You're ready to grow your business in the US market. Your product is solid, your pricing is competitive, but there's one critical piece missing: accepting payments the way US customers prefer to pay.

The US market offers immense opportunities for global businesses, but choosing the wrong payment methods can cost you sales. US consumers have strong preferences for how they pay, and if you don't offer their preferred options, they'll simply go elsewhere. In 2024, US consumers made an average of 48 payments per month across various methods, with credit cards leading at 35% of all transactions.

In this guide, we cover everything you need to know about payment methods in the USA, from the most popular options to how each one works and which ones your business should accept. So, let’s get into it.

Payment methods in the USA include various ways consumers can transfer money to businesses when making purchases or paying bills. These range from physical options like cash and checks to electronic methods such as credit cards, debit cards, digital wallets, and bank transfers.

The US payment system includes traditional payment instruments that have existed for decades alongside newer digital options. Credit cards and debit cards currently dominate consumer transactions, together accounting for 65% of all payments.

Digital payment methods through mobile phones and apps have grown rapidly, now representing 23% of transactions as consumers shift toward contactless and remote payment options.

Payment methods directly affect whether customers complete their purchases and how satisfied they feel with your business. The right payment options remove friction from checkout, while missing payment methods create barriers that send customers to competitors.

Here's why payment methods are critical for your business:

The US payments system includes both traditional and digital options, each serving different customer needs and transaction types. Credit cards, debit cards, and digital wallets dominate, but knowing when and why consumers choose each method helps you prioritize which ones to accept.

Here's how the major payment methods compare across key factors:

Let's break down each payment method in detail.

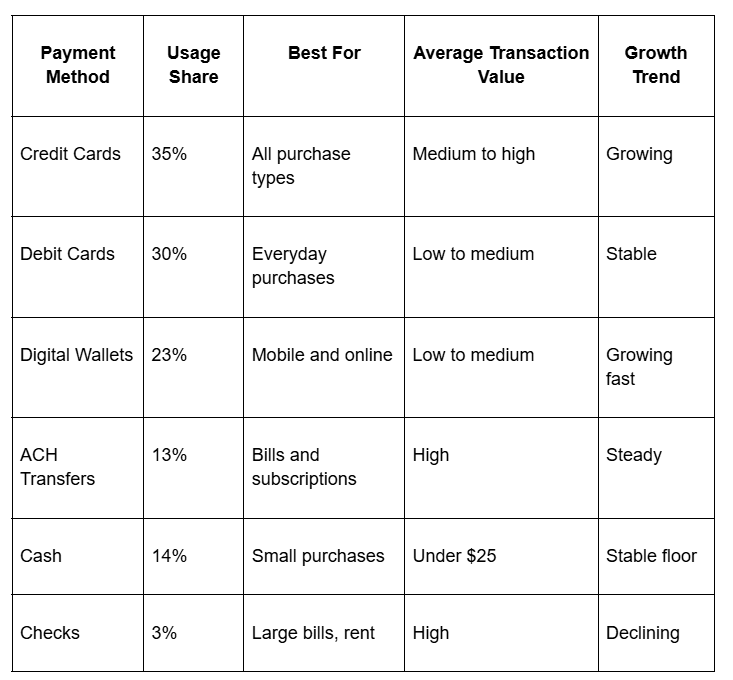

Credit cards remain the most popular payment method in the USA, used for 35% of all transactions in 2024. Major networks like Visa, Mastercard, American Express, and Discover are accepted almost everywhere, from small retailers to large e-commerce platforms.

US consumers prefer credit cards because they offer rewards programs, security, and the ability to pay over time. For businesses, credit cards provide faster settlement than checks and reduce the risk of non-payment, since the card network guarantees the transaction.

For example, a US customer buying a $500 software subscription will likely use a credit card to earn cashback or travel points, while also benefiting from extended warranty protection that many credit cards offer.

Debit cards account for 30% of US payments and are preferred for everyday purchases where consumers want to spend money they already have. Unlike credit cards, debit cards pull funds directly from a bank account, making them popular for budget-conscious consumers.

The usage pattern is consistent across age groups, with debit cards commonly used at grocery stores, gas stations, and fast-food restaurants. For instance, someone buying a $15 lunch will often swipe their debit card for quick payment without worrying about accumulating credit card debt.

Businesses benefit from accepting debit cards because the transaction fees are typically lower than credit card fees.

Digital wallets like PayPal, Apple Pay, Google Pay, and Venmo are commonly used in the US. These payment methods are especially popular among younger consumers. Data shows that adults aged 18-24 use mobile phones for 45% of all their payments.

Digital wallets work by storing card information securely on a device or in an app, allowing users to pay with a tap or click. They're used for both in-person payments at retail stores and online purchases.

For example, a customer checking out on your website can complete their purchase in seconds using Apple Pay instead of manually entering card details.

Automated Clearing House (ACH) transfers represent 13% of US payments and are commonly used for bill payments, subscriptions, and business-to-business transactions. ACH payments move money directly between bank accounts electronically.

Consumers use ACH for recurring payments like utility bills, mortgage payments, and subscription services because it's convenient to set up automatic withdrawals. For instance, a customer subscribing to your monthly service might authorize an ACH debit to automatically pay their $50 subscription fee each month.

For businesses, ACH transfers offer lower transaction fees compared to cards, though they take 1-2 business days to settle instead of the near-instant settlement of card payments.

Buy Now Pay Later (BNPL) services like Afterpay, Affirm, and Klarna have gained traction in the US, particularly for higher-ticket items. These services split a purchase into multiple interest-free installments, making expensive items more accessible.

BNPL is most popular among younger demographics and for purchases ranging from $100 to $1,000. For example, a customer buying a $600 laptop might choose to pay $150 per month for four months instead of paying the full amount upfront.

While BNPL doesn't yet match the volume of traditional payment methods, it's growing rapidly and can increase conversion rates for businesses selling higher-priced products.

Cash accounts for 14% of US payments and remains the third most-used payment instrument. Cash is most commonly used for small-value purchases under $25, with 70% of all cash payments falling in this range. It's preferred at convenience stores, farmers' markets, and situations where consumers want privacy or where card minimums apply.

For instance, someone buying a $5 coffee at a local cafe might pay with cash for speed and simplicity. About 80% of US adults carry cash in their wallets at least occasionally, showing it remains a backup payment option even for regular card users.

Selecting which payment methods to accept depends on your target customers, average transaction value, and business model. You don't need to accept every possible payment type, but you should cover the methods your specific audience prefers.

Consider these factors when choosing:

For instance, if you're a SaaS company selling $50-200/month subscriptions to US businesses, you should definitely accept credit cards (for rewards), ACH transfers (for lower fees on recurring payments), and have a simple way for customers to update their payment information when cards expire.

Your minimum viable payment stack should include credit cards, debit cards, and at least one major digital wallet. This combination covers most of the US consumer payment preferences and ensures you don't lose sales due to limited payment options.

For e-commerce businesses: Accept Visa, Mastercard, American Express, and Discover credit and debit cards. Add PayPal for customers who prefer not to enter card details, and enable Apple Pay and Google Pay for mobile shoppers. If you sell items over $200, consider adding Affirm or Afterpay.

For B2B and SaaS: Prioritize credit card acceptance (many businesses use corporate cards for subscription expenses), and add ACH transfers as a lower-cost option for customers willing to pay via bank account. Make it easy to store payment methods for recurring billing.

For freelancers and service providers: Accept major credit and debit cards as your primary method. Consider adding PayPal since many US clients already have accounts and trust it for service payments.

For high-ticket items ($500+): Include BNPL services alongside cards, as consumers increasingly expect installment options for larger purchases. This can increase your average order value.

The key is starting with broad card acceptance and adding methods based on customer requests and cart abandonment data. Don't overcomplicate your checkout, but do ensure your most common customer can pay their preferred way.

Growing your business in the US market shouldn't mean dealing with complex payment integrations, high failure rates, or expensive international transaction fees. You need a payment partner that handles the technical complexity while you focus on serving customers.

PayGlocal gives you everything you need to accept payments from US customers and get paid in your local currency without the usual headaches.

Here's how PayGlocal helps:

PayGlocal supports all major US payment methods through a single integration, so you can focus on growing your business rather than payment infrastructure.

Payment methods in the USA span from traditional options like credit cards and checks to modern digital wallets and emerging BNPL services. The key takeaway is that US consumers use multiple payment methods depending on the situation, and your business needs to accept at least the core options to compete effectively.

Credit cards remain dominant at 35% of transactions, but debit cards and digital wallets are essential for capturing the full market. The rise of mobile payments, particularly among younger demographics, shows where the market is heading, even as cash maintains a stable floor for specific use cases.

Stop losing sales due to payment friction. US customers expect smooth checkouts with their preferred payment methods. Get started with PayGlocal today to accept all major US payment methods through one simple integration.

The US market offers immense opportunities for global businesses, but choosing the wrong payment methods can cost you sales. US consumers have strong preferences for how they pay, and if you don't offer their preferred options, they'll simply go elsewhere. In 2024, US consumers made an average of 48 payments per month across various methods, with credit cards leading at 35% of all transactions.

In this guide, we cover everything you need to know about payment methods in the USA, from the most popular options to how each one works and which ones your business should accept. So, let’s get into it.

Key takeaways

- Credit cards dominate: Credit cards account for 35% of all US payments, making them essential for any business targeting US customers.

- Multiple methods matter: US consumers use 6-7 different payment methods regularly, so accepting multiple options increases your conversion rates.

- Digital wallets are growing: 23% of all payments in the US now happen via mobile phones, with digital wallets like Apple Pay and PayPal leading adoption.

- Demographics drive preferences: Younger consumers (18-24) prefer mobile payments, while consumers 55+ use cash more frequently, accounting for 19% of their transactions.

- Payment orchestration matters: Having PayGlocal as your payment partner helps you accept all major US payment methods while handling compliance, security, and currency conversion automatically.

What are the payment methods in the USA?

Payment methods in the USA include various ways consumers can transfer money to businesses when making purchases or paying bills. These range from physical options like cash and checks to electronic methods such as credit cards, debit cards, digital wallets, and bank transfers.

The US payment system includes traditional payment instruments that have existed for decades alongside newer digital options. Credit cards and debit cards currently dominate consumer transactions, together accounting for 65% of all payments.

Digital payment methods through mobile phones and apps have grown rapidly, now representing 23% of transactions as consumers shift toward contactless and remote payment options.

Why do payment methods matter for your business?

Payment methods directly affect whether customers complete their purchases and how satisfied they feel with your business. The right payment options remove friction from checkout, while missing payment methods create barriers that send customers to competitors.

Here's why payment methods are critical for your business:

- Conversion impact: Offering preferred payment methods can significantly increase your checkout completion rates, turning more visitors into paying customers.

- Market access: Each payment method unlocks specific customer segments, with younger buyers favoring digital wallets and older consumers preferring traditional cards.

- Transaction success: Having multiple payment options reduces failed transactions when one method gets declined, ensuring you don't lose sales to preventable payment errors.

- Customer trust: Recognizable payment options like Visa, Mastercard, and PayPal build confidence that your business is legitimate and secure.

- Geographic reach: US customers expect local payment methods, and accepting them makes your international business feel local to American buyers.

- Competitive advantage: Businesses with more payment options appear more professional and customer-focused compared to those accepting only one or two methods.

What are the most popular payment methods in the USA?

The US payments system includes both traditional and digital options, each serving different customer needs and transaction types. Credit cards, debit cards, and digital wallets dominate, but knowing when and why consumers choose each method helps you prioritize which ones to accept.

Here's how the major payment methods compare across key factors:

Let's break down each payment method in detail.

Credit cards

Credit cards remain the most popular payment method in the USA, used for 35% of all transactions in 2024. Major networks like Visa, Mastercard, American Express, and Discover are accepted almost everywhere, from small retailers to large e-commerce platforms.

US consumers prefer credit cards because they offer rewards programs, security, and the ability to pay over time. For businesses, credit cards provide faster settlement than checks and reduce the risk of non-payment, since the card network guarantees the transaction.

For example, a US customer buying a $500 software subscription will likely use a credit card to earn cashback or travel points, while also benefiting from extended warranty protection that many credit cards offer.

Debit cards

Debit cards account for 30% of US payments and are preferred for everyday purchases where consumers want to spend money they already have. Unlike credit cards, debit cards pull funds directly from a bank account, making them popular for budget-conscious consumers.

The usage pattern is consistent across age groups, with debit cards commonly used at grocery stores, gas stations, and fast-food restaurants. For instance, someone buying a $15 lunch will often swipe their debit card for quick payment without worrying about accumulating credit card debt.

Businesses benefit from accepting debit cards because the transaction fees are typically lower than credit card fees.

Digital wallets

Digital wallets like PayPal, Apple Pay, Google Pay, and Venmo are commonly used in the US. These payment methods are especially popular among younger consumers. Data shows that adults aged 18-24 use mobile phones for 45% of all their payments.

Digital wallets work by storing card information securely on a device or in an app, allowing users to pay with a tap or click. They're used for both in-person payments at retail stores and online purchases.

For example, a customer checking out on your website can complete their purchase in seconds using Apple Pay instead of manually entering card details.

ACH transfers

Automated Clearing House (ACH) transfers represent 13% of US payments and are commonly used for bill payments, subscriptions, and business-to-business transactions. ACH payments move money directly between bank accounts electronically.

Consumers use ACH for recurring payments like utility bills, mortgage payments, and subscription services because it's convenient to set up automatic withdrawals. For instance, a customer subscribing to your monthly service might authorize an ACH debit to automatically pay their $50 subscription fee each month.

For businesses, ACH transfers offer lower transaction fees compared to cards, though they take 1-2 business days to settle instead of the near-instant settlement of card payments.

Buy now pay later services

Buy Now Pay Later (BNPL) services like Afterpay, Affirm, and Klarna have gained traction in the US, particularly for higher-ticket items. These services split a purchase into multiple interest-free installments, making expensive items more accessible.

BNPL is most popular among younger demographics and for purchases ranging from $100 to $1,000. For example, a customer buying a $600 laptop might choose to pay $150 per month for four months instead of paying the full amount upfront.

While BNPL doesn't yet match the volume of traditional payment methods, it's growing rapidly and can increase conversion rates for businesses selling higher-priced products.

Cash

Cash accounts for 14% of US payments and remains the third most-used payment instrument. Cash is most commonly used for small-value purchases under $25, with 70% of all cash payments falling in this range. It's preferred at convenience stores, farmers' markets, and situations where consumers want privacy or where card minimums apply.

For instance, someone buying a $5 coffee at a local cafe might pay with cash for speed and simplicity. About 80% of US adults carry cash in their wallets at least occasionally, showing it remains a backup payment option even for regular card users.

How to choose the right payment methods for your business?

Selecting which payment methods to accept depends on your target customers, average transaction value, and business model. You don't need to accept every possible payment type, but you should cover the methods your specific audience prefers.

Consider these factors when choosing:

- Customer demographics: If you target younger US consumers (18-34), prioritize digital wallets and BNPL options alongside cards. For customers 35+, focus on credit and debit cards with digital wallets as a secondary option.

- Transaction size: For purchases under $50, ensure you accept debit cards and digital wallets since these are popular for smaller transactions. For purchases over $100, credit cards and BNPL become more important as customers want rewards or payment flexibility.

- Business type: E-commerce businesses should accept cards, digital wallets, and consider BNPL for higher-ticket items. B2B businesses should prioritize ACH transfers for larger invoices alongside cards for smaller purchases.

- Mobile vs desktop traffic: If most customers shop on mobile devices, make sure your checkout supports Apple Pay, Google Pay, and has a mobile-optimized card entry form.

- Geographic considerations: While this guide focuses on the US market, check if your US customers might also prefer international wallets like PayPal that work globally.

- Payment success rates: Look for payment providers that optimize authorization rates, as poor payment infrastructure can cause 10-25% of valid transactions to fail unnecessarily.

For instance, if you're a SaaS company selling $50-200/month subscriptions to US businesses, you should definitely accept credit cards (for rewards), ACH transfers (for lower fees on recurring payments), and have a simple way for customers to update their payment information when cards expire.

What payment methods should you accept from US customers?

Your minimum viable payment stack should include credit cards, debit cards, and at least one major digital wallet. This combination covers most of the US consumer payment preferences and ensures you don't lose sales due to limited payment options.

For e-commerce businesses: Accept Visa, Mastercard, American Express, and Discover credit and debit cards. Add PayPal for customers who prefer not to enter card details, and enable Apple Pay and Google Pay for mobile shoppers. If you sell items over $200, consider adding Affirm or Afterpay.

For B2B and SaaS: Prioritize credit card acceptance (many businesses use corporate cards for subscription expenses), and add ACH transfers as a lower-cost option for customers willing to pay via bank account. Make it easy to store payment methods for recurring billing.

For freelancers and service providers: Accept major credit and debit cards as your primary method. Consider adding PayPal since many US clients already have accounts and trust it for service payments.

For high-ticket items ($500+): Include BNPL services alongside cards, as consumers increasingly expect installment options for larger purchases. This can increase your average order value.

The key is starting with broad card acceptance and adding methods based on customer requests and cart abandonment data. Don't overcomplicate your checkout, but do ensure your most common customer can pay their preferred way.

Accept payments from USA customers seamlessly with PayGlocal

Growing your business in the US market shouldn't mean dealing with complex payment integrations, high failure rates, or expensive international transaction fees. You need a payment partner that handles the technical complexity while you focus on serving customers.

PayGlocal gives you everything you need to accept payments from US customers and get paid in your local currency without the usual headaches.

Here's how PayGlocal helps:

- Card Payments: Accept all major US credit and debit cards with industry-leading success rates, reducing failed transactions and increasing revenue.

- Global Payment Methods: Offer 40+ local payment methods, including digital wallets like PayPal, Apple Pay, and Google Pay, through a single integration.

- Multi-Currency Accounts: Collect payments in USD, GBP, EUR, and CAD with local accounts, giving US customers a local payment experience while you receive INR settlements.

- Recurring Payments: Set up subscription billing with automatic retries and smart payment orchestration to reduce failed recurring charges.

- One Platform: Manage all payments, view transaction data, handle refunds, and download compliance documents from a single dashboard instead of juggling multiple systems.

PayGlocal supports all major US payment methods through a single integration, so you can focus on growing your business rather than payment infrastructure.

Final thoughts

Payment methods in the USA span from traditional options like credit cards and checks to modern digital wallets and emerging BNPL services. The key takeaway is that US consumers use multiple payment methods depending on the situation, and your business needs to accept at least the core options to compete effectively.

Credit cards remain dominant at 35% of transactions, but debit cards and digital wallets are essential for capturing the full market. The rise of mobile payments, particularly among younger demographics, shows where the market is heading, even as cash maintains a stable floor for specific use cases.

Stop losing sales due to payment friction. US customers expect smooth checkouts with their preferred payment methods. Get started with PayGlocal today to accept all major US payment methods through one simple integration.