Your checkout shows prices in INR. An international buyer sees an unfamiliar amount, hesitates, and closes the tab. That was a lost sale, not because of your product, but because of currency confusion. For global businesses in 2026, this friction is the fastest way to lose a customer.

Real-time multi-currency payments solve this by displaying prices in a buyer’s local currency and processing the transaction instantly. According to recent data, the global real-time payments market is growing at 34.30% annually and is expected to cross $498.99 billion by 2034. This growth proves that the wait-and-see approach to international billing is over; the world has moved toward instant, localized checkout.

This guide covers how real-time multi-currency payments work, the benefits they bring to your cash flow, and how to choose a provider that helps you scale without the traditional banking delays.

Real-time multi-currency payments let your customers pay in their own local currency, while you receive funds quickly without long settlement delays. The payment processes and confirms within seconds. Your checkout supports more than one currency, so buyers in different countries each see prices in the currency they know.

For instance, if you run a D2C brand in India and a customer in Germany buys from you, they see the price in euros. The payment processes instantly. You receive the equivalent in your currency after automatic conversion. This is different from traditional wire transfers that pass through multiple banks, take 2-5 business days, and add conversion fees at each step.

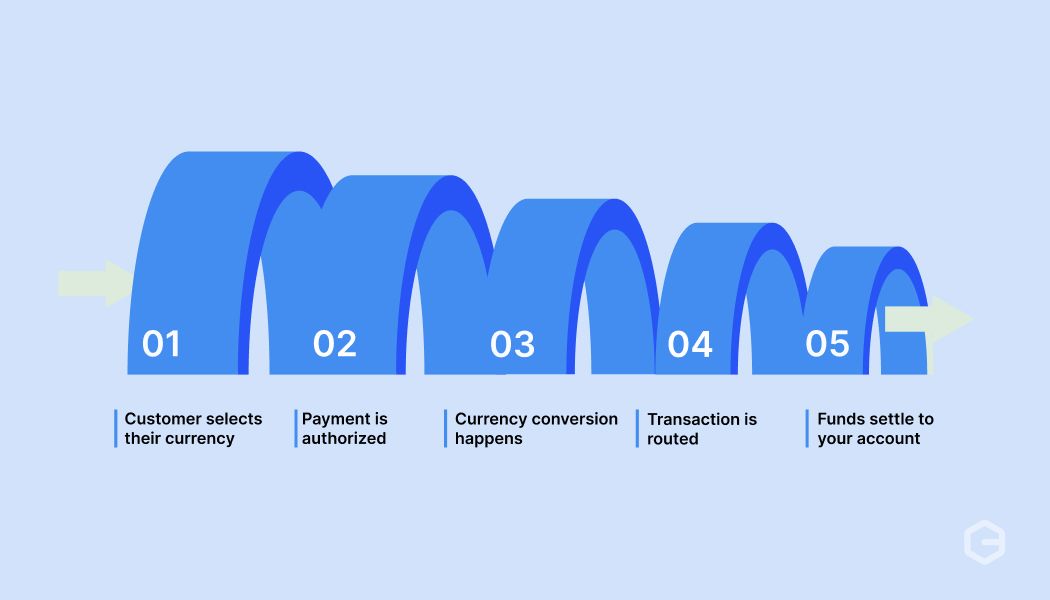

Every time a global customer checks out on your site, several steps happen in seconds behind the scenes. Each step involves currency conversion, network routing, and fraud checks working together. Here’s what the full transaction flow looks like:

1. Customer selects their currency: At checkout, the payment gateway pulls a live exchange rate and shows the price in the customer's local currency.

2. Payment is authorized: The customer pays with their card or a local payment method, and the gateway sends the transaction for approval.

3. Currency conversion happens: The gateway converts the amount from the customer's currency to your settlement currency at the rate locked at checkout.

4. Transaction is routed: Smart routing sends the payment through the network with the highest chance of approval based on location, method, and card type.

5. Funds settle to your account: Once approved, funds move to your account within seconds to minutes instead of days.

Tip: Ask your payment provider how they handle exchange rate locking. Some lock the rate at checkout, while others apply the rate at settlement. The difference can affect how much you actually receive.

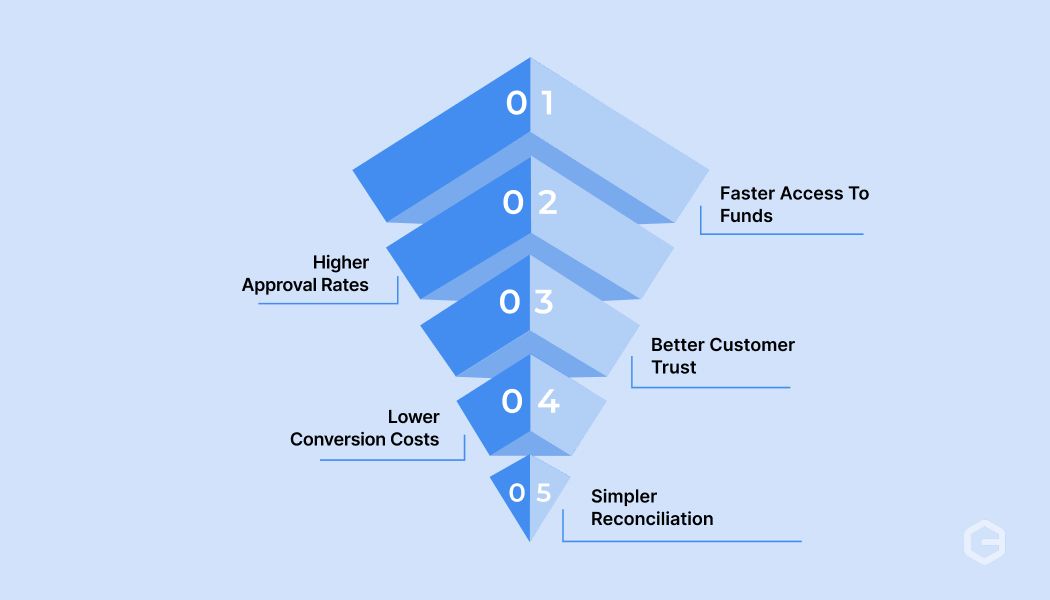

Accepting payments in local currencies with instant settlement changes how your business operates. From cash flow to customer trust, the impact shows up across your entire payment workflow. Here are some of the main benefits:

Note: Higher approval rates and lower drop-offs often have a bigger impact on revenue than saving on fees alone. Focus on both when evaluating providers.

Real-time multi-currency payments solve a lot of problems, but they come with a few things you should plan for. Knowing these upfront helps you avoid surprises once you go live. Here are the main challenges to watch for.

Most of these challenges come down to choosing the right provider. A good platform handles rate locking, unified reporting, and fraud screening out of the box, so you focus on growing your business instead of fixing payment issues.

Note: Ask providers specifically how they handle each of these challenges during your evaluation. The answers will tell you a lot about how much manual work you will need to do later.

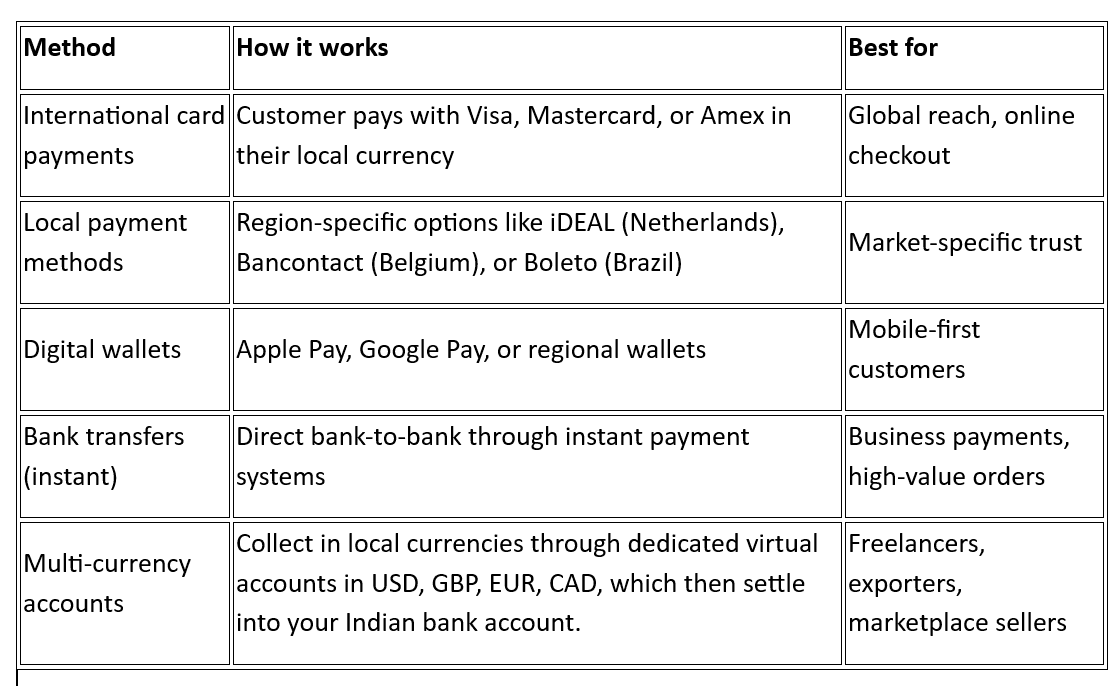

Your customers in different markets will pay differently. Cards dominate in some markets, while bank transfers or digital wallets lead in others. The right mix depends on where your buyers are located. Here’s a comparison of the most common methods:

Tip: Check which payment methods are most popular in your top 3-5 markets. Adding even one local option can noticeably improve your conversion rate in that region.

Real-time multi-currency payments are useful for any business selling across borders. Some business types see faster results than others. Here’s how it plays out for the most common use cases:

If you sell products online to global customers, your checkout experience directly affects sales. Showing prices in the customer's local currency and offering their preferred payment method reduces drop-offs.

For instance, an Indian fashion brand selling to UK customers can show prices in GBP, accept Apple Pay, and settle payments the same day. That means fewer abandoned carts and faster access to revenue.

Subscription businesses collect recurring payments across time zones and currencies. Failed renewals due to card declines or currency mismatches cost you revenue every month. Real-time multi-currency payments with built-in recurring billing keep your subscriber base stable.

For example, an Indian edtech company charging parents in the US and Canada can set up standing instructions in USD and CAD, so payments go through automatically each month.

If you provide services to international clients, getting paid should not take a week. Multi-currency accounts let you share local bank details with clients in the US, UK, or Europe.

They pay in their currency, and you receive funds without chasing wire transfers. This is especially useful for design, development, and consulting work where you invoice regularly.

Travel companies handle high-value bookings from customers across the world. A failed international payment at the booking stage means a lost customer. Real-time processing with smart fraud screening keeps approval rates high without adding friction to the booking flow.

For instance, a travel agency in India processing bookings from the Middle East and Europe needs both speed and security at checkout.

The common thing across all these use cases is that your customers expect to pay quickly, in their own currency, without extra steps. The businesses that make this easy are the ones that grow globally.

Tip: Start with the use case closest to your business. You do not need to activate every feature at once. Get your primary payment flow working first, then add recurring billing or local methods as you grow.

Your provider choice affects everything from approval rates to how much you pay per transaction. The wrong fit can mean hidden fees, failed payments, and a checkout experience your customers avoid. Here is what to look for:

Start with how many currencies and countries the provider supports. If you sell to customers in 10 countries, your provider needs to accept payments in all those local currencies. Coverage gaps mean lost sales.

Look for clear, upfront pricing with no hidden charges. Some providers add markup to exchange rates on top of their transaction fee. The best providers charge only when you transact, with no platform fees or setup costs.

Card payments alone are not enough. In many markets, customers prefer local methods over cards. Your provider should support the payment methods your customers actually use in their region.

Check how the provider connects to your existing website or platform. Good providers offer API integrations, plugins for platforms like Shopify and WooCommerce, and no-code options for quick setup.

Speed should not come at the cost of safety. Your provider should screen every transaction in real time for fraud, without blocking genuine customers.

You need clear visibility into every transaction. Look for a dashboard that shows payment status, settlement timelines, and downloadable compliance documents like the Foreign Inward Remittance Certificate (FIRC).

Tip: Before signing up, test the provider's checkout flow yourself. If it feels slow or confusing to you, it will feel the same to your customers.

Traditional international collections are often slowed down by hidden fees and manual reconciliation. PayGlocal removes this friction, offering a platform specifically designed for real-time multi-currency payments.

Here is how our features solve your global payment challenges:

PayGlocal helps businesses across travel, e-commerce, and SaaS move away from slow banking delays and start collecting global payments with total transparency and speed.

Real-time multi-currency payments give your business the speed, reach, and customer experience needed to compete globally. They reduce settlement delays, lower fees, and let your customers pay in the currency they trust.

The right provider makes all the difference. Look for broad currency coverage, transparent pricing, local payment methods, and a platform giving you full visibility into every transaction from checkout to settlement.

Several businesses are already collecting payments faster with advanced payment solutions like PayGlocal. The longer you wait, the more transactions you lose to slow checkouts and failed payments. Get started with PayGlocal today.

Real-time multi-currency payments solve this by displaying prices in a buyer’s local currency and processing the transaction instantly. According to recent data, the global real-time payments market is growing at 34.30% annually and is expected to cross $498.99 billion by 2034. This growth proves that the wait-and-see approach to international billing is over; the world has moved toward instant, localized checkout.

This guide covers how real-time multi-currency payments work, the benefits they bring to your cash flow, and how to choose a provider that helps you scale without the traditional banking delays.

Key takeaways

- Real-time multi-currency payments: They let you accept payments in your customers' local currency and settle them within seconds, not days.

- Cash flow and customer experience: Faster settlement improves cash flow, and local currency pricing builds trust and reduces cart drop-offs.

- Challenges to plan for: Exchange rate fluctuations, multi-currency reconciliation, and regional payment method differences need the right provider to manage.

- Choosing a provider matters: Look for currency coverage, transparent pricing, local payment method support, and easy integration.

- PayGlocal simplifies global payments: Businesses can collect in 33+ currencies from 180+ countries, with transparent pricing and no fixed fees.

What are real-time multi-currency payments?

Real-time multi-currency payments let your customers pay in their own local currency, while you receive funds quickly without long settlement delays. The payment processes and confirms within seconds. Your checkout supports more than one currency, so buyers in different countries each see prices in the currency they know.

For instance, if you run a D2C brand in India and a customer in Germany buys from you, they see the price in euros. The payment processes instantly. You receive the equivalent in your currency after automatic conversion. This is different from traditional wire transfers that pass through multiple banks, take 2-5 business days, and add conversion fees at each step.

How do real-time multi-currency payments work?

Every time a global customer checks out on your site, several steps happen in seconds behind the scenes. Each step involves currency conversion, network routing, and fraud checks working together. Here’s what the full transaction flow looks like:

1. Customer selects their currency: At checkout, the payment gateway pulls a live exchange rate and shows the price in the customer's local currency.

2. Payment is authorized: The customer pays with their card or a local payment method, and the gateway sends the transaction for approval.

3. Currency conversion happens: The gateway converts the amount from the customer's currency to your settlement currency at the rate locked at checkout.

4. Transaction is routed: Smart routing sends the payment through the network with the highest chance of approval based on location, method, and card type.

5. Funds settle to your account: Once approved, funds move to your account within seconds to minutes instead of days.

Tip: Ask your payment provider how they handle exchange rate locking. Some lock the rate at checkout, while others apply the rate at settlement. The difference can affect how much you actually receive.

What are the benefits of real-time multi-currency payments?

Accepting payments in local currencies with instant settlement changes how your business operates. From cash flow to customer trust, the impact shows up across your entire payment workflow. Here are some of the main benefits:

- Faster access to funds: You get paid in seconds or minutes instead of waiting days for bank transfers to clear.

- Higher approval rates: When customers pay in their own currency through a familiar method, fewer transactions get declined.

- Better customer trust: Showing prices in a customer's local currency removes confusion and surprise charges on their bank statement.

- Lower conversion costs: Direct currency conversion at checkout with transparent rates costs less than going through multiple banks.

- Simpler reconciliation: One platform handling multi-currency transactions gives you a single view of all payments.

Note: Higher approval rates and lower drop-offs often have a bigger impact on revenue than saving on fees alone. Focus on both when evaluating providers.

What are the challenges of real-time multi-currency payments?

Real-time multi-currency payments solve a lot of problems, but they come with a few things you should plan for. Knowing these upfront helps you avoid surprises once you go live. Here are the main challenges to watch for.

- Exchange rate fluctuations: Currency values change constantly, so the rate at checkout can differ from the rate at settlement unless your provider locks it upfront.

- Reconciliation across currencies: Collecting in five or six currencies makes it harder to match each payment to the right order without a unified dashboard.

- Integration with your existing setup: Connecting a new payment provider to your website or accounting tool can need developer time, especially for custom workflows.

- Payment method differences by region: What works in Europe does not always work in Southeast Asia. You need to confirm your provider supports the methods your customers prefer in each market.

- Fraud screening without blocking real customers: Faster payments leave less time to catch fraud. If risk filters are too strict, they block genuine buyers. Too loose, and you take on chargebacks.

Most of these challenges come down to choosing the right provider. A good platform handles rate locking, unified reporting, and fraud screening out of the box, so you focus on growing your business instead of fixing payment issues.

Note: Ask providers specifically how they handle each of these challenges during your evaluation. The answers will tell you a lot about how much manual work you will need to do later.

What are the common methods for real-time multi-currency payments?

Your customers in different markets will pay differently. Cards dominate in some markets, while bank transfers or digital wallets lead in others. The right mix depends on where your buyers are located. Here’s a comparison of the most common methods:

Tip: Check which payment methods are most popular in your top 3-5 markets. Adding even one local option can noticeably improve your conversion rate in that region.

Who benefits the most from real-time multi-currency payments?

Real-time multi-currency payments are useful for any business selling across borders. Some business types see faster results than others. Here’s how it plays out for the most common use cases:

1. D2C brands and e-commerce exporters

If you sell products online to global customers, your checkout experience directly affects sales. Showing prices in the customer's local currency and offering their preferred payment method reduces drop-offs.

For instance, an Indian fashion brand selling to UK customers can show prices in GBP, accept Apple Pay, and settle payments the same day. That means fewer abandoned carts and faster access to revenue.

2. SaaS companies with global subscribers

Subscription businesses collect recurring payments across time zones and currencies. Failed renewals due to card declines or currency mismatches cost you revenue every month. Real-time multi-currency payments with built-in recurring billing keep your subscriber base stable.

For example, an Indian edtech company charging parents in the US and Canada can set up standing instructions in USD and CAD, so payments go through automatically each month.

3. Freelancers and service exporters

If you provide services to international clients, getting paid should not take a week. Multi-currency accounts let you share local bank details with clients in the US, UK, or Europe.

They pay in their currency, and you receive funds without chasing wire transfers. This is especially useful for design, development, and consulting work where you invoice regularly.

4. Travel and hospitality businesses

Travel companies handle high-value bookings from customers across the world. A failed international payment at the booking stage means a lost customer. Real-time processing with smart fraud screening keeps approval rates high without adding friction to the booking flow.

For instance, a travel agency in India processing bookings from the Middle East and Europe needs both speed and security at checkout.

The common thing across all these use cases is that your customers expect to pay quickly, in their own currency, without extra steps. The businesses that make this easy are the ones that grow globally.

Tip: Start with the use case closest to your business. You do not need to activate every feature at once. Get your primary payment flow working first, then add recurring billing or local methods as you grow.

How to choose the right provider for real-time multi-currency payments?

Your provider choice affects everything from approval rates to how much you pay per transaction. The wrong fit can mean hidden fees, failed payments, and a checkout experience your customers avoid. Here is what to look for:

1. Currency and country coverage

Start with how many currencies and countries the provider supports. If you sell to customers in 10 countries, your provider needs to accept payments in all those local currencies. Coverage gaps mean lost sales.

2. Transparent pricing and fees

Look for clear, upfront pricing with no hidden charges. Some providers add markup to exchange rates on top of their transaction fee. The best providers charge only when you transact, with no platform fees or setup costs.

3. Local payment method support

Card payments alone are not enough. In many markets, customers prefer local methods over cards. Your provider should support the payment methods your customers actually use in their region.

4. Integration and setup

Check how the provider connects to your existing website or platform. Good providers offer API integrations, plugins for platforms like Shopify and WooCommerce, and no-code options for quick setup.

5. Fraud protection and security

Speed should not come at the cost of safety. Your provider should screen every transaction in real time for fraud, without blocking genuine customers.

6. Reporting and tracking

You need clear visibility into every transaction. Look for a dashboard that shows payment status, settlement timelines, and downloadable compliance documents like the Foreign Inward Remittance Certificate (FIRC).

Tip: Before signing up, test the provider's checkout flow yourself. If it feels slow or confusing to you, it will feel the same to your customers.

Get paid globally and settle faster with PayGlocal

Traditional international collections are often slowed down by hidden fees and manual reconciliation. PayGlocal removes this friction, offering a platform specifically designed for real-time multi-currency payments.

Here is how our features solve your global payment challenges:

- Multi-currency accounts: Instead of forcing customers to pay in INR, you can collect locally in USD, GBP, EUR, and CAD, and globally in 33+ currencies. This removes the currency confusion that leads to abandoned carts.

- Dynamic checkout: Our checkout automatically displays prices in your customer's local currency. By processing these transactions in real-time, we ensure a smooth experience that feels local to every buyer, regardless of their location.

- Global payment methods: We support 40+ local payment methods. Whether it’s a credit card in the US or a local wallet in Europe, your customers can pay using the methods they trust, leading to higher authorization rates.

- Recurring payments: For SaaS and subscription businesses, we offer built-in support for recurring billing on international cards. This ensures your global revenue stays predictable without the need for manual follow-ups.

- One platform for everything: Manage your entire payment lifecycle, from real-time tracking of multi-currency transactions to downloading automated FIRC, from a single dashboard.

PayGlocal helps businesses across travel, e-commerce, and SaaS move away from slow banking delays and start collecting global payments with total transparency and speed.

Final thoughts

Real-time multi-currency payments give your business the speed, reach, and customer experience needed to compete globally. They reduce settlement delays, lower fees, and let your customers pay in the currency they trust.

The right provider makes all the difference. Look for broad currency coverage, transparent pricing, local payment methods, and a platform giving you full visibility into every transaction from checkout to settlement.

Several businesses are already collecting payments faster with advanced payment solutions like PayGlocal. The longer you wait, the more transactions you lose to slow checkouts and failed payments. Get started with PayGlocal today.