to your business account, typically within 1-3 business days.

What are the different types of payment aggregators?

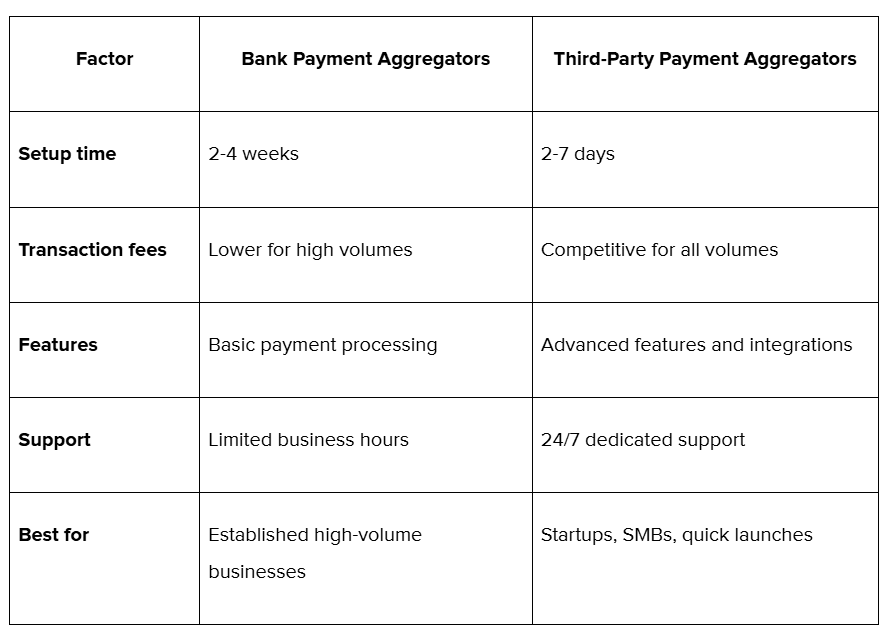

Different aggregator types serve specific business needs and transaction requirements. Here's how the main types compare:

Both types handle the same core function but differ in their approach and target customers.

- Bank payment aggregators

These are aggregation services provided directly by banks like HDFC, ICICI, or SBI. They use their existing banking infrastructure to offer payment processing services.

Best for: Established businesses with high transaction volumes who want direct bank relationships and potentially lower transaction costs after meeting volume thresholds.

Examples: HDFC PayZapp, ICICI Merchant Services

- Third-party payment aggregators

Independent companies that specialize in payment processing and offer more advanced features and integrations than bank aggregators.

Best for: Startups, SMBs, and businesses needing quick setup, advanced features, and better customer support.

Examples: PayGlocal, Razorpay, PayU

What are the benefits of using payment aggregators?

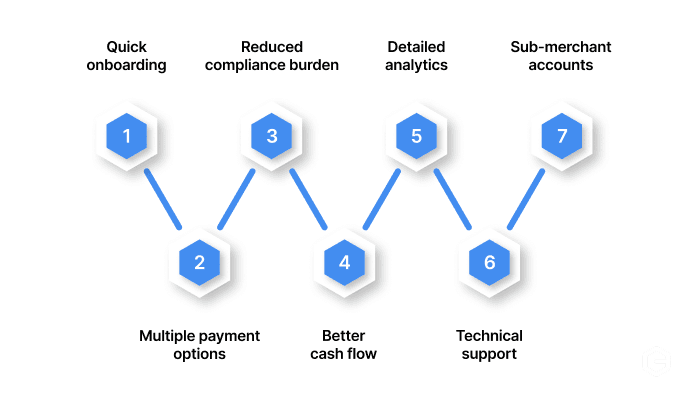

Payment aggregators solve multiple business challenges while improving your payment acceptance capabilities.

* Quick onboarding: Set up payment acceptance within days instead of the months required for direct bank relationships.

* Multiple payment options: Accept credit cards, debit cards, UPI, net banking, and wallets through a single integration.

* Reduced compliance burden: Aggregators handle PCI DSS (Payment Card Industry Data Security Standard) compliance and security requirements, reducing your regulatory overhead.

* Better cash flow: Faster settlements compared to traditional payment processing can improve your working capital.

* Detailed analytics: Real-time dashboards and transaction reports help you track performance and identify trends.

* Technical support: Dedicated support teams help resolve payment issues quickly, ensuring smooth operations.

* Sub-merchant accounts: Avoid the complexity and documentation required for individual merchant accounts with banks.

What is the difference between a payment aggregator and a payment gateway?

Payment aggregators and payment gateways serve different functions in the payment ecosystem. Here's how they compare:

The main difference lies in their scope of service. Payment gateways act as secure channels that transmit payment information between customers, merchants, and banks.

Payment aggregators provide a complete payment solution by combining gateway functionality with fund collection and settlement services. They maintain relationships with multiple banks and payment networks, allowing businesses to access these services without individual agreements.

For most businesses, a payment aggregator is the best choice because it handles both data transmission and fund settlement through a single service. This reduces complexity and speeds up the setup process significantly.

How to choose the right payment aggregator for your business?

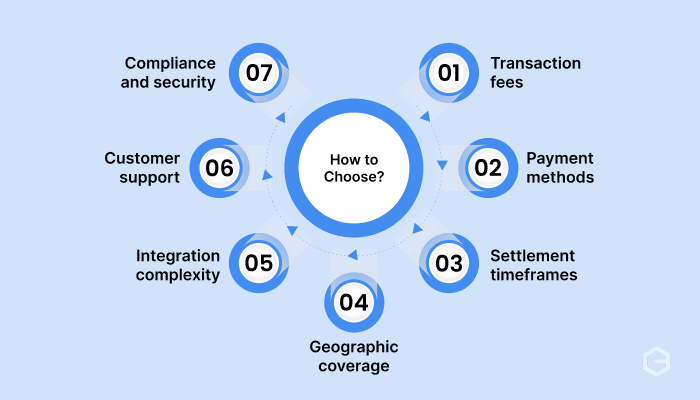

Selecting the right aggregator impacts your customer experience, costs, and operational efficiency. Here’s how to choose the right payment aggregator:

* Transaction fees: Compare percentage fees and fixed charges. Look for transparent pricing without hidden costs.

* Payment methods supported: Ensure they support the payment methods your customers prefer, such as UPI, cards, wallets, and BNPL (Buy Now Pay Later) options.

* Settlement timeframes: Check how quickly funds are transferred to your account. Daily settlements are better for cash flow.

* Geographic coverage: If you serve international customers, choose aggregators with global capabilities and multi-currency support.

* Integration complexity: Evaluate how easily their APIs (Application Programming Interfaces) integrate with your existing systems and e-commerce platforms.

* Customer support quality: Test their support responsiveness during onboarding - you'll need reliable help when issues arise.

* Compliance and security: Verify they're PCI DSS compliant and follow local regulations.

Get paid globally and scale your business with PayGlocal

Most payment aggregators work well for domestic transactions, but international payments require specialized capabilities that traditional aggregators often lack.

If you're collecting payments from international clients or customers, you need more than basic aggregation. You need a global payment infrastructure that handles multiple currencies, compliance requirements, and different payment preferences across various markets. That’s where PayGlocal comes in. Here’s how PayGlocal can help you:

* Multi-currency accounts: Accept payments in USD, GBP, EUR, CAD and 33+ other currencies without currency conversion hassles.

* Global payment methods: Support 40+ local payment methods preferred by customers worldwide, increasing your acceptance rates.

* Instant compliance documentation: Receive FIRC (Foreign Inward Remittance Certificate) documents automatically upon settlement, removing manual paperwork for export compliance.

* Transparent pricing: No hidden fees, setup costs, or annual charges. Pay only when you transact.

* One platform management: Handle all your international payments, settlements, and reporting from a single dashboard.

Whether you're a freelancer receiving payments from global clients or a SaaS company scaling internationally, PayGlocal simplifies international payments while ensuring compliance and competitive rates.

Final thoughts

Payment aggregators have changed how businesses accept payments by removing the complexity of multiple banking relationships and providing unified payment acceptance. They're particularly valuable for startups and businesses that need quick setup and multiple payment options.

For businesses with international transactions, solutions like PayGlocal become essential for handling multi-currency payments and compliance requirements while maintaining fast and secure payment processing.

Companies that choose the right payment infrastructure early save time and money while providing better customer experiences. Get started with PayGlocal today and join several businesses already collecting payments from 180+ countries with zero setup fees.